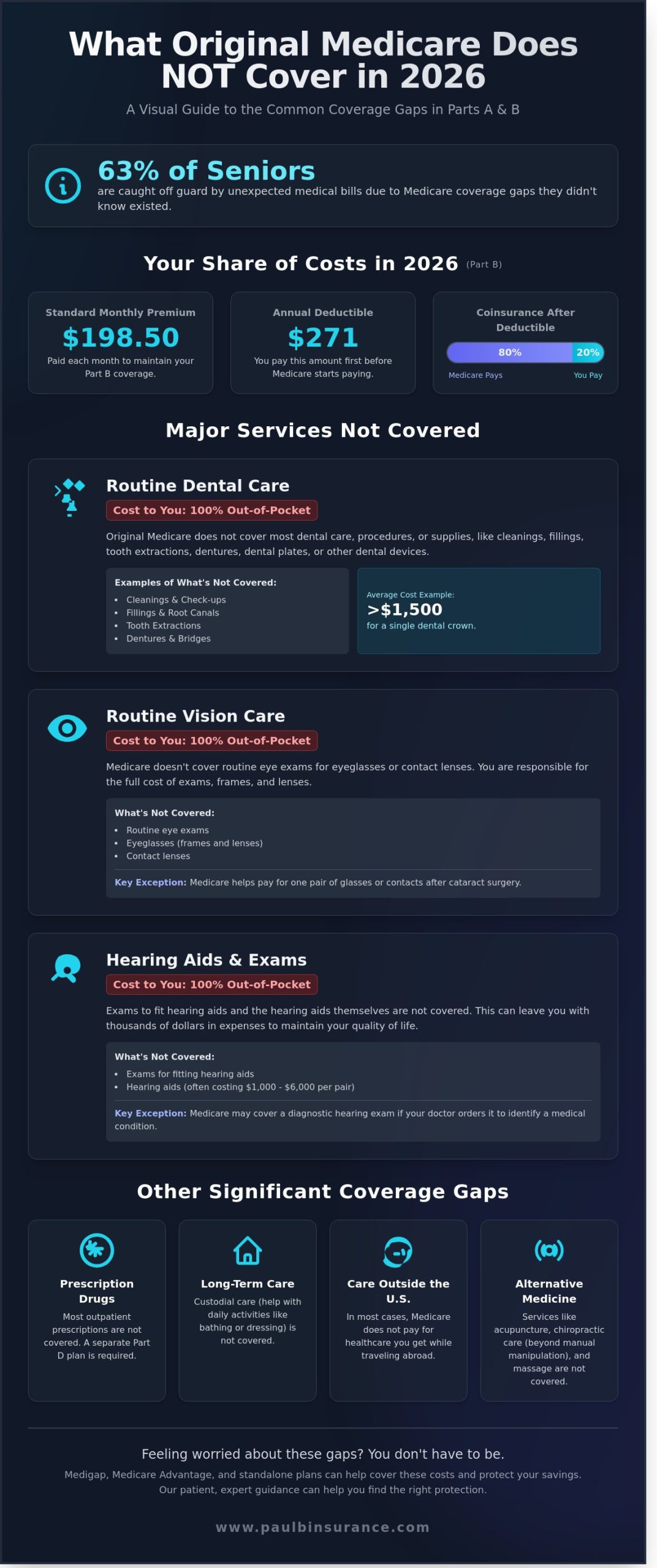

Last Tuesday, a client named Sarah called us after receiving a $1,450 bill for a dental procedure she thought was covered. Like 63% of seniors who don’t know exactly what medicare does not cover in 2026, she was caught off guard by a coverage gap she didn’t know existed. We understand how exhausting it is to feel like you’re constantly looking for hidden fees while trying to protect your hard-earned savings. You deserve to feel confident about your health instead of worrying about the next surprise in your mailbox.

In this guide, we explain the essential health services Original Medicare leaves out this year and how these omissions affect your wallet. We’ll simplify the jargon to show you why basic benefits still leave you vulnerable to costs like long-term care, vision, and hearing aids. By the time you finish reading, you’ll have a clear list of every major exclusion and a simple path to securing the full coverage you need for a stress-free retirement.

Key Takeaways

- Understand why Original Medicare was never designed to provide 100% coverage and how to identify the hidden costs that could impact your budget this year.

- Discover the simple truth about routine dental, vision, and hearing services, which remain significant out-of-pocket expenses for most seniors in 2026.

- We provide a clear roadmap of what medicare does not cover in 2026, including the high costs of long-term custodial care and the strict limits on alternative therapies.

- Learn how to navigate the updated prescription drug landscape and the new $2,000 out-of-pocket maximum to ensure your medications remain affordable.

- Find out how to close these risky coverage gaps with our patient, expert guidance on choosing the right protection to keep your hard-earned savings secure.

The Reality of Original Medicare in 2026: Why ‘Full Coverage’ is a Myth

Many of our clients begin their journey believing that their red, white, and blue card covers every medical bill they might receive. We see the stress and confusion this causes when that first unexpected bill arrives in the mail. The truth is that Original Medicare, consisting of Parts A and B, was never designed to pay for 100% of your healthcare costs. It functions as a shared-cost system between you and the government.

In 2026, the gaps in this system include significant deductibles, coinsurance payments, and entire categories of wellness care that remain outside the scope of traditional coverage. Relying solely on your basic Medicare card can lead to financial surprises during a health crisis. We focus on helping you understand what medicare does not cover in 2026 so you can plan with certainty. Our goal is to move you from a state of worry to a place of total confidence in your healthcare choices.

Understanding the 2026 Part B Deductible

For the 2026 calendar year, the Centers for Medicare & Medicaid Services (CMS) has set the standard Part B monthly premium at $198.50 for most beneficiaries. You are also responsible for the annual Part B deductible of $271 before your insurance begins to pay its share for outpatient services. You are responsible for the first few hundred dollars of your outpatient care each year. After meeting this deductible, you will generally pay a 20% coinsurance for most doctor services, outpatient therapy, and durable medical equipment.

The Difference Between ‘Medically Necessary’ and ‘Routine’

Medicare uses a strict definition to determine what qualifies for coverage in 2026. To be covered, a service must be “medically necessary,” meaning it is required to diagnose or treat a specific illness or injury. This creates a gap for routine care. While the government covers certain preventive screenings, these often differ from diagnostic tests in the eyes of the law. If a routine screening turns into a diagnostic procedure because a doctor finds a concern, your cost-sharing responsibilities change immediately. Prevention is not always covered the way we expect it to be, leaving many seniors to pay out of pocket for wellness visits that fall outside of very specific CMS guidelines.

We simplify the jargon so you know exactly how your plan works. If you are worried about these financial gaps, we invite you to explore how a Medigap plan can help cover these 20% coinsurance costs and deductibles. We are here to provide the unbiased guidance you need to protect your savings.

Routine Care Gaps: Dental, Vision, and Hearing Services

It often comes as a surprise to our clients that Original Medicare generally excludes the three things seniors rely on most: their teeth, eyes, and ears. Even in 2026, these routine services remain outside the scope of Part B coverage. Understanding what medicare does not cover in 2026 is the first step toward protecting your savings from unexpected medical bills. We want to help you move from confusion to confidence by identifying these gaps early.

The High Cost of Dental Exclusions

Original Medicare won’t pay for a root canal or a simple extraction because it views these as routine rather than medical. If you need cleanings, fillings, or dentures, you’ll likely pay 100% of the bill out-of-pocket. In 2026, the average cost for a single porcelain crown can exceed $1,500. We often recommend a standalone dental insurance plan to help manage these high costs. There are rare exceptions, such as when dental work is an integral part of a covered medical procedure like jaw reconstruction after an injury. However, for the vast majority of dental needs, you’re on your own without extra coverage.

Vision and Hearing: More Than Just ‘Routine’

Your vision and hearing are vital to your quality of life, yet Medicare coverage remains very limited. The one exception is that Medicare covers one pair of eyeglasses or contact lenses following cataract surgery. Beyond that, routine eye exams, frames, and lenses are your responsibility. Hearing care follows a similar pattern. Even if your doctor refers you for a hearing test, Medicare only pays if it’s to diagnose a medical condition. It won’t cover the exam if the goal is to fit a hearing aid. Hearing aid coverage remains a significant gap in what medicare does not cover in 2026, leaving many to pay full price for technology that keeps them connected to their families. If you’re feeling overwhelmed by these potential costs, you can view our guide on plans that often include these extra benefits.

Long-Term Care and Alternative Treatments: The Costs You Might Not Expect

We talk to families every day who feel overwhelmed by the fine print of their health insurance. One of the biggest shocks people face is realizing that Medicare doesn’t pay for long-term nursing home care. We call this the “custodial care” gap. If you need help with bathing, dressing, or getting out of bed, those costs fall entirely on you. While we help you find clarity, it’s vital to know that what medicare does not cover in 2026 includes the permanent, daily help many of us will eventually need.

The Nursing Home Trap

Medicare only pays for “skilled” nursing care for a maximum of 100 days per benefit period. To qualify, you must have a formal 3-day inpatient hospital stay first. The costs break down like this in 2026:

- Days 1 to 20: $0 co-pay per day.

- Days 21 to 100: A daily co-pay of $214.00.

- Days 101 and beyond: You are responsible for 100% of the bill.

We’ve seen how quickly these bills can drain a savings account. Defining “Custodial Care” is simple; it’s any non-medical care that helps you with activities of daily living. Because this isn’t considered medical treatment, Medicare won’t step in to help. Planning for these supports before you actually need them is the best way to protect your peace of mind and your family’s future.

Alternative Medicine and Wellness

Acupuncture is only covered for chronic low back pain, and it’s limited to 12 visits in a 90-day period. For chiropractic care, the rules are just as strict. Medicare only pays for manual manipulation of the spine to correct a subluxation, which is a misaligned joint. It won’t pay for x-rays, massage therapy, or routine adjustments to keep you feeling good. If you’re looking for gym memberships or programs like SilverSneakers, you’ll need to look at a Medicare Advantage plan because Original Medicare doesn’t include those wellness perks.

Many of our clients also ask about home health aides. Medicare pays for these aides only if you’re also receiving skilled therapy or nursing care at the same time. If you just need someone to help with meal prep, laundry, or errands, it’s your financial responsibility. Cosmetic surgery is also excluded unless it’s required to repair a malformation or an injury. Understanding what medicare does not cover in 2026 helps you avoid enrollment mistakes that lead to high costs. We’re here to make sure you have a simple path from confusion to confidence.

Prescription Drugs and International Travel: Where Part A and B Stop

Many people feel a sense of relief when they sign up for Original Medicare, thinking their medical costs are finally settled. However, understanding what medicare does not cover in 2026 is the only way to avoid a massive financial surprise at the pharmacy or while on vacation. Original Medicare (Parts A and B) treats outpatient prescription drugs as a separate category. If you don’t take specific action to enroll in a Part D drug plan, you’re responsible for 100% of your medication costs. Your local pharmacy prices can skyrocket without this coverage, leaving you to pay retail rates that often reach hundreds of dollars for a single refill.

The 2026 Prescription Drug Revolution

The year 2026 marks a major milestone for your wallet because of the Inflation Reduction Act. For the first time, your annual out-of-pocket spending for covered prescriptions is capped at exactly $2,000. The confusing “Donut Hole” that caused so much stress for decades is officially closed in 2026. While this cap provides peace of mind, you still need to be careful. Choosing a plan with the wrong “tier” structure for your specific specialty meds can still leave you with high monthly costs until you hit that $2,000 limit. We’ve seen drug prices vary by over 50% between different plans for the exact same medication.

Traveling with Peace of Mind

We often talk to seniors who are excited to finally use their retirement years to see the world. It’s vital to remember the “Border Rule.” Medicare coverage generally stops the moment you leave U.S. soil. If you suffer a medical emergency on a cruise ship or during a European tour, you could face a bill exceeding $50,000 without any help from Part A or B. This is another area where what medicare does not cover in 2026 can be dangerous for your savings. We recommend looking at specific supplemental plans that include a “Foreign Travel Emergency” benefit. These plans typically cover 80% of emergency costs abroad after a small $250 deductible, protecting your life savings while you explore.

Closing the Coverage Gaps: How We Help You Find the Right Protection

You don’t have to accept the financial risks that come with federal insurance gaps. Knowing what medicare does not cover in 2026 is just the first step toward protecting your retirement savings. We’re here to help you bridge those holes with two primary solutions. Our team uses a proven 5-step process to move you from a state of confusion to complete confidence. You’ll never feel rushed or pressured when you work with us because we act as your personal advocate.

The first path involves keeping your Original Medicare and adding a Medigap (Supplement) plan. This is a reliable way to eliminate the 20 percent coinsurance that often leads to massive out of pocket costs. The second path is switching to a Medicare Advantage plan. These plans act as an all-in-one alternative, frequently bundling the extra benefits that Medicare leaves out by default.

Medigap vs. Medicare Advantage

Medigap is the best fit for those who want total freedom of choice. You can visit any doctor or specialist in the country who accepts Medicare without needing a referral. It’s the right choice if you want to avoid surprise bills entirely. Medicare Advantage is often better for seniors who want dental, vision, and hearing coverage included for a low monthly premium. Because we represent over 40 different insurance carriers, we can match your specific doctors and medications to the plan that fits your life in 2026.

Your Next Steps for 2026

Don’t wait until you receive a high medical bill to realize your coverage is lacking. We simplify the complex insurance jargon so you understand exactly how your plan works. Our team does the heavy lifting by comparing hundreds of plan combinations for you. This ensures you steer clear of costly enrollment mistakes and late penalties that could follow you for years. Schedule a call with Paul and the team today to review your current 2026 coverage and ensure your peace of mind is protected.

Take Control of Your 2026 Healthcare Future

Navigating the gaps in your health coverage shouldn’t feel like a second job. As we look at the landscape this year, it’s clear that relying solely on Part A and Part B leaves you vulnerable to high costs for dental work, vision exams, and long-term care. Understanding what medicare does not cover in 2026 allows you to build a shield around your savings before an unexpected medical bill arrives. You don’t have to guess which plan fits your lifestyle or worry about missing a critical deadline.

We’ve helped thousands of seniors move from uncertainty to total clarity. As independent brokers licensed in 34+ states, we represent 40+ different carriers to ensure you get unbiased options rather than a limited sales pitch. Our signature 5-step “Confusion to Confidence” process is designed to simplify the jargon and put you back in the driver’s seat. We’ll look at your specific prescriptions and doctors to find the exact match for your needs.

Your health is too important to leave to chance. Schedule a Call With Paul to bridge your Medicare gaps today and let’s get you the protection you deserve. We’re here to make sure you feel supported every step of the way.

Frequently Asked Questions

Does Medicare cover dental implants or dentures in 2026?

Original Medicare doesn’t cover dental implants or dentures in 2026. You’ll pay 100% of the cost for these procedures unless you have a Medicare Advantage plan or private dental insurance. For instance, a single dental implant often costs $3,500 to $4,800 out of pocket. We help you navigate these gaps so you don’t face unexpected bills that drain your savings. Your smile and health shouldn’t be a source of financial stress.

How much does Medicare Part B cost in 2026?

The standard Medicare Part B premium is projected to be $188.40 per month in 2026. Most people have this amount deducted directly from their Social Security checks each month. If your individual income from 2024 was higher than $106,000, you might pay an extra amount known as IRMAA. Knowing exactly what medicare does not cover in 2026 helps you budget for these fixed costs and avoid any surprises during your retirement years.

Is long-term nursing home care covered by Medicare?

Medicare does not pay for long-term nursing home care or custodial help with daily living activities. While Medicare Part A covers up to 100 days of skilled nursing care after a 3-day hospital stay, it stops once you only need help with bathing or dressing. Since 70% of seniors will require some form of long-term support, this is a major gap. We can show you how to protect your assets from these high facility costs.

Does Medicare cover shingles or pneumonia vaccines in 2026?

Medicare Part D covers both shingles and pneumonia vaccines with a $0 copay in 2026. This benefit is part of the Inflation Reduction Act which ensures you pay nothing at the pharmacy counter for these essential shots. You won’t have to worry about the $200 price tags that used to be common for these preventive treatments. We want to make sure you stay healthy and protected without worrying about the cost of your medicine.

Can I get Medicare coverage if I travel to Europe or Mexico?

Original Medicare provides no coverage for healthcare services received in Europe, Mexico, or any other country outside the United States. If you have a medical emergency while traveling abroad, you’ll likely be responsible for the entire bill. Some Medigap plans, like Plan G, offer a foreign travel emergency benefit that covers 80% of the costs after a small deductible. We help you choose the right plan so you can travel with confidence and peace of mind.

What is the maximum out-of-pocket limit for Medicare in 2026?

Original Medicare has no maximum out-of-pocket limit in 2026, which means your potential medical costs are uncapped. However, the new $2,000 out-of-pocket cap for prescription drugs under Part D is now fully helping seniors save money. This $2,000 limit protects you from high pharmacy bills, but it doesn’t apply to your doctor visits or hospital stays. Understanding what medicare does not cover in 2026 is the first step toward finding a plan that stops unlimited medical spending.

Does Medicare pay for hearing aids or eye exams?

Medicare doesn’t cover routine eye exams, glasses, or hearing aids in 2026. You’ll pay the full price for a hearing aid, which usually averages $2,500 per ear. While Part B covers certain diagnostic tests for conditions like glaucoma or cataracts, it won’t help with a basic checkup or new frames. We can guide you toward supplemental options that include these vital benefits so you can keep seeing and hearing the world clearly without financial strain.

What happens if I don’t sign up for a Part D plan in 2026?

If you don’t sign up for a Part D plan when you’re first eligible in 2026, you’ll face a permanent late enrollment penalty. This penalty adds 1% of the national base premium to your monthly cost for every month you went without coverage. If you wait 36 months to join, your premium will be 36% higher for as long as you have coverage. We help you pick a simple plan now to steer clear of these costly lifetime mistakes.