On January 12, 2026, a retiree named Martha sat at her kitchen table looking at a $1,648 Part A deductible notice she didn’t expect. Like 65% of seniors who feel overwhelmed by their insurance options this year, she found herself asking: is it worth getting a medicare supplement plan to stop these surprises? We know that handling the maze of plan letters and the pressure from captive insurance agents can leave you feeling stressed and unprotected. You want to know that a single illness won’t deplete the savings you’ve worked 40 years to build.

We believe you deserve clarity instead of confusion. In this guide, we help you weigh the 2026 costs and benefits of Medigap so you can decide if that “peace of mind” is truly worth the investment for your health and budget. As independent experts, we’ll compare the most popular options for this year and show you how to secure predictable monthly healthcare costs as you move from confusion to confidence.

Key Takeaways

- Understand why the 20% gap in Original Medicare remains a major risk to your savings and how we help you protect your retirement in 2026.

- We walk you through a simple way to calculate your break-even point so you can finally decide is it worth getting a medicare supplement plan for your specific budget.

- Learn how the freedom of no networks and no referrals provides the predictable monthly costs you need for true peace of mind.

- Discover how to use your one-time “Golden Ticket” enrollment period to lock in the best rates regardless of your health history.

- See how our unbiased comparison of over 40 carriers moves you from confusion to confidence by finding the lowest price for your zip code.

The Hidden Costs of Original Medicare: Why the 20% Gap Matters in 2026

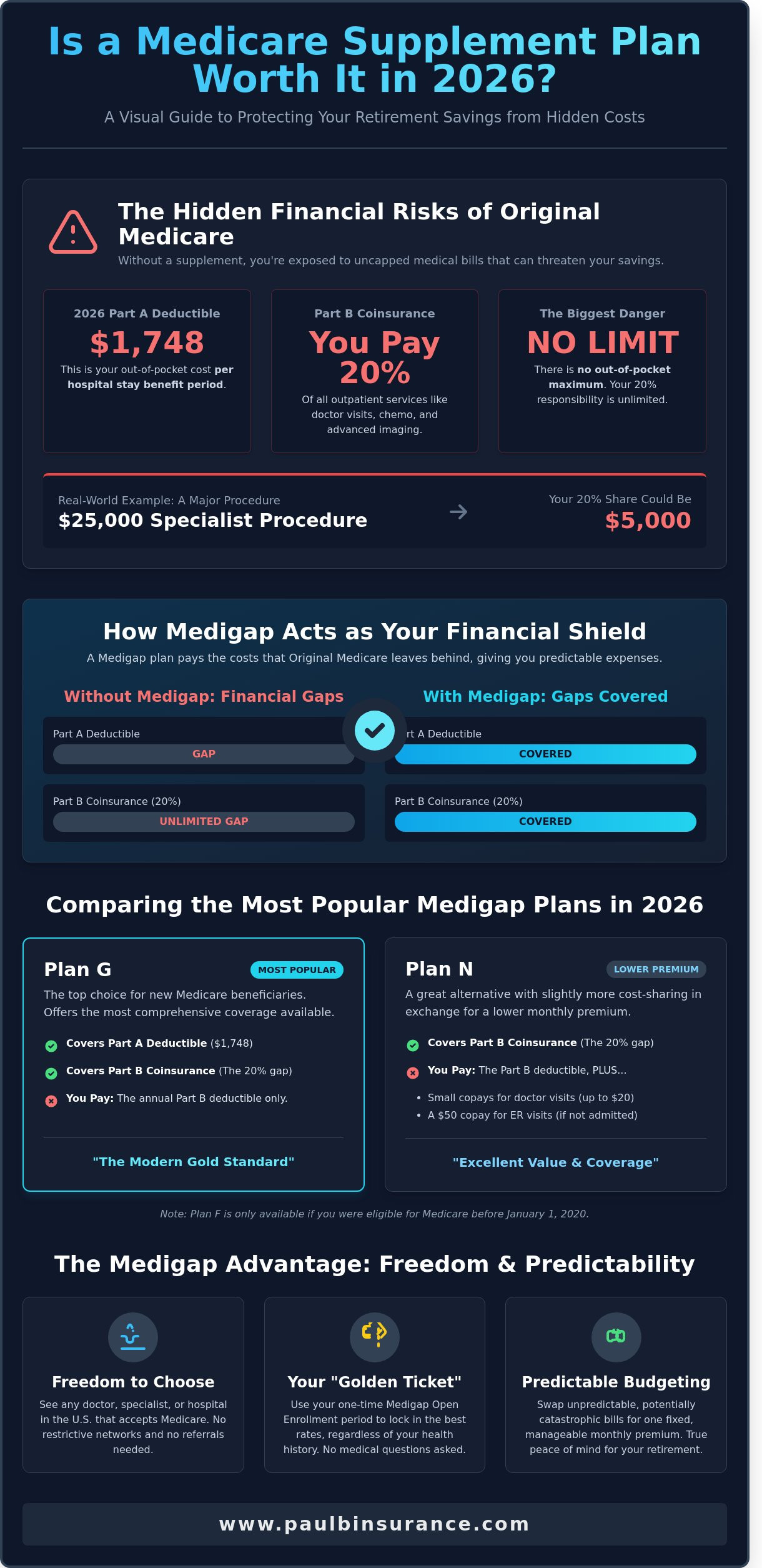

We talk to many people who feel stressed by the current Medicare system. It often feels like a maze where every turn leads to a new bill or a confusing statement. One of the biggest surprises for seniors in 2026 is the 80/20 rule. While Medicare pays for 80% of your doctor visits and outpatient care, you’re responsible for the remaining 20%. This uncapped gap is the primary reason why many wonder is it worth getting a medicare supplement plan this year.

Healthcare costs for specialists and outpatient procedures have risen by 4.5% over the last twelve months. If you require a series of treatments for a chronic condition, that 20% coinsurance can become a heavy burden. We focus on removing that anxiety by showing you how a supplement acts as a bridge over these financial gaps. Using Medigap (Medicare Supplement Insurance) helps cover these specific costs so you aren’t left guessing what you owe after every appointment.

What Exactly Does Original Medicare Leave Behind?

Original Medicare has two main parts, and both have financial holes that can swallow a retirement budget. For 2026, the Part A deductible for hospital stays has increased to $1,748. You pay this amount out of pocket before Medicare pays for your room and board. For Part B services, like chemotherapy, dialysis, or advanced imaging, you pay 20% of the total cost with no limit. These aren’t just small co-pays. If a specialist procedure costs $25,000, your share is $5,000. We see these five-figure bills often, and they can quickly drain a savings account.

The “No Limit” Risk You Should Know About

The most dangerous part of Original Medicare is the lack of a safety net. Most employer health plans have a cap on your spending, but the government plan does not. An out-of-pocket maximum is a fixed dollar limit that prevents you from spending your entire life savings on medical bills during a catastrophic health event. Without this limit, your 20% responsibility continues forever, regardless of how high the bill goes.

Deciding is it worth getting a medicare supplement plan often comes down to this single factor. A Medicare Supplement plan acts as a financial shield. It pays your share of the bills, effectively creating the out-of-pocket maximum that Medicare lacks. We want you to feel protected and empowered, knowing that a sudden illness won’t result in financial ruin. Our goal is to move you from confusion to confidence by securing a plan that provides a predictable monthly budget.

How Medicare Supplement (Medigap) Plans Work to Protect You

We know how overwhelming the Medicare maze feels. One question we hear daily from seniors is: is it worth getting a medicare supplement plan in 2026? To answer that, you first need to understand how these plans simplify your life. Unlike other insurance options, Medigap plans are standardized by the federal government. This means a Plan G with Company A provides the exact same medical coverage as a Plan G with Company B. According to the official U.S. government site for Medicare, these plans are designed to fill the “gaps” in Original Medicare, like your 20% coinsurance and various deductibles.

Because benefits are identical across companies, we can focus our energy on finding you the most stable price and a carrier with a strong history of small rate increases. You don’t have to worry about losing coverage for a specific procedure just because you switched insurers. This standardization brings a level of clarity that is rare in the insurance world. It allows you to make a choice based on value and trust rather than trying to decode complex benefit lists.

The Most Popular Medigap Plans in 2026

Plan G remains the top choice for our clients this year. It covers every gap that Original Medicare leaves behind, except for the annual Part B deductible. If you want lower monthly premiums, Plan N is a fantastic alternative. With Plan N, you’ll pay small copays for some doctor visits and emergency room trips, usually $20 or $50. We also want to clear up the confusion about Plan F. It’s still available in 2026, but only if you were eligible for Medicare before January 1, 2020. If you’re new to the system, Plan G is your modern version of the “Gold Standard.”

Network Freedom: Seeing Any Doctor in the U.S.

One of the biggest wins with Medigap is the total lack of networks. You can see any doctor, specialist, or hospital in the country that accepts “Medicare Assignment.” This term simply means the provider agrees to accept the Medicare-approved amount as full payment. You never need a referral to see a cardiologist or a physical therapist. This is why Medigap is the preferred choice for retirees who travel or spend winters in warmer states like Florida or Arizona. As long as the provider takes Medicare, your supplement plan works. You won’t ever hear the frustrating phrase, “that doctor is out-of-network.”

It’s vital to remember that Medigap plans don’t include prescription drug coverage. To protect your wallet at the pharmacy, you’ll need to pair your supplement with a standalone Medicare Part D plan. We help you coordinate these two pieces so your coverage is seamless and your medications are affordable. If you feel stuck, we can help you compare your options today to find the right fit for your unique situation.

Medigap Pros and Cons: Is the Monthly Premium Worth It?

Deciding how to spend your healthcare budget in 2026 can feel like walking through a maze. We know how it feels to look at a monthly bill and wonder if you’re overpaying for protection you might not use every day. You want to know: is it worth getting a medicare supplement plan when you could choose a plan with a $0 premium instead? The answer usually reveals itself when we look at your long-term financial safety rather than just the monthly cost.

Calculating your break-even point is the most logical way to find clarity. In 2026, a typical Plan G premium might average around $180 per month, totaling $2,160 for the year. If you face a major health event, such as a knee replacement or a five-day hospital stay, the 20% coinsurance you would owe under Original Medicare could easily exceed $5,000. In this scenario, the supplement pays for itself twice over in a single year. We focus on this predictability because it removes the “bill shock” that 62% of seniors report as their primary financial fear.

Stability is another major factor. While Medicare Advantage plans often change their co-pays, networks, and drug formularies every January 1st, Medigap benefits are standardized by the government. This means your coverage remains rock-solid year after year. You can find the specific benefit charts on the official Medicare website to see how these plans are structured to protect you.

The Pros of Choosing a Supplement

- Zero out-of-pocket costs: After you meet your small annual deductible, the plan picks up the rest of the bill for Medicare-covered services.

- Guaranteed renewability: As long as you pay your premium, the insurance company cannot cancel your policy, regardless of how many health claims you file.

- No Prior Authorizations: You and your doctor make the decisions. You won’t have to wait for an insurance company’s permission before receiving critical care or surgeries.

The Cons to Consider

The primary drawback is the higher upfront cost. These premiums generally increase as you age, often by 3% to 5% annually depending on your state’s pricing rules. These plans also lack “extra” perks. If you want coverage for routine cleanings or dentures, you will need to purchase a separate dental insurance plan. Finally, remember the “underwriting trap.” If you don’t buy a supplement when you are first eligible, you may have to pass a medical exam to get one later. By 2026, many carriers have tightened these health requirements, making it harder for people with chronic conditions to switch plans later in life. This is why we believe is it worth getting a medicare supplement plan early, while your health and options are most flexible.

When to Buy a Medigap Plan for the Best Rates

Timing is the most critical factor when deciding if is it worth getting a medicare supplement plan. We often describe the Medigap Open Enrollment Period as your “Golden Ticket” because it provides a guaranteed path to coverage regardless of your medical history. This six month window begins the very first day of the month you are 65 or older and enrolled in Medicare Part B. In 2026, with approximately 11,000 Americans reaching this milestone every day, understanding this timeline is essential for protecting your retirement savings.

Your medicare eligibility dates determine your leverage with insurance companies. If you apply during your initial window, companies cannot look at your health history or charge you more for chronic conditions. If you wait until 2027 or later to apply, you will likely face medical underwriting. This involves a detailed review of your prescriptions and doctor visits. We see many seniors who feel healthy today but find themselves locked out of coverage later because they developed a condition like high blood pressure or heart disease during the waiting period.

Your Initial 6-Month Window

This window is a strictly defined period that cannot be paused or restarted. Once your Part B is active and you are 65, the clock starts ticking. During these 180 days, you have the right to buy any plan offered in your state at the best available rate. Missing this specific window is the #1 mistake we see seniors make, and it can result in paying thousands more in out of pocket costs over your lifetime.

Switching Plans: Can You Change Your Mind?

Many people wonder if they can try a different path first. You might have a “Trial Right” if you join a Medicare Advantage plan when you are first eligible but decide to switch to a Medigap plan within the first 12 months. This gives you a safety net to change your mind without a health check. However, if you stay in another plan for several years, you lose this protection. We find that it’s much simpler to start with Medigap than to try and switch into it later when your health status is less certain.

There are also Guaranteed Issue Rights for special situations. If your current employer group coverage ends or your plan stops serving your zip code, you generally have 63 days to buy a supplement plan without answering health questions. We track these deadlines for our clients to move them from confusion to confidence. When you ask is it worth getting a medicare supplement plan, remember that the value is highest when you secure your spot early.

From Confusion to Confidence: How We Help You Decide

We know that deciding is it worth getting a medicare supplement plan in 2026 feels like a heavy burden. The Medicare system hasn’t gotten any easier to understand this year, and the sheer volume of mail on your kitchen table is proof of that. That’s why we walk beside you as a patient guide. We don’t work for the big insurance companies, we work for you. Most agents you meet are “captive,” meaning they are employees of one specific brand and can only show you their own products. We are independent brokers. We compare over 40 different carriers in your specific zip code to find the lowest price for the exact same coverage. If one company raises their rates, we have the freedom to move you to another that treats you better.

Our promise to you is simple. You will never feel rushed and you will never feel pressured. We follow a proven 5-step process to move you from a state of overwhelm to feeling fully protected:

- The Discovery Interview: We start by listening. We learn about your health priorities, your budget, and what “peace of mind” looks like for you in 2026.

- Deep Market Analysis: We don’t just look at the famous brands. We scan 40+ companies, including smaller, highly-rated carriers that often offer lower premiums for the exact same Plan G or Plan N benefits in your specific neighborhood.

- The Jargon-Free Comparison: We strip away the insurance industry “double-speak.” We show you a clear, side-by-side comparison so you can see exactly where your money goes.

- White-Glove Enrollment: We handle the paperwork for you. We ensure every form is filled out correctly to avoid the common enrollment mistakes that lead to late penalties or coverage gaps.

- Lifetime Advocacy: Our job doesn’t end when your card arrives. We provide ongoing support and annual reviews. If a carrier introduces a more competitive rate in 2027, we are the first to let you know.

Why an Independent Broker Benefits You

Captive agents are limited to one set of tools. If their company raises rates by 12 percent, they can’t offer you a better deal. We track the rate increase histories of every company we represent over the last decade. This data allows us to recommend stable companies that won’t surprise you with huge price hikes next year. Our Medigap guidance ensures you aren’t just getting a low price today, but a stable plan for the long haul. We provide the expert perspective you need to decide if the monthly premium fits your long-term retirement goals.

Your Next Steps to Peace of Mind

You don’t have to face the Medicare Maze alone. To get started, you can schedule a simple, no-obligation strategy session with us. It’s a low-pressure way to get your questions answered by an expert. Before we talk, please have a list of your current medications and your preferred doctors ready. This helps us ensure your plan fits your life perfectly. We are here to help you move from confusion to confidence. It’s time to stop worrying about unexpected medical bills and start enjoying your retirement with the security you deserve. Reach out today and let us do the heavy lifting for you.

Take the Next Step Toward Total Health Security in 2026

Navigating the 20% gap in Original Medicare doesn’t have to be a source of stress. We’ve seen how these uncovered costs can quickly add up, especially with the updated 2026 deductible and coinsurance rates. By choosing a Medigap policy, you’re effectively putting a ceiling on your out-of-pocket expenses. You might still be wondering, is it worth getting a medicare supplement plan this year? When you consider the protection against unexpected bills and the freedom to see any doctor who accepts Medicare, the answer for most seniors is a resounding yes.

We believe you deserve a partner who puts your needs first. Unlike a captive agent who only shows you one brand, our team of independent brokers works for you. We provide access to over 40 top-rated insurance carriers and offer licensed expertise across 34 states. We’ll help you move from confusion to confidence by comparing every option side by side. Don’t let the complex maze of 2026 regulations slow you down. We’re here to make sure you’re protected and empowered.

Schedule a Call With Paul to Find Your Perfect Plan

We look forward to helping you find the clarity and coverage you deserve.

Frequently Asked Questions

Is it worth getting a Medicare Supplement plan if I am healthy?

Yes, it is worth getting a medicare supplement plan even if you feel great today. Think of it as a safety net for your hard-earned savings. While you might not need it this month, health can change in an instant. In 2026, the Part A deductible has risen to $1,712 per benefit period. Without a plan, one unexpected week in the hospital could cost you thousands of dollars out of pocket. We want you to have peace of mind knowing your costs are capped.

Can I have both a Medicare Supplement plan and a Medicare Advantage plan?

No, you cannot have both types of coverage at the same time. It’s actually illegal for an agent to sell you a Medigap policy if they know you have a Medicare Advantage plan. You have to choose one path or the other. We help you look at your specific doctors and budget to decide which route gives you the most confidence. If you try to use both, the claims will get stuck in a maze of denials, leaving you with the bill.

How much does a typical Medigap plan cost in 2026?

In 2026, most 65-year-olds see monthly premiums between $165 and $235 for a standard Plan G. Prices vary based on where you live and your tobacco use. For example, a non-smoker in Florida might pay $210, while someone in Iowa might pay $155 for the same coverage. We always check every available carrier to find the lowest rate for your zip code. This ensures you don’t overpay for the exact same government-standardized benefits.

What happens if I miss my Medigap Open Enrollment Period?

If you miss your six-month window, insurance companies can look at your medical history and potentially deny your application. This period starts the first day of the month you’re both 65 and enrolled in Part B. Outside of this time, you’ll likely face medical underwriting. This means the company asks about your heart health or past surgeries. We guide you through these dates so you don’t get locked out of coverage or forced into higher rates due to a missed deadline.

Does a Medicare Supplement plan cover dental and vision?

Standard Medigap plans don’t include routine dental, vision, or hearing coverage. These plans are designed to fill the gaps in Part A and Part B, like coinsurance and deductibles. To get help with the cost of cleanings or new glasses, we usually recommend adding a separate, affordable policy. This keeps your medical coverage strong while still protecting your teeth and eyes. It’s a simple way to build a complete safety net without any hidden surprises.

Is Plan G better than Plan N for most people?

Plan G is often considered better for those who want zero surprises, but Plan N is a fantastic way to save about $500 per year in premiums. With Plan G, you only pay the Part B deductible, which is $257 in 2026. With Plan N, you pay that same deductible plus small copays of up to $20 for office visits. We’ll help you do the math to see if the monthly savings on Plan N outweigh those occasional small costs.

Do Medigap premiums go up every year?

Yes, you should expect your premium to increase by 3% to 6% each year. These adjustments happen because of your age and the rising cost of medical care across the country. However, we don’t just let you sit with a plan that gets too expensive. Our team monitors these rate hikes for you. If your current company raises prices too much, we’ll look at other trusted carriers to see if we can find a better deal for your budget.

What is the most popular Medicare Supplement plan for 2026?

Plan G is the most popular choice for people joining Medicare in 2026. It currently accounts for 62% of all new Medigap policies because it’s so simple to use. You can visit any doctor in the country who accepts Medicare, and you’ll never receive a bill for a covered service after you meet the annual deductible. This predictability is why so many seniors tell us they feel a huge sense of relief once their Plan G is active.