Does the thought of choosing a Medicare plan feel like you’re trying to solve a puzzle with missing pieces? Between the alphabet soup of ‘Parts’ and a sea of plan letters, it’s easy to feel overwhelmed. You might be worried about making a costly mistake, losing access to a doctor you trust, or simply not knowing how to balance premiums and out-of-pocket costs. It’s a heavy weight, and it leads so many of us to ask the same critical question: what is the best medicare plan for my specific needs?

You can take a deep breath, because you’ve come to the right place for clear, straightforward answers. This guide was created to provide trusted guidance, not more confusion. We will walk you through the key questions to ask yourself, helping you understand the real differences between your options. Our goal is to help you move from uncertainty to confidence, so you can select a plan that protects both your health and your budget, giving you lasting peace of mind.

Key Takeaways

- Your first step isn’t picking a specific plan, but choosing between the two foundational paths: Original Medicare with a supplement or a Medicare Advantage plan.

- The answer to what is the best medicare plan for you depends on your personal answers to five key questions about your health, budget, and lifestyle.

- Learn to identify and avoid common, costly enrollment mistakes that go beyond just looking at the monthly premium.

- You can move from confusion to confidence by using a clear framework to compare your options and understanding where to find unbiased support.

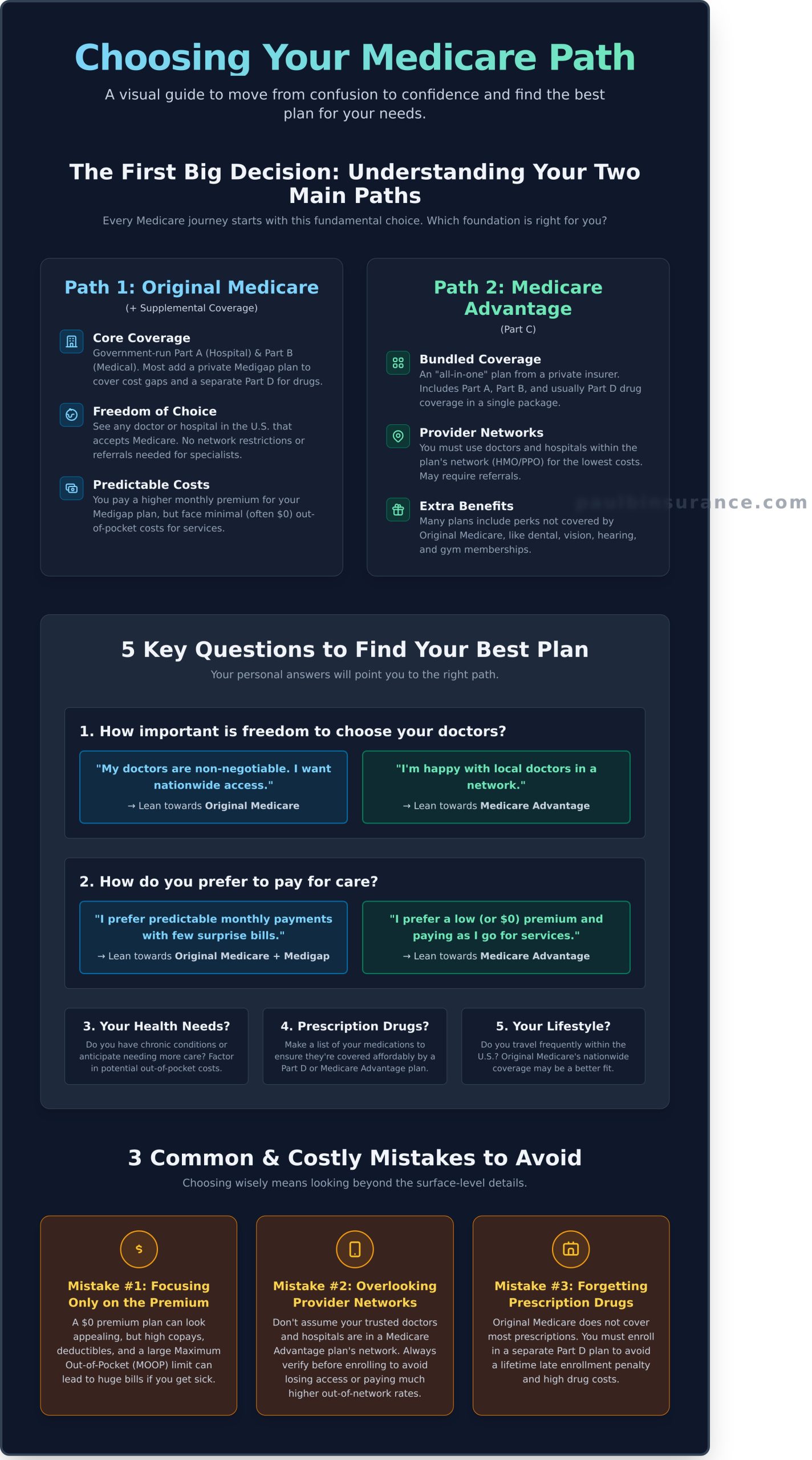

The First Big Decision: Understanding Your Two Main Medicare Paths

Navigating the world of Medicare can feel overwhelming, but we can simplify the journey right from the start. The key to finding peace of mind is understanding that every option, every plan, and every decision stems from one fundamental choice between two main paths. Answering the question of what is the best Medicare plan for you begins by choosing the foundational route that aligns with your healthcare needs and lifestyle. Before you get lost in the details of different plans, it’s helpful to have a solid grasp of the two main Medicare structures available.

Think of it this way: you can either stick with the traditional, government-administered program or you can choose an all-in-one alternative offered by a private insurance company. Let’s break down these two paths.

Path 1: Original Medicare (Part A & B) + Supplemental Coverage

This is the traditional, government-run health insurance program that has been in place for decades. It provides a solid foundation for your health coverage but leaves some costs for you to pay. This path is often chosen by those who value flexibility and broad access to care.

- Core Coverage: Consists of Part A (Hospital Insurance) and Part B (Medical Insurance).

- Freedom of Choice: You can see any doctor or visit any hospital in the U.S. that accepts Medicare, with no network restrictions or referral requirements.

- Covering the Gaps: To help pay for out-of-pocket costs like deductibles and coinsurance, most people on this path add a Medicare Supplement (Medigap) policy.

- Prescription Drugs: You will need to enroll in a separate, standalone Medicare Part D plan for your prescription drug coverage.

Path 2: Medicare Advantage (Part C)

This is an “all-in-one” alternative to Original Medicare. These bundled plans are offered by private insurance companies that are approved by Medicare. They are popular for their convenience, predictable costs, and extra perks. The journey to finding out what is the best Medicare plan for your life starts by comparing these two foundational choices.

- Bundled Coverage: These plans include all the benefits of Part A and Part B, and most also include Part D prescription drug coverage in one simple package.

- Provider Networks: You will typically need to use doctors, hospitals, and specialists who are in the plan’s network (like an HMO or PPO) to get the lowest costs.

- Extra Benefits: Many plans offer additional benefits not covered by Original Medicare, such as routine dental, vision, hearing, and fitness program memberships.

5 Key Questions to Find Your Best Medicare Plan

The single most common question we hear is, “what is the best medicare plan?” The truth is, there’s no single right answer for everyone. The best plan isn’t a specific policy number; it’s the one that fits seamlessly into your life, budget, and health needs. Instead of searching for a one-size-fits-all solution, the path to confidence begins by looking inward.

By honestly answering the questions below, you can gain tremendous clarity. This simple self-assessment will help you understand your priorities and point you toward the Medicare path that makes the most sense for you. Think of this as building a personalized roadmap from confusion to confidence.

1. Doctors & Hospitals: How important is freedom of choice?

Do you have a team of trusted doctors, specialists, or a specific hospital system you refuse to give up? Your answer here is a major signpost. Original Medicare gives you the freedom to see any doctor or visit any hospital in the U.S. that accepts Medicare, with no referrals needed. In contrast, most Medicare Advantage plans operate with local networks (like HMOs or PPOs) and may require referrals to see specialists. If maximum freedom and nationwide access are your top priorities, Original Medicare is often a better fit.

2. Your Budget: How do you prefer to pay for care?

Your financial comfort zone plays a huge role in finding the right coverage. There are two primary models for healthcare spending in Medicare:

- Predictable Costs: With Original Medicare plus a Medigap plan, you pay a higher, fixed premium each month. In return, you face very few (and sometimes zero) out-of-pocket costs when you receive care.

- Pay-As-You-Go: With a Medicare Advantage plan, you often have a $0 or low monthly premium. You then pay for services as you use them through copays and coinsurance until you reach a yearly maximum out-of-pocket (MOOP) limit.

Each approach has its benefits, depending on your risk tolerance and cash flow. For a data-driven analysis of how these choices impact beneficiary spending, the Kaiser Family Foundation offers a detailed report Comparing Your Options: A Side-by-Side Look that reviews dozens of studies on the topic.

3. Health Needs: What is your current health status?

It’s crucial to plan not just for the health you have today, but for the health you might have in the future. If you manage chronic conditions or anticipate needing more medical services, the predictable, low out-of-pocket costs of a Medigap plan can provide immense peace of mind. If you are currently in excellent health, the low-premium model of a Medicare Advantage plan can be very appealing. Just remember, if you choose an Advantage plan now and want to switch to a Medigap plan later, you may have to go through medical underwriting, and coverage is not guaranteed.

4. Prescriptions & Extra Benefits: What else do you need covered?

The answer to “what is the best medicare plan for me” often comes down to the details. Do you take daily prescription medications? If so, ensuring they are on a plan’s drug list (formulary) is non-negotiable. Furthermore, Original Medicare doesn’t cover routine dental, vision, or hearing services. Medicare Advantage plans often bundle these extra benefits into a single plan, which can be a convenient and cost-effective solution for many. If you prefer Original Medicare, you can still get this coverage by purchasing separate, standalone policies.

Comparing Your Options: A Side-by-Side Look

Navigating the maze of Medicare can feel overwhelming, but you’ve already taken the most important step by thinking about your personal needs. Now, let’s bring some clarity to the two main paths forward. Seeing the options side-by-side is often the simplest way to understand which direction is right for you. This comparison is a crucial step in answering the question, what is the best Medicare plan for your unique circumstances? Our goal is to move you from confusion to confidence, and this quick reference guide is designed to do just that.

Feature Comparison Table

| Feature | Original Medicare + Medigap & Part D | Medicare Advantage (Part C) |

|---|---|---|

| Monthly Premiums | Typically higher (Part B + Medigap + Part D premiums) | Often lower, with many $0 premium plans available |

| Doctor Choice | Freedom to see any doctor or hospital in the U.S. that accepts Medicare | Must use doctors and hospitals within the plan’s network (HMO or PPO) |

| Prescription Drugs | Covered by a separate, standalone Part D plan | Usually included in the plan (MAPD) |

| Out-of-Pocket Costs | Very predictable; minimal or no copays/deductibles for services | Pay-as-you-go with copays and coinsurance up to an annual maximum |

| Extra Benefits | Not included; must purchase separate dental, vision, or hearing plans | Often included (e.g., dental, vision, hearing, gym memberships) |

Who is Path 1 (Original Medicare + Medigap) Best For?

This combination often provides the most comprehensive and predictable coverage, offering true peace of mind against unexpected medical bills. It’s an excellent choice if you prioritize flexibility and financial stability. This path is likely a great fit for you if you:

- Want the freedom to see any specialist nationwide without needing a referral.

- Are a frequent traveler or a “snowbird” who needs reliable coverage across state lines.

- Prefer paying a higher, fixed monthly premium in exchange for little to no out-of-pocket costs when you receive care.

Who is Path 2 (Medicare Advantage) Best For?

Medicare Advantage plans are designed to be an affordable, all-in-one alternative, packing convenience and value into a single package. This path is often the answer to what is the best Medicare plan for those who want simplicity and extra perks without a high monthly cost. This path might be right for you if you:

- Are generally healthy and want to keep your monthly premium costs as low as possible.

- Value the convenience of having medical, prescription drug, and extra benefits bundled into one plan.

- Have local doctors and hospitals you trust that are already in the plan’s network.

3 Common (and Costly) Mistakes to Avoid When Choosing

Navigating the world of Medicare can feel overwhelming, but you can find the right path with confidence by simply avoiding a few common pitfalls. We see these mistakes happen often, and they can lead to unexpected costs and gaps in coverage. Our goal is to empower you with the knowledge to steer clear of them, ensuring the plan you choose truly serves your health and financial needs.

Understanding these points is a crucial step in answering the question, “what is the best medicare plan for me?”

Mistake #1: Focusing Only on the Monthly Premium

A plan with a $0 monthly premium is certainly appealing, but it’s important to remember that it is not “free” healthcare. A low or non-existent premium is often balanced by higher costs when you actually use your insurance. These can include:

- Deductibles: The amount you must pay before your plan starts paying.

- Copayments: A fixed fee for services like a doctor’s visit.

- Coinsurance: The percentage you pay for a service after meeting your deductible.

A plan with a low premium might be fine during a healthy year, but a single hospital stay could lead to thousands of dollars in bills. Always look at the plan’s maximum out-of-pocket cost-this number is your true financial safety net for the year.

Mistake #2: Not Checking if Your Doctors and Drugs are Covered

Never assume your current doctors or prescriptions will be covered, even by a plan from the same insurance company you’ve used for years. Provider networks and drug formularies (the list of covered medications) change every single year. Verifying your coverage is essential before enrolling.

If you choose a plan where your trusted doctor is out-of-network, you could be responsible for the entire bill. Likewise, check that your prescriptions are on the formulary and note the cost difference between using a preferred pharmacy versus a standard one, as it can save you hundreds of dollars.

Mistake #3: Missing Your Enrollment Window

Timing is critical with Medicare. Your Initial Enrollment Period (IEP) is the seven-month window around your 65th birthday when you first become eligible. Enrolling late in Part B or Part D can result in lifelong penalties that are added to your monthly premiums.

While the Annual Enrollment Period each fall allows you to switch plans, your initial choices are foundational. Waiting until you are sick to secure robust coverage is a risky strategy, as some options, like certain Medigap plans, may require medical underwriting and can deny you coverage based on your health history. Getting it right from the start provides lasting peace of mind. Navigating these details is where expert guidance can make all the difference.

From Confusion to Confidence: Why You Don’t Have to Decide Alone

Reading through the different parts, plans, and timelines of Medicare can feel like learning a new language. Even with all the right information, the path forward can seem unclear, and it’s completely normal to feel a bit overwhelmed. You’ve taken a huge step by educating yourself, but the final, most important step-making a choice-doesn’t have to be one you take by yourself.

The journey to finding the right coverage is about matching your unique needs to the right plan. So, when you’re still asking, “what is the best medicare plan for me?” the answer often lies in getting personalized, expert guidance from a trusted advocate.

The Difference Between a Broker and a Captive Agent

Imagine having an expert on your side. That’s an independent Medicare broker. We work for you, not a specific insurance company. This allows us to compare dozens of plans from various carriers to find your ideal fit. In contrast, a captive agent works for a single company and can only present that company’s products, which may or may not be the best option for your health and budget.

How an Independent Broker Simplifies Your Choice

Our role is to be your trusted guide. We take the framework you’ve learned here and apply it directly to your life, providing the clarity you need to make an empowered decision. Our goal is to help you truly determine what is the best medicare plan by putting your needs first, always.

- We help you answer the key questions: We’ll walk through your doctors, prescriptions, and budget to narrow down the options to only those that make sense for you.

- Our guidance comes at no cost to you: We are compensated by the insurance carriers, so you receive our expert advice and support without ever paying a fee. Our only goal is your long-term satisfaction.

- We handle the heavy lifting: From simplifying the jargon to managing the application paperwork, we ensure a smooth and error-free enrollment process.

- You get year-round support: Our relationship doesn’t end after you enroll. We’re here to help with plan questions, claim issues, or annual reviews for the life of your policy.

You’ve done the research. Now, let an expert from Paul B Insurance help you cross the finish line with confidence. Ready to find your perfect fit? Schedule a free, no-obligation consultation today.

Find Your Best Medicare Plan with Confidence

Choosing your Medicare coverage is one of the most important healthcare decisions you’ll make. The journey begins with understanding your two main paths-Original Medicare with a Medigap plan or a Medicare Advantage plan-and carefully considering your personal health needs, budget, and lifestyle. Ultimately, the answer to what is the best medicare plan is the one that is tailored specifically for you, providing the right coverage at the right cost.

But you don’t have to navigate this complex decision alone. With trusted guidance from an expert with over 18 years of experience, you can get clear, unbiased advice. We help you compare options from over 40 top insurance carriers, empowering you to make the right choice, just as we have for over 5,000 clients nationwide.

Ready to move from confusion to confidence? Let’s find your best Medicare plan together. Book your free consultation. You deserve to feel secure and cared for in your healthcare journey.

Frequently Asked Questions

Is there one Medicare plan that is universally considered the best?

No, there isn’t a single “best” plan for everyone. The search for what is the best medicare plan is deeply personal and depends entirely on your unique circumstances. Your ideal coverage hinges on factors like your health needs, prescription drugs, budget, and which doctors you want to see. A plan that’s perfect for your neighbor might be a costly mistake for you. That’s why personalized, unbiased guidance is so crucial to making a confident choice.

Can I switch from Medicare Advantage back to Original Medicare if I don’t like it?

Yes, you can switch, but only during specific enrollment periods. The most common time is the Annual Election Period from October 15 to December 7. There is also a Medicare Advantage Open Enrollment Period from January 1 to March 31. Navigating these dates can be tricky, so it’s important to understand your options ahead of time to ensure you don’t miss your window to make a change and find coverage that truly works for you.

What is the difference between a Medigap plan and a Medicare Advantage plan?

Think of it this way: Medigap works with Original Medicare (Parts A & B) to help cover out-of-pocket costs like deductibles and coinsurance. Medicare Advantage (Part C) is an alternative to Original Medicare that bundles Parts A, B, and often D (prescriptions) into one plan, usually with a specific network of doctors. Understanding this key difference is the first step to finding the right path for your healthcare needs and determining what is the best medicare plan for you.

If I’m healthy, do I really need more than just Original Medicare?

While you may be healthy now, Original Medicare has no annual out-of-pocket maximum. This means a single unexpected hospital stay could leave you with significant, uncapped medical bills. Both Medigap and Medicare Advantage plans provide a financial safety net by limiting your annual spending. Investing in more coverage is about protecting your health and your savings from unpredictable costs down the road, giving you essential peace of mind for the future.

How much does it cost to work with an independent Medicare broker?

Working with a trusted independent broker costs you nothing. Our services are provided at no charge to you, as we are compensated directly by the insurance carriers if you decide to enroll. Because we are independent, we offer unbiased, personalized advice focused solely on finding the best fit for your needs, not on promoting one specific company. This ensures you receive expert guidance without any added financial pressure or hidden fees.

What happens if my doctor leaves my Medicare Advantage plan’s network?

If your doctor leaves your plan’s network, you typically have two choices: find a new, in-network doctor or pay much higher out-of-pocket costs to continue seeing them. In certain situations, this change may trigger a Special Enrollment Period (SEP), allowing you to switch to a different plan. It’s a stressful situation, which is why having an expert to call for year-round support can help you navigate these unexpected changes and find a swift solution.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com