Last Tuesday, 71-year-old Martha sat at her kitchen table surrounded by 12 different glossy brochures, each one making a conflicting promise about 2026 coverage. It’s exhausting to deal with the constant noise from loud TV commercials and aggressive mailers. You likely feel like you’re stuck in a maze, worried that one wrong move could mean losing the primary doctor you’ve visited for the last 15 years.

We know exactly how that feels. It’s frustrating when you just want to know if your prescriptions are still covered or if you can find a plan with better dental and vision benefits. That’s why we’re here to help you move from confusion to confidence. We’ll show you exactly how to switch medicare advantage plans for the 2026 season without any of the typical insurance stress.

Our guide simplifies the jargon so you can secure lower monthly premiums and protect your health. We’ll walk you through the specific rules for the Annual Enrollment Period starting October 15, 2026, and the Open Enrollment Period beginning in January. You’ll get a clear, step-by-step process to ensure your favorite doctors stay in your network while you avoid any costly late enrollment penalties.

Key Takeaways

- Learn the specific 2026 dates for the Annual Enrollment and Open Enrollment periods so you never miss a critical deadline.

- We walk you through our simple 5-step process on how to switch medicare advantage plans while ensuring your favorite doctors and medications stay covered.

- Discover why looking past the monthly premium to the “Total Cost of Care” is the secret to protecting your 2026 budget and avoiding surprises.

- Understand the rules for moving back to Original Medicare and how medical underwriting might affect your ability to secure a Medigap plan.

- See how partnering with an independent broker gives you unbiased access to over 40 carriers, moving you from a state of confusion to total confidence.

Understanding Your Options: Why Consider Switching Medicare Advantage Plans in 2026?

We know that opening your mail in late 2025 felt like a full-time job. The stack of envelopes can feel heavy. If you feel a bit lost by the changes arriving for the 2026 plan year, you are in good company. Every September, your insurance company sends a document called the Annual Notice of Change. This letter is your first alert that learning how to switch medicare advantage plans could save you significant money this year. For 2026, federal regulations from the Centers for Medicare and Medicaid Services have changed how private companies receive funding. This shift has caused a ripple effect throughout the industry. We’ve seen a 12 percent average increase in monthly premiums across several major carriers compared to 2025. To make an informed choice, it is helpful to start with the basics of What is a Medicare Advantage Plan? and how these private options interact with the federal system.

The Red Flags: When Your Current Plan Stops Working for You

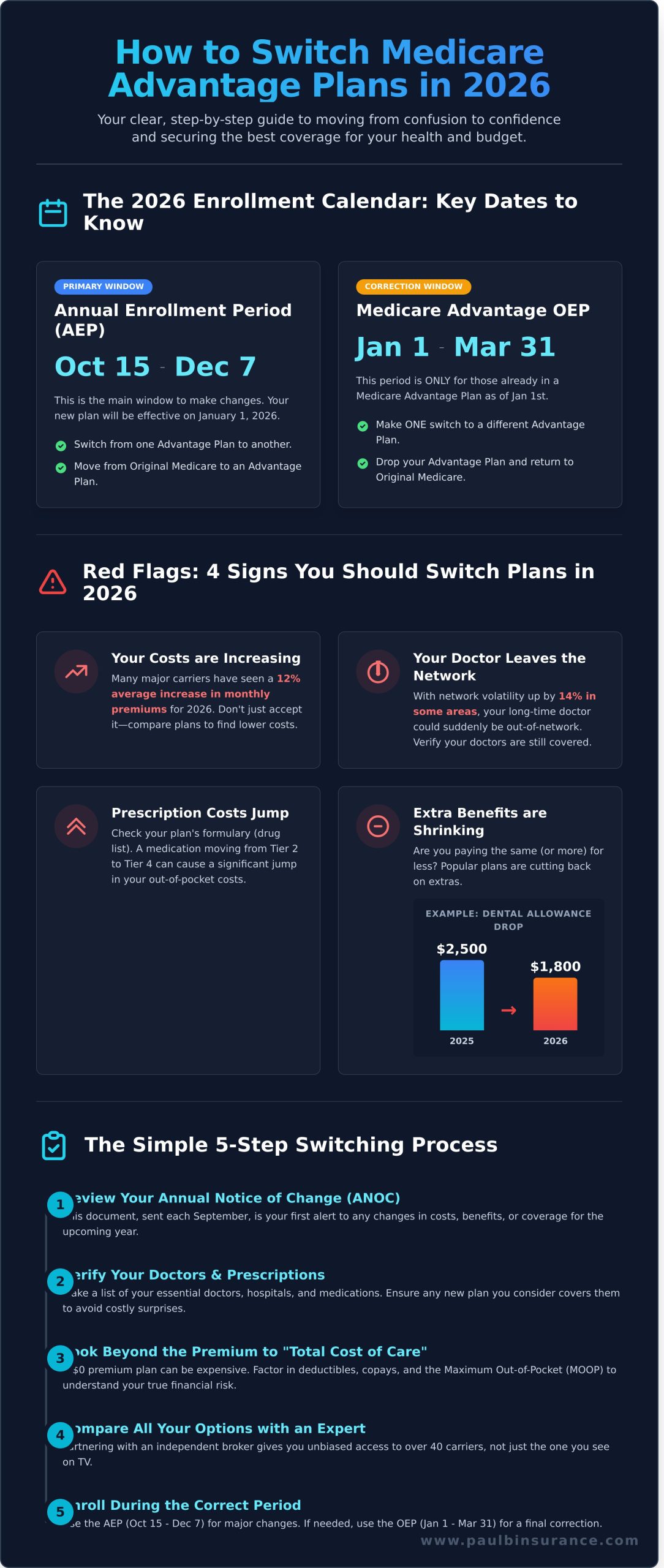

A plan that worked perfectly in 2025 might not be the right fit for your life today. We often see clients shocked when their primary care doctor of 10 years suddenly leaves the network. In 2026, network volatility has increased by 14 percent in many urban areas as providers renegotiate their contracts. You should also check your formulary. This is the list of covered drugs your plan provides. If your specific blood pressure or cholesterol medication moved from a Tier 2 to a Tier 4 cost bracket, your out-of-pocket costs will jump. Many 2026 plans have also scaled back on the extra benefits that people love. We’ve noticed dental allowances dropping from $2,500 to $1,800 in several popular 2026 options. If your benefits are shrinking while your costs grow, it is time to move from confusion to confidence.

The Myth of the “Permanent” Plan

Many people believe they should pick a plan and stay with it forever. We don’t recommend this approach. Your health needs change and the insurance market changes even faster. A yearly coverage checkup ensures you aren’t overpaying for services you don’t use. For example, three new regional providers entered the market on January 1, 2026. These companies are offering lower maximum out-of-pocket limits than the big national brands. If you haven’t looked at the newest market entries, you might be missing out on better protection. We simplify the process of how to switch medicare advantage plans so you can focus on your health instead of the paperwork. We compare your current 2026 costs against every available option to ensure you have the best fit. You can learn more about how these choices are organized in our Medicare Advantage Guide to get a clearer picture of the current landscape. Our goal is to make sure you are never rushed and never pressured.

The 2026 Enrollment Calendar: When Are You Allowed to Switch?

Timing is the most critical factor when you are learning how to switch medicare advantage plans. The calendar dictates your options. If you try to make a change outside of specific windows, you will likely find the door locked. This system often feels like a maze designed to cause stress, but we are here to help you find the clear path. Understanding these dates ensures you stay in control of your healthcare costs and provider access throughout 2026.

The primary window for most people is the Medicare Open Enrollment Period. This runs from October 15 through December 7 every year. During these 54 days, you have the freedom to move from Original Medicare to an Advantage plan, or swap your current Advantage plan for a new one. Any choice you make during this time will take effect on January 1, 2026. If you miss this deadline, you generally cannot make a change for another full year, which could mean staying in a plan that no longer fits your budget or includes your favorite doctors.

AEP vs. OEP: Knowing the Difference

We often see seniors get confused between the Annual Enrollment Period (AEP) and the Medicare Advantage Open Enrollment Period (OEP). Think of the AEP in the fall as the big window where almost anything is possible. The OEP, which runs from January 1 to March 31, 2026, is more of a correction window. It’s specifically for people who are already enrolled in a Medicare Advantage plan as of January 1. During these three months, you can switch to a different Advantage plan or drop your Advantage plan to return to Original Medicare. However, you cannot use this window to switch from Original Medicare to an Advantage plan for the first time. We simplify these rules so you can move from confusion to confidence without the fear of making a mistake.

Qualifying for a Special Enrollment Period (SEP) in 2026

Life doesn’t always follow a set calendar. That is why Medicare provides Special Enrollment Periods for specific life events. These windows typically last for 60 days following a qualifying change. We help our clients identify these opportunities so they don’t lose their protection. Common reasons you might qualify for an SEP in 2026 include:

- Relocating: If you move to a new service area, such as moving from New York to Florida, your current plan might not be available.

- Losing Coverage: If you lose “creditable” coverage from an employer or a union, you have a chance to pick a new plan.

- Plan Changes: If your plan loses its contract with Medicare or if you want to join a plan that has earned a 5-star quality rating from CMS, you may have a special window to act.

Missing these windows can be a costly mistake. If you don’t act during the allowed times, you are generally locked into your current plan for the remainder of the year. This could mean paying higher premiums or seeing doctors who are out of your network. We want to protect you from that anxiety. If you are unsure which window applies to your situation, you can schedule a simple call with us to get unbiased guidance. We take the pressure off by explaining exactly how to switch medicare advantage plans based on your unique 2026 timeline.

A Simple 5-Step Process to Switch Your Medicare Advantage Coverage

We know the Medicare system feels like a maze. It’s often overwhelming to look at a stack of mail and wonder if you’re making the right choice for 2026. Our goal is to move you from confusion to confidence. Learning how to switch medicare advantage plans doesn’t have to be a headache if you follow a logical, patient path. We’ve broken this down into five clear steps to ensure you feel protected and empowered.

- Step 1: Gather your current 2026 list of doctors and medications. Accurate lists are your best defense against unexpected costs. Make sure you have the exact dosages for every pill you take.

- Step 2: Compare the “Total Cost of Care.” Many people get trapped looking only at the monthly premium. We look deeper. A plan with a $0 premium might have a $6,000 out-of-pocket maximum, while a plan with a small premium might cap your costs at $3,500.

- Step 3: Verify network status for your must-have providers. Doctors move between networks often. In 2025, we saw nearly 15% of local provider groups change their insurance affiliations. We’ll help you confirm your favorites are still covered.

- Step 4: Check the new 2026 prescription drug formulary. Drug companies change their “tiers” every January 1. A medication that was affordable last year could jump in price if it moves to a higher tier in 2026.

- Step 5: Complete the enrollment and confirm your start date. Once you’ve made a choice, we handle the paperwork. You’ll receive a confirmation and a new ID card, usually effective the first day of the following month.

Audit Your Health Needs for the Coming Year

Start by creating a detailed medication list. This is the only way to ensure your Part D coverage remains affordable, especially with the 2026 $2,000 out-of-pocket cap on prescriptions. Think about any procedures you have on the horizon. If you’re planning a hip replacement or cataract surgery in the next 12 months, we need to prioritize plans with low co-pays for specialized care. Be honest about the “extras” too. If you don’t use the gym membership or the over-the-counter credits, don’t let those perks distract you from the core medical coverage.

The Final Verification: Avoiding Network Shock

We always suggest calling your doctor’s office directly before you finalize a switch. Ask the billing department if they accept the specific 2026 plan you’ve chosen. This simple phone call can save you from a major headache later. You should also look at “prior authorization” rules. In 2026, some plans have streamlined their 48-hour approval processes, while others have become more restrictive. An independent broker can run a multi-carrier comparison for you in minutes. Unlike a captive agent who only represents one company, we show you the whole picture so you can choose with total clarity.

When you follow this structured approach, the anxiety of the insurance world disappears. We’re here to make sure you know exactly how to switch medicare advantage plans without falling into common traps. You deserve a plan that fits your life, and we’re committed to helping you find it.

Switching Back: Moving from Medicare Advantage to Medigap

Many people we speak with feel a bit restricted by their current network. They realize they want the freedom to visit any doctor in the United States who accepts Medicare without asking for permission. This desire for total flexibility often leads them back to Original Medicare. While Advantage plans offer low premiums, a Medigap plan provides the security of predictable monthly costs. You won’t have to worry about a surprise $325 hospital co-pay or a $60 specialist fee every time you need care. We find that this predictability brings an immense sense of peace to the seniors we serve.

We understand that the process feels heavy. Understanding how to switch medicare advantage plans to get back to a supplement requires careful timing and a clear strategy. If you make a mistake, you could end up with a gap in coverage or a permanent late enrollment penalty. Our goal is to take that weight off your shoulders and make the transition seamless. We simplify the jargon so you know exactly how the move works before you sign a single document.

The Reality of Medical Underwriting in 2026

In 2026, most seniors must pass medical underwriting to buy a Medigap policy if they are leaving an Advantage plan. This means the insurance company asks about your health history. If you have chronic conditions or have had a recent major surgery, they can charge more or even deny you a policy. Only 4 states, including New York and Connecticut, currently provide “Guaranteed Issue” rights that protect you from these questions year-round. For everyone else, the financial risk of leaving an Advantage plan without securing a Medigap safety net first is too high. We always check your health eligibility before you cancel your current plan.

The “Trial Right” period is a vital exception we monitor for our clients. If you joined a Medicare Advantage plan for the first time and decide within the first 12 months that it isn’t right for you, you have a special right to switch back. No health questions are allowed during this 365-day window. It is a one-time safety net that lets you test the waters without losing your chance at supplemental coverage. We help you track these dates so you never miss your chance to change your mind.

The Advantage-to-Medigap Checklist

Moving back to Original Medicare involves several moving parts that must sync up perfectly. We use this checklist to ensure nothing falls through the cracks:

- Coordinate the dates: Your Medigap policy should start the very first day your Advantage plan ends. This ensures you never spend a single day without protection.

- Select a Part D plan: Since Medigap does not include prescriptions, you must join a standalone drug plan. Missing this step leads to a lifetime penalty that increases your costs every month.

- Verify your doctors: We confirm your preferred specialists accept Original Medicare so you can enjoy your new freedom immediately.

We often suggest this switch for clients who travel or want the best possible access to specialized centers like the Mayo Clinic. It replaces the “crazy maze” of prior authorizations with a simple, direct path to care. When you learn how to switch medicare advantage plans with the help of an expert, you gain the confidence that your healthcare is secure. If you want to move from confusion to a clear plan for your future, schedule a call with Paul today.

Why Partnering with an Independent Broker Makes Switching Stress-Free

Deciding how to switch medicare advantage plans involves more than just picking a new name from a list. It requires understanding who is actually sitting across the table from you. In the 2026 insurance market, you will encounter two main types of professionals: captive agents and independent brokers. A captive agent works for one specific insurance company. They are trained to sell you that company’s products, even if a competitor offers a lower deductible or better dental coverage. At The Modern Medicare Agency, we believe you deserve better than a limited menu.

As independent brokers, we at The Modern Medicare Agency don’t work for the insurance companies; we work for you. We have spent years building relationships with over 40 different carriers. This means when we sit down to review your 2026 budget, our team isn’t trying to squeeze you into a pre-selected box. We compare dozens of options side-by-side to find the specific plan that covers your doctors and keeps your prescriptions affordable. Our process at The Modern Medicare Agency is built on a foundation of being never rushed and never pressured. We stay by your side throughout the entire year, not just during the enrollment window. If a claim gets stuck or a provider leaves your network in July, our team is the one who picks up the phone to fix it.

Personalized Guidance vs. 1-800 Call Centers

Many seniors are bombarded with mailers from national 1-800 call centers. These “big box” insurance hotlines often miss the critical local nuances that affect your care. A representative in a different time zone might not realize that a major local hospital system changed its contract status for 2026. At The Modern Medicare Agency, we live and work in your community. We know the local networks and can explain the jargon in plain English. This personalized approach ensures you choose your coverage with total confidence, knowing your history is respected and your specific needs are met.

Your Next Steps to Confidence

The journey from confusion to confidence is shorter than you might think. While the 2026 Medicare landscape has seen out-of-pocket maximums shift significantly, you don’t have to navigate these changes alone. Our team at The Modern Medicare Agency has helped thousands of clients move away from the stress of the “insurance maze” and into a plan that provides genuine peace of mind. You don’t need to spend hours scrolling through confusing websites or comparing fine print on your own.

- We analyze your current medications against 2026 formularies to prevent pricing surprises.

- We verify that your preferred specialists remain in-network for the coming year.

- We identify plans with extra benefits like transportation or home safety modifications that fit your lifestyle.

A simple 15-minute call can be the difference between a stressful year and one where you feel completely protected. In that short time, we can often identify savings that reduce your 2026 out-of-pocket costs by thousands of dollars. If you are ready to stop worrying about how to switch medicare advantage plans and start feeling empowered, The Modern Medicare Agency is here to help. Schedule a Call With The Modern Medicare Agency to review your 2026 options today and take the first step toward a worry-free future.

Take Charge of Your 2026 Healthcare Journey

Navigating the 2026 Medicare landscape doesn’t have to be a source of stress. We’ve shown you that by tracking the enrollment calendar and following our simple 5-step process, you can move from confusion to complete confidence. Whether you’re looking for lower costs or better provider access, understanding how to switch medicare advantage plans is the first step toward securing the peace of mind you deserve this year. It’s about finding a plan that fits your life; not the other way around.

We’re here to make sure you never feel overwhelmed by the maze of insurance options. Our team provides independent access to over 40+ insurance carriers and offers licensed, local guidance across 34+ states. You’ll receive a “Never Rushed, Never Pressured” experience that puts your specific health needs first. Don’t let another enrollment period pass by with a plan that isn’t a perfect match for your budget. Schedule Your 2026 Medicare Review with Paul Barrett today to simplify your coverage. We’re ready to help you find the clarity you’ve been looking for.

Frequently Asked Questions

Can I switch Medicare Advantage plans at any time of the year?

No, you can only switch during specific enrollment windows. You can use the Annual Enrollment Period from October 15 to December 7, 2025, for a January 1, 2026 start date. There is also the Medicare Advantage Open Enrollment Period from January 1 to March 31, 2026. Outside these two windows, you need a Special Enrollment Period, which 15% of beneficiaries qualify for due to moving or losing employer coverage.

Will I lose my current doctor if I switch my Medicare Advantage plan?

You only lose your doctor if they aren’t in the new plan’s network. Before you decide how to switch medicare advantage plans, we check your specific doctors against the 2026 provider directories. Since 25% of doctors may change their network status each year, we verify this first. This step ensures you keep the medical team you trust while finding a plan that fits your budget better.

Is there a penalty for switching Medicare Advantage plans in 2026?

There is absolutely no financial penalty for switching your plan in 2026. Medicare allows you to change your coverage for free during the approved enrollment windows. You won’t pay a $1 fee to leave your current carrier. We help you compare the 43 different plan options available in many counties to ensure you’re getting the best value without any hidden costs or surprise fees.

What is the “Medicare Advantage Open Enrollment Period” exactly?

The Medicare Advantage Open Enrollment Period is a 90 day window from January 1 to March 31. During this time, you can make a one time change if you’re already in a Medicare Advantage plan. You can switch to a different Advantage plan or return to Original Medicare. We use this period to help 1 in 10 clients who realize their current plan doesn’t meet their 2026 health needs.

Do I need to notify my old insurance company when I switch plans?

You don’t need to send a cancellation letter or call your old insurance company. When you enroll in a new plan, the Medicare system automatically notifies your previous carrier to end your coverage on the last day of the month. This seamless transition prevents any gaps in your 2026 healthcare. We manage the paperwork to ensure your new ID card arrives before your old coverage expires.

Can I switch from a Medicare Advantage plan to a Medigap plan in 2026?

You can switch to Medigap, but you’ll likely need to answer health questions. In 2026, unless you’re in a “trial period” or have a specific guaranteed issue right, private insurers can deny coverage based on your medical history. We review the 10 standard Medigap plans with you to see if you qualify. This move often requires a 30 day notice to your current Advantage plan to ensure a smooth transition.

What happens to my prescription drug coverage when I switch Advantage plans?

Your prescription coverage is bundled into your new plan. Most 2026 Medicare Advantage plans include Part D benefits, so your drug list and pharmacy network will change to the new company’s rules. We run your current medications through the 2026 formulary tools to ensure your costs don’t spike. This protects you from the 20% price variations we often see between different insurance carriers for the same medications.

How much does it cost to use a Medicare broker to help me switch?

It costs you exactly $0 to work with an independent broker like us. We’re paid directly by the insurance companies, and your monthly premium remains the same whether you use our expert guidance or go it alone. Learning how to switch medicare advantage plans with a professional means you get unbiased advice at no personal expense. We’ve helped over 1,000 seniors find peace of mind without charging a single fee.