Does the thought of navigating Medicare leave you feeling overwhelmed? For many, it’s a confusing maze of complex rules, unfamiliar jargon, and the persistent fear of making a costly mistake. If you’re looking for straightforward medicare tips to cut through the noise, you’ve come to the right place. We understand the anxiety that comes with securing your healthcare in retirement, and we believe you deserve to feel confident and in control of your decisions.

This guide was created to do just that: to provide clear, actionable advice that saves you money and stress. You will discover practical strategies to help lower your expenses, avoid common pitfalls like late enrollment penalties, and choose your coverage with genuine peace of mind. Our goal is to give you the trusted support you need to understand your benefits and use them effectively, turning that feeling of uncertainty into security for the years ahead.

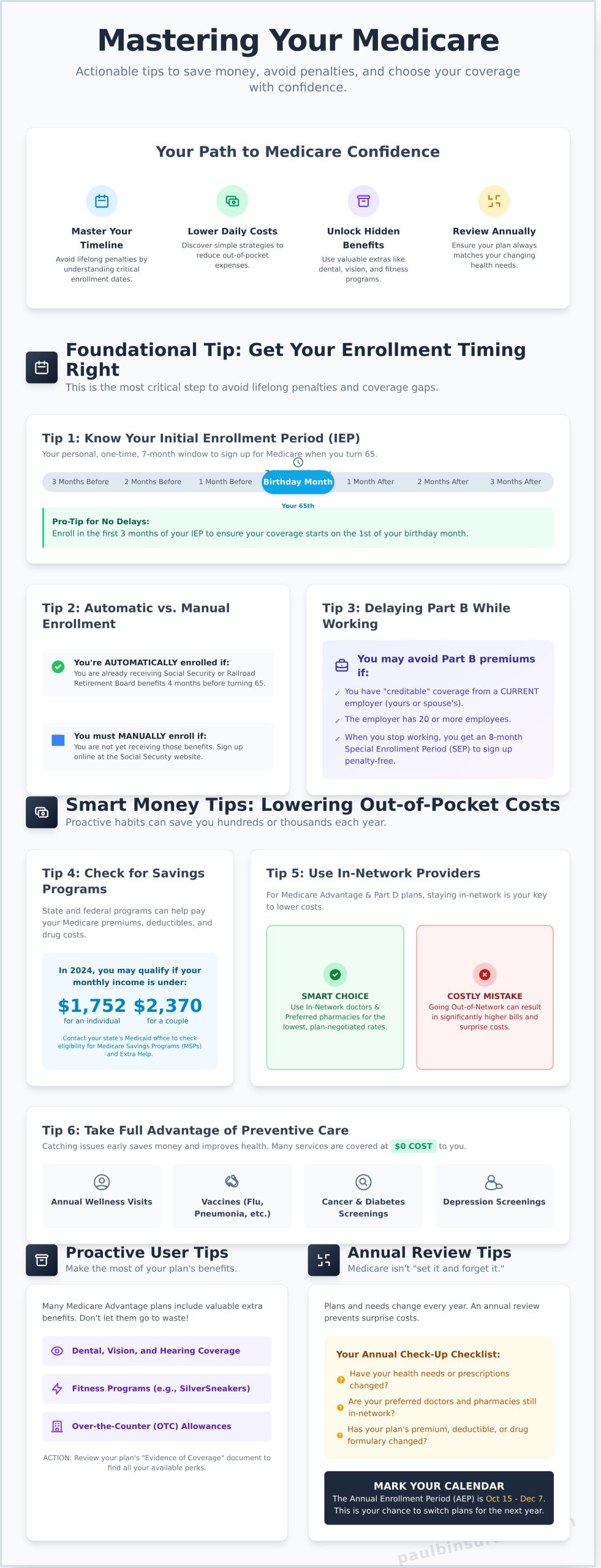

Key Takeaways

- Mastering your enrollment timeline is the first step to avoiding lifelong penalties and ensuring your coverage starts right when you need it.

- Discover simple but effective medicare tips to lower your daily out-of-pocket costs on everything from prescriptions to doctor visits.

- Your plan may include valuable, often unused, benefits that can save you money on dental, vision, and even fitness programs.

- Learn why an annual plan review is critical to prevent surprise costs and ensure your coverage continues to match your health needs.

Foundational Tips: Getting Your Enrollment Timing Right

Navigating the Medicare maze can feel overwhelming, but the first step toward peace of mind is understanding your enrollment timeline. Of all the medicare tips we share, getting this right is the most critical. A simple mistake during this initial phase can lead to lifelong late enrollment penalties and frustrating gaps in your health coverage. We’re here to provide trusted guidance and simplify these rules, helping you move from confusion to confidence.

Tip 1: Know Your Initial Enrollment Period (IEP)

Your IEP is a personal, one-time, 7-month window to sign up for Medicare. It starts three months before the month you turn 65, includes your birthday month, and ends three months after. To ensure your coverage starts without delay on the first of your birthday month, it’s best to enroll during the first three months of your IEP. If you wait until your birthday month or later, your coverage start date will be postponed, potentially leaving you uninsured.

Tip 2: Understand Automatic vs. Manual Enrollment

Not everyone needs to actively sign up. If you’re already receiving Social Security or Railroad Retirement Board benefits at least four months before your 65th birthday, you will be automatically enrolled in both Medicare Part A and Part B. Your card will simply arrive in the mail. For everyone else, enrollment is a manual process that you must initiate. The vast federal health insurance program known as Medicare (United States) requires you to sign up yourself, which you can do easily online at the Social Security Administration’s website.

Tip 3: Consider Delaying Part B if You’re Still Working

If you are still working past 65 and have health coverage through your (or your spouse’s) current employer, you may be able to delay enrolling in Part B and avoid its monthly premium. This is a powerful way to save money, but you must be careful. Your employer coverage must be considered “creditable,” which generally means it’s a group health plan from an employer with 20 or more employees. When you eventually stop working, you’ll be granted an 8-month Special Enrollment Period (SEP) to sign up for Part B without penalty.

Smart Money Tips: Lowering Your Out-of-Pocket Costs

Choosing your Medicare plan is a significant first step, but the journey to managing your healthcare costs doesn’t end there. True savings come from understanding the details of your plan and building smart daily habits. The good news is that you have more control over your expenses than you might think.

These practical medicare tips apply whether you have Original Medicare, a Medicare Advantage plan, or a Medigap supplement. By being proactive, you can potentially save hundreds or even thousands of dollars each year, giving you invaluable peace of mind.

Tip 4: Check if You Qualify for Savings Programs

Did you know that state and federal programs can help pay your Medicare costs? Medicare Savings Programs (MSPs) can help with Part A and/or Part B premiums, deductibles, and copayments. The Extra Help program helps pay for Part D prescription drug costs. In 2024, individuals with monthly incomes generally under $1,752 (or $2,370 for couples) may qualify for an MSP. We strongly encourage you to check your eligibility by contacting your state’s Medicaid office.

Tip 5: Use In-Network Doctors and Preferred Pharmacies

If you have a Medicare Advantage or Part D plan, your provider network is your key to lower costs. Visiting an in-network doctor means you pay the lower, plan-negotiated rate. Going out-of-network can result in much higher bills. Likewise, your drug plan has “preferred” pharmacies where your prescription copays are lowest. Before any appointment or refill, take a moment to confirm your provider or pharmacy is in your plan’s network-it’s a simple step that prevents costly surprises.

Tip 6: Take Full Advantage of Preventive Care

One of the most powerful and often overlooked medicare tips is using your preventive benefits. Staying ahead of health issues is not just good for your well-being; it’s a smart financial strategy. Medicare covers many preventive services at $0 cost to you, including:

- Your one-time “Welcome to Medicare” visit

- Annual Wellness Visits

- Flu shots, pneumonia shots, and COVID-19 vaccines

- Screenings for cancer, diabetes, and depression

Using these benefits helps you and your doctor catch potential problems early, avoiding more complex and expensive treatments down the road. It’s a vital investment in your health and your finances.

Proactive User Tips: Making the Most of Your Plan’s Benefits

Choosing the right Medicare plan is a critical first step, but the real value comes from actively using your benefits. It’s easy to enroll and then file your plan documents away, but many beneficiaries miss out on significant savings and health perks simply because they aren’t aware of them. This is especially true for Medicare Advantage plans, which are often packed with valuable extras.

By becoming a proactive member, you not only improve your health but also ensure you’re getting the most for your money. These simple but powerful medicare tips will help you move from confusion to confidence, transforming your experience with your plan.

Tip 7: Create Your Official Online Medicare Account

Think of your secure online Medicare account as your personal, official dashboard for all things Medicare. It is the single source of truth for your coverage information, accessible through the official government Medicare website. Creating an account is simple—you’ll just need your Medicare card and coverage start date. Once inside, you can:

- Track your claims and see what Medicare has paid.

- View your eligibility and entitlement information.

- Print an official copy of your Medicare card if it’s lost or damaged.

- Manage your prescription drug list and compare Part D plans.

Tip 8: Actually Read Your Explanation of Benefits (EOB)

When an Explanation of Benefits (EOB) arrives in the mail, many people mistake it for a bill and feel a wave of stress. But it’s important to remember: an EOB is not a bill. It is a summary of the healthcare services you received. Take a moment to review it and check for key details like the service date, the amount billed by the provider, and what your plan paid. This simple habit helps you understand your costs and spot potential billing errors before they become a problem.

Tip 9: Don’t Forget Your Plan’s Extra Perks

Are you using all the benefits you’re paying for? Many Medicare Advantage plans include a wealth of extra perks designed to keep you healthy, yet they often go unused. These are built into your plan at no extra cost. Check your plan’s Evidence of Coverage (EOC) document for valuable extras, which can include:

- Routine dental, vision, and hearing coverage.

- Gym memberships or fitness programs like SilverSneakers.

- Allowances for over-the-counter (OTC) products.

- Transportation to medical appointments.

Understanding all the documents and benefits that come with your plan can feel overwhelming. If you ever need personalized guidance to simplify the jargon and ensure you’re maximizing your coverage, our team at Paul B Insurance is always here to provide trusted support.

Annual Review Tips: Why Medicare Isn’t ‘Set It and Forget It’

One of the most common and costly mistakes people make with Medicare is treating it like a one-time decision. The truth is, your healthcare needs, your prescriptions, and the plans themselves can change significantly from one year to the next. Staying in the same plan without a yearly check-up can lead to surprise costs, uncovered medications, or finding out your favorite doctor is suddenly out-of-network. An annual review isn’t a hassle; it’s one of the smartest, most empowering moves you can make. Here are a few final medicare tips to ensure your coverage keeps up with your life.

Tip 10: Mark the Annual Enrollment Period (AEP) on Your Calendar

Every year, Medicare provides a dedicated window to make changes. This is the Annual Enrollment Period (AEP), and it runs from October 15 to December 7. During this time, you can switch plans, add or drop drug coverage, or move between Original Medicare and Medicare Advantage. It’s easy to let this window pass by, but passively staying in a plan that no longer fits your needs is a risk that can lead to unexpected bills and coverage gaps in the new year.

Tip 11: Review Your Annual Notice of Change (ANOC)

Each September, your current plan provider is required to mail you a document called the Annual Notice of Change (ANOC). Think of it as your plan’s report card for the upcoming year. Ignoring this letter is a common and costly mistake. Pay close attention to:

- Your monthly premium and annual deductible

- Changes to the drug formulary (the list of covered prescriptions)

- New copay or coinsurance amounts for doctor visits and services

This document tells you exactly how your costs and coverage will be different next year, giving you the information you need to make a smart decision during AEP.

Tip 12: The Ultimate Tip: Work With an Independent Broker

The simplest way to apply all of these tips without the stress is to partner with a trusted, independent Medicare broker. Instead of you having to decipher the ANOC and compare dozens of plans on your own, an expert does the heavy lifting. They provide unbiased, personalized guidance based on your specific health needs and budget. A good broker offers year-round support and helps you navigate the system with confidence. The best part? This expert service is provided at no cost to you. Ready for a stress-free review? Get your free, unbiased plan comparison.

Turn These Medicare Tips into Real Savings and Peace of Mind

Navigating Medicare can feel overwhelming, but as you’ve seen, a few key actions can make a world of difference. Getting your enrollment timing right prevents lifelong penalties, and proactively reviewing your plan each year ensures you’re never overpaying. These foundational medicare tips are your first step toward mastering the system, but you don’t have to put all the pieces together alone.

Imagine having a trusted expert with over 18 years of experience on your side. We have supported more than 5,000 clients by providing clear, unbiased advice on plans from over 40 top carriers. Our only goal is to find the perfect fit for your unique needs and budget, saving you time, money, and unnecessary stress.

From Confusion to Confidence: Schedule Your Free Medicare Plan Review Today.

You deserve to feel secure and confident in your healthcare choices. Let’s take that next step toward peace of mind, together.

Frequently Asked Questions About Medicare

What is the most common mistake people make when enrolling in Medicare?

The most common and costly mistake is delaying enrollment in Medicare Part B when first eligible, especially if you’re leaving employer coverage. Missing your Initial Enrollment Period can trigger a life-long late enrollment penalty, increasing your monthly premium forever. Understanding the rules around your specific situation is one of the most important medicare tips we can offer. Seeking trusted guidance helps you steer clear of these expensive errors and enroll with confidence, ensuring your coverage starts on time.

Can I switch my Medicare plan at any time of the year?

Generally, no. Most people can only make changes during the Annual Enrollment Period (AEP), which runs from October 15th to December 7th each year. However, certain life events, like moving out of your plan’s service area or losing other health coverage, may qualify you for a Special Enrollment Period (SEP). This allows you to change plans outside of the standard AEP window. It’s important to understand which rules apply to you to avoid gaps in coverage.

How can I find out if my doctor accepts a specific Medicare plan?

The most reliable way is to call your doctor’s office directly. Ask the billing department, “Do you accept the [Plan Name] from [Insurance Company]?” While insurance companies have online provider directories, they can sometimes be outdated. Verifying directly with your doctor’s office is the best way to ensure you won’t face any surprises. An expert can also help you confirm network status for all your trusted providers, simplifying the process for you.

Do I really need a Medicare Part D plan if I don’t take any prescriptions now?

It’s a wise decision to enroll in a Part D prescription drug plan when you first become eligible. If you delay, you will face a permanent late enrollment penalty that’s added to your premium once you do sign up. Enrolling in a low-cost plan now protects you from future penalties and provides peace of mind, ensuring you have coverage in place if your health needs unexpectedly change. Think of it as affordable protection for your future.

What’s the difference between a Medicare broker and calling an insurance company directly?

An agent at an insurance company can only offer you plans from that single carrier. An independent Medicare broker, however, works with multiple insurance companies. This allows us to provide unbiased, personalized guidance based on your unique needs and budget, not a sales quota. Our goal is to compare all your options and help you find the absolute best fit, giving you confidence that your choice is the right one for you and not just for the insurance company.

Is it better to choose a Medicare Advantage plan or a Medigap plan?

There isn’t a single “better” choice-it truly depends on your personal needs. Medigap plans work with Original Medicare and offer predictable costs with the freedom to see any doctor who accepts Medicare. Medicare Advantage (Part C) plans often have lower premiums and include extra benefits like dental and vision but use provider networks. One of our most helpful medicare tips is to carefully weigh your budget, health needs, and desire for flexibility before deciding which path is right for you.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com