Last Tuesday, a client named Sarah called us in a panic because her father’s 2026 Part D premium jumped by $18 a month simply because they missed a small update in his plan’s formulary. It’s a stressful realization. Many families face this same panic as they try to figure out how to help parents choose a medicare plan amidst shifting regulations. We know it feels like you’re trying to solve a puzzle where the pieces change every single January. You want to protect your parents’ health and their savings, but the sheer volume of alphabet soup parts and hidden costs can make anyone feel overwhelmed.

We’re here to turn that confusion into confidence. In this guide, we’ll show you exactly how to handle the 2026 Medicare maze, from gathering the four essential documents to picking a plan that keeps their specific doctors and medications covered. You’ll learn how to avoid the lifetime late enrollment penalties that affect 13% of new beneficiaries and find a path that offers true peace of mind. We’ve laid out a clear, step-by-step checklist to ensure your parents are protected for the entire year ahead.

Key Takeaways

- We help you step into the role of a healthcare advocate to guide your parents through the complex 2026 Medicare landscape with confidence and clarity.

- Learn how to translate the confusing “alphabet soup” of Parts A, B, C, and D into plain English to make comparing coverage options simple.

- Discover the “Big Three” details you must gather to ensure any plan you select perfectly matches your parents’ specific doctors, medications, and lifestyle.

- Follow our gentle, step-by-step guide on how to help parents choose a medicare plan that focuses on their peace of mind rather than sales pressure.

- Understand the vital difference between an independent broker and a captive agent to ensure your family receives unbiased guidance at no cost to you.

Navigating the 2026 Medicare Maze: Why Your Help is Vital

Medicare feels like a crazy maze for most seniors in 2026. Your parents are likely bombarded with flashy mailers and high-pressure TV ads every single day. We don’t view you as just a helper; you are a vital healthcare advocate. You’re the person standing between your parents and a lifetime of financial stress. If they miss a single deadline, they could face a 10% penalty on their Part B premiums for the rest of their lives. We want to move your family from confusion to confidence by making the complex simple.

Learning how to help parents choose a medicare plan starts with recognizing that the system isn’t designed for simplicity. It’s designed for options, and too many options often lead to paralysis. By stepping into the role of an advocate, you ensure that your parents don’t just pick a plan because the celebrity on the commercial looked trustworthy. You’re there to protect their health and their hard-earned savings.

The 2026 Medicare Landscape

The year 2026 marks a major shift because the $2,000 out-of-pocket cap for Medicare Part D prescription drugs is now fully active. This change is a huge win for seniors, but it has caused insurance companies to overhaul their plans across the board. Automatic enrollment is a dangerous trap this year. A plan that worked in 2025 might have dropped your parent’s primary doctor or changed how they cover specific medications in 2026. One-size-fits-all plans fail because every senior has unique health needs.

Identifying the Key Enrollment Windows

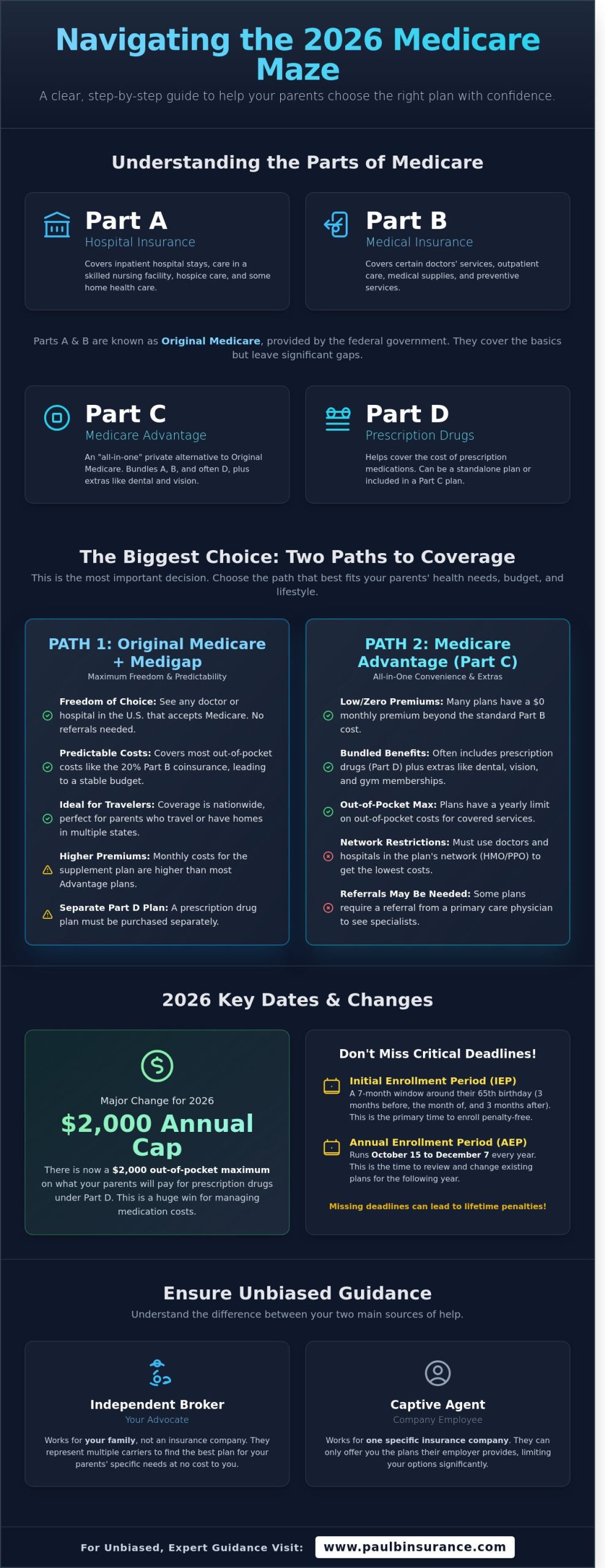

Timing is everything when you’re figuring out how to help parents choose a medicare plan without triggering penalties. The Initial Enrollment Period (IEP) is a seven-month window that opens three months before your parent turns 65. If they are already enrolled, the Annual Enrollment Period (AEP) runs from October 15 to December 7, 2026. Missing these dates is the number one mistake we see. These deadlines are strict rules that can cost your family thousands of dollars over time.

Understanding Your Parents’ Medicare Options: The Simple Breakdown

Helping your parents through the Medicare maze feels like learning a new language. We see the stress this causes families every day. Our goal is to move you from confusion to confidence by stripping away the jargon. At its core, the federal government provides Part A for hospital stays and Part B for doctor visits. While these cover the basics, they leave gaps. That’s where private insurance companies come in to provide the extra protection your parents need.

When you start learning how to help parents choose a medicare plan, you’ll see four main pieces. Part A and B are “Original Medicare.” Part C, also known as Medicare Advantage, is a private alternative. Part D covers prescriptions. Finally, Medigap (Supplement) plans work alongside Original Medicare to pay for costs like the 20 percent coinsurance that Part B doesn’t cover. Understanding these parts is the first step in knowing how to help parents choose a medicare plan that fits their lifestyle.

Medicare Advantage vs. Medicare Supplement

This is the biggest fork in the road. Medicare Advantage plans often have $0 or very low monthly premiums. They include extras like dental, vision, and gym memberships which are common in 2026 plans. However, these plans use networks. If your parents travel often or have specific specialists, a Supplement plan might be better. Supplements have higher monthly costs but allow your parents to see any doctor in the country who accepts Medicare, providing total peace of mind and predictable budgets.

The Importance of Part D Prescription Coverage

Every parent needs a Part D plan to avoid late enrollment penalties. In 2026, the rules have changed for the better. There’s now a $2,000 annual out-of-pocket cap on prescription drugs. This is a massive win for seniors on fixed incomes. We always remind families that “formularies,” or the list of covered drugs, change every January 1st. An annual review is the only way to ensure their specific medications stay affordable. If you feel stuck, you can schedule a call with us to review these options together.

The Pre-Enrollment Checklist: Gathering the Vital Information

We believe that the most effective way to protect your parents’ health and finances is to treat Medicare like a custom suit. It must be tailored to fit their exact needs. The best coverage for 2026 isn’t the one with the loudest TV commercial; it’s the one that aligns perfectly with their current health data. Knowing how to help parents choose a medicare plan starts with a clear picture of their daily health needs. We focus on the Big Three: their doctors, their medications, and their lifestyle goals.

Sometimes parents feel a bit private about their medical history or find it overwhelming to discuss. We suggest explaining that you aren’t looking to pry into their personal business. Instead, you’re acting as their advocate to ensure they don’t overpay or lose access to their favorite doctor. Before you reach out to a broker, gather these items to keep the process simple:

- Their current Red, White, and Blue Medicare card.

- A list of all current health insurance ID cards.

- A complete list of their healthcare providers and preferred hospitals.

- A detailed list of all prescription medications.

- A calendar of any planned surgeries or major procedures for the 2026 calendar year.

Mapping Out Doctors and Providers

We must verify every specialist and facility in a plan’s 2026 network before making a change. Networks are not static. In fact, many provider contracts were updated on January 1, 2026, meaning a doctor who was “in-network” last year might not be today. Out-of-network surprises are expensive. If your parent visits a specialist outside the network, they could be responsible for 100% of the bill. We always check if their local hospital is a preferred facility to ensure the lowest possible co-pays.

The Prescription Drug Inventory

To find the lowest-cost 2026 drug plan, we need an inventory of every medication, the exact dosage, and the frequency of use. This data is vital because of the 2026 updates to the $2,000 out-of-pocket maximum for prescriptions. A formulary is the specific list of drugs a plan chooses to cover. We use this list to compare different Medicare Part D options to see which plan places your parents’ specific meds in the most affordable “tier.” This simple step can save thousands of dollars annually. We want to ensure you have the tools for how to help parents choose a medicare plan with total confidence.

How to Help Your Parents Choose: A Step-by-Step Guide

Helping your folks navigate their healthcare options isn’t just about filling out paperwork. It’s about providing a sense of security for their future. We recommend starting this conversation early. Don’t wait for a health crisis or the week of a deadline to bring it up. When you sit down together, focus on peace of mind rather than insurance jargon. Most seniors feel bombarded by the mail and television ads they see every day. We find that validating their frustration helps lower their defenses and makes the process much smoother.

Starting the Medicare Conversation

When you begin, use “we” language to show you are on their team. You might say, “We want to make sure you’re protected so we can focus on enjoying our time together.” Ask them one simple question: “What is the one thing you want your insurance to do?” Their answer usually reveals their biggest worry, whether it’s keeping a specific doctor or affordably managing a chronic condition. Once you understand their priorities, narrow the choices down to two or three viable options. Providing too many paths leads to decision paralysis, which often results in no decision at all. Our goal is to move from confusion to confidence by keeping the choices simple and direct.

Evaluating the Total Cost of Care

Learning how to help parents choose a medicare plan requires looking past the flashy “$0 premium” headlines. While a plan with no monthly cost sounds great, we have to look at the potential “Maximum Out of Pocket” (MOOP) costs. In 2026, the standard MOOP for many Medicare Advantage plans can be as high as $9,350 for in-network services. We need to calculate what happens if they have a bad health year.

Specific details matter in 2026. Because of the Inflation Reduction Act, all Part D plans now have a firm $2,000 out-of-pocket cap on prescription drugs. This is a massive win for seniors on expensive medications. However, Medicare still leaves gaps in other areas. We often suggest adding a dental insurance plan and checking vision benefits to ensure they aren’t paying for basic care out of their own pockets. A truly comprehensive plan covers the person, not just the “big” medical bills.

The final step is to schedule a joint call with a trusted, independent expert. Having a third party explain the nuances ensures the advice is unbiased and professional. We can look at their specific doctors and medications together to find the perfect fit. If you’re ready to get clear answers for your family, you can schedule a call with Paul today to start the process.

From Confusion to Confidence: Why an Independent Broker is Your Best Ally

Helping your parents find coverage shouldn’t feel like a second job. When you research how to help parents choose a medicare plan, you will likely encounter two types of professionals: captive agents and independent brokers. A captive agent works for one specific insurance company. They can only show you plans from that single source, even if a better deal exists elsewhere. We are independent brokers. We work for you, not the insurance companies.

Our services at The Modern Medicare Agency are 100% free to you and your parents. We receive compensation from the insurance carriers, so you never see a bill from us. We compare plans from over 40 different carriers to find the specific best fit for your parent’s unique health needs and budget. We promise you’ll never feel rushed or pressured. We take the time needed to get it right; our commitment is to your peace of mind, not a sales quota.

Unbiased Guidance You Can Trust

We don’t have a favorite company. Our only goal is your parent’s protection. By 2026, the Medicare landscape has changed significantly with new out-of-pocket caps and drug plan restructuring. We simplify this 2026 jargon into clear, manageable choices. You won’t have to guess if a plan covers a specific medication or doctor. We check all 40 options to be sure. Learning how to help parents choose a medicare plan is easier when you have an advocate in your corner.

Our support doesn’t end when the application is signed. We provide year-round help to ensure your parents always have the coverage they deserve. If a doctor leaves a network or a prescription cost changes in 2027, we’re still here to help. We don’t disappear after the enrollment is complete; we stay by your side as your trusted guides.

Next Steps: Taking the Weight Off Your Shoulders

You don’t have to do this alone. We invite you to join your parent on a consultation call so everyone feels confident in the decision. We use a simple 5-step process to get them enrolled without the stress:

- Initial discovery of health needs, medications, and preferred doctors.

- Comprehensive review of 40+ available carriers in your specific zip code.

- Customized plan comparison that highlights the lowest total out-of-pocket costs.

- Simple, guided enrollment that avoids costly late penalties.

- Ongoing annual reviews to ensure the plan still fits as health needs change.

We are ready to help you move from a state of confusion to a state of total confidence. Schedule a Call with Paul today and let us handle the heavy lifting.

Moving From Confusion to Confidence in 2026

Helping your parents navigate the 2026 Medicare landscape doesn’t have to feel like a second job. We’ve shown you that gathering a clear checklist of their current doctors and medications is the first vital step. We also explored why comparing the latest 2026 premiums and out-of-pocket limits is essential to avoid late penalties. Knowing how to help parents choose a medicare plan means giving them the gift of security without the stress. You’ve done the hard work of learning the basics; now let us handle the heavy lifting of the fine print.

We compare over 40 carriers to ensure your family gets the perfect fit for their specific needs. Our team is licensed in 34+ states, and we provide this expert guidance at zero cost to your family. We’re here to make sure you’re never rushed and never pressured. Let’s replace that “Medicare maze” with a clear, simple path forward.

Schedule a Call With Paul – Move From Confusion to Confidence

You’re doing a great thing for your parents, and we’re honored to help you protect their health and happiness in the years ahead.

Frequently Asked Questions

When is the best time to start helping my parents with Medicare?

You should start the conversation 6 to 9 months before your parents turn 65. This gives us enough time to review their current prescriptions and doctors before their Initial Enrollment Period begins. Since the Inflation Reduction Act’s $2,000 out-of-pocket cap for Part D is fully in effect as of January 1, 2025, we’ll want to compare how different 2026 plans handle their specific medications to maximize savings.

Can I sign my parents up for Medicare myself?

You can help your parents enroll if you have a Power of Attorney or if they provide verbal permission during a recorded call with us. We often facilitate three-way calls to ensure everything is handled legally and accurately. Our goal is to show you how to help parents choose a medicare plan without the stress of navigating the Social Security website alone. We make the digital paperwork simple.

What if my parents are still working past age 65?

If your parent’s employer has 20 or more employees, they can usually delay Medicare Part B without a penalty. They’ll need to compare their current workplace premiums against 2026 Medicare costs. In 2026, the standard Part B premium is projected to be $194.50 per month, so we’ll help you calculate if staying on group coverage actually saves them money. We’ll look at the total deductible costs too.

Is there a penalty if my parents miss their enrollment window?

Missing the enrollment window results in a permanent 10% premium penalty for every 12-month period they were eligible but didn’t sign up. For Part D, the penalty is 1% of the national base beneficiary premium for every month they lacked creditable coverage. These costs add up over 10 or 20 years. We make sure your parents meet their specific seven-month Initial Enrollment Period so they don’t pay extra.

How much does it cost to use a Medicare broker like The Modern Medicare Agency?

Our services at The Modern Medicare Agency cost your parents $0 because we are compensated directly by the insurance companies. You’ll never receive a bill from us for our consultations or enrollment help. This allows us to provide unbiased guidance on how to help parents choose a medicare plan while ensuring they get the same monthly premium as if they signed up alone. We focus on their needs.

What is the difference between Medicare Advantage and a Medigap plan in 2026?

Medicare Advantage plans are private “all-in-one” alternatives that often have $0 premiums but require network doctors. Medigap plans, like Plan G, allow your parents to see any doctor in the U.S. who accepts Medicare. In 2026, many of our clients prefer Medigap to avoid the prior authorization hurdles that 30% of Advantage users sometimes face when seeking specialized care. We help you weigh the monthly costs versus flexibility.

Does Medicare cover dental and vision for my parents?

Original Medicare does not cover routine dental or vision care, but we can find 2026 Advantage plans that include these benefits. Many 2026 plans offer $1,500 to $2,500 in annual dental allowances for crowns and implants. If they choose Medigap, we’ll help them set up a separate policy so they don’t have to pay for cleanings or glasses entirely out of pocket. It’s about protecting their whole health.

What happens if my parent’s doctor leaves their plan’s network?

If a doctor leaves a Medicare Advantage network, your parent usually has to wait until the next Annual Enrollment Period to change plans. This window runs from October 15 to December 7 every year. We monitor these network changes for our clients. If a provider exit affects their access to care, we’ll guide them through the 2026 Special Enrollment Period options to find a new solution that keeps their healthcare consistent.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com