Last Tuesday, a retiree named Martha discovered that her 2026 Plan G premium had jumped by 14% while her neighbor’s identical coverage stayed flat. It’s a frustrating reality for many seniors who feel stuck in a maze of fine print and aggressive sales calls from agents who don’t have their best interests at heart. We understand how overwhelming it is to learn how to compare medicare supplement plans effectively while worrying about future rate hikes that could eat away at your savings. You shouldn’t have to guess whether your doctor is covered or if you’re overpaying for your benefits.

We are here to help you move from confusion to confidence with a simple, stress-free framework. You’ll master a clear decision-making process so you can secure the best coverage for your specific health needs and budget. We’ve simplified the process into a guide that explains 2026 rate trends, protects you from costly enrollment mistakes, and ensures your monthly costs remain predictable. Here is our step-by-step approach to finding the right Medigap option without the pressure or the headache.

Key Takeaways

- Discover why Medigap remains the “gold standard” for healthcare freedom in 2026 and how it protects you from the 20% of costs Medicare doesn’t cover.

- We simplify the letter system to show you exactly how to compare medicare supplement plans effectively, ensuring you choose the right level of coverage for your budget.

- Move beyond the monthly premium by mastering the “3 Pillars” of comparison, including pricing models that can impact your rates as you age.

- Use our straightforward 5-step checklist to navigate the 2026 landscape with confidence and avoid common enrollment mistakes.

- Learn why an independent broker is your secret weapon to bypass “captive” traps and access the best options from over 40 different carriers.

What is Medicare Supplement Insurance and Why Comparison Matters in 2026

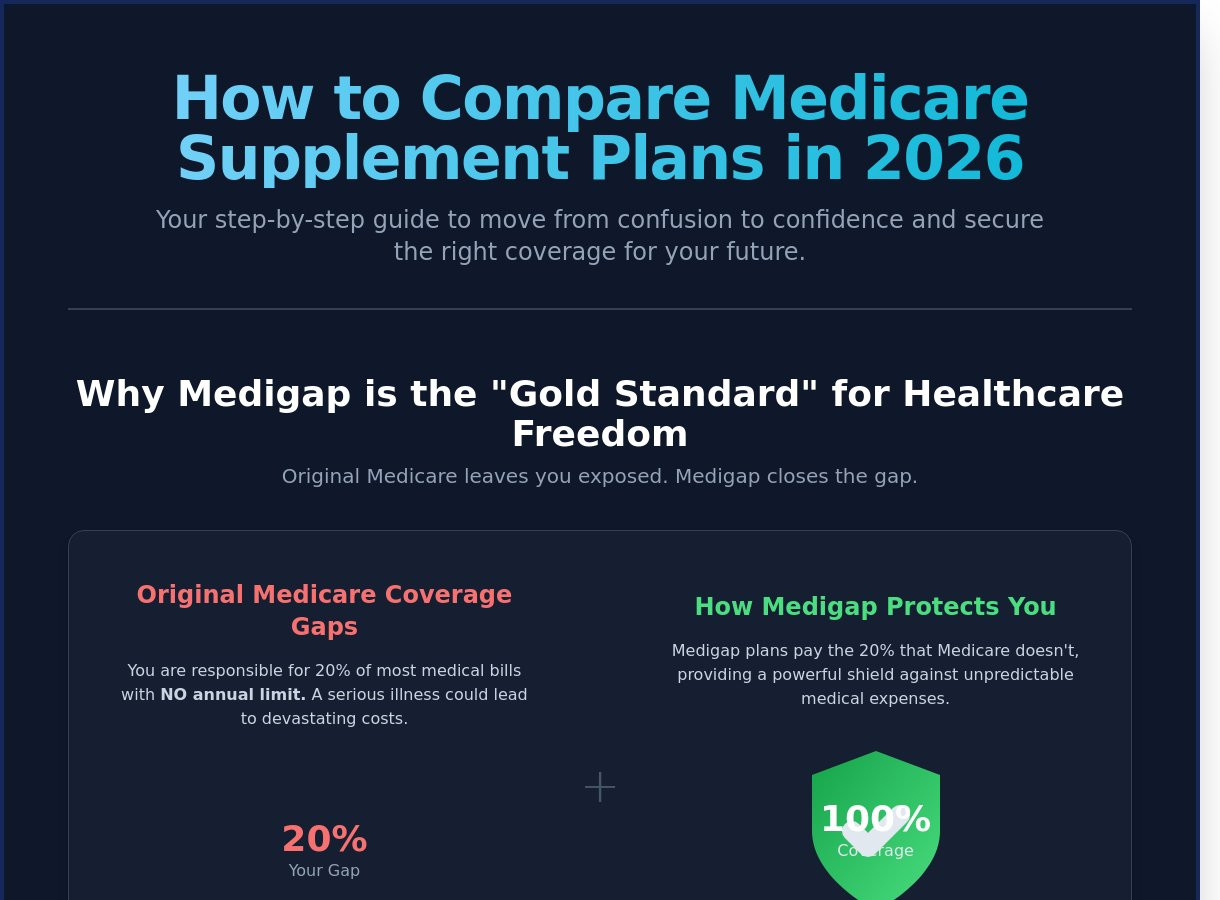

We know that staring at a pile of Medicare mailers can feel like trying to solve a puzzle with missing pieces. It is stressful to feel like one wrong move might cost you your favorite doctor or your hard earned savings. Our goal is to take you from a state of Medicare confusion to a place of total Medicare confidence. We want you to feel protected, not pressured. In 2026, Original Medicare covers a lot, but it still leaves you responsible for 20% of your medical bills. There is no limit on that 20%, which is a scary thought for anyone on a fixed income. Medigap acts as the bridge that covers those costs so you aren’t left with a surprise bill after a hospital stay.

Learning how to compare medicare supplement plans effectively starts with understanding one simple rule: standardization. The government dictates exactly what each plan letter must cover. This means a Plan G offered by a massive national carrier has the exact same medical benefits as a Plan G from a small, local company. They use the same doctors and pay claims the same way. To understand the history of these rules, you might ask What is Medigap? and find that these federal protections have been the gold standard for decades. Since the benefits are identical, your comparison focus shifts to price, company stability, and customer service.

The Difference Between Medigap and Medicare Advantage

We often see people get stuck choosing between two very different paths. Medicare Advantage plans are often lower premium but come with restrictive networks and prior authorization hurdles. If you want to keep your “freedom of doctor” without asking for permission, a Supplement plan is likely your best fit. With Medigap, you can see any provider in the country that accepts Medicare. If you are still weighing your options, our Medicare Advantage Guide provides a deeper look at that alternative path. We want you to be in the right place for your specific health needs.

Why 2026 is a Unique Year for Medicare Comparison

This year marks a major shift because of the Inflation Reduction Act. As of January 1, 2026, the new $2,000 out of pocket cap on prescription drugs is fully in effect. This change makes your choice of coverage even more vital. Medicare Supplement insurance is a federally standardized insurance product designed to eliminate out-of-pocket hospital and medical costs. However, it does not cover retail drugs. Because of the 2026 changes, we must ensure your Medigap choice is paired with an effective Medicare Part D plan to take full advantage of these new cost protections. We are here to help you look at the whole picture, not just one piece of the puzzle.

When we look at how to compare medicare supplement plans effectively in 2026, we focus on the long term. Rates can change, but your need for reliable healthcare won’t. We look at the 5 year rate increase history of companies to make sure you aren’t walking into a “teaser” rate that sky-rockets later. You deserve a plan that fits your budget today and stays affordable five years from now. We simplify the jargon so you know exactly how it works. Our process is never rushed and never pressured because we believe an educated client is a confident client. Let’s start this journey together and find the value you deserve.

The ‘Letter’ System: Understanding Your Coverage Options

The Medicare “alphabet soup” often leaves seniors feeling frustrated and stuck. We are here to change that. In 2026, Medigap plans remain standardized by the government. This means a Plan G from a famous national carrier provides the exact same medical benefits as a Plan G from a small, regional company. Understanding this standardization is the first step in learning how to compare medicare supplement plans effectively. You are not buying better medical care; you are buying a different price tag and customer service experience.

While there are ten different lettered plans, three dominate the conversation in 2026. Plan F remains available only to those who were eligible for Medicare before January 1, 2020. For everyone else, the choices usually narrow down to Plan G and Plan N. Many people assume a higher premium guarantees better access to doctors, but that is a common myth. Since these plans are regulated, your access to care is determined by Medicare, not the supplement provider. If a doctor accepts Medicare, they must accept your Medigap plan, regardless of the company name on your ID card. You can verify these rules on the official Medicare website to see how the government ensures your protection.

Plan G: The 2026 Heavyweight Champion

Plan G is the most popular choice for our clients this year. It offers the most comprehensive coverage available to new enrollees. It covers 100% of the “gaps” in Medicare except for the Part B deductible. In 2026, the Part B deductible is $257. This means after you pay that first $257 of the year for medical services, you will not receive another medical bill. We recommend Plan G for seniors who want total financial predictability. There are no co-pays and no surprises. For those who want to save on premiums, High-Deductible Plan G is an option; however, you must pay the first $2,940 of costs in 2026 before the plan begins to pay.

Plan N: The Strategic Alternative

Plan N is designed for the “strategic” shopper. It often features premiums that are 25% to 30% lower than Plan G. In exchange for these savings, you agree to pay small co-pays. You will pay up to $20 for some office visits and a $50 co-pay for emergency room visits that do not result in an inpatient stay. Plan N also does not cover Part B “Excess Charges.” While this sounds scary, data from early 2026 shows that over 96% of providers nationwide accept “Medicare Assignment,” which eliminates these charges entirely. If you are comfortable with small occasional costs to save $400 or more annually on premiums, Plan N is a fantastic fit.

We see two distinct personalities when we help clients. The “Plan G personality” wants to pay one monthly premium and never think about money when they walk into a doctor’s office. The “Plan N personality” prefers to keep more money in their bank account each month and doesn’t mind a small co-pay once in a while. Both options provide incredible peace of mind compared to the unpredictability of Medicare Advantage. If you feel stuck between the two, you can find a plan that fits your life by looking at your specific medical usage from the past year. We use that data to show you exactly which “letter” would have saved you the most money. Our goal is to move you from a state of confusion to a state of total confidence.

The 3 Pillars of Effective Medigap Comparison: Beyond the Monthly Premium

Finding a low premium feels like a big win. It’s the most common thing we see when seniors start their search. But focusing only on the current price is a mistake that can cost you thousands of dollars over the next decade. To understand how to compare medicare supplement plans effectively, you must look at the structural health of the plan. A plan that costs $150 in 2026 might seem better than one costing $175. If that cheaper plan has a history of 12% annual increases while the other stays at 3%, you’ll be paying much more by 2029. We want to protect you from that “bait and switch” feeling.

The first pillar is the pricing model. Carriers use three different ways to calculate your bill. Attained-age plans are the most common in 2026. These start with a low price but they go up every year simply because you got older. Issue-age plans are different. Your price is based on how old you were when you bought the policy. Community-rated plans charge everyone in the same area the same price regardless of age. We help you look past the “teaser” rate to see the long-term math.

The second pillar is carrier financial strength. We look at A.M. Best ratings to see if a company is stable. An “A” or “A+” rating means the company has the reserves to pay claims without panicking. If a company is struggling financially, they often try to make up for it by hitting their members with massive rate hikes. We don’t want you stuck with a company that’s on shaky ground.

The third pillar is rate increase history. This is the hidden cost that most seniors miss. Some companies have a 10 year track record of keeping increases under 4%. Others might have 15% increases every single year. We track this data so you don’t have to guess. Learning how to compare medicare supplement plans effectively means looking at what people were paying five years ago, not just what they’re paying today.

Evaluating the Insurance Carrier’s Reputation

Before you sign, we check the company’s financial grade. We prefer carriers with an A or A+ rating from A.M. Best. We also look at the “size of the block,” which refers to the total number of policyholders. A carrier with 500,000 members is usually more stable than a new company with only 5,000 members. A carrier’s historical rate increase average is the best predictor of your future premium costs.

Understanding Pricing Methods

Your zip code is one of the biggest factors in which pricing model you should choose. State laws in places like Florida or New York dictate which options are available. In 2026, we find that many people in “Attained-Age” states get lured in by low introductory rates. These plans start cheap but often become the most expensive option within five years. We analyze your specific location to find the model that saves you the most over the long haul. Our goal is to move you from confusion to confidence by showing you the real numbers.

Your 5-Step Checklist to Compare Plans Effectively

We know that looking at a stack of insurance brochures in 2026 feels like trying to solve a puzzle with missing pieces. Our goal is to give you a clear, logical path from confusion to confidence. To learn how to compare medicare supplement plans effectively, you need a repeatable system that removes the guesswork. We’ve developed this 5-step checklist to protect your savings and ensure you never pay more than necessary for your coverage.

- Step 1: Confirm your timing. You must know if you are in your 6-month Medigap Open Enrollment Period or if you have “Guaranteed Issue” rights from losing employer coverage. This determines if a company can look at your medical records.

- Step 2: Choose your plan letter. In 2026, Plan G and Plan N remain the top contenders. Plan G offers total peace of mind, while Plan N provides lower premiums if you don’t mind small copays at the doctor or emergency room.

- Step 3: Run the numbers for your zip code. Prices for the exact same Plan G can vary by $40 to $70 per month depending on the carrier. We run multi-carrier quotes to find the 2026 baseline for your specific area.

- Step 4: Audit the history. We look back at the last 5 years of rate increases for the lowest-priced carriers. A company that starts cheap but raises rates by 12% every year will cost you more in the long run than a stable carrier with 3% increases.

- Step 5: Check the extras. We look for “Value-Adds” like household discounts or integrated dental insurance options that wrap your coverage into one neat package.

Navigating the Enrollment Windows

Timing is everything when you want to learn how to compare medicare supplement plans effectively. Your 6-month Medigap Open Enrollment Period is a one-time hall pass. During this window, insurance companies cannot ask you health questions or deny you coverage. If you wait until 2027 or later to switch without a qualifying event, you’ll face “Medical Underwriting.” This means a carrier can charge you more or reject your application entirely based on your history. We help you hit these deadlines so you avoid lifetime late enrollment penalties.

The Importance of Household Discounts

You can often lower your monthly premium by 5% to 12% simply by living with another adult. Many people assume this only applies to spouses who are also on Medicare, but that’s a common misconception. In 2026, several top-rated carriers offer “Roommate Discounts” if you’ve lived with any adult for at least 12 months. Some companies have very easy qualification rules, while others are more strict. We always ask the question: “Is this the lowest possible rate you qualify for?” because these small percentages add up to thousands of dollars over a decade.

We don’t believe in high-pressure sales or rushed decisions. Our process is built on transparency and education, ensuring you feel empowered to make the right choice for your budget. We’ve seen how the 2026 market has shifted, and we’re ready to help you find the stability you deserve.

Schedule a Call With Paul to get your personalized 2026 quote comparison today.

Why an Independent Broker is Your Secret Weapon

Many seniors in 2026 make the mistake of calling a big-name insurance company directly after seeing a television commercial. This leads straight into the captive trap. A captive agent works for one specific company and can only sell you that company’s products. They won’t tell you if a competitor across the street offers the exact same Plan G for $40 less per month. Their loyalty belongs to the corporation, not to your monthly budget. When you limit yourself to one carrier, you’re essentially wearing blinders while trying to navigate a complex financial decision.

At The Modern Medicare Agency, we operate as independent brokers, which completely changes the dynamic. We represent over 40 different carriers. This independence is the foundation of how to compare medicare supplement plans effectively in today’s market. We use specialized, real-time software to compare every available rate in your specific zip code within seconds. You get the full picture of the 2026 market, not just a narrow slice of it. We don’t have a favorite company; our only favorite is the one that gives you the most coverage for the lowest possible price.

Our support remains active long after your initial enrollment. The 2026 landscape has been particularly volatile. We’ve seen several major carriers adjust their rates by more than 12% this year due to shifting federal regulations and healthcare costs. We monitor these shifts for you. If your premium spikes unexpectedly, we reach out to discuss better options. We are your long-term advocates in a system that often feels designed to ignore the individual. We handle the paperwork, the phone calls, and the stress so you can focus on your life.

- We analyze 44 different carriers to find the lowest price for your specific health needs.

- We explain how the 2026 “birthday rule” in specific states might allow you to switch plans without a medical exam.

- We provide a clear comparison of how the $2,000 out-of-pocket prescription drug cap impacts your total healthcare spending this year.

- We help you avoid the common 2026 enrollment mistakes that lead to permanent late-enrollment penalties.

Unbiased Guidance vs. High-Pressure Sales

At The Modern Medicare Agency, we live by a “Never Rushed, Never Pressured” philosophy. You’ll never feel like a sales quota when you speak with us. We take the time to explain the jargon, like the difference between “community rated” and “attained age” pricing, so you feel empowered. Best of all, our services are 100% free to you. The insurance companies pay us a commission for the administrative work we do, so you get professional expertise at no added cost.

Starting Your Journey from Confusion to Confidence

The goal is simple. We want you to sleep better knowing your medical bills are covered. We’ve helped thousands of seniors move from a state of total overwhelm to complete clarity. You don’t have to guess which plan is best for your situation. For a deeper look at the technical details of current plans, visit The Modern Medicare Agency’s Medigap overview. If you’re ready for a partner who puts you first, Schedule a Call with The Modern Medicare Agency and let’s build your custom 2026 Medicare roadmap together.

Move From Confusion to Confidence in Your 2026 Coverage

Navigating the Medicare maze doesn’t have to feel like a second job. We’ve shown you that while the lettered plans are standardized, the companies behind them are not. You now know that looking at a carrier’s 5 year rate increase history is just as critical as finding a low monthly premium. Learning how to compare medicare supplement plans effectively means looking at the big picture, from the 2026 Part B deductible to the long term stability of your provider.

You don’t have to make these big decisions alone. Since 2011, we’ve provided unbiased, independent guidance to help seniors protect their savings. We have access to 40+ top-rated carriers and hold licenses in 34+ states to ensure you get national expertise with a personal touch. We simplify the jargon so you can stop worrying about medical bills and start enjoying your retirement. It’s time to trade your stress for clarity and secure the protection you deserve. Schedule a Call With Paul to Find Your Perfect Plan. We’re here to walk beside you every step of the way.

Frequently Asked Questions

What is the best way to compare Medicare Supplement plans in 2026?

The most reliable way to compare medicare supplement plans effectively is to use an independent broker who can scan all 47 insurance carriers in your specific zip code. Because the federal government standardizes these plans, a Plan G with one company has the exact same benefits as a Plan G with another. We focus on the carrier’s 5 year history of rate stability and their current financial rating to ensure you aren’t surprised by a massive price hike next year.

Is Plan G better than Plan N for most seniors?

Plan G is generally considered the gold standard because it covers every gap in Medicare except for the annual Part B deductible. In 2026, Plan N is an excellent alternative for those who want to save roughly $420 per year in premiums. You just have to be comfortable paying a $20 co-pay for office visits and $50 for emergency room trips. We help you look at your doctor visit frequency to see which plan offers the best math for your budget.

Can I change my Medicare Supplement plan at any time of the year?

Yes, you can apply to switch your Medigap plan any day of the year. You don’t have to wait for the fall Open Enrollment period because that window only applies to drug plans and Medicare Advantage. However, in 47 states, you’ll likely need to answer health questions to qualify for a new plan if you’re past your initial 6 month enrollment window. We walk you through this underwriting process to make sure you’re accepted before you cancel your old coverage.

How much do Medicare Supplement plans cost on average in 2026?

The average monthly premium for a Plan G for a 65-year-old in 2026 is $168. Prices can fluctuate based on your location, with some rural areas offering rates near $138 while major metropolitan areas might see prices closer to $215. We compare these monthly costs across the 30 top-rated companies in your area. This ensures you get the exact same government-standardized benefits without paying a penny more than necessary for the name on the card.

Do I need to undergo a physical exam to get a Medigap plan?

No, you don’t need a physical exam to qualify, but the insurance company will review your medical history through a series of questions. Most applications in 2026 include about 20 health-related questions and a review of your prescription drug records from the last 5 years. We simplify this step by pre-screening your medications against the carrier’s guidelines. This helps us find the right company that will welcome you with open arms and total confidence.

What happens if my insurance carrier goes out of business?

You are protected by federal “Guaranteed Issue” rights that ensure you won’t lose your coverage if a carrier leaves the market. You have exactly 63 days from the date your coverage ends to choose a new plan from another company without answering any health questions. This safety net means you can’t be denied for pre-existing conditions. We act as your advocate during this 9 week window to move you into a stable, highly-rated company quickly and easily.

Does Medicare Supplement cover dental and vision care?

Standard Medigap plans do not include coverage for routine dental cleanings, eyeglasses, or hearing aids. These plans are strictly designed to fill the 20% “gap” left by Original Medicare for hospital and medical services. Since 98% of these policies focus only on medical bills, we often help our clients set up a separate, affordable policy for dental and vision. This keeps your medical protection robust while ensuring your teeth and eyes are also taken care of properly.

Why did my Medigap premium increase even though my benefits stayed the same?

Premiums typically increase due to your age and the rising cost of medical services across the country. In 2026, the national average for annual rate adjustments is 6.2% to keep up with healthcare inflation. Even though your benefits are locked in by law, the insurance company’s cost to pay those doctors increases every year. We monitor these changes for you. If your specific carrier raises rates higher than the 6.2% average, we’ll find you a more competitive option immediately.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com