IEP, GEP, SEP… if these Medicare acronyms feel like a confusing alphabet soup, you are not alone. The fear of missing a critical deadline and facing a lifelong penalty can turn this important milestone into a source of stress. Answering the simple question of when can you get Medicare often feels unnecessarily complex, leaving you worried about making a costly mistake. But it doesn’t have to be this way.

This guide is your path from confusion to confidence. We are here to provide the trusted, simple guidance you need to make the right choice at the right time. We’ll break down each enrollment period-in plain English-so you know your exact deadlines. You will learn what your options are if you plan to keep working past 65 and understand precisely when your new coverage will start. Our goal is to empower you with the clarity you need to enroll on time, avoid penalties, and begin your Medicare journey with complete peace of mind.

Key Takeaways

- Pinpoint your personal 7-month Initial Enrollment Period to ensure your coverage starts on time, penalty-free.

- Still working past 65? Discover if you can safely delay Medicare Part B without facing late enrollment penalties later on.

- Learn exactly when can you get medicare to avoid common mistakes that can lead to lifelong late enrollment penalties.

- Uncover how major life events can grant you a Special Enrollment Period and learn the separate timelines for adding crucial supplemental coverage.

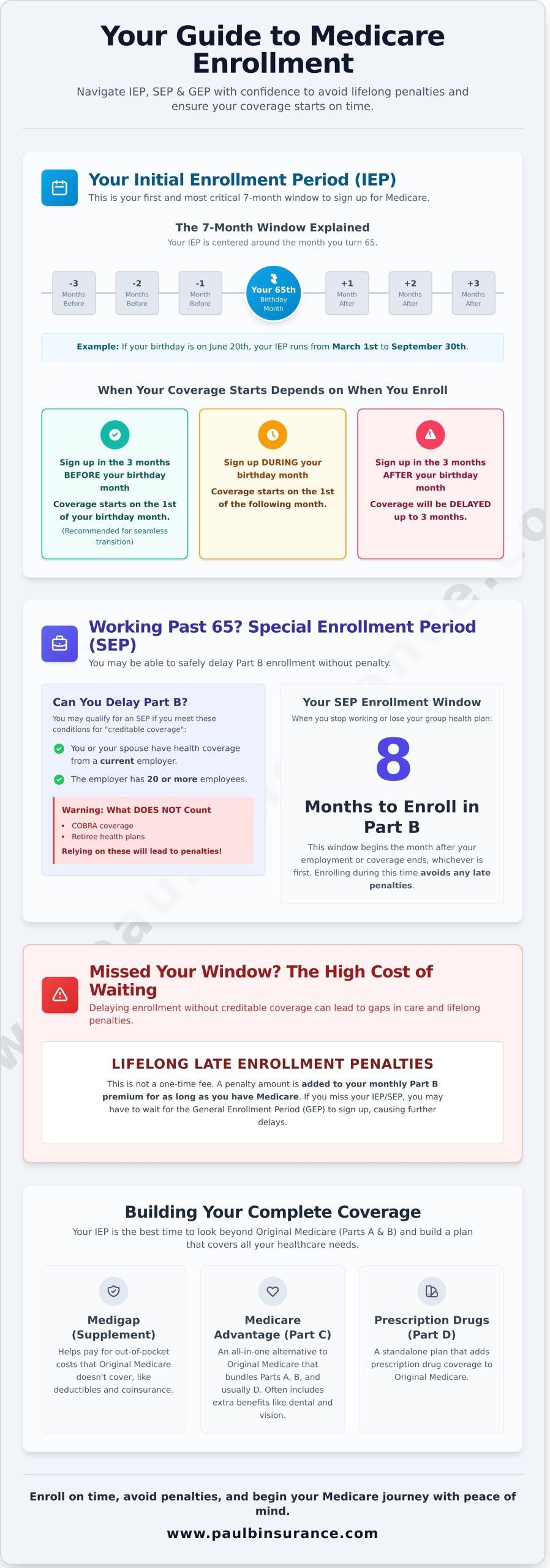

The Main Window: Your Initial Enrollment Period (IEP)

Understanding when can you get Medicare for the first time is one of the most important steps in your healthcare journey. Your Initial Enrollment Period (IEP) is your first, and most critical, opportunity to sign up. This personal 7-month window is designed for enrolling in Part A (Hospital Insurance) and Part B (Medical Insurance), which together form the foundation of the federal Medicare program. Getting this step right is essential, as missing your IEP without having other qualifying health coverage can lead to lifelong late enrollment penalties and delays in care.

The 7-Month Window Explained

Your IEP is centered around the month you turn 65. It is a straightforward, 7-month timeline that gives you ample time to make your decisions without feeling rushed. The window includes:

- The 3 months before your 65th birthday month

- The month you turn 65

- The 3 months after your 65th birthday month

For example: If your birthday is on June 20th, your IEP would start on March 1st and end on September 30th. This gives you a clear and generous timeframe to enroll with confidence.

When Your Coverage Starts: Timing is Everything

While you have seven months to enroll, when you sign up directly impacts when your coverage begins. Enrolling early is the best way to ensure there are no gaps between your previous insurance and Medicare. Here’s how it works:

- Sign up in the 3 months before your birthday month: Your coverage will start on the first day of your birthday month. This is the ideal scenario for a seamless transition.

- Sign up during your birthday month: Your coverage will start on the first day of the following month.

- Sign up in the 3 months after your birthday month: Your coverage will be delayed, starting two to three months after you enroll.

What to Do During Your IEP

Your IEP isn’t just about signing up for Parts A and B. It’s the perfect time to look at the bigger picture of your healthcare needs. Original Medicare doesn’t cover everything, so this is your chance to build a comprehensive plan. You should evaluate whether you need additional benefits like dental and vision, which are often included in a Medicare Advantage plan, or if you require coverage for prescriptions through a standalone Part D drug plan.

Still Working Past 65? Understanding the Special Enrollment Period (SEP)

One of the most common questions we hear is, “I’m still working and have good health insurance through my job. Do I really need to sign up for Medicare at 65?” For many people, the answer is no, you may not need to-at least not for Part B.

If you have health coverage from your (or your spouse’s) current employer, you may be able to delay enrolling in Medicare Part B without facing a late enrollment penalty down the road. This flexibility is a key part of understanding when you can get Medicare if your situation differs from the norm. The key is having what Medicare calls “creditable coverage.” In simple terms, this means your health plan comes from an active employer with 20 or more employees.

It’s crucial to know that not all coverage counts. COBRA and retiree health plans are not considered creditable coverage for the purpose of delaying Part B. Relying on them will likely result in lifetime penalties when you do eventually sign up.

How the Working Past 65 SEP Works

When you decide to retire or leave your job, you won’t have to wait for the General Enrollment Period. Instead, you’ll be granted a Special Enrollment Period (SEP). This gives you an 8-month window to sign up for Part B that begins the month after your employment or your group health plan coverage ends, whichever happens first. Enrolling during your SEP ensures you avoid the Part B late enrollment penalty. For example, if your last day of work is June 30, your 8-month SEP starts July 1.

Key Considerations Before Delaying Part B

Delaying Part B can be a smart financial move, but it requires careful thought. While most people sign up during their Initial Enrollment Period when they turn 65, your situation is unique. Before making a choice, be sure to:

- Compare the costs. How much are you paying for your employer plan versus what you would pay for the Part B premium plus a Medigap or Medicare Advantage plan?

- Talk to your HR department. Ask them how their plan works with Medicare. Some employer plans require you to sign up for Part A and B to provide full coverage once you turn 65.

- Understand Health Savings Accounts (HSAs). You cannot contribute to an HSA once you enroll in any part of Medicare, including Part A. This is a critical detail that is often overlooked.

Confused about your work coverage and how it fits with your Medicare options? The rules can be tricky, but you don’t have to figure it out alone. We can help you compare options.

Missed Your Window? The General Enrollment Period (GEP) & Late Penalties

It can be a sinking feeling to realize you’ve missed your Initial Enrollment Period. If you didn’t sign up for Medicare when you were first eligible and you don’t qualify for a Special Enrollment Period, don’t panic. There is a safety net, but it comes with important consequences you need to understand.

This safety net is the General Enrollment Period (GEP), which runs from January 1 to March 31 each year. While it provides another opportunity to enroll, there are two major drawbacks:

- A Gap in Coverage: Your Medicare coverage will not begin until July 1 of the year you enroll. This could leave you without health insurance for several months.

- Lifelong Penalties: Late enrollment almost always results in higher monthly premiums that you will pay for the rest of your life.

Understanding when can you get medicare is critical to avoiding these gaps and extra costs. These penalties are not meant to be punitive; they exist to encourage timely enrollment, which keeps the Medicare system stable for everyone. Let’s break down how they work.

Understanding the Part B Late Enrollment Penalty

The Part B penalty is the most common one people face. For each full 12-month period you were eligible for Part B but didn’t sign up, your monthly premium will increase by 10%. The worst part? This penalty isn’t a one-time fee-it’s added to your premium for as long as you have Part B. For example, if you waited two years to enroll, your premium would be 20% higher, forever. This is a costly mistake that trusted guidance helps you avoid completely.

What About the Part A Penalty?

The good news is that most people get Part A (Hospital Insurance) premium-free because they or their spouse worked and paid Medicare taxes for at least 10 years. However, if you have to buy Part A and you enroll late, you may face a penalty of a 10% higher premium. You would then have to pay this higher premium for twice the number of years you failed to sign up.

The Part D Penalty for Prescription Drug Coverage

Similar to Part B, there is a lifelong penalty for enrolling late in a Medicare Part D prescription drug plan. This penalty applies if you go for 63 consecutive days or more without creditable drug coverage after you’re first eligible. The cost is calculated based on how long you went without coverage and is added to your monthly Part D premium. Navigating all the official Medicare enrollment periods is key to preventing these unnecessary, lifelong costs.

Other Life Events: More Special Enrollment Periods (SEPs)

Life doesn’t always follow a neat calendar. What happens if you move, lose your job, or your plan changes mid-year? Many people worry they’re stuck with their coverage until the next Annual Enrollment Period. Fortunately, that’s not always the case. Medicare provides safety nets called Special Enrollment Periods (SEPs) for qualifying life events, giving you the flexibility to make changes when you need them most.

Understanding these opportunities is a key part of knowing when you can get Medicare coverage that truly fits your life, providing peace of mind no matter what changes come your way.

Common Qualifying Life Events

While there are many situations that can trigger an SEP, some of the most common ones include:

- Moving to a new address. If you move outside your current plan’s service area, you will typically get an SEP to enroll in a new plan available in your new location.

- Losing other health coverage. This includes losing group health coverage from an employer (yours or your spouse’s), or no longer being eligible for Medicaid.

- Your plan changes its contract. If your Medicare Advantage or Part D plan is ending its contract with Medicare, you will be granted an SEP to switch to a different plan.

- Opportunity for a 5-Star Plan. If a Medicare plan in your area with the highest quality rating (5 stars) is available, you may have a special, once-a-year opportunity to switch to it.

How to Use These SEPs with Confidence

Each Special Enrollment Period has its own set of rules and specific timing. For example, one SEP might give you 60 days to act, while another has a different window. The details matter, and navigating them alone can feel overwhelming, leading to missed deadlines or costly mistakes.

This is where trusted, unbiased guidance makes all the difference. Instead of trying to decipher complex government rules, you can work with an expert who knows the system inside and out. We help you confirm your eligibility and find the right plan for your new circumstances, ensuring you never feel rushed or pressured.

Had a life change? Find out if you qualify for an SEP today.

When to Sign Up for Additional Coverage (Medigap, Advantage, Part D)

Once you’re enrolled in Original Medicare (Parts A and B), you’ve built a strong foundation for your healthcare. However, it’s important to understand that it wasn’t designed to cover everything. You’ll still face out-of-pocket costs like deductibles, coinsurance, and prescription drug expenses. This is where supplemental coverage plays a critical role in protecting your financial well-being.

Navigating the enrollment periods for this extra coverage can feel just as confusing as figuring out when can you get Medicare in the first place. But getting the timing right is essential. Each type of plan-Medigap, Medicare Advantage, and Part D-has its own ideal sign-up window, and these are all connected to your Part A and Part B effective dates.

The Medigap Open Enrollment Period

This is, without a doubt, the single best time to buy a Medigap (Supplement) plan. This personal, six-month window begins on the first day of the month that you are both 65 or older and enrolled in Medicare Part B. During this protected period, you have “guaranteed issue rights.” This means an insurance company:

- Cannot deny you any Medigap policy it sells.

- Cannot charge you more because of pre-existing health conditions.

- Cannot make you wait for your coverage to start.

If you miss this one-time window, you may have to answer health questions to apply later and could be denied coverage.

Choosing a Medicare Advantage (Part C) or Part D Plan

Unlike Medigap, you can join, switch, or drop Medicare Advantage and Part D prescription drug plans during specific times each year. Your first opportunity is during your Initial Enrollment Period (IEP)-the same seven-month window you have when you first get Medicare.

After that, your main opportunity is the Annual Enrollment Period (AEP), which runs from October 15 to December 7 every year. This is your chance to review your current coverage and make changes for the upcoming year. Many people are drawn to Medicare Advantage plans because they often bundle medical and drug coverage into one plan and may include extra benefits like dental and vision coverage.

Understanding these deadlines is the key to avoiding coverage gaps and costly penalties. If you’re feeling overwhelmed, you are not alone. Our mission is to provide simple, trusted guidance to help you find the right fit with confidence. For unbiased advice, our team at The Modern Medicare Agency is here to help.

From Confusion to Confidence: Your Medicare Enrollment Plan

Navigating your Medicare enrollment doesn’t have to be stressful. The key takeaways are simple: your Initial Enrollment Period (IEP) is your primary window to sign up, but missing it can lead to lifelong penalties. Understanding if a Special Enrollment Period applies to your situation is crucial for avoiding gaps in coverage. Ultimately, knowing exactly when can you get medicare is the foundation of a secure healthcare future.

If you’re feeling overwhelmed by the dates and deadlines, you are not alone. That’s why we’re here. Our licensed agents in over 34 states provide the trusted, unbiased guidance you need, comparing plans from more than 40 top carriers to find your perfect fit. We use a proven 5-step process to replace confusion with absolute confidence in your decisions.

Don’t risk costly mistakes or sleepless nights. Take the next simple step toward peace of mind. Schedule a free, no-pressure call to get clear answers today.

Frequently Asked Questions About Medicare Enrollment

Do I have to sign up for Medicare Part B if I’m still working?

This is a common point of confusion, but the answer is usually no-if you have qualifying health coverage. If you work for a company with 20 or more employees and have health insurance through that job, you can typically delay Part B without a penalty. However, if your employer is smaller, you will likely need to enroll in Part B to avoid late fees. We can help you confirm your coverage is “creditable” and make the right choice with confidence.

What’s the difference between the Initial Enrollment Period (IEP) and the Annual Enrollment Period (AEP)?

Your Initial Enrollment Period (IEP) is your personal, 7-month window to sign up for Medicare when you first become eligible, usually around your 65th birthday. The Annual Enrollment Period (AEP), which runs from October 15 to December 7 each year, is for people who are already on Medicare. During AEP, you can switch your Medicare Advantage or Part D prescription drug plan. Think of IEP as your first chance to join and AEP as your yearly chance to make changes.

Can I sign up for Medicare online?

Yes, you absolutely can. The simplest way to enroll in Original Medicare (Part A and Part B) is through the Social Security Administration’s official website. The online application is secure and typically takes less than 30 minutes to complete. This is often the fastest and most convenient method, allowing you to avoid trips to a local office. Once you have your Medicare number, we can help you navigate the next steps for your supplemental coverage.

I’m under 65 but on disability. When can I get Medicare?

If you’re under 65, the question of when you can get Medicare depends on your disability benefits. Most people become eligible for Medicare after they have received Social Security Disability Insurance (SSDI) benefits for 24 months. This 24-month waiting period begins after your SSDI payments start. There are exceptions for those with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS), who may qualify for Medicare much sooner.

If I sign up on the last day of my enrollment period, when does my coverage start?

Your coverage start date depends on when you enroll during your 7-month Initial Enrollment Period. If you sign up in one of the last three months of your IEP, your coverage will be delayed. For example, enrolling in the final month of your period means your coverage won’t begin until the first day of the following month. To avoid any gaps in coverage, it is always best to sign up in the first three months of your eligibility window.

What happens if I miss my Medigap Open Enrollment Period?

Missing your Medigap Open Enrollment Period can have significant consequences. This one-time, 6-month window is your guaranteed right to buy any Medigap policy sold in your state, regardless of your health. If you miss it, insurance companies can use medical underwriting to decide whether to accept your application. This could result in higher premiums or even being denied coverage altogether based on pre-existing conditions. It’s a critical deadline to protect your future healthcare options.