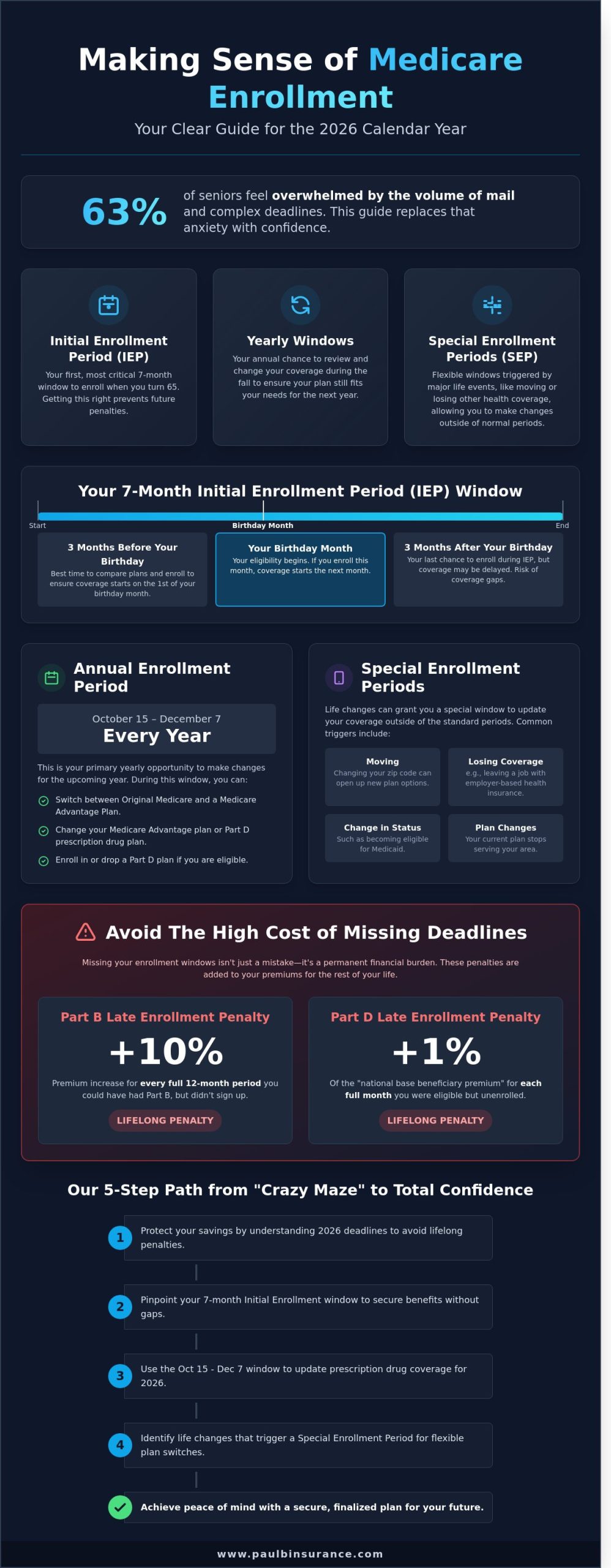

Imagine opening your mailbox on October 15, 2026, and finding 14 different insurance brochures all claiming to be “urgent.” It is no wonder that 63% of seniors report feeling overwhelmed by the sheer volume of mail they receive during the final months of the year. We know that making sense of medicare enrollment periods feels like trying to read a map in a different language while a loud clock ticks in the background. You have worked hard for your retirement, and the last thing you want is a permanent 10% late enrollment penalty on your Part B premium just because a specific date slipped through the cracks.

We agree that the system is a crazy maze designed to confuse even the sharpest minds. That is why we have created this guide to replace that anxiety with total confidence. We will explain every deadline for the 2026 calendar year in plain English, ensuring you avoid lifelong costs and secure the exact coverage you need. This article provides a clear timeline of every window you need to know so you can stop worrying and start enjoying your peace of mind.

Key Takeaways

- We help you protect your retirement savings from lifelong penalties by making sense of medicare enrollment periods and their specific 2026 deadlines.

- Understand the exact timing of your seven-month “Initial Enrollment” window so you can secure your benefits without any stressful gaps in coverage.

- See why the October 15 to December 7 window is your best opportunity to update your prescription drug coverage and prepare for the 2026 plan year.

- Identify the major life changes that trigger a Special Enrollment Period, giving you the flexibility to switch plans even outside of standard dates.

- Discover our proven 5-step path that takes you from feeling overwhelmed by the “crazy maze” to having a secure, finalized plan for your future.

Why Understanding Your Medicare Enrollment Windows Matters

Making sense of medicare enrollment periods often feels like trying to solve a complex puzzle with missing pieces. We know the stress that comes with staring at a stack of insurance mail, wondering if you are about to miss a deadline that could impact your bank account for the rest of your life. The “alphabet soup” of Parts A, B, C, and D hasn’t become any less confusing in 2026. Our mission is to protect you from that overwhelm. We want to take you from a place of frustration to a state of total confidence. These dates aren’t just suggestions; they’re strict windows that determine your healthcare security.

We see many seniors who feel pressured by aggressive marketing. It is easy to feel lost in the maze. By simplifying these dates, we help you stay in control. You deserve a clear path and a patient guide who is never rushed. Understanding these timelines is the first step toward ensuring you have the right coverage at the right price without any hidden surprises.

The Cost of Missing Your Window

Missing a deadline isn’t just a minor paperwork headache. It is a permanent financial burden that follows you. If you don’t sign up for Part B when you’re first eligible, you face a 10% premium increase for every full 12-month period you waited. This penalty is not a one-time fee. It stays attached to your monthly premium for as long as you have Medicare.

Part D carries its own set of risks. For every month you go without Part D or other creditable coverage, a 1% penalty is added to your monthly bill based on the current year’s base beneficiary premium. In 2026, creditable coverage is defined as any health insurance plan, such as one from a large employer, that is expected to pay out at least as much as the standard Medicare prescription drug plan. We want to help you avoid these unnecessary costs so your retirement funds stay where they belong.

The Three Main Categories of Enrollment

We group these windows into three clear categories to make things easier to track. Making sense of medicare enrollment periods becomes much simpler when you know which bucket you fall into:

- Initial Enrollment Period: This is your first 7-month window that opens three months before you turn 65 and closes three months after your birthday month.

- Yearly Windows: The Annual enrollment period runs from October 15 to December 7, which is your primary chance to adjust your plan for the following year.

- Special Enrollment Periods: These are triggered by specific life events, like moving to a new zip code or losing your current job-based insurance.

Whether you are approaching 65 or looking to update your 2026 coverage, knowing these categories keeps you ahead of the curve. We are here to provide the unbiased guidance you need to make the best choice for your unique situation.

The Initial Enrollment Period (IEP): Your Seven-Month Welcome Window

We understand that your mailbox is likely overflowing with flyers and letters as you approach age 65. Making sense of medicare enrollment periods can feel like trying to solve a puzzle with missing pieces. Your Initial Enrollment Period is the first and most vital opportunity to get your coverage right from the start. This seven-month window is your welcome mat to the system. It begins three months before your 65th birthday month, includes your birthday month, and continues for three months after it ends.

We strongly suggest starting your application at least two months before your birthday month. This ensures your coverage is active on the first day of your birth month, preventing any gaps in care. During this time, we often help people decide if they should stay with Original Medicare or choose a Medicare Advantage plan to help cover costs that the government doesn’t pay for. Making sense of medicare enrollment periods now will save you from a lot of stress later.

Breaking Down the 7-Month IEP Timeline

Your Initial Enrollment Period is divided into three specific phases to help you stay on track:

- The 3 months before: This is the time for preparation. We use this period to help you compare plans and choose your path.

- Your birthday month: If you enrolled in the months prior, your coverage typically starts on the first of this month.

- The 3 months after: This is your final chance to sign up. If you wait until this phase, your coverage start date will be delayed.

What Happens if You Are Still Working?

In 2026, many people choose to work past 65. If you have health coverage through an employer with 20 or more employees, you might be able to delay Part B without a penalty. However, you must verify that your current plan is considered “creditable” by 2026 standards. If your company has fewer than 20 employees, Medicare usually becomes your primary insurance. In that case, you must sign up during your IEP to avoid lifetime late fees. If you feel stuck, we can help you compare your work plan to Medicare options to see which saves you more money and provides better protection.

Annual and Open Enrollment: Making Sense of the Yearly Updates

Making sense of medicare enrollment periods often feels like trying to solve a puzzle with missing pieces. We are here to help you find those pieces so you can feel confident in your choices. Every year, the calendar brings two major windows that allow you to adjust your coverage to fit your changing health needs in 2026. These windows are your opportunity to ensure your insurance keeps up with your life, rather than the other other way around.

The Fall Shuffle: Annual Enrollment Period (AEP)

From October 15 to December 7, the Annual Enrollment Period is what we call maintenance season for your healthcare. This is the primary time to review your current setup and decide if it still serves you. Because insurance companies change their costs and coverage rules every January 1, staying on autopilot can be a costly mistake. For example, a medication that was covered in 2025 might see a price hike or a tier change in the 2026 formulary. During this window, you can:

- Switch from Original Medicare to a Medicare Advantage plan.

- Move from one Advantage plan to another to keep your specific doctors in-network.

- Add, drop, or change Medicare Part D prescription drug plans to lower your pharmacy costs.

We focus on the tiny details that matter, like whether your local pharmacy stayed in your plan’s preferred network. You can find official Medicare enrollment information to verify these specific dates, but we take the stress out of the process by doing the heavy lifting for you. We compare the plans side-by-side so you don’t have to guess.

The New Year Window: Medicare Advantage Open Enrollment

If you start 2026 and realize your Medicare Advantage plan isn’t the right fit, you have a second chance. The Medicare Advantage Open Enrollment Period (MA OEP) runs from January 1 to March 31. This window is specifically for people who are already enrolled in an Advantage plan. It’s a safety valve that provides genuine peace of mind if your doctor unexpectedly leaves a network or your copays feel too high.

You can use this time to switch to a different Advantage plan or return to Original Medicare. If you choose to go back to Original Medicare, we will help you evaluate Medigap (Medicare Supplement) options to help cover the 20 percent that Medicare doesn’t pay. Our mission is to move you from confusion to confidence. We make sure you are never rushed or pressured into a decision, because your health deserves a patient, expert advocate.

Special Enrollment Periods: Flexible Windows for Major Life Changes

Life doesn’t always follow a set schedule. You might decide to move closer to family or finally hang up your hat at work in 2026. When these big shifts happen, you shouldn’t have to worry about losing your healthcare. Special Enrollment Periods (SEPs) act as a safety net. They allow you to change your coverage when your life circumstances shift unexpectedly. We take the lead in making sense of medicare enrollment periods so you can focus on your next chapter instead of paperwork.

Most people have a window of 60 to 83 days to make a change. This timeline depends on your specific situation. If you miss this window, you might have to wait until the next standard enrollment date. We work as your personal advocate during this time. Our team ensures insurance carriers recognize your special status and process your enrollment without delay. We want you to feel confident that your transition is being handled by experts who care.

Common Life Events That Trigger an SEP

Moving is a very common reason for an SEP. If you move to a new zip code where your current plan isn’t offered, you get a chance to switch. This is vital if you move into a long-term care facility or back into the community. Retiring after age 65 is another major trigger. If you’ve been covered by a large employer plan with more than 20 employees, you can jump into Medicare without penalties once that job ends. Sometimes, plans simply stop serving a specific area. If your current provider leaves the Medicare program in 2026, you’ll have a window to find a new home for your health needs.

How to Prove Your Eligibility for an SEP

Medicare requires proof before they let you change plans outside of standard dates. You’ll usually need a “Loss of Coverage” letter from your HR department or a utility bill to prove a move. Collecting these documents can feel overwhelming. We help you gather what’s needed and submit it correctly the first time. Working with an independent broker is critical here. We help you compare options like those found in our Medicare Advantage guide to ensure you don’t face a single day without protection. Our goal is to move you from a state of confusion to complete certainty.

Avoiding Penalties and Gaps: How We Simplify Your 2026 Enrollment

We believe no senior should have to navigate the crazy maze of the insurance system alone. It’s a complex world, especially with the significant Part D restructuring taking full effect in 2026. You shouldn’t feel rushed or pressured into a decision that affects your health and your wallet. Our team is dedicated to making sense of medicare enrollment periods so you can avoid lifelong late enrollment penalties and frustrating gaps in your coverage.

We provide unbiased guidance because we represent over 40 different carriers. Unlike a captive agent who can only sell you one company’s products, we work for you. We look at your whole health picture, from your core medical needs to dental insurance plans, ensuring every piece of the puzzle fits together perfectly. Our goal is to move you from a state of confusion to a place of total confidence.

The Modern Medicare Agency Approach

Our 5-step process is designed to be methodical and stress-free. It begins with a calm, no-pressure conversation to understand your specific health needs and budget. We then simplify the jargon so you know exactly how each plan works. Finally, we compare options from 40+ carriers to find your best fit. This logical path ensures you’re never rushed. You’ll understand your 2026 benefits clearly before you ever sign a single document.

Your Year-Round Medicare Partner

We don’t just sign you up and disappear; we provide year-round support to protect your interests. When you receive a “Notice of Change” letter in the mail this September, you don’t have to worry about what the fine print means. You can simply reach out to us. We help you decode those changes and determine if your current plan remains the strongest option for your needs.

Waiting until the last minute often leads to mistakes. By starting your 2026 planning now, you stay ahead of deadlines and keep your costs predictable. Making sense of medicare enrollment periods is much easier when you have a dedicated advocate by your side. Schedule a Call With Paul to get started on your 2026 planning today and experience the peace of mind that comes with expert, personal guidance.

Take Control of Your 2026 Medicare Journey

Navigating the healthcare landscape in 2026 doesn’t have to feel like wandering through a maze. We’ve explored how your seven-month Initial Enrollment Period and the yearly Open Enrollment window are vital for keeping your coverage on track. Missing these specific dates can lead to permanent Part B late enrollment penalties or unexpected gaps in your medical care. By making sense of medicare enrollment periods today, you’re taking a proactive step to protect both your health and your retirement savings.

You don’t need to tackle these complex deadlines alone. Our team provides zero-cost guidance for seniors and is currently licensed in over 34 states. We represent more than 40 different insurance carriers; this means we offer unbiased choices that a captive agent simply can’t provide. We’ll help you compare 2026 plan updates and find the right fit for your lifestyle. Our mission is to move you from a state of confusion to a place of total confidence. Let’s make sure your 2026 enrollment is handled with the care and expertise you deserve.

Schedule a Call With Paul for a Stress-Free Enrollment

We’re ready to help you secure the peace of mind you’ve been looking for.

Frequently Asked Questions

What happens if I miss my Initial Enrollment Period for Medicare?

You may face lifetime late enrollment penalties and must wait until the General Enrollment Period to sign up. Your Part B monthly premium increases by 10% for every full 12-month period that you could have had coverage but didn’t. This extra cost follows you forever. We help you track your unique 7-month Initial Enrollment window so you can avoid these permanent financial mistakes and find peace of mind.

Can I change my Medicare plan at any time during the year?

No, you can generally only change your coverage during specific windows like the Annual Enrollment Period from October 15 to December 7. Outside of this, you need a Special Enrollment Period triggered by events like moving or losing employer coverage. We help you understand these dates so you don’t feel stuck in a plan that isn’t working for your health needs or your monthly budget.

Is the Medicare Open Enrollment Period the same as the General Enrollment Period?

No, these two periods serve different groups of people and happen at different times. The Open Enrollment Period runs from October 15 to December 7 for plan changes, while the General Enrollment Period is January 1 to March 31 for those who missed their first chance to sign up. Making sense of medicare enrollment periods becomes much easier when we help you identify which specific window applies to your situation.

How do I know if my employer coverage is “creditable” for Medicare Part D?

Your employer must send you a written Notice of Creditable Coverage by October 14 each year. This document confirms that your current prescription drug plan pays out at least as much as the standard Medicare Part D benefit in 2026. If you don’t receive this notice, contact your HR department immediately to avoid a 1% monthly late enrollment penalty. We can review your notice to ensure your transition is seamless.

What is the Special Enrollment Period for someone moving to a new state in 2026?

You typically have a 2-month window to switch your Medicare Advantage or Part D plan when you move to a new service area. This period starts either the month before you move or the month you notify your plan, and it lasts for two full months after the move. We guide you through this transition to ensure your new 2026 coverage is active the day you arrive at your new home.

Do I need to re-enroll in Medicare every year during the Annual Enrollment Period?

No, your current Medicare coverage will automatically renew for 2027 unless the insurance company leaves the program. However, we recommend a review because 80% of plans change their costs or drug formularies annually. Checking your options between October 15 and December 7 ensures you still have the most affordable plan for your specific medications and doctors. We provide the unbiased guidance you need to make this choice.

Can I switch from Medicare Advantage back to Original Medicare?

Yes, you can switch back during the Medicare Advantage Open Enrollment Period from January 1 to March 31 each year. During this 90-day window, you can also join a standalone Part D drug plan. We help you evaluate if this move is right for you, especially if you want more flexibility in choosing providers without needing referrals. Our goal is to move you from confusion to confidence during this switch.

How much are the Medicare late enrollment penalties in 2026?

The Part B penalty is an extra 10% charge on your premium for every 12-month period you delayed signing up. For Part D, the penalty is 1% of the $36.78 national base beneficiary premium for every month you lacked coverage. These costs are added to your monthly bill for as long as you have Medicare. Making sense of medicare enrollment periods ensures you don’t pay these unnecessary lifetime fees and protects your retirement savings.