Medicare education is the process of learning about Medicare coverage options, costs, and enrollment rules so you can make confident healthcare decisions at age 65 or when leaving employer coverage. Why Medicare education matters becomes clear the moment you realize that most people approaching this transition carry serious misconceptions about what Medicare actually covers and what it costs. Proactive Medicare conversations ease stress and uncover retirement planning opportunities that most people miss entirely. At Paulbinsurance, we have worked with Medicare consumers since 2007, and the pattern is consistent: the people who struggle most are the ones who waited too long to learn.

Why Medicare education matters more than most people realize

The average person approaching Medicare eligibility knows far less than they think. Consumers scored fewer than 4 correct answers out of 10 on a Medicare basics quiz, and nearly 80% say they want help understanding coverage, timing, and costs. That score means most people heading into one of the biggest financial decisions of their retirement are working with less than half the information they need.

The knowledge gaps are not limited to consumers. Only 15% of consumers discussed Medicare with a financial professional, and those professionals averaged just 6 correct answers out of 10 themselves. This means the people most likely to be asked for guidance are also operating with incomplete information.

The consequences show up in real dollars. Only 26% of U.S. adults correctly understand that Medicare covers roughly two-thirds of retiree healthcare costs. The remaining third includes premiums, copays, deductibles, prescriptions, dental, vision, hearing, and long-term care. Overestimating coverage leads directly to underestimating retirement expenses.

“The biggest mistake I see isn’t choosing the wrong plan. It’s assuming Medicare covers everything and building a retirement budget around that assumption.”

Common knowledge gaps include:

- Enrollment windows: Missing your Initial Enrollment Period triggers late enrollment penalties that follow you for life.

- Coverage limits: Medicare does not cover routine dental, vision, or hearing without a supplement or Advantage plan.

- Out-of-pocket exposure: Original Medicare has no annual out-of-pocket maximum, which surprises most new enrollees.

- Part D complexity: Drug formularies change annually, meaning a plan that covered your medications in 2025 may not in 2026.

How does Medicare differ from employer coverage?

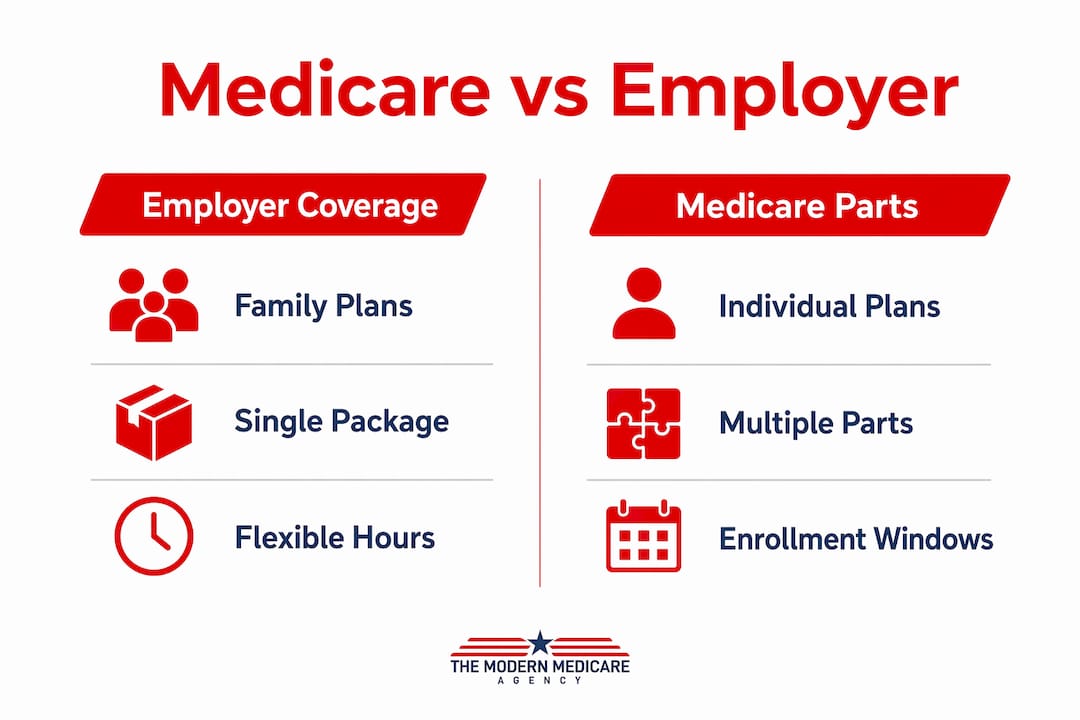

Employer coverage works as a single package. Medicare does not. Medicare is divided into parts, and each part covers a different category of care. Part A covers hospital stays, Part B covers outpatient services and doctor visits, Part C (Medicare Advantage) bundles A and B through private insurers, and Part D covers prescription drugs. Understanding Medicare’s parts and costs is the foundation of making any enrollment decision well.

The structural differences go beyond coverage categories. Employer plans often cover your entire family under one policy. Medicare covers only the individual. Your spouse must enroll separately and on their own timeline. This catches couples off guard, particularly when one spouse is younger than 65 and loses dependent coverage when the older spouse retires.

| Feature | Employer coverage | Medicare |

|---|---|---|

| Family coverage | Yes, typically included | No, individual enrollment only |

| Annual out-of-pocket maximum | Yes, required by law | Only with Advantage plans |

| Prescription drug coverage | Usually bundled | Requires separate Part D enrollment |

| Provider network | Employer-selected | Varies by plan type |

| Enrollment timing | At hire or open enrollment | Strict windows tied to age and work status |

Choosing the right Medicare path requires evaluating your health status, the medications you take, your preferred doctors, and your tolerance for cost-sharing. These are factors employer plan selection rarely forces you to think through in the same detail.

Pro Tip: If you are still working at 65 and covered by employer insurance, you may be able to delay Part B without penalty. Confirm with your HR department whether your employer plan qualifies as creditable coverage before making any decisions.

Missing enrollment windows is one of the most financially damaging mistakes a new beneficiary can make. The Part B late enrollment penalty adds 10% to your premium for every 12-month period you were eligible but did not enroll. That penalty is permanent. Our guide on avoiding enrollment mistakes walks through exactly when and how to enroll without triggering penalties.

What is the “knowing vs. doing” gap in Medicare enrollment?

Understanding Medicare and actually completing Medicare enrollment are two different problems. Medicare patients face a significant administrative burden that blocks access even when they know what they need to do. Forms are lengthy. Phone wait times are long. Follow-up calls get dropped. Verification steps get missed.

“Information alone does not produce enrollment. Action does. And action requires someone to guide you through the steps, not just hand you a brochure.”

The execution gap shows up in predictable ways. Here are the most common administrative hurdles new beneficiaries face:

- Social Security coordination: Enrolling in Medicare Part B requires coordination with the Social Security Administration, which involves separate applications and timing rules that confuse most first-time enrollees.

- Prescription drug plan selection: Comparing Part D plans requires entering your specific medications into Medicare’s Plan Finder tool and evaluating formularies, tiers, and pharmacy networks.

- Supplement underwriting: Medigap plans outside of your Open Enrollment Period require medical underwriting in most states, meaning your health history affects your eligibility and pricing.

- Annual plan reviews: Medicare Advantage and Part D plans change every year during the Annual Enrollment Period (October 15 to December 7). Failing to review your plan annually can result in higher costs or lost coverage.

Patient advocates and independent agents close this gap by turning knowledge into completed tasks. Educational materials structured as actionable task lists with timing, document requirements, and verification steps produce better outcomes than benefit overviews alone.

Pro Tip: Before your 65th birthday, create a simple checklist: confirm your Social Security enrollment status, list your current medications, identify your preferred doctors, and note your current plan’s creditable coverage status. This 30-minute exercise prevents most common enrollment errors.

How does Medicare education improve financial confidence?

The financial stakes of Medicare literacy are not abstract. 62% of Medicare beneficiaries say Medicare is extremely important to their ability to afford healthcare. Six in ten adults are more concerned about Medicare changes today than they were a year ago. Education does not eliminate that concern, but it gives you the tools to plan around it rather than react to it.

Fidelity estimates $172,500 in healthcare costs per person over retirement, excluding long-term care. Healthcare inflation consistently outpaces general inflation. A retiree who overestimates Medicare coverage and underestimates out-of-pocket costs will face a cash flow crisis that no amount of Social Security income can easily absorb.

Medicare literacy reduces that risk by teaching you to evaluate total cost, not just monthly premiums. The factors that matter most include:

- Deductibles: The 2026 Part B deductible and Part A hospital deductible both affect your annual out-of-pocket exposure before coverage kicks in.

- Coinsurance: Original Medicare typically covers 80% of approved costs. You are responsible for the remaining 20% with no cap unless you have a Medigap policy.

- Drug formularies: Your Part D plan’s formulary determines which medications are covered and at what cost tier. A formulary change mid-year can double your monthly drug costs.

- Supplemental coverage: Medicare Supplement plans (Medigap) and Medicare Advantage plans handle cost-sharing differently. Knowing which structure fits your health and financial situation is the core of evaluating total Medicare costs.

You can also reduce prescription costs significantly through tools like prescription savings programs that work alongside your Part D coverage. Combining a well-chosen drug plan with a savings program is a strategy most new beneficiaries never consider because no one explained it to them.

Key takeaways

Medicare education is the single most effective way to prevent costly enrollment mistakes, coverage gaps, and retirement budget shortfalls for anyone approaching age 65.

| Point | Details |

|---|---|

| Knowledge gaps are widespread | Consumers average fewer than 4 correct answers out of 10 on Medicare basics, making education urgent. |

| Medicare differs structurally from employer plans | No family coverage, strict enrollment windows, and separate parts require individual planning. |

| Execution matters as much as knowledge | Administrative burdens block enrollment even for informed beneficiaries; guided task lists improve outcomes. |

| Financial stakes are high | Fidelity estimates $172,500 per person in retirement healthcare costs, making accurate coverage knowledge critical. |

| Total cost beats premium focus | Evaluating deductibles, coinsurance, and drug formularies prevents budget surprises that premiums alone do not reveal. |

Why I tell every client to start learning before they think they need to

I have been working with Medicare consumers since 2007, and the single most consistent pattern I see is this: people wait until they are 64 and a half to start asking questions, and by then, they are already behind. The enrollment window opens three months before your 65th birthday. If you start learning at 64 and a half, you have weeks, not months, to make decisions that will affect your healthcare costs for the rest of your life.

The second pattern I see is what I call the premium trap. People compare plans by monthly premium and pick the lowest number. Then they spend the year paying for services their plan does not cover well, or they discover their doctor is out of network, or their medication jumped two formulary tiers. The premium was low. The total cost was not.

What I have found actually works is treating Medicare education as a retirement planning task, not a healthcare task. The people who come in with a list of their medications, their doctors, and a rough sense of their retirement income are the ones who make good decisions. The people who come in with a plan brochure and a question about the monthly cost are the ones who need the most help.

My honest advice: start with our Medicare 101 seminar before you talk to anyone about specific plans. Get the foundation right first. Then the plan comparison becomes a much shorter conversation.

— Paul

Get personalized Medicare guidance for 2026

Paulbinsurance specializes in Medicare education and independent plan comparison for individuals approaching 65 or leaving employer coverage. Our team of independent agents does not represent one carrier. We represent you.

Whether you need a clear explanation of your 2026 options or hands-on help completing enrollment, we have the resources to support you. Start with our 2026 Medicare confidence guide for a plain-language breakdown of every coverage decision you will face. If cost management is your priority, our retirement healthcare cost guide walks through strategies for controlling out-of-pocket expenses through smart plan selection. Contact us directly for a no-pressure, one-on-one consultation.

FAQ

What does Medicare education actually cover?

Medicare education covers the structure of Medicare Parts A, B, C, and D, enrollment timelines, cost-sharing rules, and how to compare plan options based on your health needs and budget. It also addresses the administrative steps required to complete enrollment without triggering penalties.

When should I start learning about Medicare?

Start at least six months before your 65th birthday. Your Initial Enrollment Period opens three months before the month you turn 65, so you need time to research options before that window begins.

Why does Medicare education matter if I already have good employer coverage?

Employer coverage ends or changes when you retire or reduce your hours. Medicare has strict enrollment windows tied to your work status, and missing them results in permanent late enrollment penalties. Understanding the transition rules before you leave employer coverage prevents costly mistakes.

How is Medicare Advantage different from Original Medicare?

Medicare Advantage (Part C) bundles hospital, outpatient, and usually drug coverage through a private insurer, often with lower premiums but narrower provider networks. Original Medicare offers broader provider access but no annual out-of-pocket cap without a Medigap supplement.

Can Medicare education help me reduce my healthcare costs in retirement?

Yes. Evaluating total out-of-pocket costs including deductibles, coinsurance, and drug formularies rather than focusing only on premiums is the most direct way education reduces retirement healthcare expenses. Fidelity estimates $172,500 per person in retirement healthcare costs, and informed plan selection is the primary lever for managing that figure.