The “cheapest” monthly premium might actually cost you more in stress than it saves you in dollars. Choosing between medigap plan G vs plan N for new enrollees isn’t just a math problem; it’s a test of your personal “hassle threshold” regarding copays and surprise bills. We know the Medicare system feels like a crazy maze, especially when you’re being pressured by captive agents who only show you one side of the story. You want to feel protected, not confused, and you certainly don’t want to worry about “excess charges” every time you see a specialist.

We’re here to help you move from confusion to confidence by comparing these two popular options for 2026. In this guide, we’ll break down why Plan G’s $120 to $250 monthly premium offers total peace of mind after you meet the $283 Part B deductible. We’ll also look at Plan N, where premiums are typically $25 to $60 lower per month but require $20 office copays and don’t cover Part B excess charges. You’ll get a clear look at the numbers and the benefits so you can choose the right coverage with total certainty.

Key Takeaways

- Understand why Plan G and Plan N are the primary choices for 2026 now that older plans like Plan F are no longer available to new enrollees.

- Learn how Plan G provides the most comprehensive “peace of mind” coverage, leaving you with only the $283 Part B deductible as an out-of-pocket cost.

- Compare medigap plan G vs plan N for new enrollees to see if trading slightly lower premiums for small office copays fits your personal “hassle threshold.”

- Discover how to protect yourself from “excess charges” that some doctors may bill beyond what Medicare typically pays.

- Find out how our simple 5-step process helps you steer clear of captive agents and find the unbiased guidance you deserve.

Why Plan G and Plan N Are the Top Choices for New Medicare Enrollees

Entering the Medicare system in 2026 feels different than it did just a few years ago. Many people are moving away from Medicare Advantage plans because of shrinking networks and changing benefits. Instead, they’re looking for the stability of Original Medicare paired with a supplement. For anyone starting their journey now, the conversation almost always boils down to medigap plan G vs plan N for new enrollees. These two plans account for about 90% of our new clients because they offer the best balance of protection and value.

You might hear older friends or neighbors talk about Plan F. While it was once the most popular choice, federal law changed the landscape on January 1, 2020. If you’re new to Medicare today, you aren’t allowed to buy a plan that covers the Part B deductible. This rule pushed Plan G to the top spot as the most comprehensive option available for those who want the least amount of “bill surprises.”

What Are Medigap Plans? Simply put, they’re private insurance policies designed to pay the costs that Original Medicare leaves behind. Without one, you’re responsible for 20% of your medical bills with no upper limit. That’s a scary thought when you’re trying to plan a budget. A supplement fills those “gaps” so you can visit the doctor without fear.

The Standardized Benefit Rule

We want you to know a secret that captive agents often hide. Every Plan G offers the exact same medical benefits, regardless of which company sells it. A Plan G with a famous household name provides the same coverage as one from a smaller, stable company. We help you shop across dozens of carriers at our Medigap resource page to find the best rate. In early 2026, we saw some Plan G rates jump by 12% to 26% in certain states. This makes choosing a carrier with a history of stable pricing more important than just picking a big brand name.

What Both Plans Cover in 2026

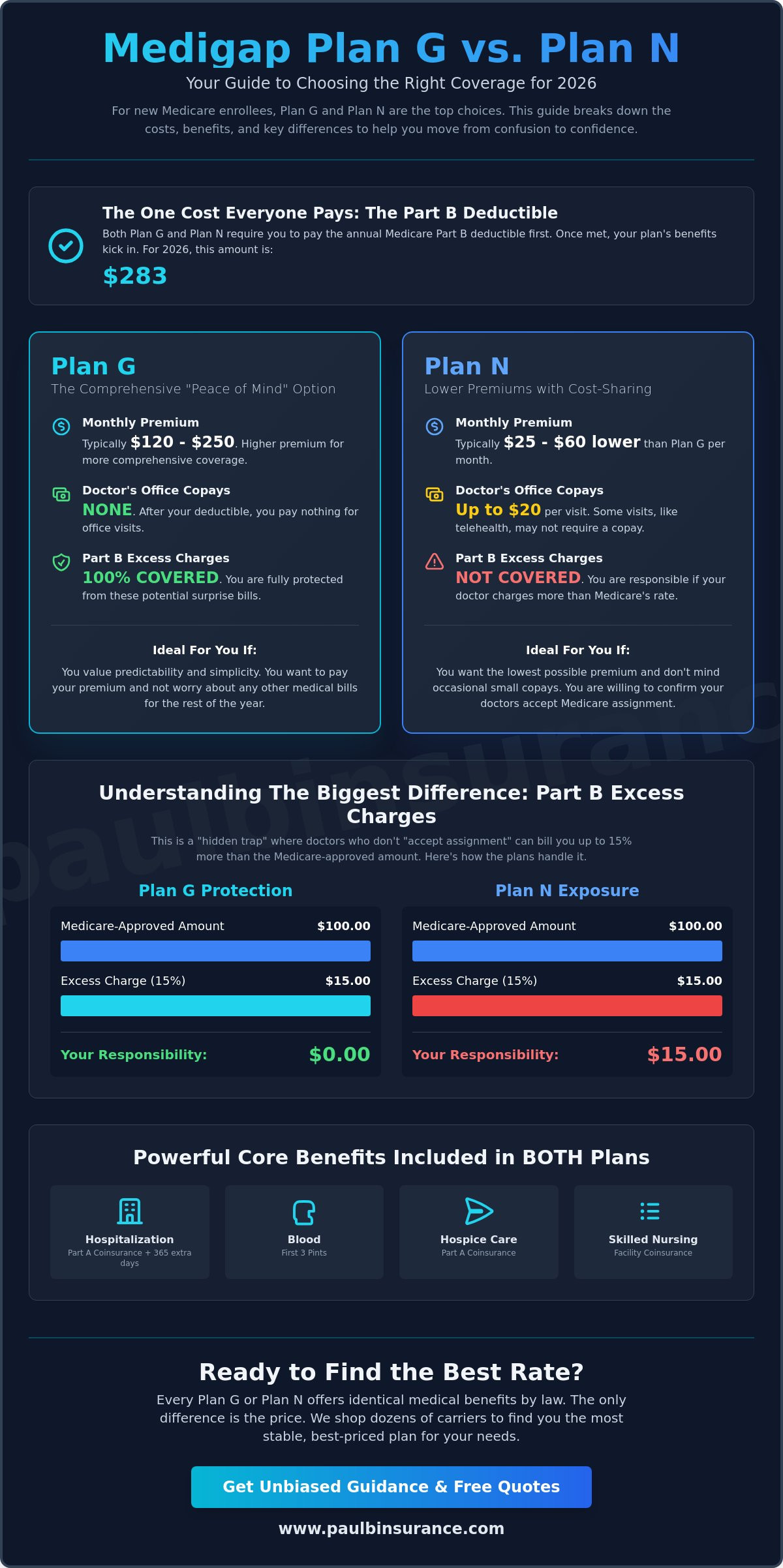

Both Plan G and Plan N provide a massive safety net for your finances. They both cover the following essential costs:

- Hospitalization: Part A coinsurance and hospital costs for an extra 365 days after Medicare benefits are exhausted.

- Blood: The first three pints of blood needed for a medical procedure.

- Hospice: Part A hospice care coinsurance or copayments.

- Skilled Nursing: Coinsurance for care in a skilled nursing facility, which is vital for recovery after a hospital stay.

Because they share these core benefits, the choice between medigap plan G vs plan N for new enrollees usually comes down to how you want to pay for your outpatient care and your comfort level with small copays.

Medigap Plan G: The Comprehensive “Peace of Mind” Option

Many of our clients call Plan G the “Cadillac” of Medicare Supplements, and it’s easy to see why. If you want a plan where you can walk into any doctor’s office in the country and never reach for your wallet, this is likely your winner. When comparing medigap plan G vs plan N for new enrollees, Plan G is the choice for those who value simplicity above all else. Once you pay your monthly premium, your financial responsibility for Medicare-approved services is almost entirely finished for the year.

The only major out-of-pocket cost you’ll face with Plan G is the annual Medicare Part B deductible. For 2026, the government has set this deductible at $283. Once you’ve paid that first $283 for the year, Plan G steps in to cover 100% of your remaining Medicare-approved medical bills. There are no copays for doctor visits and no surprise fees for physical therapy or specialist consultations. It’s a “one and done” approach to healthcare that removes the anxiety of opening your mailbox to find unexpected medical bills. You can see how this compares to other options on the Official Medicare Comparison Chart.

Understanding Part B Excess Charges

One of the biggest reasons we recommend Plan G is the protection it provides against “excess charges.” These happen when a doctor or provider doesn’t “accept assignment,” which means they don’t agree to Medicare’s pre-set payment rates. In these cases, the law allows them to charge you up to 15% more than the Medicare-approved amount. Excess charges are the hidden trap of Medicare. While they aren’t common in every state, they can be a nasty surprise if you see a specialist who doesn’t follow the standard fee schedule. Plan G acts as a total shield, paying that 15% upcharge so you don’t have to.

The Predictability Factor

If you’re managing a chronic condition or simply prefer a fixed budget, Plan G offers unmatched predictability for your 2026 expenses. You’ll know exactly what your healthcare will cost for the next twelve months: your monthly premium plus the $283 deductible. This level of certainty is why so many seniors choose Plan G over Plan N, even if the monthly premium is a bit higher. If you’d like to see how these numbers look for your specific area, you can learn more about our Medigap services and get a personalized quote. We want you to feel confident that your savings are protected, no matter what health challenges might come your way. If you have questions about your specific situation, feel free to reach out to our team for a friendly chat.

Medigap Plan N: Lower Premiums with a Focus on Cost-Sharing

If Plan G is the “Cadillac” of supplements, we like to think of Plan N as the “smart saver” option. It’s becoming a top choice in 2026 because it helps you keep more of your hard-earned money in your pocket every month. The trade-off is straightforward. You accept a lower monthly premium in exchange for a few small, predictable out-of-pocket costs. For many people comparing medigap plan G vs plan N for new enrollees, this plan offers the best value without leaving them exposed to massive hospital bills.

In 2026, Plan N premiums typically range from $80 to $200 per month. This is usually $25 to $60 lower than what you’d pay for Plan G. While you still have to meet the $283 Part B deductible, your monthly savings can really add up over the course of a year. If you’re a relatively healthy person who doesn’t need to see a specialist every other week, the math often leans heavily in favor of Plan N. It provides the same high-level hospital protection as Plan G but asks you to share a tiny bit of the cost for routine care.

The “Copay” Nuance

We often hear from clients who are worried that every little medical interaction will trigger a new bill. That isn’t how Plan N works. You only pay a copay of up to $20 for office visits that involve a doctor or specialist. If you’re just stopping by for lab work, a flu shot, or an X-ray, you won’t owe that $20. The same applies to telehealth. As virtual visits have become the standard in 2026, many of our clients find they rarely trigger a copay at all. If you only visit the doctor three or four times a year, your total copay cost might be less than $100, while your premium savings could be over $500.

The Excess Charge Risk on Plan N

The biggest difference to keep in mind is that Plan N does not cover Part B excess charges. As we discussed earlier, these are the 15% upcharges that happen when a doctor doesn’t accept Medicare’s standard payment rates. However, you can easily avoid these by asking your doctor if they “accept assignment” before your appointment. If you live in a state like New York, Ohio, or Pennsylvania, these charges are actually prohibited by law. You can see a full list of these “MOM” states and how they affect your choice at our Medigap information page. For most of our clients, this risk is very manageable and shouldn’t stand in the way of the significant savings Plan N provides.

How to Choose: A Practical Decision Framework for Your Lifestyle

Deciding between medigap plan G vs plan N for new enrollees isn’t a one-size-fits-all answer. We often tell our clients that the choice depends on their personal “hassle threshold.” Some people feel a spike of anxiety every time a $20 medical bill hits their kitchen table. Others are happy to manage those small costs if it means saving $500 or more on annual premiums. We ask you to consider how you feel about unpredictable expenses. If you want your healthcare costs to be as steady as a heartbeat, Plan G is your answer. If you’re comfortable with a little bit of back-and-forth in exchange for lower monthly costs, Plan N is a fantastic tool.

Your location in 2026 also plays a massive role in the medigap plan G vs plan N for new enrollees comparison. In some states, the price gap between these two plans is very narrow, making the move to Plan G an easy choice. In other areas, the savings on Plan N are so significant that it’s hard to ignore. We also encourage you to check with your specific specialists. While most doctors accept Medicare assignment, some highly sought-after specialists might not. If your preferred doctor is one of the few who bills for excess charges, Plan G will protect your savings from those 15% upcharges.

The Healthy New Enrollee Strategy

If you’re entering Medicare in 2026 with a clean bill of health, starting with Plan N can be a brilliant financial move. Over a decade, the lower premiums could save you thousands of dollars that stay in your retirement account. However, you must be aware of the “switching trap.” In most states, moving from Plan N to Plan G later requires you to answer health questions and go through medical underwriting. If your health changes down the road, you might not be able to switch. You can find more details on how these rules work on our Medigap guide page.

The “Total Protection” Strategy

We almost always recommend Plan G for clients who have upcoming surgeries or are managing chronic conditions like diabetes or heart disease. The value of “confidence” often outweighs “savings” when you’re navigating a complex health journey. A client we helped in early 2026 shared how glad they were to have Plan G after a series of specialist visits in a state that allows excess charges. They saved over $1,200 in upcharges that Plan N wouldn’t have covered. If you want to stop worrying about the “what ifs,” Plan G provides that total shield. If you’re ready to see which strategy fits your life best, schedule a call with us today.

Moving From Confusion to Confidence: How We Help You Decide

We know that making a final choice on medigap plan G vs plan N for new enrollees feels like a heavy weight. You aren’t just picking an insurance policy; you’re deciding how you want to experience your retirement years. Do you want the absolute certainty of Plan G, or the strategic savings of Plan N? We’ve helped thousands of people answer that question by acting as a committed advocate. Unlike a captive agent who only represents one insurance company, we are independent brokers. This means we work for you, not the big brands. We have the freedom to compare rates from 40+ different carriers to ensure you get the most stable pricing available in 2026.

Our goal is to protect you from the pressure and noise of the insurance system. We follow a simple 5-step process to move you from confusion to confidence. First, we listen to your specific health needs and budget. Second, we educate you on the jargon so you understand exactly what you’re buying. Third, we run a side-by-side comparison of the best plans in your zip code. Fourth, we handle the enrollment paperwork to avoid costly mistakes or late penalties. Finally, we provide ongoing support, checking your rates every year to make sure you’re still in the best spot. You’re never rushed and never pressured when you work with us.

Unbiased Guidance You Can Trust

The best part of our service is that it comes at no cost to you. We are paid by the insurance carriers, which allows us to provide professional, unbiased guidance for free. We simplify the complex rules so you know exactly how your coverage works before you ever sign a document. If you want to dive deeper into how this partnership works, you can read our guide on why you should work with a Medicare Broker. We believe everyone deserves an expert in their corner who is focused on their best interests, not a sales quota.

Ready to Take the Next Step?

Don’t let the crazy maze of the Medicare system keep you up at night. Whether you’re leaning toward Plan G for its total protection or Plan N for its monthly savings, we can provide the clarity you need. We’ll show you the 2026 rate filings for your area and help you assess your “hassle threshold” with total honesty. It’s time to stop feeling overwhelmed and start feeling protected. Reach out to us today to see how simple this process can be. You can Schedule a Call With Paul right now to get started on your path to peace of mind.

Secure Your Peace of Mind for 2026 and Beyond

Choosing between medigap plan G vs plan N for new enrollees is a personal decision that shapes your daily life. You’ve seen how Plan G offers a total shield against medical bills, while Plan N provides a strategic way to lower your monthly costs. Neither plan is “better” in a vacuum; the right choice is the one that lets you sleep soundly at night. We’re here to remove the anxiety from this process and replace it with clarity.

Our team represents over 40 top-rated carriers, allowing us to find the most stable rates for your specific needs. We offer unbiased guidance with no pressure, and we’re proud to serve clients in 34+ states across the country. You don’t have to navigate this crazy maze alone or worry about making a costly enrollment mistake. We simplify the jargon and stay by your side long after your policy begins.

Schedule a Call With Paul to Find Your Perfect Plan and let’s turn your confusion into confidence. You’ve earned a worry-free retirement, and we’re honored to help you protect it.

Frequently Asked Questions

Is Plan G better than Plan N for a new enrollee in 2026?

The best plan depends on your personal preference for fixed costs versus monthly savings. For many people comparing medigap plan G vs plan N for new enrollees, Plan G is the winner for those who want zero surprises after paying their deductible. Plan N is often better for healthy seniors who want to save $300 to $700 per year in premiums and don’t mind paying a few $20 copays.

Can I switch from Plan N to Plan G later without a medical exam?

In most states, you cannot switch from Plan N to Plan G without answering health questions. This process is called medical underwriting, and it means an insurance company can decline your application based on your medical history. It’s usually safer to start with the higher level of coverage if you think you might need it later, as your health could change and lock you into your current plan.

Do both Plan G and Plan N cover prescription drugs?

No, Medigap plans sold today do not cover retail prescription drugs. These plans are designed to focus strictly on your medical and hospital costs. To get coverage for your medications, you’ll need to enroll in a separate Medicare Part D plan. We can help you compare drug plans alongside your supplement to make sure all your needs are met under one simple strategy.

How much are the copays for Medigap Plan N in 2026?

Plan N copays are very specific and predictable. You’ll pay up to $20 for some office visits and up to $50 for emergency room visits that don’t result in you being admitted as an inpatient. You won’t pay these copays for lab work, flu shots, or other preventative services. This small bit of cost-sharing is why Plan N premiums stay so much lower than Plan G.

What is the Part B deductible I have to pay with these plans?

The Medicare Part B deductible for 2026 is $283. You must pay this amount out of pocket once per year before your Medigap plan begins to pay for outpatient services. Both Plan G and Plan N require you to meet this deductible yourself. Federal law prohibits any Medigap plan from covering this cost for anyone who became eligible for Medicare after January 1, 2020.

Are these Medigap plans accepted by any doctor who takes Medicare?

Yes, both plans offer you total freedom to choose your own providers. You can see any doctor or specialist in the country who accepts Medicare patients. There are no provider networks to navigate and you don’t need a referral to see a specialist. This flexibility is a huge relief for our clients who want to keep their trusted doctors or see specialists at top hospitals.

What happens if I choose Plan N and my doctor has an excess charge?

If your doctor doesn’t accept Medicare assignment, you’ll be responsible for the 15% upcharge known as an excess charge. While over 95% of doctors across the country accept the standard Medicare rates, some specialists do not. Choosing Plan N means you accept this risk yourself, while Plan G would pay that extra 15% for you automatically.

Is there a “High Deductible” version of Plan G available for new enrollees?

Yes, High-Deductible Plan G is available and can be a great budget-friendly option. It offers the exact same benefits as the standard Plan G, but only after you pay a much higher annual deductible first. We often suggest this for clients who are looking for catastrophic protection rather than help with their smaller, everyday medical bills.