Imagine standing at the pharmacy counter, waiting for the pharmacist to read your total, and feeling that familiar knot in your stomach. You might be wondering if this is the month a “tier change” or a “formulary update” sends your bill skyrocketing. Finding a medicare plan that covers my prescriptions shouldn’t feel like a high-stakes gamble with your health and savings. We understand that the fear of a surprise $500 bill is enough to keep anyone awake at night.

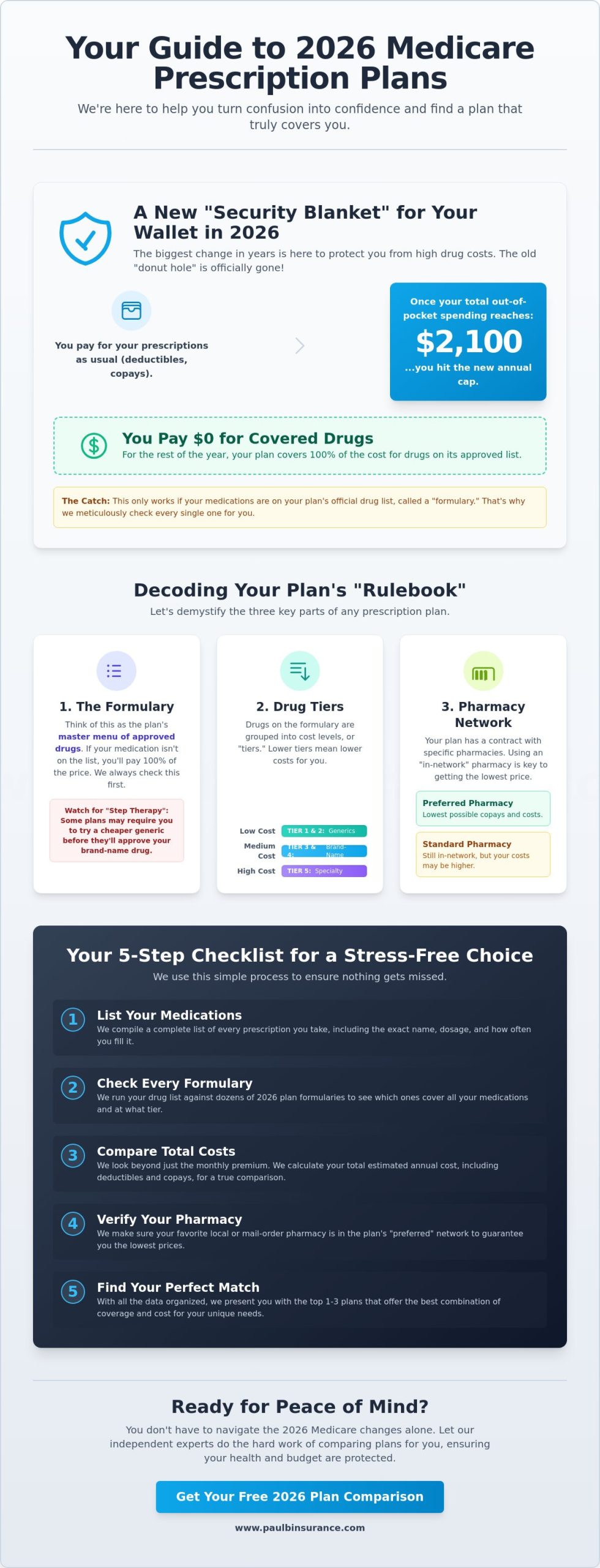

You’ve likely heard that things are different this year, and you’re right. With the coverage gap, or “donut hole,” officially eliminated and a new $2,100 out-of-pocket cap in place, 2026 offers more protection than ever before. However, more rules often mean more confusion. We’re here to help you turn that uncertainty into a clear, predictable plan. We show you exactly how to evaluate 2026 Medicare options to ensure every one of your medications is covered at the lowest possible cost.

In this guide, we’ll explain the new federal spending caps, show you how to use the Medicare Prescription Payment Plan, and provide a simple checklist to compare Medicare Advantage and Part D options. By the time you finish reading, you’ll have the peace of mind that comes from knowing your budget is safe and your health is protected.

Key Takeaways

- Understand how “formularies” work like a master menu to decide which medications are covered and how much you’ll pay at the register.

- Compare the “all-in-one” approach of Medicare Advantage with the “a la carte” style of Original Medicare to see which path fits your lifestyle best.

- Use our 5-step checklist to organize your medications so finding a medicare plan that covers my prescriptions becomes a simple, stress-free process.

- Find out why your choice of pharmacy is just as important as the plan itself when it comes to keeping your monthly costs predictable and low.

- Learn how an independent expert helps you filter through dozens of carriers to find the specific plan that prioritizes your health and your budget.

Why Finding a Medicare Plan That Covers Your Prescriptions is Different in 2026

We know the feeling of staring at a stack of insurance mailers and feeling your blood pressure rise. Looking at a list of forty or more different plans feels like a full-time job you never applied for. It’s exhausting, and the fear of making a wrong choice that costs you thousands of dollars is very real. But 2026 is a milestone year. Finding a medicare plan that covers my prescriptions is no longer just about navigating the confusing “donut hole,” because that coverage gap is finally gone. Instead, we’re looking at a brand-new landscape designed to offer you more security.

The rules have changed significantly this year. If you’ve been on the same plan for a long time, the “set it and forget it” strategy has become dangerous. Plans are adjusting their costs and drug lists to keep up with new federal laws. We’re here to simplify the jargon and act as your guide. Our goal is to find the specific plan that says “yes” to your medications while keeping your monthly budget predictable.

The New 2026 Spending “Security Blanket”

This year brings the most significant change in decades for Medicare Part D. Thanks to the Inflation Reduction Act, you now have a $2,100 annual out-of-pocket limit on your covered medications. Once you reach this cap, you pay $0 for your covered drugs for the rest of the year. It’s a massive relief, but there’s a catch. Your 2025 plan might have changed its “formulary,” which is the list of drugs it agrees to cover. If your medication isn’t on that list, it won’t count toward your $2,100 cap. This is why we carefully check that every one of your pills is classified as a “covered drug” under the new 2026 rules.

Why One Size Never Fits All in Medicare

It’s tempting to pick the same plan as your neighbor because they like their low premium. However, their plan might be a total disaster for your specific needs. Medicare plans are highly individual. A plan that offers a great price on a common heart medication might charge a fortune for the specific insulin you use. When we help with Medicare Part D comparisons, we perform a personalized drug list review. We don’t just look at the names of your meds; we look at your exact dosages and how often you fill them. A plan might cover a 10mg dose at a low “Tier 1” price but move the 20mg dose to a much more expensive tier. We make sure those details are caught before you sign up.

Understanding Formularies, Tiers, and Pharmacy Networks

Finding a medicare plan that covers my prescriptions is easier when you understand the “master menu” each insurance company creates. In the insurance world, this menu is called a formulary. It’s a complete list of every medication the plan agrees to pay for. If a drug isn’t on this list, the plan won’t cover it at all, and you’ll be stuck paying the full retail price. We don’t want that for you. Every plan has a different menu, which is why we spend so much time comparing them side by side.

You should also be aware of the “Step Therapy” trap. This happens when a plan refuses to pay for a specific brand-name drug until you try a cheaper, generic version first. It’s a way for insurance companies to save money, but it can be a huge headache for you and your doctor. We look for these restrictions ahead of time so you aren’t surprised at the pharmacy counter. By looking at the details now, the process of finding a medicare plan that covers my prescriptions becomes much more logical and less stressful.

Decoding the Tier Structure

Insurance companies group drugs into “tiers” to determine your cost. Think of tiers as price levels. Tier 1 and Tier 2 usually include budget-friendly generics. These are the lowest-cost options and often have a $0 copay. Tier 3 and Tier 4 are for brand-name medications. These costs can fluctuate significantly between different plans. Tier 5 is reserved for specialty drugs. While these are the most expensive, the 2026 rules provide a safety net. Once your out-of-pocket costs hit the $2,100 cap, your responsibility for these Tier 5 drugs drops to $0 for the rest of the year.

Why Your Pharmacy Choice is a Contract

Where you shop matters just as much as what you buy. Most plans have a network of “preferred” pharmacies where they’ve negotiated the lowest prices. If you go to a “standard” pharmacy or one that’s out-of-network, you’ll likely pay much more for the exact same pill. You can find more details about how these networks function in our guide to Medicare Part D Explained.

Some people prefer the convenience of mail-order pharmacies, which often offer a 90-day supply for a lower total cost. Others value the relationship they have with their local pharmacist. You can check the official Medicare website to see general network rules, but we prefer to run a custom report for your specific zip code. If you’re feeling overwhelmed by these choices, reviewing your 2026 options with us can provide the clarity you need to move forward with confidence.

Standalone Part D vs. Medicare Advantage: Two Paths to Coverage

When you begin the journey of finding a medicare plan that covers my prescriptions, you’ll eventually reach a fork in the road. Your choice isn’t just about the pills you take; it’s about how you want your entire healthcare experience to feel. We often describe these two paths as the “A la Carte” approach versus the “All-in-One” approach. Both paths include the new 2026 protections, like the $2,100 out-of-pocket spending limit, but they handle your medical and drug coverage very differently.

It’s vital to understand that your choice of medical coverage dictates your prescription options. If you choose Original Medicare, you generally need to add a separate drug plan. If you choose a private Medicare Advantage plan, the drug coverage is usually already bundled inside. We’re here to help you weigh the pros and cons so you can decide which structure provides the most peace of mind for your specific situation.

When Standalone Part D Makes Sense

The first path involves keeping Original Medicare and adding Medicare Supplement Insurance to cover the “gaps” in your medical bills. Because these supplement plans don’t include drug coverage, you must purchase a standalone Part D plan. This “A la Carte” style offers incredible flexibility. For example, if your favorite pharmacy leaves your drug plan’s network next year, you can switch to a different Part D plan without ever having to worry about your doctors or your medical coverage changing. This path is often the best fit for people who want to see any doctor in the country who accepts Medicare while still ensuring their medications are covered.

The Convenience of Medicare Advantage (MAPD)

The second path is choosing Medicare Advantage Plans that include prescription drug coverage, often called MAPD plans. This is the “All-in-One” approach. You have one insurance card for your doctor visits, hospital stays, and pharmacy trips. These plans often simplify your life by keeping your billing in one place. Many people find this path attractive because these plans frequently include extra perks that Original Medicare doesn’t offer, such as Dental Insurance Plans or vision benefits.

However, because your medical and drug coverage are tied together, you can’t change one without the other. If you find a better drug plan elsewhere, you’d have to leave your entire Medicare Advantage plan to get it. This is why finding a medicare plan that covers my prescriptions requires a careful look at the “big picture.” You can use the Medicare Plan Finder tool to see raw data, but we prefer to sit down with you and look at how these networks actually affect your daily life. We want to make sure your doctors and your drugs are all on the same team.

Your 5-Step Checklist for Matching a Plan to Your Medications

We believe that clarity is the best cure for anxiety. While the new 2026 rules offer a safety net, the process of finding a medicare plan that covers my prescriptions still requires a bit of detective work. You don’t have to do this alone, but having a structured path makes the journey much easier. We’ve developed a simple checklist to help you organize your thoughts and ensure no detail is overlooked before you sign your name to a new plan.

- Step 1: Gather your current bottles. Don’t rely on memory. Write down the exact name, the dosage (like 20mg), and how often you take it. Even a small change in dosage can move a drug to a different price level.

- Step 2: Identify your “must-have” pharmacy. Do you prefer the local shop around the corner or the convenience of mail-order? We need to verify that your pharmacy is “preferred” in the plan’s 2026 network to get you the lowest price.

- Step 3: Check the 2026 Formulary. We look at the updated master menu for every plan to confirm your specific medications are still listed as covered drugs.

- Step 4: Calculate the “Total Annual Cost.” This is the most important math. We add the monthly premium to your expected copays and any deductible to see the real price tag.

- Step 5: Verify restrictions. We check if your medications require “Prior Authorization” or have “Quantity Limits.”

The “Total Cost” Trap

It’s very common to see a plan with a $0 monthly premium and think it’s the best deal. However, we often find that a plan with a $30 premium actually saves you more money over the full year. This happens because the $0 premium plan might have much higher copays for your specific brand-name drugs. When we look at Medicare Part D options, we look at the big picture. We do all this math for you for free, comparing every cost until we find the lowest total number. It’s about finding a medicare plan that covers my prescriptions without hidden financial surprises.

Checking for Restrictions Before You Enroll

Some plans use “Prior Authorization,” which means your doctor must get the “okay” from the insurance company before they’ll pay for the drug. Others have quantity limits that might prevent you from getting a full 90-day supply at once. These hurdles can be frustrating, but we help you navigate them during the enrollment window. We want you to walk into the pharmacy in January knowing exactly what to expect. If you’re ready to see how these steps apply to your specific medications, request a personalized drug cost review from our team today.

How We Help You Navigate the 2026 Prescription Landscape

We believe that finding a medicare plan that covers my prescriptions should be a journey from distress to absolute certainty. You’ve already seen how complex the 2026 rules can be with the new $2,100 spending cap and the removal of the old coverage gap. While automated search tools can give you a list of numbers, they often fail to capture the nuances of pharmacy networks or specific drug restrictions. We don’t want you to be a victim of a “tier change” or a surprise bill at the pharmacy counter. We’re here to act as your personal advocate and educator.

Our support doesn’t end once you’ve signed up for a plan. If your doctor prescribes a new medication in the middle of the year, we’re here to help you understand how your coverage applies. We provide year-round support because your health needs don’t follow a calendar. We’ve helped thousands of people move from a state of confusion to a clear, confident choice. We do the hard work of comparing dozens of options so you can focus on your health.

Why Independent Guidance Matters

There’s a significant difference between a “captive” agent who works for one insurance company and an independent broker. A captive agent is restricted to the limited options their employer offers. We’re different. We work for you, not the insurance carriers. We have access to plans across 34 states, which allows us to find the specific plan that prioritizes your unique drug list and budget. Our commitment is to provide unbiased, expert education. We explain the “why” behind every recommendation, ensuring you feel empowered rather than pressured.

Ready to Find Your 2026 Plan?

You don’t have to tackle this process alone. Finding a medicare plan that covers my prescriptions is much simpler when you have a dedicated expert by your side. We invite you to reach out to us for a no-obligation drug list review. Before we talk, gather your current medication bottles so we have the exact dosages and frequencies. When you speak with Paul and the team, we’ll walk through your options step-by-step until you feel completely secure in your decision. We’re ready to help you secure the coverage you deserve for 2026. Contact us today to get started and leave the pharmacy anxiety behind.

Secure Your Health and Savings for the Year Ahead

You now have the tools to move from a state of uncertainty to one of total confidence. We’ve explored how the new federal spending caps and the removal of the coverage gap have fundamentally changed the way you’ll experience Medicare this year. Finding a medicare plan that covers my prescriptions is the final piece of the puzzle in protecting your retirement budget. By following our 5-step checklist and understanding your pharmacy network, you’ve already done the hard work of preparing for the months ahead.

Our team is ready to take the weight off your shoulders by doing the detailed comparison work for you. Paul Barrett and his expert staff offer year-round support and access to plans from over 40 carriers across more than 34 states. We’re committed to being your advocate; we’ll ensure your coverage remains reliable even if your medications change in the future. Let us help you find the perfect 2026 plan; contact The Modern Medicare Agency today. You’ve worked hard for your health; let’s make sure your insurance works just as hard for you.

Common Questions About 2026 Prescription Coverage

What is the out-of-pocket cap in 2026?

The 2026 out-of-pocket cap is $2,100. This is a major improvement from previous years. Once you spend $2,100 on covered medications, your plan pays 100% of your drug costs for the rest of the year. You won’t have to worry about the “donut hole” anymore because it has been officially eliminated. This cap provides a much-needed safety net for your retirement savings.

Can I change my Medicare drug plan if my doctor prescribes a new medication?

You can generally only change your plan during the Annual Enrollment Period from October 15 to December 7. Changes made then start on January 1. If you have a Medicare Advantage plan, you also have a window from January 1 to March 31 to make one change. Special circumstances, like moving to a new state, might also let you switch plans mid-year.

What happens if a Medicare plan drops my drug from its formulary?

Plans must send you a written notice before they remove a drug or move it to a more expensive tier. If this happens, your doctor can help you request a “formulary exception” to keep your cost low. We recommend reviewing your coverage every autumn because finding a medicare plan that covers my prescriptions depends on the most current drug list provided by the carrier.

Do I need a prescription drug plan if I don’t take any medications right now?

Yes, we strongly suggest enrolling in at least a basic plan. Medicare requires you to have “creditable” drug coverage once you’re eligible. If you go 63 days or more without it, you’ll likely face a permanent late enrollment penalty. Picking a plan with a low monthly premium now protects you from future fees and ensures you’re covered if your health needs suddenly change.

Is there a penalty for not signing up for a drug plan when I first get Medicare?

There is a permanent monthly penalty added to your premium if you delay enrollment without having other creditable coverage. The government calculates this fee based on how many months you went without a plan. It’s a lifelong cost that can really add up. We help you avoid this mistake by finding a plan that meets the requirements as soon as you’re eligible.

Will my Medicare Advantage plan automatically cover my prescriptions?

Most Medicare Advantage plans include drug coverage, but some don’t. You should always look for “MA-PD” on the plan details to be sure. Finding a medicare plan that covers my prescriptions within an Advantage plan requires a careful look at the specific formulary. We can verify if your medications are included before you make any decisions about your 2026 healthcare.

How do I know if my pharmacy is “preferred” in my 2026 plan?

You can find this information in the plan’s pharmacy directory or by using the search tools on the Medicare website. Preferred pharmacies are those that have agreed to charge lower copays for the plan’s members. If you use a “standard” or out-of-network pharmacy, you’ll pay more for the exact same pills. We can check your favorite local pharmacy’s status for you.

What is the difference between a Brand name drug and a Generic drug on the formulary?

Generic drugs use the same active ingredients as brand-name drugs but are much more affordable. On your plan’s tier system, generics are usually in Tier 1 or Tier 2 with very low copays. Brand-name drugs sit in higher tiers and cost more. If your drug is expensive, we can help you talk to your doctor about switching to a generic version to save money.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com