It is June 2026, and you just realized your 65th birthday was several months ago, meaning your seven-month window for Medicare has officially closed. You are likely staring at your calendar and wondering exactly what happens if i miss my initial enrollment period. We know that heavy, anxious feeling that comes when you realize a major deadline has passed. It is completely normal to feel overwhelmed by these complex rules or to worry about how a delay might affect your monthly budget for years to come.

We want you to know that while the rules are strict, your situation is fixable. You are not alone in this, and there is a clear path forward to regain your peace of mind and your health security. We will show you how to navigate the current 2026 enrollment landscape to secure your coverage while minimizing the impact of lifetime penalties. We’ll walk through the General Enrollment Period, explain how to check if you qualify for a Special Enrollment exception, and provide a simple roadmap to get your Medicare Part B and Part D drug coverage back on track.

Key Takeaways

- Identify your personal seven-month window to determine if you are still eligible for standard enrollment or need a new strategy.

- Understand exactly what happens if i miss my initial enrollment period and how 2026 late enrollment penalties for Part B and Part D are applied to your monthly costs.

- Check if a life event, like leaving employer coverage, qualifies you for a Special Enrollment Period to avoid penalties entirely.

- Learn the specific steps to take during the General Enrollment Period so you can secure health coverage as quickly as possible.

- Explore how we act as your advocate to compare Medicare Supplement and Part D plans, helping you find the right fit for your health needs and budget.

What is the Medicare Initial Enrollment Period (IEP)?

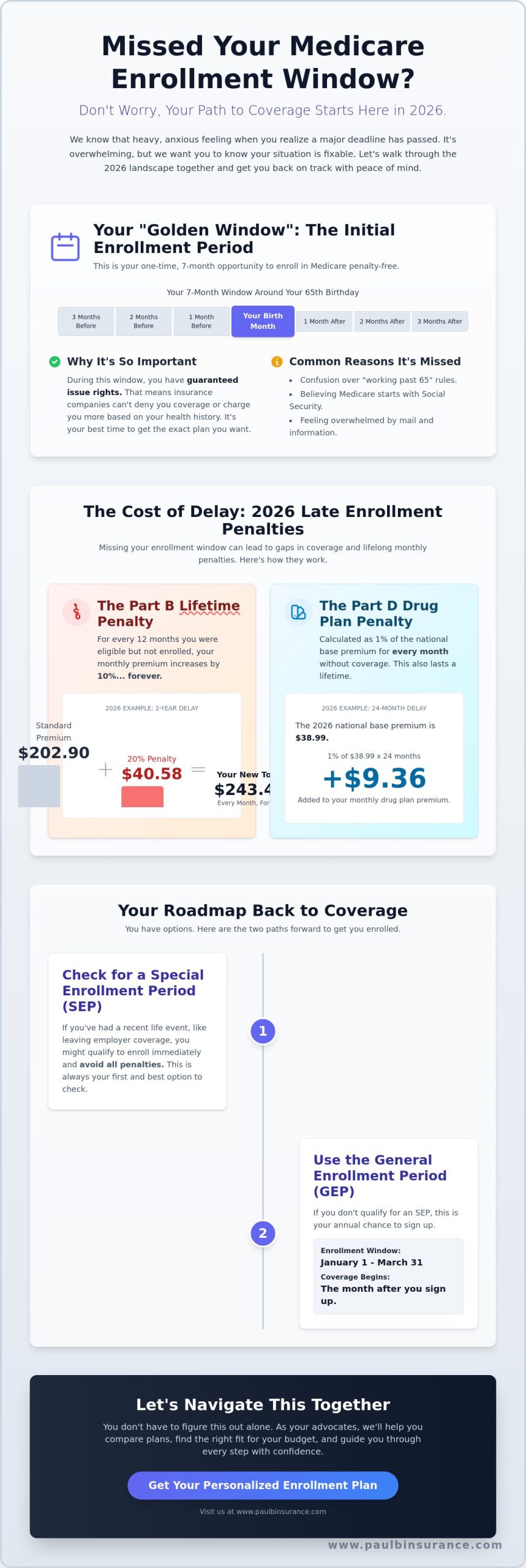

If you turn 65 in 2026, your Initial Enrollment Period is the seven-month window that starts three months before your birth month, includes the month you turn 65, and ends three months later. We consider this timeframe the most critical milestone in your healthcare journey. It is your personal opportunity to join the Medicare program without facing extra costs or coverage delays. If you miss this window, you generally cannot enroll until a specific designated time later in the year, which often leaves people wondering what happens if i miss my initial enrollment period while they wait for a new chance to sign up.

Why the IEP is your ‘Golden Window’

We often refer to these seven months as your “Golden Window” because of the unique protections it provides. During this time, you have guaranteed issue rights, which means insurance companies cannot use medical underwriting to look at your health history. They can’t charge you more or deny you a policy because of a pre-existing condition. You have the total freedom to choose between Original Medicare or various Medicare Advantage plans based on what fits your life best in 2026.

Some people are lucky enough to be enrolled automatically. If you’ve already been receiving Social Security benefits for at least four months before you turn 65, the government usually handles the paperwork for you. However, if you aren’t yet collecting Social Security, you must manually enroll. We’ve seen many people miss their start date simply because they didn’t realize the responsibility to act was on their shoulders.

Common reasons people miss their initial window

It is incredibly easy to let this deadline slip by. Life is busy. Many of our clients tell us they felt completely paralyzed by the sheer volume of mail and conflicting advice they received. When you’re being hit with dozens of brochures every week, it’s natural to want to tune it all out.

One of the biggest hurdles we see is the confusion surrounding “working past 65” rules. You might assume that your employer’s health insurance means you can ignore Medicare for now. While that’s true for some, it depends on the size of your company and whether your coverage is officially “creditable.” Another common trap is the belief that Medicare and Social Security start at the same time. People often wait to sign up for health benefits until they are ready to retire, only to realize later what happens if i miss my initial enrollment period once they see the late enrollment penalties that have been quietly accumulating.

Understanding the Cost of Delay: Late Enrollment Penalties in 2026

Realizing you missed a deadline is stressful enough without the threat of extra costs hanging over your head. We want to help you understand exactly what happens if i miss my initial enrollment period regarding your monthly budget. Beyond the extra fees, the most significant danger is the gap in coverage. If you have a sudden medical emergency while you are waiting for the next enrollment window to open, you could be responsible for the full cost of your care out of your own pocket.

The Part B Lifetime Penalty

The Medicare Part B penalty is particularly frustrating because it is designed to stay with you. It doesn’t disappear after a year or two. For every full 12-month period you were eligible for Part B but didn’t sign up, you’ll face a 10% late enrollment penalty. This amount is added to your monthly premium for as long as you remain in the program.

Let’s look at a concrete example for 2026. The standard Part B premium this year is $202.90 per month. If you waited two full years to enroll, your penalty would be 20%. That means you would pay an extra $40.58 every single month for the rest of your life. This is why waiting just a few more months to see how things go can become a very expensive decision. We see many people who regret delaying because those small monthly additions really add up over a decade of retirement.

The Part D Prescription Drug Penalty

Even if you don’t take any medications right now, skipping Medicare Part D can lead to what we call the 1% rule. Medicare calculates this penalty by taking 1% of the national base beneficiary premium for every month you went without creditable drug coverage. In 2026, that national base premium is $38.99.

If you go 24 months without coverage, you’ll pay an extra 24% of that base premium every month. This amount is rounded to the nearest ten cents and added to your plan’s cost. To avoid this, you must have creditable coverage, which is insurance that is expected to pay at least as much as Medicare’s standard drug plan. If you’re unsure if your current employer or retiree plan counts as creditable, we can help you review your documents to find the answer. It’s much better to have a simple, low-cost drug plan in place now than to pay a penalty forever.

Your Roadmap Back: How to Enroll If You Missed the Deadline

If you are feeling stuck, we want to help you move from a state of worry to a state of action. We have built a clear roadmap to help you understand what happens if i miss my initial enrollment period and, more importantly, how to fix it. This is not a dead end; it is simply a detour. By following a structured path, you can secure the health coverage you need while keeping your future costs as low as possible.

- Step 1: Check for a Special Enrollment Period. This is your first priority. We look for specific life events that allow you to bypass the standard waiting times and penalties.

- Step 2: Mark the General Enrollment Period on your calendar. If you don’t qualify for an exception, this is your annual opportunity to get back into the system.

- Step 3: Collect your records. You will need proof of any “creditable” health insurance you’ve had since turning 65. This includes documents from your employer or a union plan.

- Step 4: Submit your application. You can do this through the Social Security website or by calling their office directly. We recommend the online portal for the fastest processing in 2026.

- Step 5: Partner with an independent expert. Once your basic Medicare is active, we help you compare supplemental options to fill the gaps in your coverage.

The General Enrollment Period (GEP)

If you missed your initial window and don’t have a special circumstance, the General Enrollment Period is your primary solution. This window opens every year from January 1st through March 31st. In 2026, the rules are much more user friendly than they used to be. Your coverage will now begin the first day of the month after you sign up. For example, if you enroll in February, your benefits start on March 1st. This change helps reduce the time you spend without protection, though you may still face the late enrollment penalties we discussed earlier.

Special Enrollment Periods (SEP): The ‘Get Out of Jail Free’ Card

An SEP is a specific timeframe where you can sign up for Medicare without any penalties. The most common reason people qualify is because they stayed at their job past age 65 and had health insurance through their employer. If your company has 20 or more employees, this usually counts as “creditable” coverage. When that job ends or the insurance stops, you have an eight-month window to enroll. Other life events, such as moving to a new state, losing Medicaid eligibility, or leaving a union plan, can also trigger an SEP. We take the time to review your history carefully because finding an SEP is the best way to protect your peace of mind and your wallet.

Choosing the Right Plan After a Late Enrollment

Once your Part A and Part B are finally active, you can breathe a sigh of relief. The hardest part of understanding what happens if i miss my initial enrollment period is over. Now, you have a fresh opportunity to select a private plan that fills the gaps in Original Medicare. Since you are joining later than most, we want to ensure you choose a path that provides the most security without unnecessary hurdles. We’ll help you look at how your current health needs align with the options available in 2026.

Medigap vs. Medicare Advantage for Late Enrollees

Choosing between Medicare Supplement (Medigap) and Medicare Advantage is a major decision for anyone starting late. If you are enrolling during the General Enrollment Period, you might find that “guaranteed issue” rights for Medigap are limited. In many states, this means an insurance company could look at your health history before accepting your application. If you have chronic health concerns, this can make Medigap more difficult or expensive to obtain because you missed that first six-month window where your health didn’t matter.

On the other hand, Medicare Advantage plans in 2026 remain a very accessible option. These plans do not use medical underwriting, so your health history won’t prevent you from joining. Since industry data shows average premiums for these plans are projected to decrease overall this year, they are often the simplest path for those who missed their first chance. We help you look at the provider networks and co-pays to make sure your doctors are included so you don’t face any surprises at the clinic.

Don’t Forget Dental and Vision

We often see people focus so much on their hospital and doctor coverage that they forget about their teeth and eyes. It is a common surprise to learn that Original Medicare doesn’t cover routine cleanings, fillings, or glasses. To protect your savings from unexpected high costs, we suggest exploring dental insurance plans that can be added to your coverage. This ensures you aren’t paying for every checkup out of your own pocket.

Creating a “Total Care” package is about more than just checking a box. It is about ensuring that a simple toothache or a new prescription for glasses doesn’t turn into a financial burden. We can help you bundle these services so your coverage feels complete and your mind is at ease. If you are ready to see which 2026 plans fit your specific needs, contact us today for a personalized plan comparison.

How We Help You Navigate Medicare Enrollment with Confidence

We know that the fear of a permanent penalty can make you feel stuck. When you are wondering what happens if i miss my initial enrollment period, you need more than just a list of rules. You need a partner who can help you take the next step. We act as your personal advocate. This means we don’t represent the insurance companies. Instead, we represent you. Our goal is to protect your health and your budget by finding the most logical path through the 2026 Medicare landscape.

Our planning process is deeply personal. We don’t use a one-size-fits-all approach because your history is unique. We look at your exact birth date, your employment records, and your current health needs. By comparing over 40 different carriers, we can identify which ones are the most flexible for late enrollees. This wide perspective allows us to find options that a restricted representative simply cannot offer. We stay by your side year-round, ensuring you never have to worry about missing another deadline again.

The Value of an Independent Broker

Having choices is the best way to lower your 2026 healthcare costs. As independent brokers, we have access to a vast range of plans that can fit almost any situation. We take pride in explaining the jargon in plain English so you can make an empowered decision without feeling confused. If you are still worried about what happens if i miss my initial enrollment period, we focus on the practical solutions available to you right now. One of the most valuable services we provide is helping you document your “creditable coverage.” If you had insurance through work, we help you gather the right paperwork to show Medicare. This is often the difference between paying a lifetime penalty and having it waived entirely.

Taking the First Step Toward Peace of Mind

We invite you to share your story with us. Often, a simple 15-minute conversation can remove weeks of enrollment stress and replace it with a clear, actionable plan. You don’t have to figure this out alone. We are here to guide you from a state of uncertainty to one of absolute confidence. We’ve helped many people in 2026 turn their Medicare confusion into a secure plan for the future. Let’s fix your Medicare timeline together; contact us today.

Secure Your Health Future with Confidence

Missing a deadline feels heavy, but it does not have to define your retirement. You now have the facts about how penalties work and the steps required to get your coverage started. Understanding what happens if i miss my initial enrollment period is simply the first stage of your journey back to certainty. Whether you use a Special Enrollment Period or the next General Enrollment window, a solution is waiting for you.

We are ready to act as your advocate throughout this process. Our team is licensed in 34+ states and represents 40+ top-rated carriers, giving you the power of choice. We provide this expert guidance at no cost to you, focusing entirely on your specific needs and history. You don’t have to navigate these complex 2026 rules alone.

Get a Personalized Medicare Enrollment Roadmap

You have taken a great first step by learning your options today. Take a deep breath and know that we are here to help you move forward with a clear plan and total peace of mind.

Frequently Asked Questions

Is there a way to waive the Medicare late enrollment penalty?

Yes, you can avoid the penalty if you qualify for a Special Enrollment Period or can prove you had creditable coverage from an employer. If you believe a penalty was applied by mistake, you have the right to file an appeal with Social Security. We often help our clients review their past insurance records to find the documentation needed to challenge these extra costs.

What is considered ‘creditable coverage’ for Medicare Part B?

Creditable coverage for Part B is typically health insurance from a current employer, or a spouse’s current employer, where the company has 20 or more employees. It’s important to know that COBRA and most retiree plans do not count as creditable for Part B purposes. We can help you look at your specific policy to see if it meets the 2026 requirements to prevent penalties.

Can I still get a Medicare Advantage plan if I missed my IEP?

Yes, you can join a Medicare Advantage plan as soon as your Medicare Part A and Part B are active. If you enroll in Part B during the General Enrollment Period, you have a window from January 1 through March 31 to select an Advantage plan. With average 2026 Advantage premiums projected at $14.00, these plans remain a popular way to coordinate your care and lower your out of pocket costs.

How much is the Medicare Part B penalty in 2026?

The penalty is calculated as 10% of the standard monthly premium for every full 12 month period you were eligible but didn’t enroll. In 2026, the standard Part B premium is $202.90. This means each year you waited adds an extra $20.29 to your monthly bill for as long as you have Medicare. We focus on getting you enrolled as quickly as possible to stop this amount from growing further.

What happens if I miss the General Enrollment Period too?

If you miss the March 31 deadline for the General Enrollment Period, you must usually wait until January of the following year to apply again. This creates a dangerous gap where you have no health coverage and your lifetime late enrollment penalty continues to increase. Understanding exactly what happens if i miss my initial enrollment period is vital so you can catch the next available window and protect your health.

Do I have to pay the penalty if I was living outside the U.S.?

Yes, you generally still face the penalty unless you were working in another country and had group health coverage through that employer. Simply living abroad without a specific group work plan does not exempt you from the Part B enrollment rules. We can look at the specific 2026 regulations for international residents with you to see if your situation qualifies for a rare exception.

How do I sign up for Medicare Part B if I missed my initial window?

You can sign up online through the Social Security website or by mailing in the required forms during a valid enrollment window. If you are using a Special Enrollment Period, you must also provide Form CMS-L564, which is signed by your employer to prove you had prior coverage. We can walk you through this paperwork so you don’t have to worry about a technical error delaying your start date.

Will my Social Security benefits be reduced by the penalty?

Yes, your monthly Social Security check will be smaller because Medicare premiums and any associated penalties are deducted automatically. If you aren’t yet receiving Social Security, you will receive a bill for your premiums every three months. We help you calculate these costs ahead of time so you can maintain a clear and predictable budget for your retirement in 2026.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com