The most expensive Medicare supplement plan isn’t always the one that offers you the most security. For many of our neighbors on Long Island, deciding between Plan G vs High deductible plan G which is better in Patchogue often comes down to a simple choice between paying now or paying later. You might feel overwhelmed by the rising 2026 premiums, but New York’s unique rules actually give you more control than you think.

We know how stressful it is to watch your monthly fixed costs climb while worrying about whether you can still see your favorite Long Island doctors. It’s frustrating to feel like you’re locked into a plan that might not fit your current budget. We’re here to help you find peace of mind by breaking down the 2026 deductibles and showing you how the math actually works for your specific situation. We’ll look at the $2,950 deductible for the high-deductible version compared to the standard Plan G premiums to see which path leads to the most certainty for your future.

Key Takeaways

- Understand the core differences between Plan G vs High deductible plan G which is better in Patchogue based on your personal health needs and monthly budget for 2026.

- Learn why New York’s unique rules mean you’re never stuck in a plan and can change your coverage whenever your needs change.

- Discover the exact break-even point to see if saving on monthly premiums outweighs the 2026 high deductible of $2,950.

- Find out how both versions of Plan G protect you from unexpected bills at local facilities like NYU Langone Suffolk.

- See how we simplify the process by comparing dozens of carriers to find the most competitive rates for the 11772 ZIP code.

The Patchogue Medicare Crossroads: Understanding Your Plan G Options in 2026

Living in Patchogue means enjoying the best of Long Island, whether you’re grabbing coffee on Main Street or watching the ferries from Mascot Dock. But as we move through 2026, many of our neighbors are facing a stressful decision at the local Medicare crossroads. With healthcare costs shifting, the question of Plan G vs High deductible plan G which is better in Patchogue has become a daily conversation. We see the worry in your eyes when those premium notices arrive. It’s a choice between the comfort of a plan that covers almost everything and a version that asks you to take on a bit more risk for a much lower monthly bill.

We view this choice as a journey. It’s about moving from a state of confusion to one of financial certainty. Plan G has become the “Gold Standard” for New York seniors, especially since Plan F closed to new enrollees years ago. It offers a clear path to protecting your savings, but the version you choose depends entirely on your personal comfort level with “what-if” scenarios. We’re here to walk you through the math so you can feel empowered rather than pressured.

What exactly is Medicare Supplement Plan G?

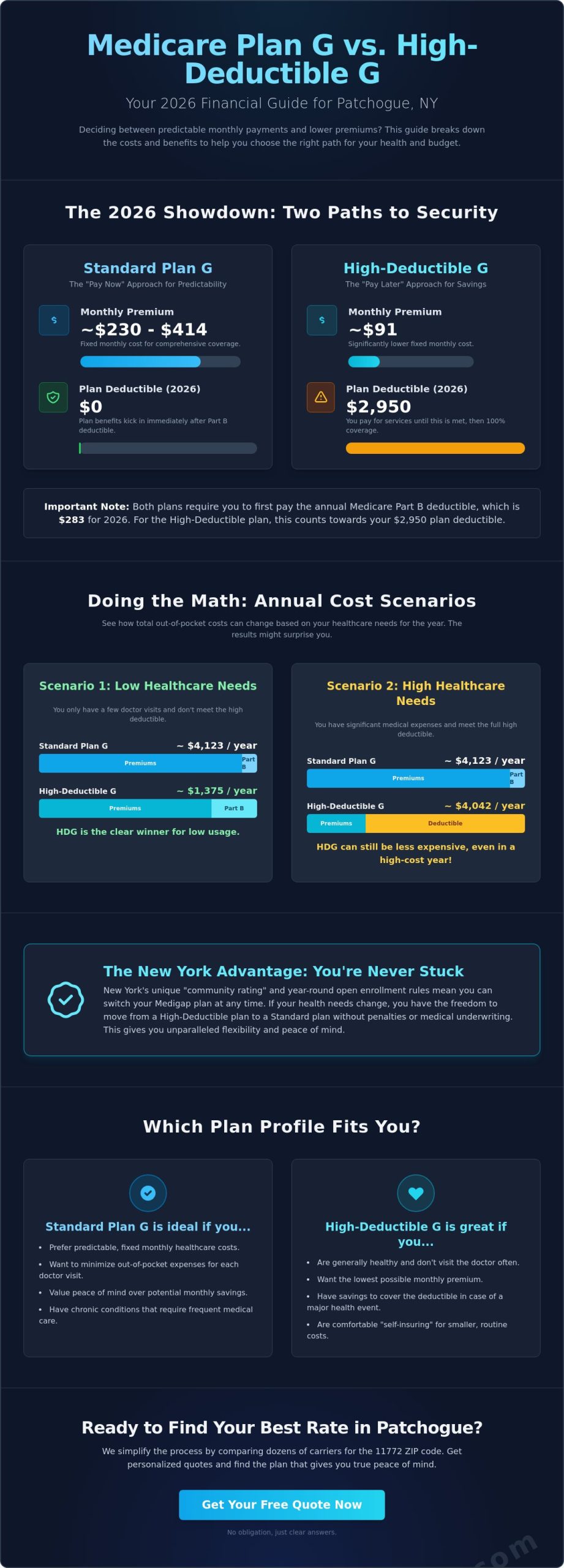

Plan G is designed to pick up where Original Medicare leaves off. It covers almost every gap, including the 20% coinsurance that can otherwise lead to massive bills. Understanding Medigap is much simpler when you realize that all Medigap plans are standardized by the government. This means the benefits are identical regardless of which insurance company you choose. In 2026, Plan G remains the most comprehensive option available. The only thing you’ll need to pay out of pocket for covered services is the Part B deductible, which is $283 this year.

The “High Deductible” Twist Explained

The high-deductible version of Plan G (HDG) provides the exact same coverage but changes your cost structure. Instead of paying a high premium every month, you agree to pay your own medical bills until you reach the 2026 deductible of $2,950. Once you hit that limit, the plan pays 100% of your covered costs. We like to think of this as “self-insuring” the small stuff. If you’re generally healthy, paying a lower monthly premium of around $91 can save you thousands over the year, even if you have a few doctor visits. It’s a strategic way to keep more of your hard-earned money in your pocket while still having a safety net for major health events.

Standard Plan G vs. High Deductible Plan G: The 2026 Comparison

Choosing between these two options often feels like a high-stakes guessing game. We want to remove that pressure by showing you that the core benefits are actually identical. Both plans cover your Part A hospital coinsurance, skilled nursing facility care, and even foreign travel emergency care. The only real difference is how you choose to pay for that security. When we look at Plan G vs High deductible plan G which is better in Patchogue, we aren’t comparing the quality of care. We’re comparing your cash flow strategy.

Both versions of Plan G require you to pay the 2026 Part B deductible of $283 for outpatient services. After that small hurdle, the standard Plan G starts paying immediately. The High Deductible Plan G (HDG) requires you to meet a $2,950 deductible before it takes over the remaining costs. While that larger number can feel intimidating, it’s often the best-kept secret for New York seniors who want to maintain access to any doctor in the country without paying for coverage they might not fully use every month.

Side-by-Side: Benefits and Costs

To help you see the landscape clearly, we’ve outlined the 2026 costs for Suffolk County below. Remember that both plans allow you to visit any specialist who accepts Medicare, whether they’re right here in Patchogue or across the country. You can also find more details in the official Medicare guide to choosing a Medigap policy to see how these standardized plans compare.

| Feature | Standard Plan G | High Deductible Plan G |

|---|---|---|

| Monthly Premium (Suffolk) | ~$230 – $414 | ~$91 |

| Plan Deductible (2026) | $0 | $2,950 |

| Part B Deductible (2026) | $283 | $283 |

| Access to Doctors | Any Medicare Provider | Any Medicare Provider |

The Premium Savings Math

The math is where the “hidden” value of the high-deductible plan really shines. In 2026, the lowest-cost standard Plan G in our area is about $230 per month. The high-deductible version is roughly $91. That is a monthly savings of $139, or $1,668 per year. If you choose the high-deductible path, those savings act as your own personal reserve fund. If you have a healthy year, that money stays in your pocket. Even if you have a difficult health year and meet the full $2,950 deductible, your total out-of-pocket cost might only be slightly higher than if you had paid the expensive monthly premiums all year long. We help our neighbors run these specific numbers every day so they can view our local Medigap options with complete confidence.

Why New York’s Unique Rules Make This Choice Easier in Patchogue

One of the biggest fears we hear from Patchogue seniors is the fear of being “locked in.” You might worry that if you choose the High Deductible Plan G today to save money, you’ll be stuck with it forever even if your health takes a turn. In most other states, that fear is a reality. But here in New York, the rules are written to protect you. These local protections change the entire conversation around Plan G vs High deductible plan G which is better in Patchogue because they remove the permanent risk from your decision. We want you to feel empowered to choose the plan that fits your current budget without worrying about the future.

Continuous Open Enrollment Explained

New York is one of the few states that offers continuous open enrollment. This means you have the right to switch your Medigap plan at any time during the year. You don’t have to wait for a specific window or a life-changing event to make a move. Most importantly, there is no medical underwriting in our state. In other parts of the country, an insurance company could look at your health history and deny your application or charge you more if you have a pre-existing condition. In Patchogue, that simply doesn’t happen. You can start with a lower premium plan while you’re healthy and move to a more comprehensive plan later if you need it. For a deeper look at these state-specific protections, you can read more about Medicare Supplement Insurance on our site.

Community Rating: Fairness for All Patchogue Residents

Another reason your choice is simpler here is a rule called “community rating.” In states like Florida or Arizona, premiums often go up just because you’ve had another birthday. This can make plans unaffordable as you age into your 70s and 80s. New York requires insurance companies to charge everyone in our area the same rate, regardless of their age or health status. Whether you are 65 or 85, you pay the same premium for the same plan. This rule provides a massive amount of long-term certainty. It ensures that your rates stay predictable and that you won’t be penalized for simply growing older in the community you love. When you combine this with the fact that New York doctors aren’t allowed to bill for Part B excess charges, you have a level of security that seniors in most other states can only dream of. These local protections are the secret to deciding Plan G vs High deductible plan G which is better in Patchogue for your specific lifestyle. We help you navigate these rules so you can make a choice based on your budget today, knowing you’re protected for whatever tomorrow brings.

Doing the Math: Which Plan Saves You More at NYU Langone Suffolk?

Numbers on a page can feel cold and confusing, but when we apply them to your life here in Patchogue, they start to tell a clear story. We want to help you see exactly how your bank account might look at the end of 2026. Whether you are visiting a specialist near Main Street or facing a more serious stay at NYU Langone Suffolk, the choice between Plan G vs High deductible plan G which is better in Patchogue often comes down to your personal “break-even” point. This is the moment where the monthly savings of one plan either outweigh or fall short of the out-of-pocket costs of the other.

We look at this as a balance between a guaranteed monthly expense and a potential one. Some of our neighbors prefer the peace of mind that comes with a higher monthly bill because it means they’ll almost never see another medical invoice. Others find that “self-insuring” with a high-deductible plan allows them to keep more of their pension or Social Security income for daily living. Let’s look at how these two scenarios play out with the 2026 rates.

The Healthy Year Scenario

A “Healthy Year” is one where your only major medical expense is the 2026 Part B deductible of $283 for your routine doctor visits and tests.

- Standard Plan G: You’ll pay roughly $2,760 in annual premiums plus the $283 deductible, totaling $3,043.

- High Deductible Plan G: You’ll pay roughly $1,092 in annual premiums plus the $283 deductible, totaling $1,375.

In this scenario, choosing the high-deductible version keeps an extra $1,668 in your pocket. That is money you can use for travel, family, or simply as an emergency fund.

The Major Medical Event Scenario

If 2026 brings an unexpected surgery or a stay at a facility like NYU Langone Suffolk, the math shifts. With the high-deductible plan, you are responsible for the first $2,950 of your covered costs. When you add that deductible to your annual premiums, your total yearly spend would be approximately $4,042. Compared to the $3,043 you would spend on a standard Plan G, the “worst-case” year costs you about $1,000 more. For many seniors, the “known cost” of the standard plan is worth it to avoid that $1,000 surprise. However, if you have three healthy years for every one difficult year, the high-deductible plan still saves you more in the long run. We invite you to compare 2026 Medigap rates with us to see which math makes you feel the most secure.

Choosing Your Path: How We Help You Find Peace of Mind

Deciding on Plan G vs High deductible plan G which is better in Patchogue is a significant step toward your future security. We understand that this choice isn’t just about spreadsheets and deductibles. It’s about your peace of mind. You deserve to know that you’ve made the right decision for your health and your wallet as you move through 2026. We’re here to act as your personal guide, removing the noise and pressure from the process so you can focus on what matters most. Our goal is to take you from a state of uncertainty to a place of total confidence in your coverage.

The 2026 Medicare landscape can feel like a maze, but you don’t have to walk it alone. We view our role as your advocate and educator. We’ve spent years learning the local rules so you don’t have to. Whether you’re worried about the $2,950 deductible of the high-deductible plan or the rising monthly premiums of the standard version, we provide the clarity you need to choose the path that fits your life on Long Island.

The Value of an Independent Expert

When you speak with a “captive” agent who only works for one insurance company, you only hear one side of the story. They’re restricted to selling only what their brand offers, which limits your choices. We take a different approach. As independent brokers, we work for you, not the insurance companies. We compare over 40 different carriers specifically for the 11772 ZIP code to find the most competitive rates available today. Because New York uses community rating, we focus on which companies have a history of stable pricing and reliable service. We monitor rate increases across the state to ensure you aren’t surprised by a sudden jump in your monthly bill. We’d love to sit down for a coffee right here in Patchogue or have a simple phone call to hear your story and answer your questions without any high-pressure tactics.

Ready to Compare Plans?

If you’re turning 65 in 2026 or thinking about switching your current coverage, the next step is simple. We can provide a personalized quote that shows you the exact premium savings for a Medigap plan in our local area. Our support doesn’t end once your application is submitted. We remain your advocate year-round. If you get a bill that doesn’t look right or have a question about how your Medicare Part D plan interacts with your supplement, we’re just a phone call away. We’re committed to protecting you from the confusion of the system. Let’s work together to find the path that gives you the most certainty for the years ahead. We’re ready to help you simplify this process and protect your financial future.

Securing Your Health and Your Savings in 2026

Choosing the right path for your healthcare is a deeply personal journey. We’ve seen how the 2026 rules in New York offer you a unique safety net that seniors in other states don’t have. Whether you choose the standard Plan G for its predictable costs or the high-deductible version for its monthly savings, you aren’t making a permanent decision. You can change your mind later without health questions. This flexibility is your greatest advantage as a New York resident.

Deciding on Plan G vs High deductible plan G which is better in Patchogue depends on your comfort with monthly bills versus occasional deductibles. We are here to make that math clear and simple. As your local independent broker, we compare over 40 carriers to find the best fit for your budget. Our expertise is focused right here in Patchogue, providing you with no-cost, unbiased Medicare guidance that puts your needs first. We want to remove the stress and replace it with the certainty that you have the right coverage.

Let us help you find the perfect Medicare fit in Patchogue—Get your 2026 quote today!

You deserve to enjoy your retirement with total peace of mind. We’re ready to help you take the next step toward a stress-free and secure 2026.

Frequently Asked Questions

Is High Deductible Plan G the same as Plan G?

Yes, the medical benefits for both plans are identical. Both versions cover the same services, such as hospital stays, skilled nursing, and doctor visits. The only difference is the cost structure. With the standard version, you pay a higher monthly premium for immediate coverage. With the high-deductible version, you pay a much lower premium but agree to pay for your own care until you reach a set limit.

What is the High Deductible Plan G deductible for 2026?

The deductible for High Deductible Plan G in 2026 is $2,950. You must pay this amount for covered services before the plan begins to pay its share. It’s important to remember that this is separate from the $283 Part B deductible. Once you meet the $2,950 limit, your plan functions exactly like the standard Plan G for the rest of the calendar year.

Can I switch from High Deductible Plan G to Standard Plan G later in New York?

Yes, you can switch at any time because New York has continuous open enrollment. This is a huge relief for local seniors. You don’t have to worry about medical questions or being denied coverage due to your health history. This flexibility makes deciding Plan G vs High deductible plan G which is better in Patchogue much less stressful because you aren’t locked into your choice forever.

Do Patchogue doctors accept High Deductible Plan G?

Yes, any doctor who accepts Medicare also accepts both versions of Plan G. Your doctor doesn’t actually see which version you have; they simply bill Medicare and your supplement company. This means you can keep your favorite specialists at NYU Langone Suffolk or any other local practice without any interruption in your care. We ensure our clients feel confident that their access to local doctors remains secure.

Does Plan G cover prescription drugs (Part D)?

No, Plan G does not include prescription drug coverage. Medicare rules require you to purchase a separate Part D plan to help with the cost of your medications. We help our neighbors find a Part D plan that fits their specific prescriptions so they have complete coverage. Combining Plan G with a solid Part D plan is the best way to ensure you don’t face unexpected bills at the pharmacy.

How much can I save in premiums with the High Deductible version in Suffolk County?

You can save approximately $139 per month by choosing the high-deductible version in Suffolk County. Over the course of 2026, those savings add up to roughly $1,668. For many healthy seniors, this extra cash flow provides a significant sense of financial freedom. We help you look at these savings to see if they provide a large enough “cushion” to cover the deductible if you need it.

What happens if I cannot meet the deductible in a bad health year?

If you have high medical costs and struggle to meet the deductible, the plan will not pay for your share of the bills until the $2,950 limit is reached. However, because of New York’s unique rules, we can help you switch to a standard Plan G to lower your out-of-pocket risk for the future. We always suggest keeping your premium savings in a dedicated account to help cover the deductible during a difficult health year.

Is there a “waiting period” for pre-existing conditions when switching in New York?

No, there is typically no waiting period for pre-existing conditions when you switch Medigap plans in New York. Since our state is a “guaranteed-issue” state, you are protected from being penalized for your health history. This is one of the many reasons why deciding Plan G vs High deductible plan G which is better in Patchogue is a journey we can navigate together with total confidence and peace of mind.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com