The cheapest monthly premium you see in your mailbox today might actually be the most expensive choice you make for your retirement. With some Plan G rates jumping by over 20 percent in early 2026, identifying the best medicare supplement plan companies is no longer just about finding the lowest starting price. We understand how stressful it feels to open those glossy envelopes and worry if your fixed income can keep up with these spikes. You deserve a plan that offers more than just a low introductory rate. You need a carrier that values your financial security as much as you do.

We agree that the system feels designed to confuse you, especially when companies offer the exact same standardized benefits but charge wildly different prices. Our goal is to replace that anxiety with a clear, step-by-step path to certainty. We will help you cut through the noise to find the most stable, cost-effective carriers for your 2026 coverage. In this review, we’ll break down which companies have maintained the best rate stability and explain how to secure benefits like household discounts. We will compare the financial strength of top-tier brands to ensure your coverage remains reliable for the long haul.

Key Takeaways

- Learn why identical benefits don’t mean identical costs. We explain how to look past the marketing to find true rate stability for your 2026 coverage.

- Discover our expert criteria for ranking the best medicare supplement plan companies, including why we prioritize A+ financial ratings to protect your peace of mind.

- Get an inside look at how top-rated 2026 carriers like AARP/UnitedHealthcare and Humana compare so you can choose the right fit for your health needs.

- Find out how to secure a household discount to lower your monthly premiums, even if your spouse is not enrolled in the same plan.

- Understand how an independent advocate uses proprietary data to shield you from the sharp rate increases hitting the market this year.

Why the Carrier Matters: Standardized Plans vs. Company Stability

Choosing a plan often feels like walking through a maze of identical doors. You see Plan G offered by twenty different names, yet the prices are all over the map. We want to help you understand why this happens. Federal law requires that Medigap (Medicare Supplement Insurance) plans be standardized. This means a Plan G from a small, new company covers your hospital stays and doctor visits exactly the same way a Plan G from a household name does.

If the benefits are the same, why does the carrier matter? The insurance company is responsible for three main things: processing your claims, providing customer service, and setting your monthly premium. While the medical coverage is identical, your experience as a policyholder is not. Some of the best medicare supplement plan companies have refined their systems over decades to ensure claims are paid instantly without you ever seeing a bill. Others might have slower systems or less helpful staff. This adds unnecessary stress to your life when you should be focusing on your health.

One of the biggest risks we see is something called a “closed block” of business. Sometimes, a company will stop selling a specific version of a plan to new members. When no healthy, younger people are joining that group, the costs for everyone left inside start to climb rapidly. We help you avoid these traps by looking for carriers committed to long-term stability rather than short-term gains. We want to ensure you don’t get stuck in a plan that becomes unaffordable just when you need it most.

The 2026 Medigap Landscape

In 2026, Medigap remains the gold standard for anyone who wants to avoid surprise medical bills. With the Part B deductible rising to $283 this year, having a plan that picks up those costs after you meet your deductible is vital. New regulations in 2026 have increased transparency, but they’ve also led to more competition. You can learn more about these basics in our guide on What Is Medicare Supplement Insurance? to see how these pieces fit together. We believe that clarity is the first step toward peace of mind.

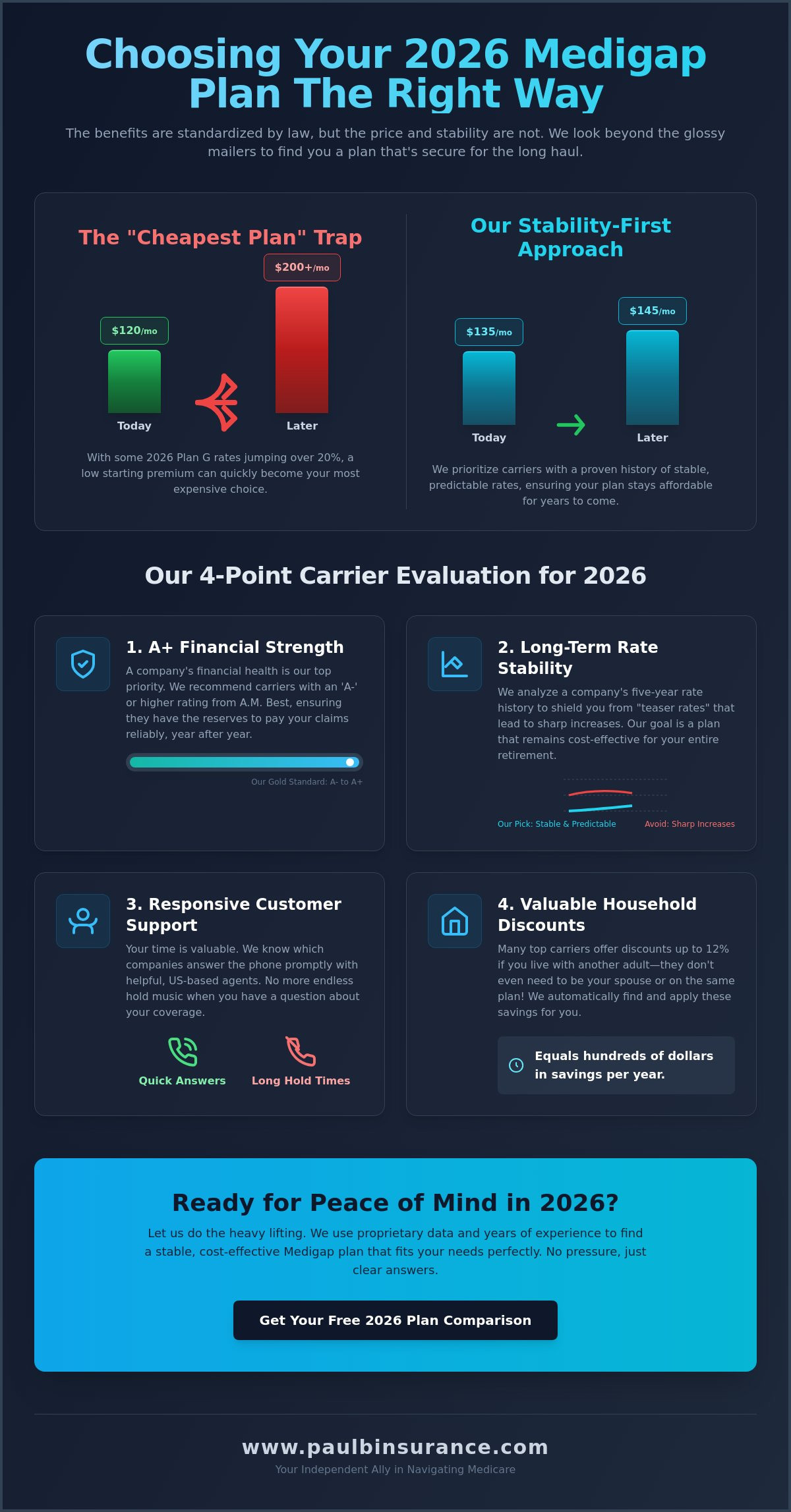

The Myth of the “Cheapest” Plan

It’s tempting to pick the plan with the lowest price on day one. However, the cheapest plan today is often the one with the highest rate increases later. We always advise our clients to look at a company’s five-year history of rate changes before signing up. Standardized plans mean the medical benefits stay the same across every carrier, leaving price and customer service as the only true differences between the best medicare supplement plan companies. By focusing on long-term stability, we help you secure a plan that stays cost-effective for years to come.

How We Evaluate the Best Medicare Supplement Companies

Finding the right coverage in 2026 shouldn’t feel like a gamble. We analyze the best medicare supplement plan companies using a strict set of criteria that goes far beyond the monthly price tag. While the official Medicare website explains the basic benefits of each plan letter, it doesn’t tell you which company might double your rates in two years. We do.

We look at financial strength first. An A+ rating from A.M. Best is our gold standard for the best medicare supplement plan companies. It tells us a company has the cash reserves to pay claims even during difficult economic years. We also look at market share. New companies often enter the market with “teaser rates” to attract seniors. Once they’ve gathered enough people, they frequently hit them with double-digit increases. We prefer carriers with decades of experience who have seen it all before.

Your time is valuable. We track how long it takes for a real person to answer the phone at these companies. If you have a question about your $283 Part B deductible, you shouldn’t be on hold for an hour. Finally, we factor in household discounts. These can save you up to 12 percent, making a slightly more expensive plan the better deal in the end. Our team can help you compare these hidden factors to find the best value for your specific needs.

A.M. Best and Weiss Ratings Explained

These grades are like a report card for an insurance company’s wallet. We rarely suggest any carrier with a rating below an “A-“. If a company’s rating slips, it’s often a sign of financial instability. This can lead to a “death spiral” where the company stops paying claims efficiently or raises rates so high that healthy people leave the plan. This leaves only the sickest people in the pool, causing rates to skyrocket even faster.

The Importance of Rate Stability History

The high-inflation years leading into 2026 have tested every carrier in the country. We track how each company behaved during this time. Did they keep increases modest, or did they pass every penny of inflation onto you? We also look at their pricing models. An “attained age” plan gets more expensive simply because you’re getting older. An “issue age” plan is based on how old you were when you bought it. We track these histories across all 40+ carriers we represent to ensure you’re making a sustainable choice.

Top-Rated Medicare Supplement Carriers for 2026

We know that looking at a list of names like Humana, Aetna, or Mutual of Omaha can feel overwhelming. How do you know which one will actually be there for you when a medical bill arrives? In our search for the best medicare supplement plan companies, we prioritize carriers that have shown they can handle the rising costs of healthcare in 2026 while keeping your premiums as steady as possible. We look for a history of reliability so you don’t have to worry about a sudden rate spike forcing you to change plans when you’re older.

Aetna and CVS Health have become strong contenders this year by offering very competitive pricing and some of the best digital tools in the industry. Their 2026 portal makes it simple to see how your claims are being paid against the $283 Part B deductible. While digital tools are nice, we also value the “Mutual” structure of Mutual of Omaha. Because they’re owned by their policyholders rather than stockholders, they often prioritize long-term stability over quarterly profits. This is why they remain a favorite for our clients who choose Plan G.

Humana Medicare Supplement Plans: A 2026 Deep Dive

Humana has shown a deep commitment to the Medigap market this year. We’ve noticed they’re focusing heavily on Plan G and Plan N, offering a balance of value and comprehensive coverage. One major pro of Humana is how well they integrate with other senior services, making the transition into Medicare feel much smoother. However, it’s always wise to check an expert review of Medicare supplement plans to see how their rate increases in your specific state compare to the national average. They’re an excellent choice for those who want a modern, responsive insurance experience.

AARP/UnitedHealthcare: The Industry Giant

UnitedHealthcare, through its partnership with AARP, remains the largest player in the Medicare space. They often use a “Community Pricing” model. In many states, this means everyone in the same area pays the same rate regardless of their age. This massive membership base acts as a buffer, helping to keep rate increases more predictable than smaller, newer carriers. You can read more about whether AARP Medicare Supplement Plans: Are They Worth It? in our detailed breakdown of their 2026 offerings. Their size provides a sense of security that many of our clients find deeply reassuring.

We compare all these brands side-by-side for you to ensure you’re getting the most stable coverage available. Whether you’re looking at regional favorites like Blue Cross Blue Shield or national leaders like Cigna, we help you find the best medicare supplement plan companies for your unique health and budget needs. Our mission is to move you from a state of confusion to a state of absolute certainty about your future.

Choosing the Right Carrier for Your Specific Needs

Finding the best medicare supplement plan companies for your neighbor might not mean finding the best one for you. We believe your choice should depend on your unique health habits and living situation. To help you move from a state of uncertainty to a clear decision, we suggest following a simple four-step process. This method removes the guesswork and ensures you aren’t overpaying for coverage you don’t need.

- Step 1: Decide if you want the absolute lowest price today or a company with a proven record of small, steady increases. We often find that paying a few dollars more now saves you much more in the long run.

- Step 2: Always check for household discounts. This is a major factor that most automated price tools miss.

- Step 3: Pick the right plan letter. We help you evaluate Plan N versus Plan G based on how often you actually visit your doctor.

- Step 4: Verify the company’s local reputation. A carrier that is excellent in one state might have higher rate increases in another due to local regulations.

The Power of the Household Discount

A household discount is often the deciding factor in which company is actually the most affordable for you. These discounts typically range from 5 percent to 12 percent of your monthly premium. Many people don’t realize that some of the best medicare supplement plan companies offer this even if your spouse isn’t on the same plan. In fact, some carriers only require that you’ve lived with another adult for the past year to qualify. We use these discounts to save our clients hundreds of dollars annually by looking at the “real” cost after all savings are applied. We invite you to reach out to us to see which of these hidden discounts apply to your household.

Plan N: The “Secret” to Lower Premiums in 2026

Plan N is becoming the preferred choice for healthy seniors who want to lower their fixed costs. It usually offers much lower premiums than Plan G. In exchange for those savings, you agree to pay a small copay of up to $20 for some office visits and up to $50 for emergency room trips. If you don’t visit the doctor every month, the annual savings on your premiums can be significant. When we compare carrier-specific Plan N rates, we often find they are the most stable options in a company’s portfolio. You can explore the specific benefits of this plan on our Medicare Supplement (Medigap) Insurance page. We want to ensure you feel empowered to choose the plan that fits your lifestyle perfectly.

Why an Independent Broker is Your Best 2026 Ally

The flood of mailers and phone calls you receive in 2026 can make anyone feel overwhelmed. You might speak to a “captive agent” who works for just one insurance company. While these agents are often helpful, their options are limited. They can only offer you the plans their specific employer sells. We take a different approach. As an independent agency, we don’t work for the insurance companies. We work for you. This independence allows us to scan the entire market to find the best medicare supplement plan companies without any bias toward a single brand name.

Our team uses proprietary software to track rate increase histories across all 34+ states where we are active. We don’t just look at the price you’ll pay today. We look at what people in your zip code were paying three, five, and ten years ago. This data helps us predict which carriers are likely to keep your costs stable as you age. We believe that true peace of mind comes from knowing your future is protected by data, not just a salesperson’s promise. We help you avoid the “teaser rates” that lead to double-digit spikes later on.

Our commitment to you doesn’t end when your policy starts. We provide year-round support to help with billing questions or to review your plan if your local market changes. Best of all, our services are 100 percent free to you. We are compensated by the carriers themselves, so you get expert guidance without adding another expense to your budget. We are here to serve as your dedicated advocate and protector in a complex system.

The Modern Medicare Agency Difference

Paul Barrett and our team provide an unbiased, empathetic perspective that puts your needs first. We use a “Simplicity First” approach to explain everything in plain English. We strip away the confusing insurance jargon so you can make a decision with total confidence. You can explore more about how we help you find the right fit on our Medicare Supplement (Medigap) Insurance page. We are committed to being the champion you deserve in the 2026 market.

Your Journey to Peace of Mind Starts Here

Your first consultation with us is a calm, low-pressure conversation about your health goals. We listen first, then we use our tools to identify the best medicare supplement plan companies for your specific situation. We help you move from a state of distress to one of absolute certainty. When you are ready to stop the confusion and start your journey toward a secure retirement, we are ready to help. We invite you to schedule a simple, stress-free consultation with our team today.

Secure Your Financial Peace of Mind for 2026

Choosing your healthcare coverage is one of the most important decisions you will make this year. We have shown that while benefits are standardized by law, the company you choose determines your long-term costs and your daily peace of mind. By focusing on financial strength and rate stability history, you can protect yourself from the sharp premium increases we are seeing across the market. Remember that hidden savings like household discounts can turn a premium brand into your most cost-effective option.

Finding the best medicare supplement plan companies is much easier when you have a dedicated advocate by your side. Paul Barrett and our expert team provide unbiased advice to clients in over 34 states. We represent more than 40 top-rated insurance carriers to ensure you get a plan that fits your specific needs and budget. You don’t have to navigate these complex systems alone; we are here to simplify the process and remove the anxiety from your journey. Let us help you compare 40+ carriers to find your perfect match. We look forward to helping you move from a state of uncertainty to one of absolute confidence.

Frequently Asked Questions

Which Medicare Supplement company is the best for Plan G in 2026?

The best company for Plan G depends heavily on your specific zip code and age. While AARP/UnitedHealthcare and Mutual of Omaha are often top choices due to their size, the “best” carrier for you is the one that combines a competitive price with a history of low rate increases in your state. We look at the actual data for your area to ensure you aren’t just getting a low price today that will skyrocket tomorrow.

Do all Medigap companies cover the same things?

Yes, every company must offer the exact same medical benefits for a specific plan letter like Plan G or Plan N. A Plan G from any carrier will cover your Part B coinsurance and the $1,736 Part A hospital deductible in the same way. The only differences you will find between companies are the monthly premium price, the availability of household discounts, and the quality of their customer service.

What is the most stable Medicare Supplement company?

Stability usually comes from companies with the largest membership pools, such as AARP/UnitedHealthcare. Because these giants have millions of members, the medical claims of a few people don’t force everyone’s rates to jump significantly. We prioritize carriers with A+ financial ratings because they have the reserves to pay claims while keeping your monthly costs as predictable as possible over many years.

Can I switch my Medicare Supplement company at any time?

You have the right to apply for a new company at any time during the year. However, in most states, you’ll need to answer health questions to qualify for a new policy if you are outside of your initial enrollment period. We can help you determine if you live in a state with special rules that allow you to switch to one of the best medicare supplement plan companies without a medical exam.

Which company has the best household discount for Medigap?

Mutual of Omaha and several regional carriers currently offer some of the most generous household discounts, often reaching 12 percent. Some companies are very flexible and only require that you have lived with another adult for the past year to qualify. These discounts are a powerful way to lower your “real” cost, and we always check them first when comparing plans for couples or roommates.

Is AARP UnitedHealthcare better than Mutual of Omaha?

Neither company is objectively better for every person. AARP/UnitedHealthcare often uses community pricing models that can be very stable as you age, while Mutual of Omaha is a “mutual” company owned by its policyholders. We compare both side-by-side because one might have a much better rate history in your specific county than the other. Your choice should be based on local data rather than national brand names.

How much do Medicare Supplement premiums increase each year?

In 2026, many seniors are seeing average premium increases between 10 percent and 15 percent. Some companies have even issued spikes of over 20 percent to keep up with the rising costs of medical care. This trend makes it vital to choose a carrier that has a reputation for modest, steady adjustments rather than one that uses a “teaser” rate to get you in the door.

Why should I use an independent broker instead of buying directly from a company?

An independent broker works for you rather than a single insurance company. We have the tools to compare the best medicare supplement plan companies across the entire market, giving you an unbiased view of every option. We track the rate increase histories that companies don’t advertise, and our support continues long after your plan is active to ensure you always have the best value available.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com