What Medicare Doesn’t Cover: Your 2026 Guide

Understanding the Gaps So You Can Plan Ahead

📋 What You’ll Learn in This Guide

Let’s talk about something that catches a lot of people off guard when they turn 65: Medicare doesn’t cover everything. I know – it seems like it should, right? You’ve been paying Medicare taxes your whole working life, and now that you’re eligible, you discover there are some pretty significant gaps.

Here’s the truth: Medicare is fantastic at covering the big stuff – hospital stays, doctor visits, preventive care. But there are some everyday health needs that Medicare simply doesn’t pay for. And if you’re not prepared for these gaps, they can really impact your budget in retirement.

I’ve been helping people navigate Medicare for 18 years, and one of the most common things I hear is: “I wish I had known about this before I enrolled.” That’s why I put this guide together – so you can go into Medicare with your eyes wide open and make smart decisions about filling those coverage gaps.

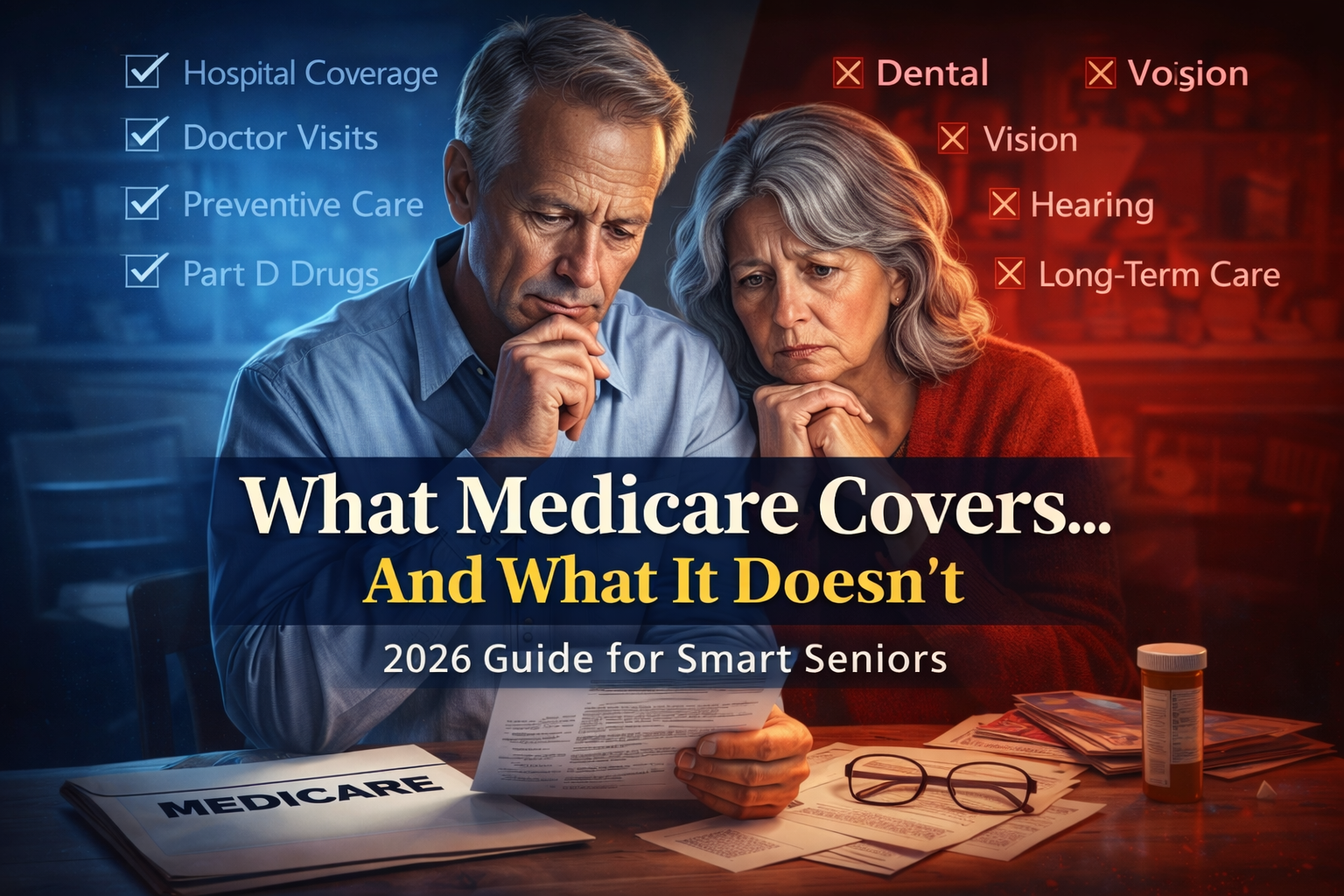

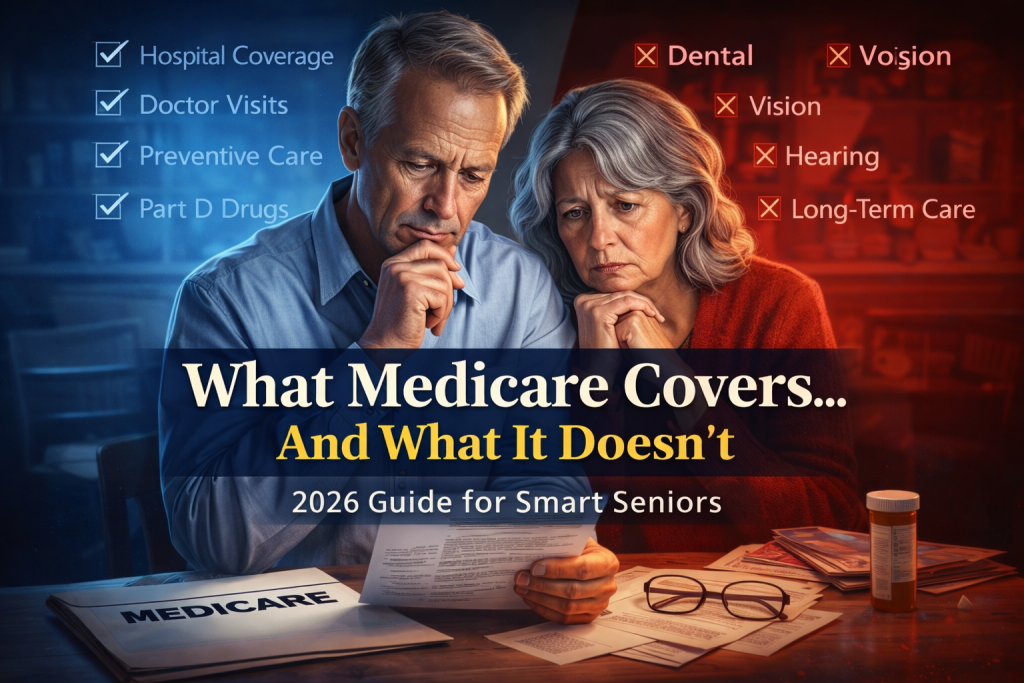

First, Let’s Talk About What Medicare DOES Cover

Before we dive into the gaps, it helps to understand what you’re actually getting with Original Medicare (Parts A and B). Think of it as knowing what’s in your toolbox before figuring out what tools you’re missing.

2026 Medicare Costs at a Glance

Part A Deductible

Part B Premium

Part B Deductible

Part B Coinsurance

What Medicare Part A Covers (Hospital Insurance)

Part A is your hospital coverage, and here’s the good news: if you or your spouse worked and paid Medicare taxes for at least 10 years, you don’t pay a monthly premium for Part A. It’s already paid for through those payroll taxes you’ve been contributing.

Part A Covers:

- Inpatient Hospital Stays: Your room (semi-private), meals, nursing care, and medical supplies. You’ll pay a $1,736 deductible per benefit period in 2026, and if you’re in the hospital longer than 60 days, daily coinsurance kicks in.

- Skilled Nursing Facility Care: Up to 100 days after a qualifying 3-day hospital stay. Days 1-20 are fully covered. Days 21-100, you pay $217 per day in 2026. Important: this is for skilled medical care, NOT custodial long-term care.

- Hospice Care: If you’re facing a terminal diagnosis with 6 months or less to live, Medicare covers pain management, medical equipment, medications, and even family counseling – usually with little to no cost to you.

- Home Health Services: Part-time skilled nursing, physical therapy, and medical social services when you’re homebound and your doctor says you need it.

What Medicare Part B Covers (Medical Insurance)

Part B is your outpatient coverage – doctor visits, preventive care, medical equipment. In 2026, you’ll pay $202.90 per month for Part B (higher if you’re a high earner). After you meet your $257 annual deductible, Medicare pays 80% of approved costs and you pay 20%.

Part B Covers:

- Doctor Visits: Primary care, specialists, emergency room visits – you’ll pay 20% coinsurance after your deductible

- Preventive Services: This is where Medicare really shines. Cancer screenings, flu shots, mammograms, colonoscopies, and your annual wellness visit are 100% covered when you use a provider who accepts Medicare assignment

- Diagnostic Tests: X-rays, MRIs, CT scans, lab work, EKGs – covered when medically necessary

- Durable Medical Equipment: Wheelchairs, walkers, hospital beds, oxygen equipment

- Mental Health Care: Outpatient therapy and counseling, same 20% coinsurance as other services

- Ambulance Services: Emergency transportation when your medical condition requires it

💡 Pro Tip: Preventive Care is Your Friend

Take full advantage of Medicare’s preventive services – they’re completely free when you use in-network providers. Annual wellness visits, cancer screenings, cardiovascular screenings, diabetes screenings – these catch problems early when they’re easier and cheaper to treat.

Now Here’s What Medicare DOESN’T Cover

Okay, now we get to the part that surprises people. Medicare is comprehensive, but it’s not complete. There are some pretty significant services that aren’t covered at all, and if you’re not prepared for this, you could face some hefty out-of-pocket costs.

Dental Care

Routine cleanings, fillings, dentures

Vision Care

Eye exams for glasses, eyeglasses, contacts

Hearing Aids

Hearing tests, hearing aids, fittings

Long-Term Care

Nursing homes, assisted living

Most Prescriptions

Medications you take at home

Foreign Travel

Healthcare outside the US

The Big Gaps: What Catches People by Surprise

Dental Services

What’s NOT Covered: Routine dental cleanings, fillings, crowns, dentures, tooth extractions, root canals – basically all the regular dental care you need.

Limited Exceptions: Medicare WILL cover dental care if it’s part of a covered medical procedure (like dental work needed before heart surgery) or if you have a jaw fracture that requires hospitalization.

What This Means for You: Budget for dental insurance or dental savings plans separately. Dental costs can add up fast in retirement – a routine cleaning might be $100-150, but if you need crowns or dentures, you’re looking at thousands of dollars.

Vision Care

What’s NOT Covered: Routine eye exams for glasses or contact lenses, the glasses or contacts themselves, LASIK surgery.

What IS Covered: Medicare covers eye exams and treatment for medical conditions like diabetic retinopathy, glaucoma screenings if you’re high-risk, and one pair of glasses or contacts after cataract surgery with an artificial lens.

What This Means for You: If you wear glasses or contacts, you’ll pay out-of-pocket for routine eye exams and new lenses. Plan on $100-300 annually for vision care.

Hearing Services

What’s NOT Covered: Hearing aids, routine hearing tests, hearing aid fittings and adjustments.

What IS Covered: Diagnostic hearing tests if your doctor orders them to check for a medical condition, medical treatment for ear infections, hearing-related surgeries.

What This Means for You: Hearing aids can cost $1,000-6,000 per ear. This is one of the biggest out-of-pocket expenses retirees face. Many people delay getting hearing aids because of the cost, but untreated hearing loss is linked to cognitive decline and social isolation.

Long-Term Care (The Really Big One)

What’s NOT Covered: This is huge and often misunderstood. Medicare does NOT cover long-term custodial care – help with daily activities like bathing, dressing, eating – whether at home, in assisted living, or in a nursing home.

What IS Covered: Medicare covers skilled nursing care for up to 100 days after a 3-day hospital stay, but only if you need skilled medical care or rehabilitation. Once you no longer need skilled care and just need help with daily living, Medicare stops paying.

What This Means for You: A private nursing home room costs an average of $108,000+ per year nationally. Without long-term care insurance or significant savings, this can devastate retirement finances. This is separate from Medicare planning, but it’s critical to think about.

Prescription Drugs (Under Original Medicare)

What’s NOT Covered: Original Medicare (Parts A & B) doesn’t cover most medications you take at home. This is a massive gap.

What IS Covered: Part B covers drugs administered in a medical setting – chemotherapy, injections during doctor visits, etc.

What This Means for You: You MUST get a Part D prescription drug plan or a Medicare Advantage plan with drug coverage. Don’t skip this! If you delay enrolling in Part D and don’t have other creditable coverage, you’ll pay a late enrollment penalty for life.

⚠️ The Part D Late Enrollment Penalty

If you don’t sign up for Part D when you’re first eligible and don’t have other creditable prescription coverage, you’ll pay a penalty. The penalty is calculated as 1% of the national base beneficiary premium ($35.63 in 2026) times the number of months you were late. This penalty is added to your premium FOREVER.

Example: If you’re 24 months late, that’s a $8.55/month penalty ($35.63 × 0.01 × 24 = $8.55) that you’ll pay every month for the rest of your life, on top of your regular Part D premium.

The Complete List: What Medicare Doesn’t Cover

| Category | What’s NOT Covered | Important Exceptions |

|---|---|---|

| Dental Care | Routine cleanings, fillings, crowns, dentures, extractions, root canals | Emergency dental for jaw fractures, pre-surgery dental work for certain procedures |

| Vision Care | Eye exams for glasses, eyeglasses, contact lenses, LASIK | Post-cataract surgery glasses, diabetic retinopathy exams, glaucoma screenings for high-risk |

| Hearing | Hearing aids, routine hearing tests, fittings | Diagnostic tests for medical conditions, ear infection treatment |

| Long-Term Care | Nursing home care, assisted living, custodial care (help with bathing, dressing, eating) | Skilled nursing for up to 100 days after 3-day hospital stay (Days 1-20 free, Days 21-100 cost $209.50/day) |

| Prescription Drugs | Medications you take at home under Original Medicare | Drugs given in doctor’s office, hospital, or clinic covered under Part B |

| International Care | Health services outside the United States | Emergency care if foreign hospital is closer than U.S. facility |

| Cosmetic Surgery | Face lifts, tummy tucks, liposuction, aesthetic procedures | Reconstructive surgery after mastectomy or accidents |

| Routine Foot Care | Nail trimming, corn/callus removal, most orthopedic shoes | Therapeutic shoes for diabetics, foot care for specific medical conditions |

| Alternative Medicine | Massage therapy, most acupuncture, naturopathic treatments | Acupuncture for chronic lower back pain (limited coverage) |

| Personal Comfort Items | Hospital TVs, private rooms (unless medically necessary), telephone | None – these are your responsibility |

What To Do About These Coverage Gaps

Okay, so now you know what Medicare doesn’t cover. The question is: what do you do about it? You’ve got several options, and the right choice depends on your health, your budget, and your priorities.

Your Action Plan for Filling Medicare Gaps

Consider Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurance companies and include everything Original Medicare covers PLUS often include prescription drug coverage (Part D), dental, vision, and hearing benefits. Many plans have $0 premiums (you still pay your Part B premium of $202.90/month).

The Tradeoff: You must use the plan’s network of doctors and hospitals, and you may need referrals to see specialists. But you get extra benefits and an out-of-pocket maximum that protects you from catastrophic costs.

Add a Medigap Supplement Plan

If you want to stick with Original Medicare, a Medigap supplement plan fills in the gaps – paying your deductibles, coinsurance, and copays. You can see any doctor who accepts Medicare nationwide, no networks, no referrals needed.

The Tradeoff: You’ll pay a monthly premium ($150-$480+ depending on plan and location), plus you’ll need a separate Part D plan for prescriptions. Medigap doesn’t cover dental, vision, or hearing – those gaps remain.

Don’t Forget Part D Prescription Coverage

If you choose Original Medicare + Medigap, you MUST add a standalone Part D plan. Don’t skip this even if you don’t take medications now – the late enrollment penalty applies for life if you delay.

2026 Part D Changes: Out-of-pocket costs are now capped at $2,100 annually (down from $3,300 in 2024), and insulin is capped at $35/month for Medicare beneficiaries.

Look Into Dental, Vision, and Hearing Coverage

Standalone dental and vision insurance plans are available, though they often have waiting periods and annual maximums. Some people find dental discount plans more cost-effective for routine care.

Many Medicare Advantage plans include these benefits – another reason to compare your options carefully.

Check If You Qualify for Financial Assistance

If you have limited income or resources, several programs can help:

- Medicare Savings Programs: Help pay Medicare premiums, deductibles, and coinsurance

- Extra Help (Low-Income Subsidy): Helps pay for Part D prescription drug coverage

- Medicaid: Can work alongside Medicare to cover gaps

Know Your Appeal Rights

If Medicare denies coverage for something you think should be covered, you have the right to appeal within 120 days. Get your doctor to provide documentation showing the service was medically necessary. Many denials are overturned on appeal.

Feeling Overwhelmed? You’re Not Alone.

Medicare decisions are complicated, and the stakes are high. One wrong choice could cost you thousands of dollars or leave you without coverage you need.

I’ve helped over 5,000 people navigate these exact decisions over the past 18 years. Let me review your specific situation and help you find coverage that actually fits your health needs and budget.

📞 Call (631) 358-5793 for a Free ReviewNo pressure, no obligation – just honest guidance from someone who’s been doing this since 2007.

The Bottom Line: Plan Ahead for the Gaps

Look, Medicare is an incredible program. It provides financial security for millions of Americans and covers the big, expensive stuff that could otherwise bankrupt you in retirement. But it’s not perfect, and it’s not complete.

The people who do best with Medicare are the ones who go in with realistic expectations. They know about the gaps, they’ve made a plan to fill them, and they’re not caught off guard when they need dental work or hearing aids.

💰 Quick Budget Reality Check

Here’s what the “gaps” might cost you annually if you don’t have supplemental coverage:

- Dental care: $300-1,500+ (cleanings, fillings, potential crown work)

- Vision care: $100-300 (eye exam, glasses or contacts)

- Hearing aids: $2,000-12,000 (if needed, typically lasts 5-7 years)

- 20% coinsurance on medical bills: Can add up to thousands without a cap

The right supplemental coverage can turn these unpredictable costs into a fixed, manageable monthly premium.

Your Medicare Coverage Checklist

✓ Make Sure You Have:

- Part A and Part B (or Medicare Advantage Part C)

- Part D prescription drug coverage (standalone or built into Advantage plan)

- Supplemental coverage for the gaps (Medigap or Medicare Advantage extras)

- A plan for dental, vision, and hearing costs

- Understanding of your out-of-pocket maximums and potential costs

Frequently Asked Questions

Let’s Find the Right Coverage for YOUR Situation

Every person’s health needs and budget are different. What works great for your neighbor might not be the best fit for you.

I’m Paul Barrett, and I’ve been specializing in Medicare for 18 years right here in New York. I represent 40+ insurance carriers with 200+ plan options, so I’m not tied to any one company – my job is to find what works best for YOU.

📞 (631) 358-5793Free Medicare Planning Session

No Pressure • No Obligation • Just Honest Answers

Serving clients across New York and 34+ states nationwide

About the Author: Paul Barrett is an independent Medicare insurance broker based in Huntington Station, NY. Since 2007, he’s helped over 5,000 clients navigate Medicare enrollment, comparing plans from 40+ carriers to find coverage that fits their specific needs and budget. Paul specializes in educational, no-pressure guidance for people new to Medicare.

This article is for educational purposes only and reflects 2026 Medicare costs and coverage rules. Individual situations vary – always consult with a licensed Medicare specialist for personalized advice.