Paying a higher monthly premium for the “full coverage” of Plan F might actually be the very thing causing your financial stress in 2026. We know how it feels to stare at a stack of insurance mailers and feel your heart sink. You want total protection from medical bills, but you don’t want to overpay for a name. When comparing medigap plan f vs plan g, the choice often comes down to one small number: the Part B deductible.

We know you value security and want to avoid any surprise costs at the doctor’s office. We promise to simplify the jargon and show you the 2026 hidden math so you can stop guessing about your coverage. This guide explores why the January 1, 2020 eligibility rule still matters today and how medical underwriting impacts your ability to switch. You’ll get a clear roadmap to help you move from confusion to confidence while securing the lowest possible monthly premium for your health needs.

Key Takeaways

- Understand the 2020 cutoff rule and whether you are still eligible to keep or join the most comprehensive Medicare Supplement plans available in 2026.

- We simplify the medigap plan f vs plan g debate by revealing the 2026 math behind the Part B deductible and which choice truly protects your savings.

- Discover the specific “Trial Right” and “Guaranteed Issue” periods that allow you to switch plans without the stress of a medical exam.

- Learn how to avoid the “captive agent” trap and use an independent advocate to scan the entire 2026 market for your best value.

- Clear the confusion around rising premiums and see our step-by-step guide to securing a plan that offers you confidence and predictable costs.

Understanding the Basics of Medigap Plan F and Plan G in 2026

Trying to make sense of your healthcare options often feels like wandering through a maze without a map. We know how stressful it is to face a stack of insurance mailers that all say something different. Our mission is to move you from confusion to confidence by making these choices clear and simple. We want you to feel protected, not pressured. We simplify the jargon so you know exactly how your coverage works.

Medicare is a vital safety net, but it doesn’t pay for everything. Original Medicare generally covers about 80% of your medical costs. That remaining 20% can lead to massive bills if you have a serious health event. This is where Medigap, also known as Medicare Supplement Insurance, comes in. It acts as a bridge, crossing the gap between what Medicare pays and what you owe. When we look at medigap plan f vs plan g, we are comparing the two most robust options available to help you sleep better at night.

The right choice for you often comes down to your Medicare “birthday.” If you were eligible for Medicare before January 1, 2020, you have access to both plans. If you became eligible after that date, Plan G is your top tier option. We help you figure out exactly where you stand so you can steer clear of costly enrollment mistakes.

What Exactly Is a Medigap Plan?

A Medigap plan is a private insurance policy designed to work hand in hand with your Part A and Part B coverage. These plans help eliminate those surprise hospital or doctor bills that can drain a savings account. Even though private companies sell these policies, the government requires standardized Medigap plans to ensure you get specific benefits regardless of the carrier. You can learn more about how these pieces fit together in our Medicare Supplement Insurance guide. We are here to be your calm, patient guide through this process.

The “First-Dollar” Coverage Concept

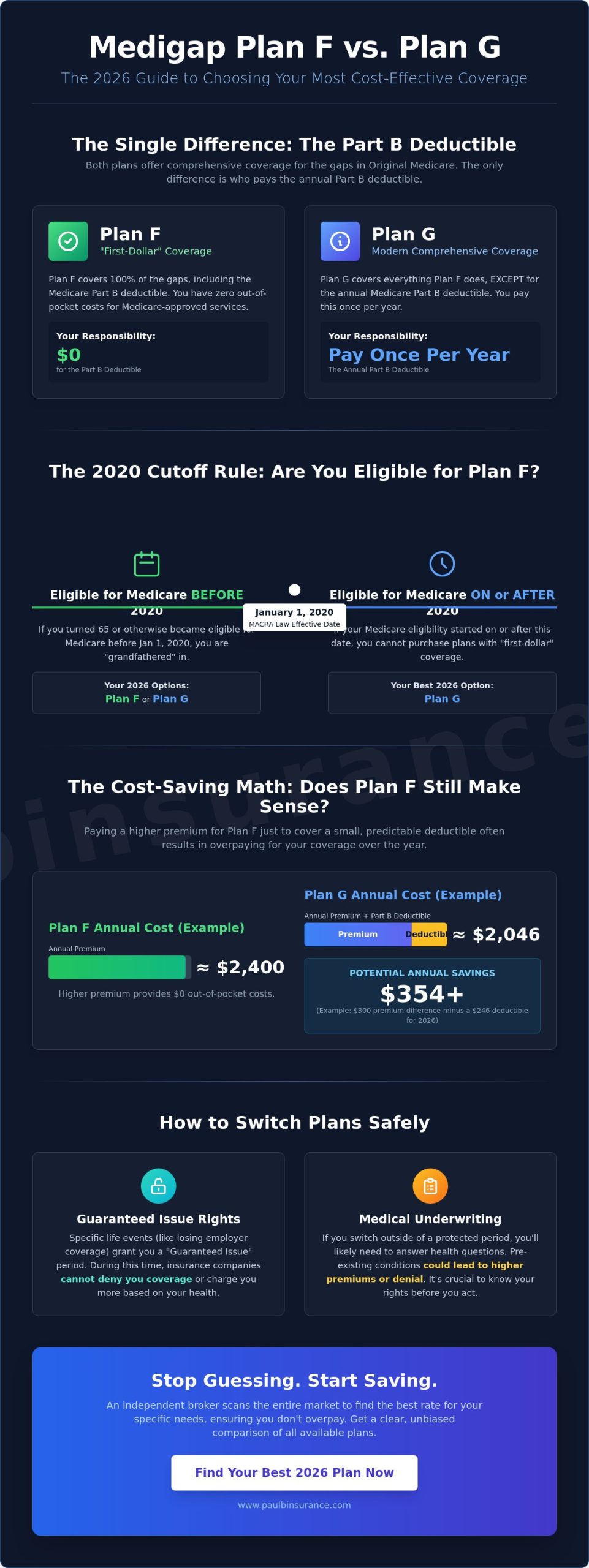

For decades, Plan F was the undisputed king of Medicare supplements because it offered first-dollar coverage. This means you have $0 out of pocket costs at the doctor office. You don’t even have to reach a deductible before the plan starts paying. In 2026, first dollar coverage is a legacy feature. Federal law changed on January 1, 2020, to phase out plans that cover the Part B deductible for new enrollees. This shift is why the medigap plan f vs plan g debate is so important today. While Plan F still exists for those grandfathered in, Plan G has become the modern standard for comprehensive care without the high price tag of older legacy plans.

The Eligibility Rule: Why Your Initial Medicare Date Changes Everything

If you have spent any time researching the medigap plan f vs plan g debate, you might feel like you arrived at the party just as the doors were closing. It is a common source of stress for our clients. We often hear from seniors who feel frustrated because they heard Plan F was the “gold standard,” only to find out it isn’t even an option on their enrollment forms. We want to clear up that confusion right now. You haven’t necessarily missed out on a better deal; you’re simply following a different set of rules designed for a new era of Medicare.

The shift happened because of a law called MACRA, which stands for the Medicare Access and CHIP Reauthorization Act of 2015. This law changed the landscape of supplemental insurance by prohibiting the sale of plans that cover the Part B deductible to anyone “newly eligible” for Medicare on or after January 1, 2020. The goal was to ensure beneficiaries have a small amount of “skin in the game” regarding their outpatient costs. While this feels like an extra hurdle, we are here to show you that Plan G is a powerful and often more cost-effective alternative.

Who Can Still Buy Medigap Plan F in 2026?

Even in 2026, Plan F is not completely gone. It’s simply restricted to a specific “grandfathered” group of people. If you turned 65 or became eligible for Medicare due to a disability before January 1, 2020, you’re still eligible for Plan F today. This is true even if you didn’t buy it back then. You can still switch from your current coverage to a Plan F, or even move between different Plan F providers to find a better rate, provided you can pass the health underwriting requirements in your state.

Any individual who attained age 65 or became eligible for Medicare benefits prior to January 1, 2020, retains a permanent right to purchase Medigap Plan F.

If you fall into this group, we can help you compare the costs to see if the higher premiums of Plan F still make sense. Sometimes, the peace of mind of having zero out-of-pocket costs is worth the extra monthly expense. If you want to see how these rules apply to your specific birthday, you can view our Medigap comparison resources to find your best fit.

Why Plan G Is the New Standard for New Enrollees

For those of you turning 65 in 2026, Plan G is the most comprehensive coverage the law allows you to buy. It covers every single gap in Medicare except for the Part B deductible. In 2026, that deductible is a relatively small annual amount that you pay once per year before the plan takes over completely. The government removed the deductible coverage to encourage more thoughtful use of medical services, but the trade-off is often lower monthly premiums for you.

- Plan G covers 100% of Part A hospital costs and coinsurance.

- It covers 100% of Part B excess charges, which Plan F also covers.

- The only difference is that you pay the Part B deductible yourself.

We find that most of our clients actually prefer this setup. When we do the math together, the yearly savings on Plan G premiums often outweigh the cost of that one-time deductible. Choosing between medigap plan f vs plan g in 2026 often comes down to when you started your Medicare journey, but rest assured that Plan G offers nearly identical protection and incredible peace of mind.

Comparing Coverage and Costs: The Plan F vs. Plan G Price Gap

We know that looking at insurance charts can feel like staring at a bowl of alphabet soup. It is easy to feel overwhelmed by the options, but we are here to help you find clarity. When we look at medigap plan f vs plan g in 2026, the comparison is actually much simpler than it looks. These two plans are nearly identical twins. They both cover your hospital stay costs, your 20 percent coinsurance for doctor visits, and even foreign travel emergencies. They use the exact same networks; if a doctor accepts Medicare, they accept both of these plans.

The only difference between them is how the Medicare Part B deductible is handled. Plan F pays this for you, while Plan G requires you to pay it out of your own pocket once per year. In 2026, the Centers for Medicare and Medicaid Services (CMS) has set this deductible at approximately $270. That is the only “gap” in coverage you need to worry about when choosing between these two paths.

The Coverage Chart: Side-by-Side Comparison

To give you total confidence in your choice, we want to highlight how much these plans have in common. Both plans provide 100 percent coverage for the following items:

- Medicare Part A hospital deductible and coinsurance.

- Part B excess charges (important if a doctor charges more than the Medicare approved amount).

- The first three pints of blood needed for a medical procedure.

- Skilled nursing facility care coinsurance.

Because the benefits are standardized by the government, a Plan G with one company offers the exact same medical coverage as a Plan G with another. The lone outlier remains that Part B deductible. We often tell our clients that paying a higher premium for Plan F is simply paying the insurance company to write a check that you could easily write yourself.

The “Hidden Math” of Plan G

We believe in being your advocate, which means showing you where the “hidden” savings live. To find the true value, we use a simple three step formula. First, we take the monthly premium for Plan F and subtract the Plan G premium. Second, we multiply that number by 12 to see your annual savings. Finally, we compare that total to the $270 Part B deductible.

For example, if Plan F costs $50 more per month than Plan G, you are paying $600 extra per year in premiums. “In 2026, we often find that Plan F owners are essentially paying an insurance company $600 just to avoid a $270 bill.” By choosing Medigap Plan G, you keep $330 in your own bank account.

Stability is another reason we prefer Plan G for most seniors. Because Plan F is “closed” to new Medicare members who joined after 2020, the group of people in those plans is getting older. Older groups typically have more health claims, which causes premiums to rise faster. Plan G remains open to everyone, which generally leads to more stable rates over time. We want to make sure you have a plan that stays affordable long after your initial enrollment.

Is It Time to Switch? How to Move from Plan F to Plan G Safely

Many seniors feel a deep sense of loyalty to Plan F, but they also feel the weight of rising monthly premiums. We often hear the same concern: “What if I switch and my health declines later?” It’s a natural fear. However, in 2026, the cost difference in the medigap plan f vs plan g debate has become too large to ignore. Most Plan F users are paying $500 to $800 extra every year just for the “convenience” of not paying a small annual deductible. That is money that should stay in your pocket.

We want to put your mind at ease. If you decide to move, you don’t lose your protection. Plan G covers everything Plan F does except for the Part B deductible, which is $257 in 2026. If your health changes after you’re on Plan G, your coverage is still “guaranteed renewable.” This means the insurance company cannot cancel your policy or raise your rates specifically because of your health. You have the same ironclad protection you’ve always had, just at a better value.

The Medical Underwriting Process Simplified

Underwriting is not a long, drawn-out ordeal. It usually involves a 15-minute phone call and a quick review of your current medications. In 2026, we find that about 85% of our clients in relatively stable health pass this process easily. Common conditions like well-controlled high blood pressure, high cholesterol, or even managed Type 2 diabetes are typically “auto-pass” items for many carriers. We focus on ensuring you’re a good candidate before we ever submit an application. We pre-screen every client to protect you from a denial. If you’re currently managing a serious condition like active cancer treatment, a planned heart surgery, or end-stage renal disease, we’ll be honest and tell you that staying on Plan F is your safest bet. Our goal is your security, not just a sale.

Step-by-Step Transition Guide

Moving from one plan to another doesn’t have to be stressful. We follow a proven path to move you from confusion to confidence without any gaps in your coverage. We handle the heavy lifting so you can focus on your life.

- Step 1: Get a customized quote for Plan G from a Medicare broker who can compare every company in your zip code to find the lowest rate.

- Step 2: Apply for your new Plan G policy before you cancel your current Plan F. We never want you to leave your old plan until the new one is officially approved and in your hands.

- Step 3: Set the effective date for the 1st of the upcoming month. This ensures a seamless handoff so you never spend a single day without your supplemental insurance coverage.

We’re here to make sure you don’t make a costly mistake. If you want to see if you qualify for these 2026 savings, view our Medigap comparison tools to get started today.

Why Working with an Independent Broker Simplifies Your 2026 Choice

Deciding on medigap plan f vs plan g in 2026 feels like a math problem that never ends. You shouldn’t have to solve it alone. Most people talk to a “Captive Agent” without knowing it. These agents work for one specific insurance company. Their job is to sell you that company’s product, even if a better deal exists across the street. We do things differently. As independent brokers, we represent over 40 different insurance companies. We don’t work for the carriers; we work for you. This means we can look at the whole market to find the right fit for your budget and your health needs.

Our role is to act as your personal advocate. We aren’t here to push a specific brand. Instead, we help you weigh the pros and cons of each carrier based on their real-world performance. We provide year-round support that lasts long after you sign your application. If you receive a confusing bill in six months or need help understanding a benefit change in 2027, we are just a phone call away. We help you move from confusion to confidence by handling the heavy lifting of the insurance search for you.

The Power of Choice: Comparing 40+ Carriers

In 2026, every company offering a Medigap plan must provide the exact same set of benefits for that letter grade. A Plan G with AARP has the same coverage as a Plan G with Mutual of Omaha or Aetna. However, the premiums can differ by hundreds of dollars per year. We help you find the “sweet spot” where low monthly costs meet high financial stability ratings. You can visit our Medigap service page to see how we compare these rates side by side. We look at the history of rate increases so you aren’t surprised by a massive price jump later on.

Our No-Pressure, No-Jargon Approach

Paul Barrett started this mission to help seniors move from confusion to confidence. We know the 2026 Medicare system feels like a maze. Our team takes the time to explain the nuances of medigap plan f vs plan g without using confusing industry talk. You’ll never feel rushed or pressured to make a decision. Best of all, our services are 100% free to you. The insurance companies pay us a commission for helping you enroll, so your premium stays exactly the same as if you went directly to the carrier. We are here to protect your health and your wallet, one simple conversation at a time.

Take Control of Your Medicare Journey

Choosing between medigap plan f vs plan g in 2026 comes down to one simple question: are you getting the best value for your hard-earned money? We’ve seen that while Plan F offers the convenience of zero out-of-pocket costs, its premiums continue to climb for those who were eligible before 2020. Plan G remains the standout choice for most seniors today, offering robust protection and lower monthly rates even after you account for the annual Part B deductible. Switching might require answering a few health questions, but we’ll help you navigate that process safely.

You don’t have to face these complex decisions alone. Our team provides unbiased guidance from 40+ top-rated carriers across 34+ states to ensure you’re never overpaying for coverage. We take pride in offering 5-star personalized support for both Medicare Supplement and Medicare Advantage Plans. Let’s look at your specific situation together and find a plan that lets you sleep soundly at night.

Schedule a Call With Paul: Let’s Turn Your Medicare Confusion Into Confidence

We’re ready to help you simplify your 2026 Medicare journey today.

Frequently Asked Questions

Is Plan F being phased out completely in 2026?

No, Plan F is not being phased out for everyone in 2026. It remains available to anyone who was eligible for Medicare before January 1, 2020. If you already have Plan F, you can keep it as long as you continue to pay your premiums. We help many clients maintain this coverage every year, though it’s no longer an option for those who are new to Medicare.

Can I switch from Plan G back to Plan F later if I change my mind?

Moving from Plan G back to Plan F is very difficult and usually requires passing a medical exam. Since Plan F offers more coverage by paying the Part B deductible, insurance companies view it as a higher risk. Unless you live in a state with specific “birthday rules” or “guaranteed issue” periods, you might be denied based on your health history. We recommend choosing carefully now so you don’t feel trapped later.

Does Plan G cover the Part B deductible in 2026?

Plan G does not cover the Part B deductible, which is $257 in 2026. You are responsible for paying this amount out of your own pocket once per calendar year before your supplemental benefits begin. This is the primary difference to remember when comparing medigap plan f vs plan g. Once you meet that annual deductible, Plan G provides the exact same 100 percent coverage as Plan F.

How much can I expect to save by switching from Plan F to Plan G?

Most seniors save between $400 and $600 per year in premiums by switching to Plan G in 2026. Even after you pay the $257 Part B deductible yourself, you often end up with a net gain of several hundred dollars. We look at your specific zip code to find the exact price gap. These savings help provide the peace of mind that you aren’t overpaying for your healthcare.

Will my doctor know if I switch from Medigap Plan F to Plan G?

Your doctor’s office will see the change when they scan your new insurance card, but it won’t affect your access to care. Both plans allow you to see any provider in the United States who accepts Medicare. Because Medicare remains your primary payer, your doctor receives the same reimbursement regardless of which lettered plan you choose. We ensure your transition is smooth so your medical care never misses a beat.

What happens if I have a pre-existing condition and want to switch to Plan G?

If you have a pre-existing condition, you may have to answer health questions on a medical application to switch to Plan G in 2026. In most states, insurance companies can look at your medical records and decide to charge you more or deny your application entirely. However, 4 states currently have community rating laws that protect you. We can review your health history privately to see which companies are most likely to accept your application.

Is there a “High Deductible” version of Plan G available in 2026?

Yes, High Deductible Plan G is a widely available option this year with a 2026 deductible of $2,870. This plan offers significantly lower monthly premiums because you agree to pay the first few thousand dollars of your medical costs yourself. It’s a great strategy for healthy individuals who want to protect their savings from a catastrophic illness without paying high monthly fees. We can help you decide if the lower premium is worth the higher risk.

Do Plan F and Plan G cover prescription drugs (Part D)?

Neither Plan F nor Plan G includes coverage for retail prescription drugs that you pick up at a pharmacy. To get help with those costs, you must enroll in a separate Standalone Part D plan. When we analyze medigap plan f vs plan g for your situation, we also look at your current medications. This ensures your total package covers both your doctor visits and your prescriptions without any hidden gaps.