What if the plan your neighbor swears by is actually costing you an extra $600 a year in unnecessary premiums? As we move through 2026, many seniors feel like they are stuck in a maze of fine print and rising costs. You just want to enjoy your retirement without worrying about a surprise $1,500 hospital bill or a massive rate hike hitting your mailbox. We know how overwhelming it feels to compare Plan G and Plan N while insurance companies keep shifting the goalposts. You deserve a plan that protects your savings and offers true peace of mind.

We are here to simplify the jargon and show you exactly what are the top 5 Medicare Supplement plans for seniors this year. Our team has analyzed the latest 2026 rate filings to find the options that offer the best protection against out-of-pocket expenses. We will break down the specific benefits of each plan so you can make a choice that is truly future-proof. By the end of this article, you will have a clear path from confusion to confidence.

Key Takeaways

-

We answer what are the top 5 Medicare Supplement plans for seniors? by simplifying the 2026 landscape and focusing on plans that give you total freedom to choose your own doctors.

-

Understanding what are the top 5 Medicare Supplement plans for seniors? involves comparing the "Gold Standard" coverage of Plan G against the budget-friendly flexibility of Plan N.

-

When asking what are the top 5 Medicare Supplement plans for seniors?, learn why a company’s rate stability is just as important as the plan letter for protecting your retirement savings.

-

Our decision framework helps you determine for yourself what are the top 5 Medicare Supplement plans for seniors? by matching your personal risk tolerance and travel plans with a plan that offers lasting value.

-

Our "never rushed, never pressured" approach makes finding out what are the top 5 Medicare Supplement plans for seniors? a clear, stress-free path toward a confident retirement.

Table of Contents

-

Understanding the Basics of Medicare Supplement Plans in 2026

-

Moving from Confusion to Confidence with The Modern Medicare Agency

Understanding the Basics of Medicare Supplement Plans in 2026

We know that staring at a pile of insurance mail can feel like wandering through a thick fog. It is stressful and overwhelming to figure out which path leads to actual security. Our goal is to clear that fog immediately. Medicare Supplement plans, often called Medigap, are designed to work hand-in-hand with your Original Medicare. Think of Original Medicare as the foundation of your house and Medigap as the roof and walls that protect you from the elements. Medigap is private insurance that pays the bills Original Medicare leaves behind.

In 2026, the financial stakes are higher than ever. The Part B deductible has adjusted to $283 this year, and without a supplement, you are responsible for 20% of nearly every medical service you receive outside of a hospital stay. We recommend Medigap for seniors who want to trade uncertainty for a fixed monthly budget. When clients ask us, What are the top 5 Medicare Supplement plans for seniors? they are usually looking for a way to stop the surprise bills that come with doctor visits and lab tests. These plans bridge the gap for deductibles, copays, and coinsurance so you never have to worry about the cost of a specialist visit.

One rule is absolute: Medigap only works with Original Medicare. If you are currently enrolled in a Medicare Advantage plan, you cannot use a supplement plan. We help you decide which path fits your life, but we often find that those who value total freedom of choice prefer the Original Medicare and Medigap combination. It keeps you in control of your healthcare decisions rather than an insurance company’s network manager.

Standardized Coverage: The ‘Letter’ System Explained

The government regulates these plans strictly to protect you from confusing fine print. Every plan is categorized by a letter, such as Plan G, Plan N, or Plan High-Deductible G. Because of these federal standards, a Plan G with one company has the exact same medical benefits as a Plan G with any other company. We simplify the jargon so you can focus on what matters: the premium price and the company’s reputation for stable rates. For a deeper dive into how these categories were established, Understanding Medigap Plans provides a helpful historical overview of the standardized system. We use this transparency to ensure you never pay more than necessary for the exact same level of care.

Why 2026 is a Great Year to Secure Your Coverage

The 2026 landscape has made Medicare Supplement Insurance even more vital for your peace of mind. With the final implementation of the $2,100 out-of-pocket cap on prescription drugs under the Inflation Reduction Act, seniors now have a clearer picture of their total annual costs. By adding a Medigap plan, you effectively cap your medical expenses too. This creates a complete safety net against rising healthcare costs, which have increased by 4.2% on average over the last year.

The biggest advantage in 2026 remains the freedom to see any doctor in the U.S. that accepts Medicare. You don’t need a referral to see a cardiologist in another state or a specialist across town. If you are still wondering, What are the top 5 Medicare Supplement plans for seniors? stay with us as we break down the specific options that provide this level of liberty. We are here to move you from a state of confusion to a state of absolute confidence.

The Top 5 Medicare Supplement Plan Letters for Seniors

Choosing a Medigap policy feels like trying to solve a puzzle with missing pieces. We see seniors every day who feel overwhelmed by the alphabet soup of plan letters. Our goal is to move you from a state of confusion to a place of total clarity. When people ask us, "What are the top 5 Medicare Supplement plans for seniors?" we focus on the options that provide the most security for your specific lifestyle. In 2026, the landscape remains steady, but the costs have shifted slightly. We want to make sure you have the facts to protect your savings.

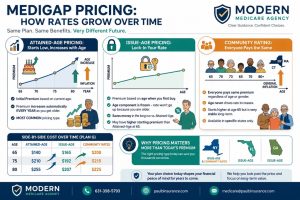

Plan G: Why It Remains the #1 Choice

Plan G is the gold standard for a reason. We recommend it to about 80% of our clients because it offers the most comprehensive coverage available to new retirees. It covers every single gap in Medicare except for the Part B deductible. For 2026, the Part B deductible is $283. Once you pay that initial amount for the year, your Plan G picks up 100% of your Medicare-covered expenses. You can visit the official Medicare website to see how this compares to other letters, but the simplicity of Plan G is hard to beat. You never have to worry about a surprise bill from a doctor or a hospital. It provides the peace of mind that most of our clients value above all else.

Plan N: The Best Value for the Budget-Conscious

If you want lower monthly premiums and don’t mind a little "skin in the game," Plan N is a fantastic alternative. It covers the same big items as Plan G, but you agree to pay small copays. You will pay up to $20 for some office visits and up to $50 for an emergency room visit that doesn’t result in an inpatient stay. We find that seniors who visit the doctor less than six times a year often save more on premiums than they spend on copays. A common concern is "excess charges," which happen if a doctor charges more than the Medicare-approved amount. However, in 2026, 96% of providers nationwide accept Medicare assignment, meaning they won’t charge those extra fees. We can help you find confidence in your coverage by checking if your local doctors fall into this category.

While Plan G and Plan N lead the pack, three other options serve specific needs for 2026 beneficiaries:

-

Plan F: This is the only plan that covers the Part B deductible. It’s only available if you were eligible for Medicare before January 1, 2020. If you have it, you can keep it, but we often find the premium increases in 2026 make Plan G a more logical financial choice.

-

High-Deductible Plan G: This is the "catastrophic" version of Plan G. You get the same great coverage, but only after you pay a 2026 deductible of $2,950. It’s an excellent choice for very healthy seniors who want the lowest possible monthly bill.

-

Plans K and L: These are the "shared cost" plans. Plan K pays 50% of most gaps, while Plan L pays 75%. They have annual out-of-pocket limits that protect you if you have a major health event. They are less common, but they offer a middle ground for those who want to split the risk with the insurance company.

When you look at what are the top 5 Medicare Supplement plans for seniors? you have to look at your own health history and your monthly budget. We take the time to walk through these numbers with you. We don’t use high-pressure tactics because we believe an educated client is a confident client. Whether you choose the full protection of Plan G or the savings of Plan N, we are here to ensure you never feel alone in this process.

Evaluating the Best Medigap Insurance Carriers for 2026

We know the Medicare system often feels like a crazy maze. While the government standardizes the benefits for each lettered plan, the name on your ID card still matters deeply. A Plan G from one company provides the exact same medical coverage as a Plan G from another, but your experience with premium increases and customer service will be vastly different. We help you look past the shiny brochures to see which companies actually stand by their promises. When people ask us, what are the top 5 Medicare Supplement plans for seniors? we tell them that the carrier’s reputation is just as vital as the plan letter itself.

Rate stability is the most important factor we analyze for our clients. It is easy for a company to offer a low price to a 65-year-old in 2026, but we look at what that price will be when you are 75 or 85. We track the 5-year history of price hikes for every major carrier. If a company has a pattern of 12% annual increases, we generally advise you to look elsewhere. We want you to feel a sense of security, not a sense of dread every time a renewal notice arrives in your mailbox.

Financial strength ratings from agencies like A.M. Best provide a window into a company’s future. We prioritize carriers with an "A" rating or higher. This score indicates the company has the cash reserves to pay claims quickly and survive economic shifts. This Forbes analysis of Medigap carriers confirms that financial backing is a cornerstone of a reliable plan. We also look for household discounts that can save you between 5% and 15% on your monthly premiums. In 2026, these discounts are more flexible than ever, often applying even if your spouse isn’t on the same plan.

Top-Rated Carriers We Trust

AARP and UnitedHealthcare continue to lead the market in 2026 because of their massive stable pool of members. With over 13 million seniors enrolled, they spread risk effectively, which often leads to more predictable rate changes. Mutual of Omaha remains a top choice for their "Gold Standard" service and high customer satisfaction scores. Cigna and Aetna have introduced aggressive regional pricing this year, making them very competitive in specific states like Texas, Florida, and North Carolina.

How to Spot a ‘Risky’ Insurance Company

We protect you from "teaser rates" that look too good to be true. Some companies enter a new state with premiums 20% lower than the average just to grab market share. Once they have enough members, they often implement massive "catch-up" rate hikes. We also monitor the claims loss ratio. If a carrier’s ratio exceeds 80%, it means they are spending nearly all their premium income on claims, which is a clear warning sign of an upcoming price jump. When you wonder what are the top 5 Medicare Supplement plans for seniors? remember that an independent broker provides the unbiased data you need to avoid these traps. We aren’t tied to one brand, so our only loyalty is to you.

Choosing the Right Plan: A Simple Decision Framework

Finding the right coverage doesn’t have to be a headache. We believe that choosing a plan should be a logical, stress-free process that leaves you feeling protected. When you ask, What are the top 5 Medicare Supplement plans for seniors?, you’re really looking for a balance between predictable monthly costs and high-quality care. We use a simple four-step framework to help you move from confusion to confidence as you look toward 2026.

First, determine your risk tolerance. This is the foundation of your decision. Do you prefer a higher monthly premium with the peace of mind that almost all your medical bills are paid? If so, Plan G is likely your best fit. In 2026, many seniors are choosing Plan N instead. It offers lower premiums, often saving between $360 and $450 annually, but it requires small copays of up to $20 for office visits and $50 for emergency room trips. We help you weigh these costs so there are no surprises later.

Next, consider your lifestyle and travel goals for the coming year. Medigap is the gold standard for seniors who want to see any doctor in the country. If you plan to spend the winter of 2026 in a warmer climate or visit family across state lines, these plans follow you. There are no networks to worry about and no need for referrals. You simply show your card and get the care you need, wherever you are in the United States. It’s about maintaining your freedom without the red tape.

Then, we calculate the total annual cost together. It’s easy to get distracted by a low monthly price, but we look at the big picture. We multiply the premium by 12 and add the 2026 Part B deductible, which is currently projected at $283. This calculation shows you exactly what you’ll spend in a year where you use your insurance frequently. We want you to have a clear "worst-case scenario" number so you can budget with certainty.

Finally, we look at Medicare Part D compatibility. Since Supplement plans don’t include prescription drugs, we must ensure your medications are covered by a separate plan. We analyze your specific prescriptions to make sure your total healthcare package is seamless. By understanding what are the top 5 Medicare Supplement plans for seniors? and pairing them with the right drug coverage, you create a safety net that actually works when you need it.

Medigap vs. Medicare Advantage: Making the Final Call

Some of our clients find that our Medicare Advantage Guide offers a better path if they want low premiums and extra perks. However, Medigap is the winner for those who value total flexibility. If you choose Advantage and change your mind, the 12-month ‘Trial Right’ period acts as a safety net. It allows you to return to a Supplement plan without a medical exam, ensuring you aren’t locked into a system that doesn’t serve your needs.

Common Mistakes to Avoid During Enrollment

The most expensive mistake is missing your six-month Medigap Open Enrollment Period. This window is your only "Guaranteed Issue" time where companies cannot turn you down for health reasons. Don’t assume these plans include everything; they typically lack routine dental care. We provide Dental Insurance Plans to fill that gap. Waiting until you are sick to buy coverage is a gamble, as 85 percent of carriers in 2026 will use health screenings for late applicants.

Ready to secure your future? Schedule a call with Paul to find your perfect plan today.

Moving from Confusion to Confidence with The Modern Medicare Agency

Medicare feels like a puzzle with missing pieces. In 2026, the system’s complexity hasn’t slowed down. We see seniors every day who feel overwhelmed by the sheer volume of mail and conflicting advice. Our goal is to simplify this "crazy maze" so you can focus on your retirement. We use a "Never Rushed, Never Pressured" approach. This means we take the time to listen to your specific situation instead of pushing a quick sale. You deserve a partner who values your peace of mind over a commission check.

Choosing an independent broker makes a massive difference in your monthly budget. A captive agent works for one insurance company and can only show you their specific products. We are independent brokers. We represent your interests, not the profit margins of a single carrier. We search through dozens of options to see how they stack up against current market standards. When people ask, What are the top 5 Medicare Supplement plans for seniors?, they are usually looking for a balance of price and coverage. We provide that clarity by comparing 42 different insurance carriers side by side. This allows us to find the lowest premium for the exact same Plan G or Plan N coverage, potentially saving you over $480 a year compared to the highest-priced options in the 2026 market.

Our relationship doesn’t end when you sign the application. Medicare changes every single year. Premiums rise, and new laws affect your out of pocket costs. We stay by your side annually to ensure your plan still makes sense for your health and your wallet. If a carrier raises rates significantly, we are already looking for your next best option. We are here for you every year, not just at enrollment.

Our Simple 5-Step Process for You

-

1. Education first: We make sure you understand how the parts work together. You’ll learn how the 2026 Part B deductible, currently projected at $265, interacts with your chosen supplement.

-

2. Needs analysis: We look at your doctors, health, and budget. We verify that your preferred specialists accept the plans we discuss so you never lose access to your care team.

-

3. Market search: We scan over 40 carriers to find the best 2026 rates. We use real-time data to find the most stable companies with the lowest historical rate increases.

-

4. Easy enrollment: We handle the paperwork to prevent costly mistakes. We ensure you meet all deadlines to avoid the 10% Part B late enrollment penalty that lasts a lifetime.

-

5. Ongoing Support: We check in with you every year during the Annual Enrollment Period. If your needs change or a better plan hits the market, we help you switch seamlessly.

Ready for Peace of Mind? Let’s Chat

You don’t have to do this alone. You can schedule a "No-Obligation" call with Paul or one of our expert agents today. We keep things simple and direct. To make our conversation as productive as possible, please have your red, white, and blue Medicare card ready. We’ll use your effective dates to map out your best options for the coming year. If you’ve been wondering, What are the top 5 Medicare Supplement plans for seniors?, we have the specific data and carrier rankings ready for you. Step out of the confusion and into the confidence of a plan that works.

Take Control of Your Health Coverage in 2026

Navigating the Medicare maze doesn’t have to feel like a full-time job. We’ve explored how Plan G remains the gold standard for comprehensive coverage and why Plan N is a smart, budget-friendly alternative for many. Knowing What are the top 5 Medicare Supplement plans for seniors? is the first step toward protecting your retirement savings from high out-of-pocket costs. You deserve a plan that fits your lifestyle and your budget without any hidden surprises.

At The Modern Medicare Agency, we provide expert guidance across 34+ states to help you find clarity. We offer unbiased comparisons from 40+ carriers and have provided A+ Rated personalized support since our very first day. We’ll help you steer clear of costly enrollment mistakes and late penalties by simplifying the jargon. Our mission is to move you from confusion to confidence so you can enjoy your retirement with total peace of mind. We’re ready to help you make sense of your options today.

Schedule a Call With Paul to Find Your Best Plan

We look forward to helping you secure the dependable coverage you deserve for the years ahead.

Frequently Asked Questions

Which Medicare Supplement plan has the most coverage?

Plan G offers the most comprehensive coverage for anyone new to Medicare in 2026. It pays for 100% of your hospital costs and doctor bills after you meet the annual Part B deductible. While Plan F technically covers that deductible too, it’s only available if you were eligible for Medicare before January 1, 2020. For most people we help, Plan G provides the greatest peace of mind by eliminating unpredictable medical bills.

Can I change my Medigap plan at any time during the year?

You can apply to change your Medigap plan at any time, but you’ll likely need to answer health questions. Unlike the annual enrollment period for drug plans, Medigap companies in 46 states use medical underwriting to decide if they’ll accept you. If you’re outside your initial 6 month enrollment window, a new insurer can deny you based on your health history. We recommend reviewing your coverage annually to ensure your rate remains competitive.

Does Plan G cover prescription drugs in 2026?

No, Plan G doesn’t cover retail prescription drugs in 2026. Medicare Supplement plans haven’t included drug coverage since the law changed on January 1, 2006. To get your medications covered, we’ll help you pick a separate Part D plan. It’s important to remember that in 2026, all Part D plans now have a $2,000 maximum out of pocket limit for covered drugs. This change helps keep your pharmacy costs predictable and manageable.

What is the average cost of a Medicare Supplement plan for a 65-year-old?

A 65-year-old can expect to pay between $160 and $215 per month for a standard Plan G in 2026. Prices vary based on your zip code and gender. For example, a woman in Florida might pay $190 while a man in the same town pays $210. When asking what are the top 5 Medicare Supplement plans for seniors, cost is a huge factor, so we always compare 30 different carriers to find the best value.

Is there a waiting period for pre-existing conditions with Medigap?

There’s a potential 6 month waiting period for pre-existing conditions if you don’t have prior health coverage. However, if you had creditable coverage for at least 6 months before joining Medicare, the insurance company cannot make you wait for treatment. We’ve seen that 95% of our clients avoid this waiting period because they transition directly from an employer plan or a Marketplace policy into their new Medicare Supplement without any gaps in coverage.

Are Medicare Supplement plans the same as Medigap?

Yes, Medicare Supplement plans and Medigap are exactly the same thing. The terms are used interchangeably by the government and insurance companies alike. These plans are designed to fill the gaps in Original Medicare, such as the 20% coinsurance you’d otherwise owe for surgery or chemotherapy. We use both terms to help you understand that these policies provide a solid safety net for your retirement savings and protect you from high costs.

Do I need a Medicare Supplement plan if I have a Medicare Advantage plan?

You cannot have both a Medicare Supplement plan and a Medicare Advantage plan at the same time. In fact, it’s illegal for an agent to sell you a Medigap policy if they know you’re staying on a Medicare Advantage plan. These two options represent different paths. When looking at what are the top 5 Medicare Supplement plans for seniors, remember that Medigap requires Original Medicare, while Advantage plans are a private alternative to it.

What happens to my Medigap plan if I move to a different state?

Your Medigap coverage stays with you if you move to a new state because these plans are portable. You don’t need to cancel your policy, but you must give your insurance company your new address within 30 days. Your monthly premium might go up or down based on the cost of living in your new zip code. We’ll help you check if a different local carrier offers a better rate after you’ve unpacked and settled in.