What if the heavy stack of insurance mailers on your kitchen table is actually hiding the most important date for your future health? Many people believe they must wait for the autumn season to make a change, but the best time to buy a medigap policy is usually a much more personal window that has nothing to do with October. We understand the pressure you feel when you try to decode these complex rules. It is frustrating to worry that a past health issue might keep you from getting the protection you need, especially with the Part B deductible rising to $283 this year.

We want to replace that anxiety with a clear, simple plan. We will explain exactly how to use your one-time enrollment “hall pass” to lock in lifelong security without answering a single medical question. You will also learn how new 2026 rules in states like Delaware and Indiana are creating fresh opportunities to switch plans. This guide provides the specific timeline you need to ensure you secure the lowest rates and guaranteed acceptance for your Medicare Supplement coverage.

Key Takeaways

- Learn why the six-month window after you start Part B is the best time to buy a medigap policy to guarantee you get the lowest rates.

- Understand how to skip medical underwriting entirely, ensuring your health history never prevents you from getting the coverage you deserve.

- Discover the specific rules for those working past 65 so you don’t miss your chance to secure a plan when your employer coverage ends.

- Find out how new state laws in 2026 provide annual opportunities to switch plans without the stress of health questions.

- We show you how to move from confusion to certainty by comparing options from over 40 different carriers in one simple step.

Understanding the ‘Golden Window’ for Medigap in 2026

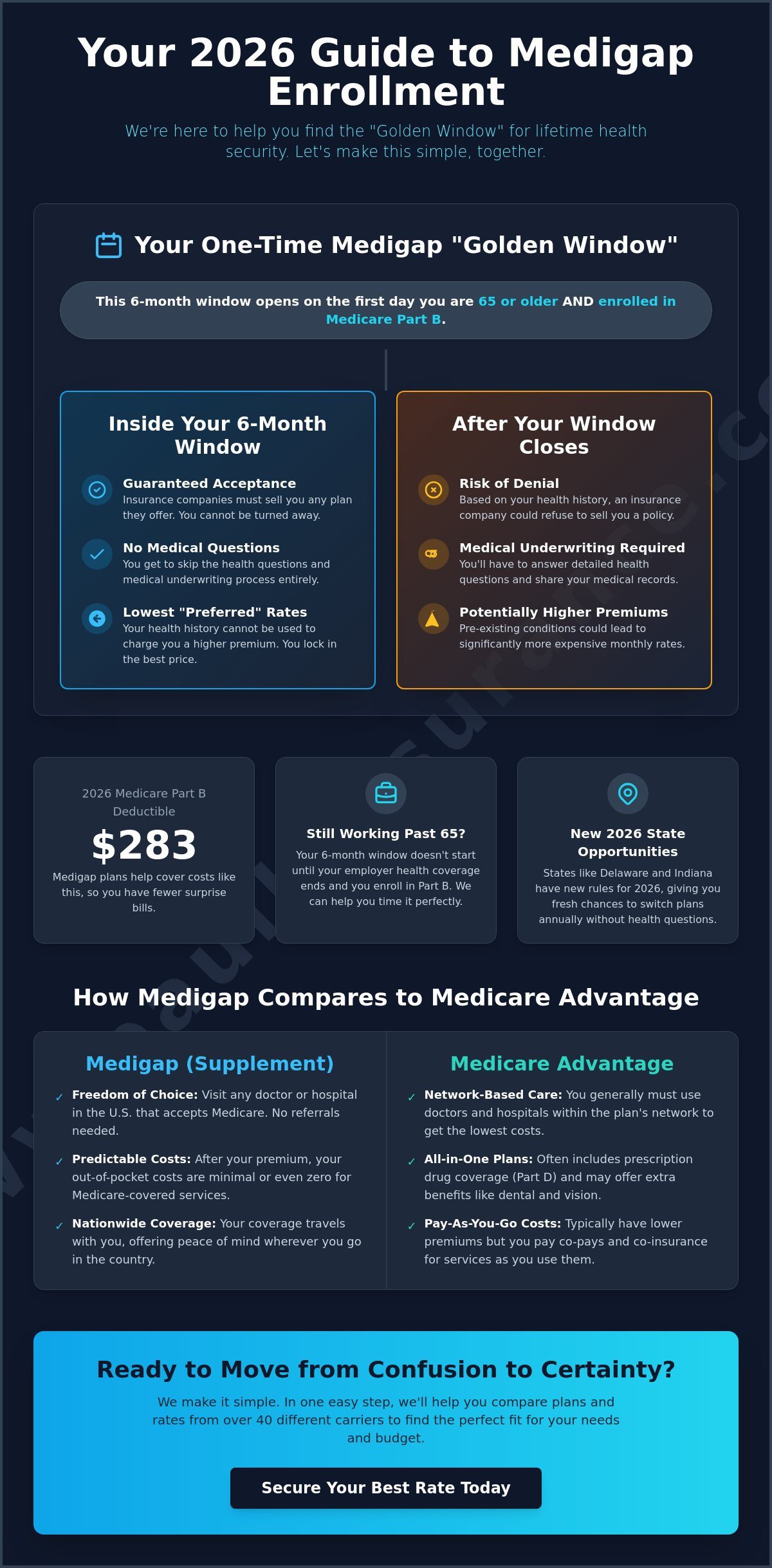

We believe your health coverage should feel like a sturdy safety net rather than a stressful puzzle. Many people feel overwhelmed by the constant stream of insurance mailers, but there is one specific timeframe that simplifies everything. The best time to buy a medigap policy is during your one-time Medigap Open Enrollment Period. This six-month window starts automatically the very first day you are both 65 or older and enrolled in Medicare Part B. We call this your “Golden Window” because it provides a level of health security that is difficult to find at any other time.

During this period, you have a unique protection called “guaranteed issue” rights. This means insurance companies must sell you any policy they offer, and they cannot charge you more because of your health history. It is a moment of total clarity in a complex system. Since Medigap plans are designed to work alongside Original Medicare, they help pay for costs that the government doesn’t cover. For example, in 2026, the Medicare Part B deductible is $283. A supplement plan can help manage these out-of-pocket expenses so you aren’t surprised by medical bills.

Why Timing Matters More Than You Think

Waiting even a few months past your window can change the entire process. If you apply for coverage later, you may have to go through medical underwriting. This involves answering detailed questions about your health, which could lead to higher rates or even a denial of coverage. We want to help you avoid that stress entirely. We work with you to identify your exact start date based on your Part B effective date, ensuring you don’t miss a single day of this protected status. Securing your plan during the best time to buy a medigap policy is the most effective way to protect your physical and financial well-being for the long term.

Medigap vs. Other Options: A Quick Look

You might be wondering how these plans compare to other choices like Medicare Advantage. While both provide value, they work very differently. Medigap plans generally offer more freedom. You can visit any doctor or specialist in the country who accepts Medicare without needing a referral. If you prefer a plan that includes extra perks like dental or vision within a specific network, you might explore Medicare Advantage Plans: A Simple Guide. However, for those who prioritize predictable costs and the ability to see any provider, a supplement plan remains the gold standard. We are here to help you weigh these options so you can move forward with absolute peace of mind.

Your One-Time Medigap Open Enrollment Period

Imagine a clock starting the moment you step into a new chapter of life. For most people, that clock begins ticking on the first day of the month they turn 65. This is your Medigap Open Enrollment Period. It lasts for exactly six months. We see many people feel rushed during this time, but we are here to help you move at your own pace while keeping an eye on the deadline. This period is the best time to buy a medigap policy because it is your only chance to get coverage without a health check. We want you to feel protected. It is a simple goal. We achieve it by watching the calendar together.

You must have Medicare Part B active to participate in this window. If you skip Part B, you cannot buy a supplement plan. We often find that clients who plan ahead feel much more confident. They don’t just wait for the mailers to arrive; they take charge of their timeline. If you have questions about how these plans work, you can explore What Is Medicare Supplement Insurance? to see which options fit your lifestyle. By coordinating your start dates, we ensure you never face a day without the coverage you need.

The Part B Trigger Explained

Your enrollment in Medicare Part B acts as the starting gun for your 180-day window. It doesn’t matter if you are 65 or 75 when you first sign up for Part B; the six-month clock starts the same way. We help you coordinate your application so your supplement plan begins the same day your Part B coverage starts. This prevents any gaps in your protection. If you want to see how these rates compare for your specific area, you can view our plan comparison tools to get started.

Securing the Best Rates in 2026

In 2026, insurance companies continue to offer their most competitive prices to people in their initial enrollment window. These are often called “Preferred Rates.” When you apply during this time, companies cannot charge you more for a pre-existing condition. This is why we emphasize that this is the best time to buy a medigap policy. You lock in a lower rate from the start, giving you financial peace of mind. We believe everyone deserves access to these rates, regardless of their medical history. Our role is to act as your advocate, ensuring the insurance companies honor these protections and provide you with the most affordable options available today.

Special Situations: When You Get a Second Chance

Life rarely follows a perfect schedule. While we often focus on the 65th birthday, we know that many of you are still thriving in your careers well past that age. If you have health insurance through a large employer, your timeline looks different. You don’t have to worry about missing out on coverage. For you, the best time to buy a Medigap policy is simply paused until you decide to retire. We help you navigate these unique turns in the road, ensuring you never feel pressured to make a choice before you are ready.

There are also moments where the system gives you a fresh start. If your current plan stops serving your area or you move to a new state, you may qualify for a “Guaranteed Issue” right. This is a 63-day window where you can secure a plan without any health questions. We see many people worry when their coverage changes unexpectedly, but we view these moments as opportunities to find a more stable path. In 2026, with the Part D out-of-pocket cap rising to $2,100, having a reliable supplement in place is more important than ever. We stay by your side to make sure you meet these short deadlines with confidence.

Working Past 65 and Delaying Part B

If you have “creditable” coverage from an employer with 20 or more employees, you might choose to delay Medicare Part B. This is a smart move for many, as it saves you from paying unnecessary premiums. Your six-month enrollment window doesn’t start until your Part B coverage begins. A common mistake we see is people assuming COBRA counts as creditable coverage. It doesn’t. We help you time your retirement so your Part B and your Medigap plan start the same day, preventing any expensive gaps in your care.

The Medicare Advantage Trial Right

We often meet people who decided to give Medicare Advantage a “test drive” but found it didn’t meet their needs. Perhaps you realized you wanted more freedom to choose your own doctors. If it’s your first time in a Medicare Advantage plan and you have been enrolled for less than 12 months, you have a special “Trial Right.” This allows you to switch back to a Medigap plan with guaranteed acceptance. We specialize in helping people navigate this transition through our Medigap service page, making the journey back to supplement coverage simple and stress-free. For many, the best time to buy a medigap policy is the moment they realize they need more flexibility than their current plan provides.

The Risks of Waiting: Understanding Medical Underwriting

We know it is tempting to put off another monthly premium when you feel healthy today. It’s a natural reaction to a busy life. However, waiting until you actually need medical care to apply for a supplement plan is a risky strategy. Outside of your initial window, insurance companies use a process called medical underwriting. Underwriting is the process where a company evaluates your “risk” before agreeing to cover you. They look at your health history to decide if they will offer you a policy and at what price. This is why the best time to buy a medigap policy is while you still have your “hall pass” of guaranteed acceptance.

If you miss your open enrollment window, you lose your protection against health questions. The insurance company can then look back at your medical records. They might see a minor issue that you haven’t thought about in years, but to them, it represents a future cost. We want to help you avoid the frustration of being told “no” simply because you waited too long. By securing coverage early, you protect your future self from these difficult hurdles.

Common Health Knockouts

Every insurance company has its own set of rules, but many use similar “knockout” conditions to deny coverage. We have seen people struggle to find a plan after being diagnosed with chronic conditions such as COPD or diabetes with certain complications. Companies also use different “look-back” periods, which are the number of years of medical history they review. One company might look back two years, while another looks back five. We help you understand these differences so you can make an informed choice before your health changes. It is much easier to get the plan you want when you are healthy than it is to search for one after a diagnosis.

The Cost of a Late Entry

Even if a company agrees to cover you after your window has closed, it may cost you more every month. They often use two different price levels: Preferred and Standard. Preferred rates are the lowest prices available, and they are usually only guaranteed during your initial enrollment. If you have to go through underwriting, you might be assigned a Standard rate, which can significantly increase your monthly budget. Over ten or twenty years, that extra cost adds up to thousands of dollars. We believe in protecting your wallet as much as your health. To see if you are still in your protected window, you can view our medigap plan options and let us help you find the most stable path forward. Securing your plan now is truly the best time to buy a medigap policy to ensure you never face these financial penalties.

Navigating Your 2026 Medicare Journey With Us

We know that the noise of insurance marketing can feel overwhelming, especially when you are trying to make a decision that affects your health for years to come. Our mission is to turn down that noise. We act as your personal advocate, moving you from a state of confusion to a place of total certainty. Because we are independent, we aren’t restricted to just one company. We look at over 40 different carriers to find the plan that fits your specific needs. We believe that the best time to buy a medigap policy is when you have an expert guide by your side to ensure every detail is handled correctly.

Our relationship with you doesn’t end once your application is submitted. We provide support all year long. If you receive a confusing bill or a notice from your insurer, we are the first call you make. We pride ourselves on offering unbiased guidance that prioritizes your peace of mind over any sales target. You deserve a partner who is as committed to your health security as you are. By choosing an independent professional, you gain access to a wider range of options and a champion who works only for you.

What’s New in 2026?

The landscape has shifted this year, and we have kept a close watch on every change. In 2026, the Medicare Part B deductible has increased to $283. We also see significant updates in prescription coverage, with the Part D out-of-pocket spending cap rising to $2,100. These rising costs make choosing the right supplement plan even more vital to your financial health. If you are also looking for help with your medications, we suggest you explore our Medicare Part D Guide to see how these new caps affect your monthly budget. Additionally, new “birthday rules” in states like Indiana and Delaware now offer annual windows to switch plans, providing a second chance for those who missed the initial best time to buy a medigap policy.

How to Get Started Today

We have simplified our process into three easy steps to remove any remaining stress from your journey. First, we have a brief conversation to understand your health goals and budget. Second, we perform a side-by-side comparison of the top-rated plans in your area. Finally, we help you complete the enrollment process with ease. Our support comes at no cost to you, as we are compensated by the insurance carriers. We invite you to reach out for a simple “Medicare check-up” to ensure your 2026 coverage is exactly where it needs to be. We are ready to help you secure your future with confidence and clarity.

Secure Your Peace of Mind for 2026

We want you to feel confident that your health coverage is built on a solid foundation. You’ve learned that the six-month window following your Part B enrollment is the absolute best time to buy a medigap policy because it removes the stress of health questions. Whether you are retiring today or exploring a “trial right” after a year with another plan, timing is the key to locking in lower rates and lifelong security. We are here to help you navigate these dates so you never have to worry about being turned away due to a pre-existing condition.

With access to over 40 insurance carriers and licenses in 34+ states, we provide the unbiased expert guidance you need to make the right choice. Our help is always free; and we pride ourselves on being your long-term advocate. Let us help you find the perfect Medigap timing—reach out to our friendly team today!

You don’t have to face these complex decisions alone. We look forward to helping you move from uncertainty to a place of total clarity for your 2026 healthcare journey.

Frequently Asked Questions

What is the Medigap Open Enrollment Period?

The Medigap Open Enrollment Period is a unique six-month window that begins the first day of the month you are 65 or older and enrolled in Medicare Part B. During this time, we can help you secure any plan available in your area without a single health question. It’s the most important date on your Medicare calendar because it guarantees you the right to buy a policy at the best available rate.

Can I buy a Medigap policy at any time during the year?

You can apply for a policy at any point during the year; however, the best time to buy a medigap policy is during a protected enrollment window. Outside of these specific times, insurance companies usually require you to answer medical questions to determine your eligibility. We can help you check if you currently qualify for a special window that bypasses these health hurdles.

What happens if I miss my 6-month Medigap window?

If you miss your initial window, you may be subject to medical underwriting, which allows an insurance company to review your health history. They might charge you a higher premium or deny your application if you have certain chronic conditions. We also look for state-specific rules, like the new 2026 laws in Indiana and Delaware, that might give you a second chance to enroll without these health checks.

Do I need a Medigap policy if I already have Medicare Advantage?

No, you cannot have both a Medicare Advantage plan and a Medigap policy at the same time. It’s actually illegal for a company to sell you a supplement plan if they know you’re already enrolled in an Advantage plan. We can help you compare these two different paths to see which one provides the long-term peace of mind you deserve.

What are “guaranteed issue rights” and do I have them?

Guaranteed issue rights are legal protections that require insurance companies to sell you a plan regardless of your medical history. You typically have these rights during your initial six-month window or if your current coverage ends, such as when an employer plan stops. We track these rules closely to ensure you never miss an opportunity for guaranteed acceptance when your circumstances change.

Can an insurance company drop my Medigap coverage if I get sick later?

An insurance company cannot cancel your coverage because of your health as long as you pay your premiums on time. All Medigap policies are “guaranteed renewable,” which means your protection stays in place even if you develop a new illness years after signing up. We only work with carriers that offer this level of stability so you can feel secure in your coverage for life.

Is 2026 a good year to switch from Advantage to Medigap?

Yes, 2026 is an excellent year to consider a switch because the Part D drug spending cap is increasing to $2,100. Many people find that the best time to buy a medigap policy is when they want more predictable costs than an Advantage plan provides. With some Advantage plans reducing extra benefits this year, we can help you evaluate if your current plan still meets your needs.

How much does a Medigap policy cost in 2026?

The cost of a policy in 2026 depends on which plan letter you choose, your age, and where you live. While we don’t provide a single price for everyone, we can show you a side-by-side comparison of over 40 different carriers to find the most competitive rate. We believe in finding a balance between an affordable monthly premium and the comprehensive coverage that protects you from the $283 Part B deductible.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com