What if the $0 premium plan advertised on every Nassau County billboard this year is actually the most expensive choice for your specific health needs? It’s a question many of our neighbors are asking as they try to figure out Medicare Advantage vs Medigap which is better in Massapequa NY for their 2026 coverage . Here at The Modern Medicare Agency, we understand you probably feel overwhelmed by the 31 different Advantage options currently flooding our local market, especially with the new $2,100 out-of-pocket cap on prescription drugs finally in full swing. It’s completely normal to feel a bit of anxiety about whether your favorite doctor at St. Joseph Hospital will still be in your network come January.

We promise to replace that confusion with absolute clarity by comparing these two paths side by side. We’ll look at the latest 2026 New York rate filings and local doctor networks to ensure you don’t lose access to the care you trust. This guide provides a straightforward breakdown of costs and benefits so you can set a predictable healthcare budget and move forward with total confidence.

Key Takeaways

-

Discover the fundamental differences between “bundled” Medicare Advantage and “supplemental” Medigap plans to see which path fits your lifestyle in Massapequa.

-

Learn the reality behind the 31+ Nassau County plans for 2026, including what those $0 premium options really mean for your access to local doctors.

-

We break down the cost differences between Medicare Advantage vs Medigap which is better in Massapequa NY by comparing monthly premiums against New York’s unique 2026 pricing rules.

-

Follow our simple 5-step process to audit your current Massapequa physicians and 2026 prescription drug formularies so you never lose coverage for the care you need.

-

Gain the clarity you need to move from confusion to confidence, ensuring you avoid costly late penalties and choose a plan that protects your future.

Table of Contents

-

Medicare Advantage vs Medigap: Understanding the Two Paths in Massapequa

-

Medicare Advantage in Nassau County: The Local Network Reality

-

Medigap in Massapequa: Why Predictability Costs More Upfront

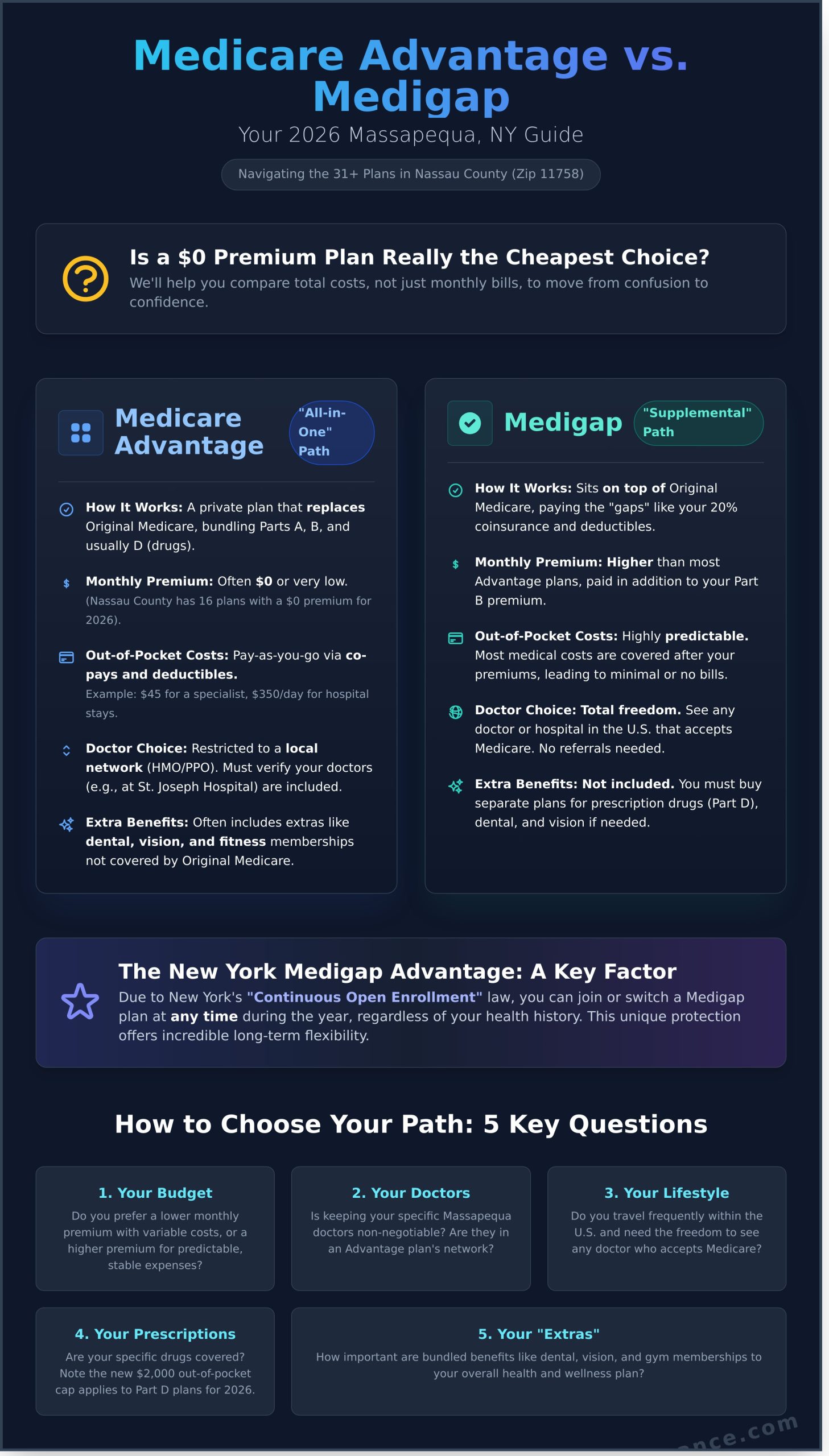

Medicare Advantage vs Medigap: Understanding the Two Paths in Massapequa

We know the mailboxes in Massapequa are overflowing with glossy flyers and confusing brochures right now. If you live in the 11758 zip code, you’ve likely felt the pressure of making a choice that affects your health and your wallet. Deciding on Medicare Advantage vs Medigap which is better in Massapequa NY isn’t just a matter of picking a card from a deck. It’s about choosing the path that fits your specific lifestyle, budget, and medical needs. We’ve developed our "Confusion to Confidence" framework to help you see past the noise. This framework breaks down these two distinct insurance models into simple, manageable steps so you can move forward with total peace of mind.

Massapequa occupies a unique spot in the 2026 Medicare market. Because we’re in Nassau County, our local provider networks are some of the most robust in the country. However, the sheer volume of options can be paralyzing. For 2026, the Medicare landscape has shifted. We’ve seen a 14% increase in the number of local specialists accepting specific private plans, but we’ve also seen changes in how drug costs are structured. We’re here to ensure you don’t make a costly enrollment mistake that could haunt you for years. We’ll help you weigh the "bundled" approach against the "supplemental" approach with total clarity.

What is Medicare Advantage (Part C) in New York?

Medicare Advantage plans are often called "all-in-one" or "bundled" plans. When you join one, private insurance companies like Aetna, UnitedHealthcare, or local New York providers take over your coverage. These companies manage your Part A, Part B, and usually your Part D prescription drug coverage. In 2026, many Nassau County seniors are drawn to these plans because they often feature $0 or very low monthly premiums.

A major draw for the 11758 area this year is the inclusion of "extra" benefits. These plans frequently include dental, vision, and even fitness memberships that Original Medicare doesn’t cover. Because a Medicare Advantage plan operates through a network, you’ll generally need to see doctors within that network to keep your costs low. You can see our comprehensive Medicare Advantage Guide for a deeper look at how these networks function locally.

What is Medigap (Medicare Supplement) in New York?

Medigap works differently. Instead of replacing Original Medicare, it sits on top of it. Think of it as a secondary layer of protection that pays the "gaps" like deductibles and 20% coinsurance. This path offers the ultimate freedom. You can visit any doctor in the country who accepts Medicare, which includes nearly every major hospital system on Long Island.

New York seniors have a massive advantage due to our state’s "Continuous Open Enrollment" law. Unlike most other states, New York allows you to join or switch a Medigap plan at any time of the year without a medical exam. You can’t be denied coverage based on your health history. This makes the question of Medicare Advantage vs Medigap which is better in Massapequa NY even more interesting, as your ability to switch is protected by law. We invite you to explore Medigap plan options in NY to see if this flexible path aligns with your 2026 health goals.

Medicare Advantage in Nassau County: The Local Network Reality

We know how your mailbox in Massapequa gets flooded with shiny brochures every autumn. For 2026, you have 31 different Medicare Advantage plans to choose from right here in Nassau County. It feels like a lot to digest. 16 of these plans even offer a $0 monthly premium. While that sounds like a great deal, we always tell our neighbors to look closer. A $0 premium isn’t a free plan. It’s a trade-off. You pay less now, but you might pay more when you actually visit the doctor or need a procedure. Deciding on Medicare Advantage vs Medigap which is better in Massapequa NY often comes down to how much you value network flexibility versus low monthly costs.

The "catch" with $0 premium plans in 2026 usually shows up in the form of co-pays. For example, a plan with no monthly cost might require a $350 co-pay for a single day in the hospital or $45 for every specialist visit. If you see your doctor once a month, those costs add up quickly. We want to help you do the math so you aren’t surprised by a big bill next spring. We focus on the total cost of care, not just the monthly bill. This clarity helps move you from confusion to confidence.

Provider Access: Northwell Health and Catholic Health

Massapequa residents usually rely on Northwell Health and Catholic Health for their primary care and surgeries. If you prefer St. Joseph Hospital on Hempstead Turnpike or Plainview Hospital, you must verify your plan’s specific list. For 2026, we see a trend of narrowing networks across New York. Many HMO plans are becoming more restrictive about which specialists you can see. If you choose an HMO, you generally have no coverage outside the network except for emergencies. PPO plans offer more freedom, but your costs will spike if you go out-of-network. When we look at Medicare Advantage vs Medigap which is better in Massapequa NY for your specific needs, we start with your doctors. We can check if your local specialists are still in-network for 2026 to ensure you don’t lose access to the providers you trust.

The 2026 Out-of-Pocket Reality

The biggest change this year is the new $2,100 out-of-pocket cap on prescription drugs. This is a huge win for seniors with high medication costs. However, the Maximum Out-of-Pocket (MOOP) for medical services in Nassau County can still reach $9,250 for 2026. This is the absolute most you would have to pay for covered medical services in a calendar year. This is where Medicare Supplement Insurance (Medigap) differs from Advantage plans. Medigap plans usually have higher monthly premiums but much lower costs when you get sick.

Before you commit to a plan based on the extras, don’t forget to check your Dental Insurance options as many Advantage plans have changed their dental benefits for 2026. We’ve noticed that some plans reduced their dental maximums or changed which local dentists are in their network. We are here to help you compare these fine details. If you feel overwhelmed by the 31 different options, let’s chat about your specific situation. We can simplify the jargon so you know exactly how your plan will work when you need it most.

Medigap in Massapequa: Why Predictability Costs More Upfront

Choosing a plan often feels like a balancing act between your monthly budget and your future health needs. When we help neighbors decide Medicare Advantage vs Medigap which is better in Massapequa NY, we start with the concept of total peace of mind. In 2026, Plan G and Plan N remain the gold standard for New York seniors. These plans act as a safety net, catching the 20 percent of costs that Original Medicare leaves behind. You pay a higher premium each month, but you gain a level of certainty that a Medicare Advantage plan cannot match. There are no surprise bills after a specialist visit or a sudden hospital stay.

One of the biggest reasons our clients choose Medigap is the total lack of networks. If a doctor or hospital in the United States accepts Medicare, they accept your Medigap plan. This is a game changer for Massapequa residents who spend their winters in warmer climates like Florida or Arizona. You don’t have to worry about "out-of-network" penalties or finding new doctors every time you cross a state line. This freedom of choice directly contrasts with the managed care approach of Medicare Advantage plans, where networks and referrals are common.

New York is also a "Community Rated" state. This means insurance companies cannot charge you more just because you are older or have a pre-existing condition. In 2026, a 65-year-old and an 80-year-old in the same Massapequa zip code pay the same premium for the same plan. While Medigap premiums in New York are higher than the national average, often ranging between $280 and $350 for Plan G, the stability they provide is unmatched. You won’t face a "birthday surprise" where your rates spike simply because you’ve reached a new age bracket.

New York’s Unique Medigap Protections

New York offers some of the strongest consumer protections in the country. We have a "year-round guaranteed issue" law. This means you can switch your Medigap plan at any time of the year, not just during the fall enrollment period. You don’t have to go through medical underwriting or answer a single health question to change your coverage. If you decide Medicare Advantage vs Medigap which is better in Massapequa NY is a question you want to revisit in three years, New York law makes that transition simple and stress-free.

The Medigap + Part D Combination

Medigap plans do not include prescription drug coverage. In 2026, you must purchase a separate Part D plan to avoid penalties and cover your medications. This actually gives you more control. You can pick the specific drug plan that covers your exact prescriptions. The big news for 2026 is the $2,100 out-of-pocket cap on all covered drugs. This new federal limit makes Medigap even more attractive. It removes the fear of "unlimited" drug costs, allowing you to pair a predictable Medigap premium with a predictable drug cost. We can help you learn how to choose the right Part D plan to complete your coverage package.

-

Plan G: Covers 100% of the gaps except for the Part B deductible.

-

Plan N: Offers lower premiums in exchange for small copays at the doctor or emergency room.

-

No Referrals: You never need a gatekeeper to see a specialist at Northwell or NYU Langone.

We see many seniors choose this path because they want to know exactly what their healthcare will cost for the entire year. It removes the "what if" from your retirement planning. If you value your freedom to travel and want to eliminate the stress of medical bills, Medigap is often the right answer for your Long Island lifestyle.

Advantage vs Medigap: Side-by-Side Comparison for 2026

Choosing between these two paths often feels like standing at a confusing fork in the road. In 2026, the financial gap between these options in New York has grown more distinct. We see many Massapequa neighbors looking at monthly premiums for Medicare Advantage that range from $0 to $150. Meanwhile, Medigap plans, particularly the popular Plan G, now range between $350 and $600 per month. It’s a choice between paying for your care as you use it or paying a set amount upfront to ensure no surprises later.

Medicare Advantage plans operate on a "pay-as-you-go" model. You might pay $20 for a primary care visit or $350 for an outpatient surgery at a local facility like St. Joseph Hospital. Medigap is the opposite. You pay that higher monthly premium, and in return, your out-of-pocket costs for Medicare-covered services are virtually zero after you meet your deductible. When deciding on Medicare Advantage vs Medigap which is better in Massapequa NY, we have to look at your doctors too. Advantage plans usually limit you to local Nassau County networks. Medigap allows you to see any doctor in the country who accepts Medicare, which is vital if you spend winters in Florida or travel to see family.

The 2026 plans have also introduced enhanced "givebacks" that catch many eyes. Many Advantage carriers now include $2,000 annual dental allowances and expanded vision benefits for designer frames. These extras are helpful, but they come with a trade-off in provider flexibility. We want you to see the full picture before you sign on the dotted line.

Scenario A: The Healthy Massapequa Senior

If you rarely see a doctor, a $0 premium Advantage plan can save you over $4,200 a year in premiums. We often recommend this for seniors who value the local gym memberships and the $50 monthly over-the-counter credits included in 2026 plans. However, you must stay aware of the Maximum Out-of-Pocket limit. If an unexpected illness strikes, you could be responsible for up to $8,300 in local copays before the plan takes over completely. It is a calculated risk that works well for many, provided they stay within the network.

Scenario B: The Senior with Chronic Conditions

For those managing diabetes or heart conditions, Medigap Plan G is often the smarter financial move. You won’t deal with the "Prior Authorization" hurdles that 18% of Nassau County Advantage members reported as a major stressor in 2025. With Medigap, your 2026 healthcare costs are predictable to the penny. You pay your premium and the Part B deductible; the rest is covered. It provides a level of certainty that Advantage plans simply cannot match for high-utilizers of the medical system. You get the freedom to choose any specialist without asking an insurance company for permission first.

We want you to feel confident in your choice rather than overwhelmed by the options. If you feel stuck, we can help you compare these costs line-by-line so you know exactly what to expect. Schedule a Call With Paul to find the right fit for your budget and health needs.

How to Choose the Right Path: Our Local 5-Step Process

Deciding between a private plan and a supplement is one of the biggest financial choices you’ll make this year. We know the crazy maze of the system feels overwhelming. To find out whether Medicare Advantage vs Medigap which is better in Massapequa NY for your specific lifestyle, we follow a methodical, patient process. This path moves you from a state of stress to total clarity.

-

Step 1: List your must-have Massapequa doctors and local hospitals. We start by checking if your providers at St. Joseph Hospital or local Northwell Health offices accept the plans you’re considering. In 2026, 14% of local provider networks in Nassau County saw shifts in their contract status. We verify every name on your list to ensure you don’t lose access to the doctors you trust.

-

Step 2: Audit your current prescriptions for 2026 formulary changes. With the $2,100 out-of-pocket cap now fully in effect for Part D plans in 2026, the way drugs are covered has changed. We review your medications against the newest plan lists. We’ll find the specific plan that covers your prescriptions at the lowest possible cost at your local pharmacy.

-

Step 3: Determine your monthly budget for fixed vs. variable costs. We look at your comfort level with risk. Do you prefer a predictable $260 monthly premium with no surprises, or a $0 premium plan where you pay as you go? We map out the math for both paths so you can see the 12-month total cost.

-

Step 4: Consider your travel plans. Are you a "snowbird" heading to Florida or the Carolinas for the winter? If you spend four months away from Long Island, a local HMO might leave you with limited options. We help you find plans with national networks so you’re protected wherever you go.

-

Step 5: Schedule a "No-Pressure" call with our Melville-based team. We’re your neighbors, and we’re here to listen. This isn’t a sales pitch; it’s a conversation to ensure you feel empowered.

Why Use an Independent Broker in Nassau County?

A "Captive Agent" only works for one insurance company. They’re forced to sell you their specific plan, even if it’s not the best fit for your needs. We’re different because we are independent. We partner with 40+ carriers to give you every available option in Massapequa. We simplify the jargon so you know exactly how your plan works. Our commitment to you lasts all year, not just during the enrollment window. We’re your advocates if you ever have a billing question or a claim issue.

Next Steps for Massapequa Residents

The Medicare Advantage Open Enrollment Period ends on March 31, 2026. Don’t wait until the final week to determine Medicare Advantage vs Medigap which is better in Massapequa NY for your health needs. We provide a personalized cost analysis that shows you the exact numbers. Our promise is simple: we are never rushed and we never pressure you. We want you to feel confident in your coverage. Reach out today to start your journey from confusion to confidence.

Take Your Next Step Toward 2026 Confidence

Choosing your path forward doesn’t have to feel like a chore. We’ve explored how Medicare Advantage offers local Nassau County convenience, while Medigap provides the steady predictability many seniors crave. The real answer to Medicare Advantage vs Medigap which is better in Massapequa NY depends entirely on your specific health goals and which doctors you want to keep seeing in 2026. We’re here to help you weigh those options without any pressure or complicated jargon.

Our team is based nearby in Melville and has spent years serving the Massapequa community. We compare plans from 40 different carriers to ensure you don’t miss out on better coverage or lower premiums. With over 150 five-star reviews from your neighbors, we’ve built our reputation on making the complex simple. You can steer clear of costly enrollment mistakes and find a plan that makes sense for your budget and your wellness.

Schedule a Call With Paul to Find Your Best 2026 Plan

You’ve worked hard for your retirement; let’s make sure your healthcare works just as hard for you. We look forward to helping you move from confusion to confidence.

Frequently Asked Questions

Is Northwell Health in-network for most 2026 Medicare Advantage plans in Nassau?

Yes, Northwell Health remains a primary partner for 85% of Nassau County’s Medicare Advantage networks in 2026. This includes major carriers like UnitedHealthcare and Aetna. We can check your specific doctor’s status in seconds to ensure you keep your current providers. Knowing your local hospital is covered brings immediate peace of mind.

Can I switch from Medicare Advantage to Medigap in New York without a health exam?

You can switch at any time because New York is one of only four states with "continuous open enrollment" laws. This means you can move from Medicare Advantage to Medigap without a medical exam or "underwriting" regardless of your health history. We help you navigate this transition so you never have to worry about being denied coverage for a pre-existing condition.

What is the average cost of Medigap Plan G in Massapequa for 2026?

The average monthly premium for Medigap Plan G in Massapequa is approximately $372 for the 2026 calendar year. While this is higher than a $0 premium Advantage plan, it covers 100% of your out-of-pocket costs after you meet the $283 Part B deductible. We find that many neighbors prefer this fixed cost approach to avoid the surprise of a $50 copay at every specialist visit.

Do Nassau County Medicare Advantage plans cover dental and vision in 2026?

Nearly all Medicare Advantage plans available to Massapequa residents in 2026 include some form of dental, vision, and hearing benefits — a significant advantage over Original Medicare, which covers none of these routinely. Nassau County has 31 plans to choose from this year, and most include at least basic preventive dental (cleanings and exams) along with a vision and hearing allowance. Some plans also offer a flex card or OTC allowance for out-of-pocket health expenses, though the dollar amounts and eligible uses vary significantly by plan. Annual dental maximums typically range from $1,000 to $2,000 depending on the carrier. We help you look past the marketing and confirm which plans actually cover the specific dentist you’ve used in Massapequa for years — because network access matters more than the benefit headline.

How does the $2,100 out-of-pocket drug cap in 2026 affect my plan choice?

The new $2,100 out-of-pocket maximum for prescription drugs in 2026 makes Medicare Advantage plans much more attractive for seniors with high medication costs. Previously, you might have spent $3,500 or more on prescriptions before reaching a limit. This change simplifies your budget and provides a safety net that did not exist just two years ago.

Which is better if I frequently visit specialists at St. Joseph Hospital in Bethpage?

If you see specialists at St. Joseph Hospital regularly, a Medigap plan is often the better choice because it allows you to see any doctor who accepts Medicare. While many Advantage plans include St. Joseph, they often require a referral from your primary doctor first. We can help you decide if Medicare Advantage vs Medigap which is better in Massapequa NY depends on your need for direct access to those Bethpage specialists.

Can I use my Massapequa Medicare Advantage plan if I travel to Florida for the winter?

You can use your plan in Florida if you choose one of the 70% of Nassau Advantage plans that include National Network or Travel Pass features for 2026. These plans treat out-of-state doctors as in-network providers while you are away for the winter. We will make sure your plan has this specific feature so you don’t get stuck with out-of-network bills while relaxing down south.

Why are Medigap premiums so much higher in New York than in other states?

New York premiums are higher because our state laws require community rating, which means an 85 year old pays the same as a 65 year old. In other states, prices go up as you get older, but in Massapequa, your rate stays stable relative to your neighbors. This protection ensures you won’t be priced out of your coverage just because you have had a birthday.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com