Figuring out how do you qualify for medicare can feel overwhelming. With complex rules, different paths, and critical deadlines, it’s easy to feel lost and worried about making a costly mistake. You might be wondering if your work history is enough, or how a specific health condition changes the requirements. This uncertainty is a common source of stress for many people approaching this milestone, but it doesn’t have to be your experience.

Our simple guide is here to provide the trusted guidance you need, moving you from confusion to confidence. We will break down the exact eligibility requirements based on your age, disability, or specific health situation in plain, easy-to-understand language. You will learn precisely which path applies to you and gain a clear, step-by-step plan for what to do next. Consider this your roadmap to understanding your Medicare eligibility, so you can move forward with total peace of mind.

Key Takeaways

- Most people qualify for Medicare at age 65, but understanding the exact timing is essential to avoid any gaps in your health coverage.

- A qualifying disability or specific health condition, like ESRD or ALS, could make you eligible for Medicare benefits much earlier than age 65.

- Lacking enough work credits isn’t a dead end; we’ll show you how a spouse’s work history is a common answer to how do you qualify for medicare.

- Learn how special circumstances can impact your eligibility and what crucial next steps to take once you confirm you are able to enroll.

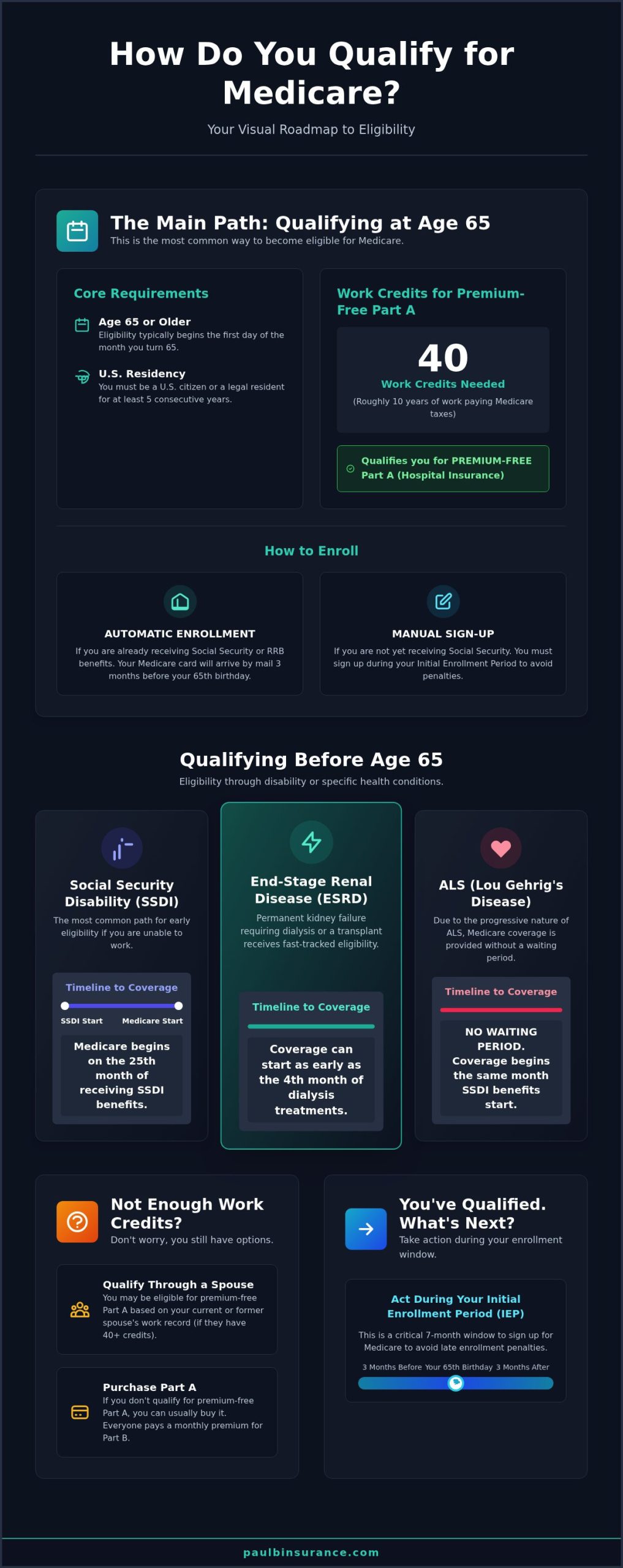

The Main Path to Medicare: Qualifying at Age 65

While some situations allow for earlier access, the most common answer to the question, “how do you qualify for medicare?” is by turning 65. This is the traditional age of eligibility, and understanding this path provides the foundation for every other scenario. For most people, this journey is straightforward and depends on two key factors: your age and residency status, and your work history.

First, you must be a U.S. citizen or a legal resident who has lived in the United States for at least five consecutive years. Your eligibility typically begins on the first day of the month you turn 65. So, if your birthday is on June 20th, your Medicare coverage can start on June 1st. This is a fundamental part of the Medicare (United States) program designed to provide health coverage for seniors.

Understanding ‘Work Credits’ for Premium-Free Part A

The second piece of the puzzle is your work history, which determines if you get Medicare Part A (Hospital Insurance) for free. This is measured in “work credits” you earn by working and paying Medicare taxes. To receive premium-free Part A, most people need 40 credits, which is roughly equivalent to 10 years of work. It’s important to remember that even if you don’t have enough credits, you can usually still buy into Part A. And regardless of your work history, nearly everyone pays a monthly premium for Part B (Medical Insurance).

Automatic Enrollment vs. Needing to Sign Up

Navigating the enrollment process can feel confusing, but it often comes down to one question: are you already receiving Social Security benefits?

- If you are receiving Social Security: You will be enrolled in Medicare Part A and Part B automatically. Look for your Medicare card to arrive in the mail about three months before your 65th birthday.

- If you are not receiving Social Security: You will need to sign up for Medicare yourself. This is done during your Initial Enrollment Period, a seven-month window around your 65th birthday. Taking action during this time is crucial to avoid potential late enrollment penalties.

Qualifying Before Age 65: Disability and Health Conditions

While most people associate Medicare with turning 65, a significant number of Americans become eligible earlier due to a disability or a specific health condition. Facing a serious illness is challenging enough without having to worry about healthcare coverage. Fortunately, Medicare provides a crucial safety net for those who can no longer work, offering peace of mind during a difficult time.

Understanding how do you qualify for Medicare under these special circumstances is the first step toward securing your benefits. The process and waiting periods differ depending on your situation. Let’s walk through the three main pathways to early eligibility so you can move forward with clarity and confidence.

Qualifying Through Social Security Disability Insurance (SSDI)

This is the most common path to early Medicare. If you qualify for Social Security Disability Insurance (SSDI), you will be automatically enrolled in Medicare Parts A and B after a waiting period. Here’s a simple breakdown of what you need to know:

- You must receive SSDI benefits for at least 24 months.

- This 24-month period does not need to be consecutive.

- Your Medicare coverage automatically begins on the first day of your 25th month of receiving disability benefits.

While enrollment is automatic, it’s always wise to be proactive. You can learn more about the specific steps and timelines when you apply for Medicare through the official government portal, ensuring you have all the necessary information for a smooth transition.

Qualifying with End-Stage Renal Disease (ESRD)

If you have been diagnosed with End-Stage Renal Disease (ESRD)-permanent kidney failure requiring regular dialysis or a kidney transplant-you do not have to wait 24 months. Medicare eligibility for ESRD is fast-tracked. Your coverage can often start as early as the first day of the fourth month of your dialysis treatments. In certain situations, coverage may begin even sooner, and even a spouse or dependent child of an eligible person may qualify.

Qualifying with ALS (Lou Gehrig’s Disease)

For individuals diagnosed with Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig’s Disease, there is no waiting period for Medicare. This special provision recognizes the severe and progressive nature of the illness. If you have ALS, your Medicare coverage will begin the very same month that your SSDI benefits start, providing immediate and essential health coverage when you need it most.

What if You Don’t Have Enough Work Credits?

When you’re exploring how do you qualify for Medicare, finding out you’re short on the 40 work credits needed for premium-free Part A can be stressful. But please don’t worry. This is a common situation, and it doesn’t mean you’re out of options. The Medicare system has several pathways to ensure you can still get the quality health coverage you need. Understanding these alternatives is the key to preventing any gaps in your care and moving forward with confidence.

Navigating these rules can feel complicated, but we’re here to provide the straightforward guidance you need. Let’s break down the two most common solutions.

Qualifying on Your Spouse’s Work Record

Even if you have never worked or have an inconsistent work history, you may still be eligible for premium-free Part A through your spouse. You can qualify based on your spouse’s (or former spouse’s) record as long as they have earned the required 40 credits and are at least 62 years old.

Here’s how it generally works:

- Current Spouses: You can qualify if you are at least 65 years old and your spouse is at least 62.

- Divorced Spouses: You may qualify on an ex-spouse’s record if you were married for at least 10 years, are currently unmarried, and are age 65 or older.

- Surviving Spouses: If your spouse has passed away, you may qualify on their record at age 65 if you were married for at least nine months and are currently unmarried.

Buying into Medicare: Paying for Part A

If you cannot qualify through your own record or a spouse’s, you can often buy into the Medicare program. To do this, you must be 65 or older and a U.S. citizen or a legal resident for at least five consecutive years. It’s important to know that if you buy Part A, you must also enroll in and pay the monthly premium for Part B (Medical Insurance).

The monthly premium for Part A depends on the number of work credits you have. For 2024, if you have between 30-39 credits, the premium is $278 per month. If you have fewer than 30 credits, the premium is $505 per month. The Social Security Administration is the best resource for confirming your exact work credit count and eligibility. This path ensures that even without a full work history, you have a direct way to secure comprehensive hospital coverage.

Special Circumstances That Affect Qualification

Life isn’t always straightforward, and Medicare’s rules can feel just as complex. Certain situations, like working past 65, your citizenship status, or living abroad, can directly impact your eligibility and enrollment choices. Understanding these nuances is the key to making confident decisions and steering clear of costly, irreversible mistakes.

These scenarios often require careful, personalized planning. Let’s walk through some of the most common situations to give you the clarity you need.

Still Working Past 65?

Turning 65 while still employed doesn’t disqualify you from Medicare, but it does present you with important choices. The most critical factor is the size of your employer, as this determines whether your work insurance or Medicare pays first.

- For companies with 20 or more employees: You can generally delay enrolling in Part B without facing a penalty, as your employer’s group health plan is considered your primary coverage.

- For companies with fewer than 20 employees: You will almost always need to enroll in Medicare Part A and Part B when you turn 65. In this case, Medicare becomes your primary insurer, and failing to sign up can lead to major gaps in coverage and permanent late enrollment penalties.

Comparing your employer plan to Medicare is essential, but delaying enrollment must be done correctly to avoid future issues.

Rules for Non-U.S. Citizens and Legal Residents

For non-U.S. citizens, understanding how do you qualify for Medicare hinges on a foundational residency rule. To be eligible, you must be a lawful permanent resident (often called a “Green Card” holder) and have lived in the United States continuously for at least five years. After you meet this 5-year requirement, the standard eligibility rules apply-you must be 65 or older or have a qualifying disability, and you or your spouse must have earned the necessary work credits.

Living Abroad and Medicare

It’s crucial to know that Original Medicare provides virtually no coverage outside of the United States. However, your enrollment decisions while living abroad still matter. Many expatriates choose to enroll in Part A (if it’s premium-free) and Part B when they first become eligible. This strategy helps them avoid lifelong late enrollment penalties if they ever decide to move back to the U.S. For those who travel, certain Medicare Supplement (Medigap) plans can offer valuable coverage for foreign travel emergencies, providing peace of mind on your adventures.

Navigating these special circumstances requires trusted guidance. If you need help understanding your unique situation, our team at paulbinsurance.com is here to simplify the process and help you move from confusion to confidence.

You’ve Qualified. What’s the Next Step?

First, congratulations! Understanding how do you qualify for Medicare before age 65 is a significant first step, and you’ve successfully navigated it. Now, the journey shifts from eligibility to enrollment, and making the right choices here is crucial for your long-term health and financial well-being. Getting your coverage right from the start helps you steer clear of costly mistakes and future headaches.

Your next step is to understand the two main paths you can take to receive your Medicare benefits. Each path has a different structure, and your decision will impact your costs, your choice of doctors, and your overall coverage.

Understanding Original Medicare vs. Medicare Advantage

Think of this as your foundational choice. You can either get your benefits directly from the government or through a private insurance company approved by Medicare.

- Original Medicare (Parts A & B) is the traditional, government-administered health plan. It gives you broad access to doctors and hospitals nationwide, but it has significant gaps in coverage, leaving you responsible for deductibles and 20% of most medical bills.

- Medicare Advantage (Part C) plans are offered by private companies. They bundle your Part A, Part B, and usually Part D (prescription drug) coverage into one plan. Many also include extra benefits not covered by Original Medicare, like routine dental, vision, and hearing care.

Covering the Gaps with Medigap and Part D

If you choose the path of Original Medicare, it’s highly recommended that you add supplemental coverage to protect yourself from unpredictable out-of-pocket costs. This is where Medigap and Part D plans come in.

- Medigap (Medicare Supplement) plans help pay for the costs that Original Medicare doesn’t cover, such as your deductibles and coinsurance.

- Part D plans provide essential prescription drug coverage, which is not included in Original Medicare.

It’s important to remember: You cannot have both a Medigap plan and a Medicare Advantage plan at the same time. You choose one path or the other.

Why Expert Guidance Makes a Difference

Navigating these choices can feel overwhelming, but you don’t have to do it alone. The path you choose now will affect your healthcare for years to come. An independent expert can help you compare all your options from dozens of carriers, ensuring you find a plan that truly fits your unique health needs and budget. We’re here to turn confusion into confidence.

Let’s find the right path forward for you. Book a Free, Unbiased Consultation today and get the clear, personalized guidance you deserve.

From Qualified to Confident: Your Medicare Next Steps

Understanding your eligibility is the first crucial step. Whether you are nearing age 65, qualify due to a disability, or are navigating special circumstances with work credits, there is a clear path forward. While figuring out how do you qualify for medicare can seem daunting, you don’t have to do it alone.

Once you’re eligible, the real journey of choosing the right coverage begins. This is where expert, patient guidance makes all the difference. At Paul B Insurance, we’ve guided over 5,000 clients to peace of mind by providing truly unbiased advice from over 40 top carriers. We’re here to provide personalized, year-round support.

Feeling overwhelmed? Let’s simplify your Medicare journey together. Book a Free, Unbiased Consultation and let us help you move from confusion to confidence today.

Frequently Asked Questions About Medicare Eligibility

Can you qualify for Medicare at age 62?

While the standard age for Medicare is 65, there are specific situations where you can enroll earlier. The most common way how do you qualify for medicare before 65 is by receiving Social Security Disability Insurance (SSDI) for 24 months. You may also qualify almost immediately if you are diagnosed with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS). Age 62 alone, without a qualifying disability or health condition, does not make you eligible for Medicare.

Do I have to be a U.S. citizen to qualify for Medicare?

To be eligible for Medicare, you must be a U.S. citizen or a legal resident who has lived continuously in the United States for at least five years. This residency requirement is a crucial part of the eligibility criteria, alongside the age or disability requirements. If you are a recent legal resident, it’s important to verify your five-year residency period to ensure you meet this key qualification when you apply for your Medicare benefits.

What happens if I retire early but am not yet 65?

Retiring early does not grant you early access to Medicare. If you retire before you turn 65 and lose your employer-sponsored health insurance, you will need to find alternative coverage to bridge the gap. Options often include continuing your old plan through COBRA, purchasing a plan from the Affordable Care Act (ACA) Marketplace, or getting a private health insurance plan. Planning for this coverage is a critical step in your early retirement journey to avoid being uninsured.

How long do I have to be on disability to get Medicare?

Typically, you must receive Social Security Disability Insurance (SSDI) benefits for 24 months before you are automatically enrolled in Medicare. This two-year waiting period starts from the date your disability benefits begin. However, there are important exceptions. If you have End-Stage Renal Disease (ESRD) or ALS (Lou Gehrig’s disease), you can qualify for Medicare much sooner, often without any waiting period at all. Understanding these rules is key to navigating your eligibility.

Can I use my ex-spouse’s work history to qualify for Medicare?

Yes, it is possible to use an ex-spouse’s work record to qualify for premium-free Medicare Part A. To be eligible, you must have been married to them for at least 10 years, you must currently be unmarried, and you must be at least 62 years old. This provision can be incredibly helpful if you don’t have the required 40 work credits from your own employment history to qualify for Part A without a premium.

Do I automatically get Medicare when I turn 65?

You are only automatically enrolled in Medicare Part A and Part B at 65 if you are already receiving benefits from either Social Security or the Railroad Retirement Board. If you have delayed taking these benefits, you will not be signed up automatically. In this case, you must proactively enroll during your Initial Enrollment Period-the seven-month window around your 65th birthday-to avoid late enrollment penalties and gaps in your health coverage.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com