Navigating the maze of Medicare can feel overwhelming, leaving you with one big, stressful question: what is the best medicare plan that covers everything? You worry about unexpected medical bills, gaps in coverage for essentials like dental or vision, and being locked into a limited network of doctors. The fear of making a costly mistake is real, and the search for a simple, all-in-one solution that brings you peace of mind is completely understandable.

While the honest answer is that no single Medicare plan is designed to truly cover it all, you absolutely can achieve that comprehensive protection. In this guide, we will provide the simple, trusted guidance you need. We’ll demystify the different parts of Medicare and show you exactly how to combine plans to build the robust coverage you’re looking for-including medical, hospital, prescription drug, dental, and vision care. It’s time to move from confusion to confidence, knowing you are fully protected.

Key Takeaways

- Discover why no single Medicare plan covers 100% of everything and how to build a combination of plans for true peace of mind.

- Answering “what is the best medicare plan that covers everything” for you means choosing between two main paths: Original Medicare with supplements or an all-in-one Medicare Advantage plan.

- Learn the simple way to get coverage for routine dental, vision, and hearing care-benefits that Original Medicare does not include.

- Confidently compare the two primary coverage strategies to determine which one best fits your personal health needs, doctor preferences, and budget.

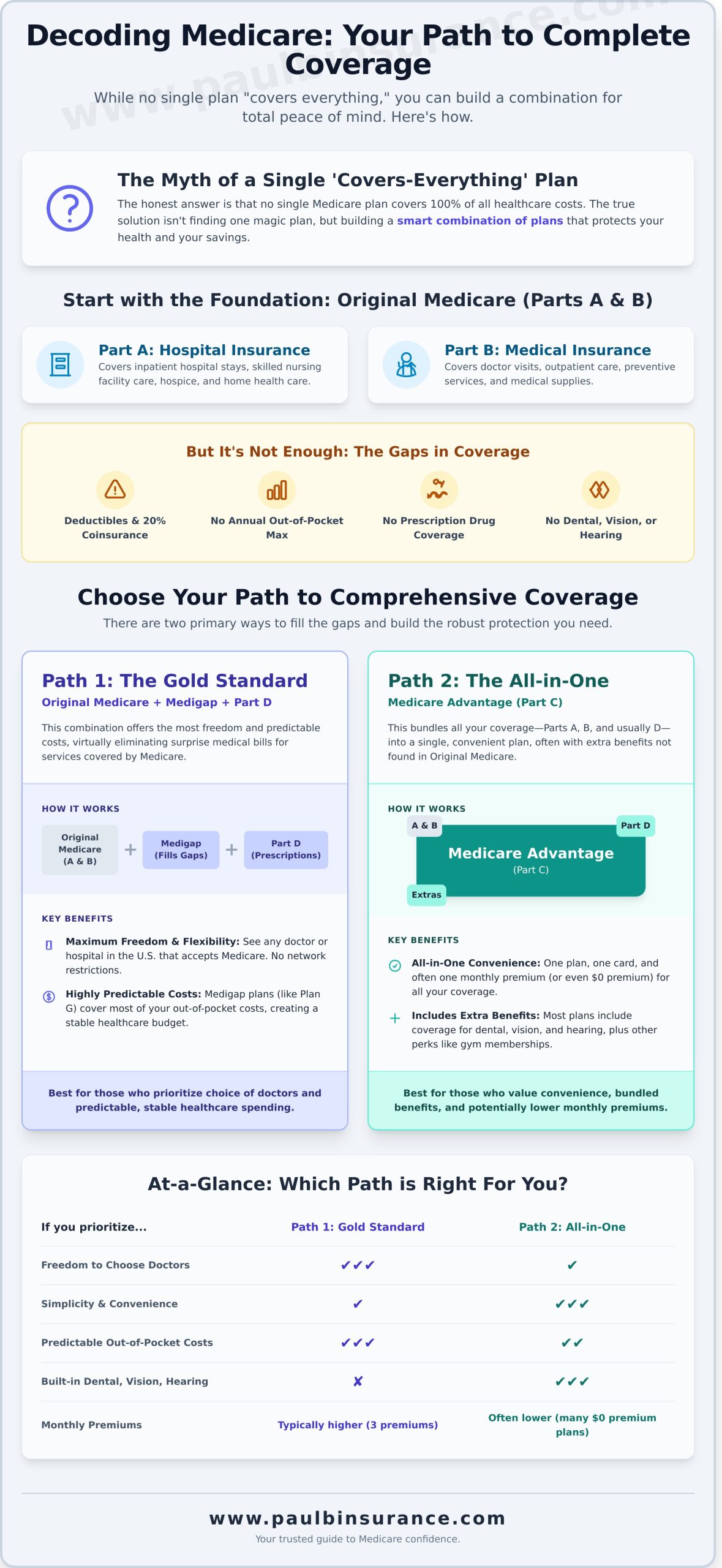

The Honest Answer: The Myth of a Single ‘Covers-Everything’ Medicare Plan

When you’re first exploring your options, it’s natural to ask, “what is the best medicare plan that covers everything?” It’s a question rooted in a desire for security and peace of mind. The simple, honest answer is that no single Medicare plan covers 100% of all healthcare costs with no out-of-pocket expenses.

But please, don’t let that discourage you. While there isn’t one “magic” plan, you absolutely can achieve nearly complete coverage. The goal isn’t to find a single plan, but to build a smart combination of plans that protects your health and your savings. This is where clarity replaces confusion. Essentially, you have two primary paths to build this comprehensive coverage:

- Path 1: Original Medicare (Part A & B) + a Medicare Supplement (Medigap) Plan + a Part D Prescription Drug Plan.

- Path 2: A Medicare Advantage Plan (Part C), which bundles Parts A, B, and often D, into one plan.

We will explore these paths in detail, but first, it’s crucial to understand why the government’s basic coverage isn’t enough on its own.

Why Original Medicare (Part A & B) Isn’t Enough

Think of Original Medicare as the strong foundation of your healthcare coverage. This is the federally administered program, Medicare (United States), that includes Part A (Hospital Insurance) and Part B (Medical Insurance). While essential, this foundation has significant gaps. Relying on it alone leaves you exposed to potentially unlimited out-of-pocket costs from deductibles, copayments, and a 20% coinsurance for most medical services with no annual cap. It also completely excludes coverage for prescription drugs, which can be a major expense.

Defining ‘Comprehensive Coverage’ in the World of Medicare

So, when you search for what is the best medicare plan that covers everything, what are you really looking for? For most people, “everything” means having robust protection for the major costs you might face, giving you confidence that a health issue won’t become a financial crisis. This typically includes:

- Hospital stays and inpatient care

- Doctor visits and outpatient services

- Prescription medications

- Preventive care and screenings

It also often includes those important “extras” like dental, vision, and hearing care. The following sections will guide you step-by-step on how to build a plan that covers these areas, moving you from confusion to confidence.

Path 1: The Gold Standard for Comprehensive Coverage (Original Medicare + Medigap + Part D)

For those seeking the most freedom and financial predictability in their healthcare, this three-part combination is often the ideal solution. It starts with Original Medicare (Part A for hospital and Part B for medical services), which is the foundational coverage provided by the government. As the official Medicare website explains, this is one of the two main ways to get your coverage. However, Original Medicare was never designed to cover 100% of your costs.

That’s where the other two parts come in to create an answer to the question, “what is the best medicare plan that covers everything?” The key benefit of this path is unparalleled freedom: you can see any doctor or visit any hospital in the U.S. that accepts Medicare, with no network restrictions or referral requirements to see a specialist. While the trade-off is typically paying three separate monthly premiums (for Part B, Medigap, and Part D), what you gain in return is incredible peace of mind and powerful protection from catastrophic medical bills.

How Medigap Plans Fill the Gaps

Think of a Medicare Supplement plan, also known as Medigap, as insurance that pays for the “gaps” Original Medicare doesn’t cover. It works directly with Part A and Part B to pay for your share of the costs, such as deductibles, copayments, and coinsurance. Popular options like Medigap Plan G are designed to cover nearly all of your out-of-pocket medical expenses after you’ve paid the small, annual Part B deductible. This powerful combination transforms your healthcare budget from unpredictable to highly stable, virtually eliminating surprise medical bills for services covered by Medicare. Learn more about Medicare Supplement (Medigap) Plans.

Adding Prescription Drug Coverage with Part D

A critical piece of this puzzle is prescription drug coverage. Original Medicare does not cover most medications you pick up from the pharmacy. To get this essential coverage and avoid lifelong late enrollment penalties, you must add a standalone Medicare Part D plan. This is a separate policy with its own monthly premium. Choosing the right Part D plan is crucial and should be based on the specific medications you take. Each plan has its own list of covered drugs (called a formulary) and pharmacy network, so matching the plan to your needs is the key to keeping your prescription costs low. Find the right Medicare Part D prescription plan for your needs.

Path 2: The ‘All-in-One’ Convenience of Medicare Advantage (Part C)

For many people, the search for what is the best medicare plan that covers everything leads them to a single, bundled option. This is the promise of Medicare Advantage, also known as Part C. Instead of getting your benefits from the government and adding separate policies, you can choose an all-in-one plan offered by a private insurance company that contracts with Medicare. These plans are incredibly popular for their convenience, low (and often $0) monthly premiums, and a host of extra benefits. However, it’s crucial to understand that this convenience comes with important trade-offs.

How Advantage Plans Aim to ‘Cover Everything’

When you enroll in a Medicare Advantage plan, a private insurer manages your health benefits on behalf of Medicare. These plans are required by law to cover everything that Original Medicare (Parts A and B) covers. To create a more complete package, most also bundle in prescription drug coverage (Part D) and other attractive perks that can make a real difference in your daily life. Common extra benefits include:

- Routine dental, vision, and hearing care

- Gym memberships and fitness programs (like SilverSneakers)

- Allowances for over-the-counter health products

- Transportation to medical appointments

A key feature that provides peace of mind is the annual out-of-pocket maximum. This is a yearly cap on what you’ll spend on medical services. Once you reach this limit, the plan pays 100% for covered services for the rest of the year-a critical safety net that Original Medicare doesn’t offer on its own. To explore these plans in more detail, you can read our complete Medicare Advantage Guide.

Understanding the Trade-Offs: Networks and Costs

The biggest trade-off for the low premiums and extra perks is the network structure. Most Advantage plans are HMOs or PPOs, meaning you must use doctors, specialists, and hospitals that are in the plan’s network to get the lowest costs. As explained in the official Social Security Administration guide to Medicare, these private plans manage your care differently than the original government program. While your monthly premium may be low, you pay for care as you use it through copayments, coinsurance, and deductibles. It is absolutely essential to check that your trusted providers are in-network before enrolling to avoid any stressful surprises down the road.

What About Dental, Vision, and Hearing? Covering the ‘Extras’

One of the most common points of confusion when searching for the right Medicare coverage is how to handle routine care for your teeth, eyes, and ears. It’s a critical question, so let’s clear it up: Original Medicare (Part A and Part B) does not cover routine dental, vision, or hearing services. This includes things like cleanings, fillings, eye exams for glasses, or hearing aids.

For many people, finding what is the best medicare plan that covers everything means finding a solution for these essential services. The good news is you have two primary paths to get the coverage you need, and we’re here to help you understand them without the confusing jargon.

Coverage within Medicare Advantage Plans

Many Medicare Advantage (Part C) plans bundle dental, vision, and hearing benefits to create an all-in-one package. These built-in “extras” are convenient, but it’s vital to understand their limitations. Often, the coverage is basic and may include:

- One or two dental cleanings per year.

- A small annual allowance for eyewear (e.g., $150-$200).

- A routine hearing exam and a limited benefit for hearing aids.

Always check the plan’s “Evidence of Coverage” document to see the exact details, as benefits and provider networks can be quite restrictive. The dentist you’ve seen for years might not even be in the plan’s separate dental network.

Standalone Dental and Vision Plans

For more comprehensive and predictable coverage, a standalone insurance plan is often the best choice. This is a separate policy you can buy whether you have Original Medicare with a Medigap plan or want to supplement the limited benefits in your Medicare Advantage plan.

These plans offer more robust benefits for a separate monthly premium, giving you higher annual maximums and coverage for major services like root canals, crowns, or dentures. They provide the peace of mind that a significant expense won’t be a surprise. To get the reliable care you deserve, you can explore your options for a dedicated dental insurance plan.

Navigating these choices can feel overwhelming, but you don’t have to do it alone. At The Modern Medicare Agency, we provide the simple, unbiased guidance you need to find a solution that truly fits your life.

So, Which Path Is Best for ‘Covering Everything’ For YOU?

After exploring all the options, the answer to the question, “what is the best medicare plan that covers everything?” isn’t a specific plan number-it’s a personal strategy. The right choice for your neighbor might not be the right choice for you. It all comes down to what you value most: predictable costs and total freedom, or lower premiums and bundled benefits.

To make it simple, here’s a side-by-side look at the two main paths to comprehensive coverage:

.medicare-table {

width: 100%;

border-collapse: collapse;

margin: 20px 0;

font-size: 1em;

font-family: sans-serif;

min-width: 400px;

box-shadow: 0 0 20px rgba(0, 0, 0, 0.15);

}

.medicare-table thead tr {

background-color: #005a9c;

color: #ffffff;

text-align: left;

}

.medicare-table th,

.medicare-table td {

padding: 12px 15px;

border-bottom: 1px solid #dddddd;

}

.medicare-table tbody tr:last-of-type {

border-bottom: 2px solid #005a9c;

}

.medicare-table tbody tr.active-row {

font-weight: bold;

color: #005a9c;

}

| Feature | Original Medicare + Medigap | Medicare Advantage (Part C) |

|---|---|---|

| Monthly Premiums | Higher, predictable monthly costs (for Medigap & Part D). | Low or often $0 monthly plan premium. |

| Doctor Choice | Freedom to see any doctor or specialist nationwide that accepts Medicare. No referrals needed. | Must use doctors and hospitals in the plan’s network (HMO or PPO). Referrals may be needed. |

| Out-of-Pocket Costs | Minimal to none for Medicare-covered services after premiums are paid. | Pay-as-you-go with copays and coinsurance for services, up to an annual maximum. |

| Extra Benefits | Requires a separate Part D plan for drugs. No built-in extras. | Often includes prescription drugs, dental, vision, and hearing benefits in one plan. |

Choose the Medigap Path If…

This path offers the ultimate peace of mind and predictability. It’s often the best choice if you prioritize stability and flexibility. You might prefer this route if:

- You want the freedom to see any doctor or specialist in the U.S. that accepts Medicare.

- You prefer a fixed monthly budget with virtually no surprise bills from the doctor’s office.

- You travel frequently or are a “snowbird” who lives in different states throughout the year.

Choose the Medicare Advantage Path If…

This path provides an affordable, all-in-one solution that works perfectly for many people. It could be the right fit for you if:

- You prefer a low or $0 monthly premium and are comfortable with a pay-as-you-go system of copays.

- Your trusted doctors, specialists, and hospitals are already in the plan’s network.

- You value the convenience of having medical, prescription, and extra benefits like dental and vision bundled into a single plan.

You Don’t Have to Decide Alone

Feeling like this is still a complex and overwhelming decision? You are not alone. Choosing your Medicare path is one of the most important healthcare decisions you’ll make, and you deserve to get it right without stress or confusion.

This is where trusted, unbiased guidance makes all the difference. An independent broker works for you, not for a single insurance company. Our mission is to help you understand your options clearly, compare every plan available in your area, and find what is the best Medicare plan that covers everything for you. We are here to move you from confusion to confidence, ensuring you make a choice that protects your health and your budget for years to come.

If you’re ready for clear answers and a simple process, get in touch for a no-cost, no-obligation consultation today.

From Confusion to Confidence: Finding Your Best Medicare Path

As we’ve seen, the idea of a single Medicare plan that covers everything is a myth. The journey to comprehensive coverage involves a choice between two main paths: the flexibility of Original Medicare paired with a Medigap and Part D plan, or the all-in-one structure of a Medicare Advantage plan. The honest answer to what is the best medicare plan that covers everything depends entirely on your unique health needs, budget, and lifestyle.

Making that choice alone can feel overwhelming, but you don’t have to navigate this maze by yourself. As an independent broker representing over 40 carriers, The Modern Medicare Agency provides truly unbiased advice to clients in New York, California, and Florida. Our goal is simple: to offer personalized support that moves you from confusion to confidence, ensuring you find the right combination of coverage without the pressure.

Ready to find clarity and peace of mind? Schedule a free, no-obligation call with Paul to find your perfect Medicare coverage. You deserve to feel certain about your healthcare decisions, and we’re here to help you get there.

Frequently Asked Questions

Can I have a Medigap plan and a Medicare Advantage plan at the same time?

No, you cannot have both at the same time. In fact, it is illegal for an insurer to sell you a Medigap policy if they know you already have a Medicare Advantage plan. These two options work in completely different ways: Medigap supplements Original Medicare, while an Advantage Plan is an alternative way to receive your benefits. Choosing the right path is a foundational decision, and we are here to provide the clear, unbiased guidance you need to make it confidently.

What happens if I pick the wrong plan? Can I change it?

This is a common worry, but rest assured, you are not locked in forever. If your plan isn’t the right fit, you can make changes during specific times, most notably the Annual Enrollment Period from October 15th to December 7th each year. Special circumstances can also grant you a Special Enrollment Period. We help our clients review their coverage annually to ensure it continues to meet their health and budget needs, protecting them from costly mistakes.

Do all doctors accept Medicare Advantage plans?

No, and this is a critical distinction. Unlike Original Medicare, which is accepted by nearly every doctor in the country, Medicare Advantage plans use provider networks (like HMOs or PPOs). Before enrolling in an Advantage plan, it is essential to verify that your trusted doctors, specialists, and hospitals are in-network. We help you perform this vital check to ensure you can keep the healthcare providers you depend on and avoid surprise out-of-network bills.

Is there a Medicare plan that covers long-term care, like nursing homes?

This is a frequent and important question. Unfortunately, no Medicare plan-including Original Medicare, Medigap, or Medicare Advantage-is designed to cover long-term custodial care in a nursing home or assisted living facility. Medicare may cover short-term, skilled nursing care after a qualifying hospital stay, but not ongoing assistance. Planning for long-term care requires a separate strategy, which we can help you navigate with clarity and foresight to protect your future.

How can I find out which prescription drugs are covered by a Part D or Advantage plan?

The key is to check the plan’s formulary, which is simply its official list of covered drugs. You can find this on the insurance company’s website or, more easily, by using the Plan Finder tool at Medicare.gov. This allows you to enter your specific prescriptions and dosages to see how they are covered by different plans. We walk our clients through this process step-by-step, simplifying the jargon to find the plan that saves them the most money.

What is the real difference between Medigap Plan F and Plan G?

When searching for *what is the best Medicare plan that covers everything*, many look at these two plans. The only difference is that Plan G requires you to pay the annual Medicare Part B deductible yourself ($240 in 2024), while Plan F covers it for you. Because of this, Plan G premiums are typically lower. Importantly, Plan F is now only available to those eligible for Medicare before January 1, 2020. For most new beneficiaries, Plan G offers the most comprehensive coverage available.