Most people shopping for a Medicare Supplement plan spend all their energy comparing monthly premiums. They look at the number, pick the lowest one, and call it a day.

That’s completely understandable. But it’s also one of the most common — and costly — mistakes I see people make.

Here’s why: two people can enroll in the exact same Plan G, with the exact same benefits, paying very different monthly premiums — and the person who paid less at 65 can easily end up paying more by 75 or 80. How your plan is priced at the start determines how it grows over time. And most people have no idea that three completely different pricing systems exist.

After 18+ years of working exclusively in Medicare, I’ve had this conversation thousands of times. This guide is my attempt to finally explain it in plain English — no jargon, no insurance-speak — so you can make a decision that holds up not just this year, but ten or fifteen years from now.

Key Takeaways

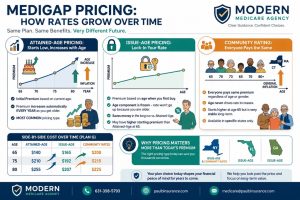

- There are three ways Medigap plans are priced: attained-age, issue-age, and community rating. Most people have never heard of the difference.

- Attained-age is the most common pricing type. It starts low and increases every year as you get older — on top of any general rate increases.

- Issue-age locks in your rate based on how old you are when you buy. Your premium won’t go up just because you’re aging.

- Community rating charges everyone the same price regardless of age. A 65-year-old and an 80-year-old pay the same amount for the same plan.

- Which type is available to you depends almost entirely on the state you live in.

- The cheapest premium at 65 is not always — or even usually — the best long-term value.

Table of Contents

- Why Pricing Type Matters More Than the Number You See

- Attained-Age Pricing: The Most Common — and the Trickiest

- Issue-Age Pricing: Lock In Your Rate When You’re Young

- Community Rating: Everyone Pays the Same

- Side-by-Side: What Each Pricing Type Really Costs Over Time

- Which States Use Which Pricing System?

- The Important Myth to Bust: “Issue-Age Means My Rate Never Goes Up”

- So Which One Is Best?

- What This Means If You’re in New York

- Frequently Asked Questions

Why Pricing Type Matters More Than the Number You See

Let’s say you’re looking at two Plan G quotes. Both cover the exact same benefits. Carrier A is $155 a month. Carrier B is $170 a month.

Most people pick Carrier A without a second thought. And on day one, they’re right — they’re saving $15 a month.

But here’s the question nobody asks: How is each of those premiums calculated, and how will they grow?

If Carrier A is attained-age rated, that $155 will increase automatically every year as you get older — not just because of inflation or rising healthcare costs, but simply because you had another birthday. If Carrier B is issue-age or community rated, the $170 won’t increase based on your age at all.

By the time you’re 75 or 80, the person who “saved” $15 a month at 65 could easily be paying significantly more than the person who started a little higher. The gap tends to widen every year.

This is the conversation most people never have with their agent. Let’s fix that.

Attained-Age Pricing: The Most Common — and the Trickiest

Attained-age pricing is by far the most common type of Medigap pricing across the country. The word “attained” simply means your current age — the age you’ve reached, or attained, right now.

How it works: When you enroll, your premium is based on how old you are at that moment. Every year on your policy anniversary, your premium goes up because you’re now one year older. On top of that, your premium can also go up for inflation and general healthcare cost increases — just like any insurance plan.

So with an attained-age plan, you’re dealing with two separate forces pushing your premium up at the same time: your age, and everything else.

Why it looks attractive at 65: Because you’re starting at the youngest age you’ll ever be on Medicare, your initial premium is the lowest it will ever be under this pricing model. That low starting number is what draws people in.

The long-term reality: Those automatic age-based increases compound over time. A plan that cost $150 a month at 65 could be $200 or more at 75 — and that’s before accounting for any general rate increases the carrier files. By your late 70s and into your 80s, attained-age premiums can become genuinely difficult to manage on a fixed income.

A simple illustration: Imagine you buy an attained-age Plan G at 65 for $140 a month. With modest annual increases of around 5% to 6% (combining the age factor plus inflation), here’s roughly how that can look:

- Age 65: $140/month

- Age 70: $170/month

- Age 75: $210/month

- Age 80: $255/month

That’s an 82% increase over 15 years — on a plan that covers the same exact benefits it always did.

Who attained-age pricing is most common for: Most people in most states, because it’s the default pricing method for the majority of carriers nationwide.

Issue-Age Pricing: Lock In Your Rate When You're Young

Issue-age pricing works on a fundamentally different philosophy. With this model, your premium is set based on how old you are when you first buy the plan — your “issue age” — and it stays tied to that age forever.

How it works: If you enroll at 65 and your rate is $165 a month, you’ll keep paying the rate for a 65-year-old for as long as you have that plan. When you turn 70, 75, or 80, your premium won’t go up because of your age. The age-based component is frozen at the moment you enrolled.

The important nuance: This doesn’t mean your premium never changes. It can still go up due to medical inflation and general healthcare cost increases — the same forces that affect all Medigap plans. What won’t happen is an automatic age-related bump every single year.

Why it costs more upfront: The insurance company knows from day one that they can’t charge you more just because you’re getting older. So they bake more of that long-term exposure into the starting premium. A 65-year-old buying an issue-age plan will typically pay $15 to $30 more per month than an attained-age plan for the same coverage.

The long-term payoff: That higher starting cost tends to look smarter and smarter as the years go by. While your neighbor on an attained-age plan watches their premium climb every birthday, yours only moves when the insurer files a general cost-of-living type increase.

Where it’s available: Issue-age pricing isn’t available everywhere. The states where it’s most commonly offered or required include Arizona, Florida, Georgia, and Missouri. In other states, some carriers may offer it as an option, but it’s not the norm.

Community Rating: Everyone Pays the Same

Community rating is the simplest concept of the three, and in many ways the most consumer-friendly — though it comes with a tradeoff at the starting line.

How it works: Under community rating, every single person enrolled in the same plan from the same carrier in the same area pays the same monthly premium — regardless of age, regardless of gender. A 65-year-old pays the same as a 75-year-old. A 75-year-old pays the same as an 85-year-old. Age is simply not a factor.

Why it’s higher at 65: Because a 65-year-old is being pooled with people who are 70, 75, 80, and older, the starting premium is higher than what an attained-age plan would charge that same 65-year-old. You’re essentially sharing cost responsibility with an older, higher-utilizing group from day one.

Why it becomes the better deal over time: As you age, community rating gets increasingly favorable relative to the alternatives. By 75 or 80, you’re still paying the same rate as a newly enrolled 65-year-old — because that’s how the system works. Meanwhile, someone on an attained-age plan that same age has been absorbing age-based increases for a decade or more.

Premium increases still happen: Community-rated premiums are not frozen forever. They can still rise due to inflation and claims costs — they just can’t rise because of your age. The pool as a whole may see rate adjustments, but everyone in the pool moves together.

Where it’s available: Community rating is required by law in eight to nine states. More on that in a moment.

Side-by-Side: What Each Pricing Type Really Costs Over Time

Here’s the clearest way I know to show how these three pricing types actually play out in real life. Let’s follow two people — Carol and David — both enrolling in Plan G at age 65 in a state where they have a choice.

Carol chooses the attained-age plan at $140/month because it’s the lowest starting price. David chooses the issue-age plan at $165/month — $25 more per month to start.

Here’s how their costs might reasonably compare over time, assuming Carol’s plan increases about 5% to 6% annually (age plus inflation) and David’s increases about 2% to 3% annually (inflation only):

| Age | Carol (Attained-Age) | David (Issue-Age) | Who Pays More? |

|---|---|---|---|

| 65 | $140/month | $165/month | David (+$25) |

| 70 | $170/month | $178/month | David (+$8) |

| 73 | $193/month | $185/month | Carol (+$8) |

| 75 | $210/month | $192/month | Carol (+$18) |

| 80 | $255/month | $207/month | Carol (+$48) |

By around age 72 to 73, the crossover happens and Carol starts paying more every month. By 80, she’s paying nearly $50 more per month than David — for the exact same Plan G benefits. Over the course of a decade after the crossover, that gap can easily add up to thousands of dollars.

Note: These are illustrative figures based on typical rate behavior. Your actual numbers will vary based on your state, your carrier, and market conditions. This is exactly the kind of projection a good independent broker should be able to run for you.

Which States Use Which Pricing System?

This is where it gets very important — because your options are largely determined by where you live.

Community Rating Required (age doesn’t affect your premium): Arkansas, Connecticut, Massachusetts, Maine, Minnesota, New York, Vermont, and Washington require community rating for policyholders 65 and older. Idaho is sometimes included in this list as well depending on the source and plan type.

In these states, every carrier selling Medigap must charge the same premium to all eligible enrollees, regardless of age.

Issue-Age Required or Common: Arizona, Florida, Georgia, and Missouri specifically prohibit attained-age rating — meaning if you live in one of these states, you’re automatically getting issue-age pricing, which is a significant consumer protection most residents don’t even know they have.

Attained-Age (Everyone Else): The remaining states — the majority of the country — default to attained-age pricing. Carriers in these states can offer issue-age or community-rated plans if they choose, but they’re not required to, and most don’t.

The bottom line on states: If you live in New York, Massachusetts, or Washington, you’re already in a community-rated system — which is genuinely good for long-term cost stability, even if it means a higher starting premium. If you live in Florida or Georgia, you’re in an issue-age system. If you live almost anywhere else, you’re likely dealing with attained-age plans, which means long-term rate trajectory should be a major part of your carrier evaluation.

The Important Myth to Bust: "Issue-Age Means My Rate Never Goes Up"

This one comes up constantly, and I want to address it directly.

When people hear “issue-age,” they sometimes assume it means their premium is locked in forever and will never change. That’s not quite right — and believing it can lead to an unpleasant surprise down the road.

What issue-age means is that your premium won’t go up because of your age. The age component is frozen. But insurance carriers can still file general rate increases that apply to everyone in that plan — increases driven by rising healthcare costs, medical inflation, and claims experience. Those can affect issue-age policyholders just like everyone else.

The difference is this: with an attained-age plan, you’re getting hit by two separate forces every year — the age factor and general inflation. With an issue-age plan, you’re only exposed to one — general inflation. That’s a meaningful structural advantage over 15 to 20 years, but it’s not the same as a frozen premium.

Same principle applies to community rating. The whole community can see rate adjustments — they just move together, and age is never the trigger.

So Which One Is Best?

Honest answer: it depends on three things — where you live, how old you are when you enroll, and how long you plan to keep the plan.

If you’re 65 and in good health: The lower starting premium of an attained-age plan can make sense if you’re working with a carrier with a strong history of conservative rate increases. The key is not treating the starting price as the only variable — you also need to know the carrier’s rate increase track record over the past five to ten years. A carrier with a low starting premium and a history of aggressive rate hikes is worse than a carrier with a slightly higher starting premium and stable increases.

If you want the most predictable long-term cost: Issue-age or community rating is the stronger structural choice. Yes, you pay more upfront. But you eliminate the automatic annual age-based escalation, which is what tends to make plans unaffordable in people’s late 70s and 80s.

If you’re enrolling later (say, age 70 or older): Attained-age plans start to look less attractive because you’re already older, meaning your “low starting premium” advantage is smaller and the age-based increases hit harder sooner. Issue-age or community-rated plans — if available in your state — can be a stronger option.

The most important thing I can tell you: The pricing type is one piece of the puzzle. The other piece is the specific carrier’s rate increase history. An issue-age plan with a carrier that has a history of steep general rate increases can still end up costing more than an attained-age plan with a carrier that has managed rates carefully for decades. You need both pieces of information to make a truly informed decision.

This is exactly why I ask every client I work with about their long-term budget goals — not just what’s comfortable today.

What This Means If You're in New York

Since a significant part of my practice is on Long Island and in New York State, I want to address this specifically.

New York is a community-rated state with year-round guaranteed issue. That’s actually a remarkable combination of consumer protections that most states don’t offer.

What it means practically:

- Everyone pays the same premium for the same plan from the same carrier, regardless of age

- You can apply for Medigap coverage at any time of year without needing to pass medical underwriting

- You cannot be turned down for a plan based on your health

The tradeoff: because everyone — including 80-year-olds with significant health needs — is in the same pool, New York’s Medigap premiums are among the highest in the country. The average Plan G in New York in 2026 runs around $354 a month, compared to a national average closer to $180.

But here’s what that high premium buys you: predictability, flexibility, and no fear of being locked into a plan you can’t afford to leave because you developed health conditions. For many New Yorkers, that peace of mind has real dollar value.

Frequently Asked Questions

Which pricing type is most common? Attained-age is by far the most common across the country. Most carriers in most states default to this model. Issue-age and community-rated plans are available in specific states only.

Can I switch from an attained-age plan to a community-rated plan? Potentially, yes — but switching requires medical underwriting in most states outside of specific guaranteed issue windows. If you have significant health conditions, you may not qualify. In New York, you can switch at any time without underwriting. This is why your initial enrollment decision is so critical.

Does the pricing type affect the benefits I receive? No. Medigap plans are federally standardized. A Plan G is a Plan G regardless of whether it’s attained-age, issue-age, or community-rated. The only difference is how your premium is calculated and how it changes over time.

Is community rating always better than attained-age? Not necessarily at 65 — community-rated plans typically start higher for younger enrollees. But over a 15 to 20-year horizon, community rating tends to become increasingly favorable because age never drives your premium up. The longer you keep the plan, the more the math tends to favor community rating.

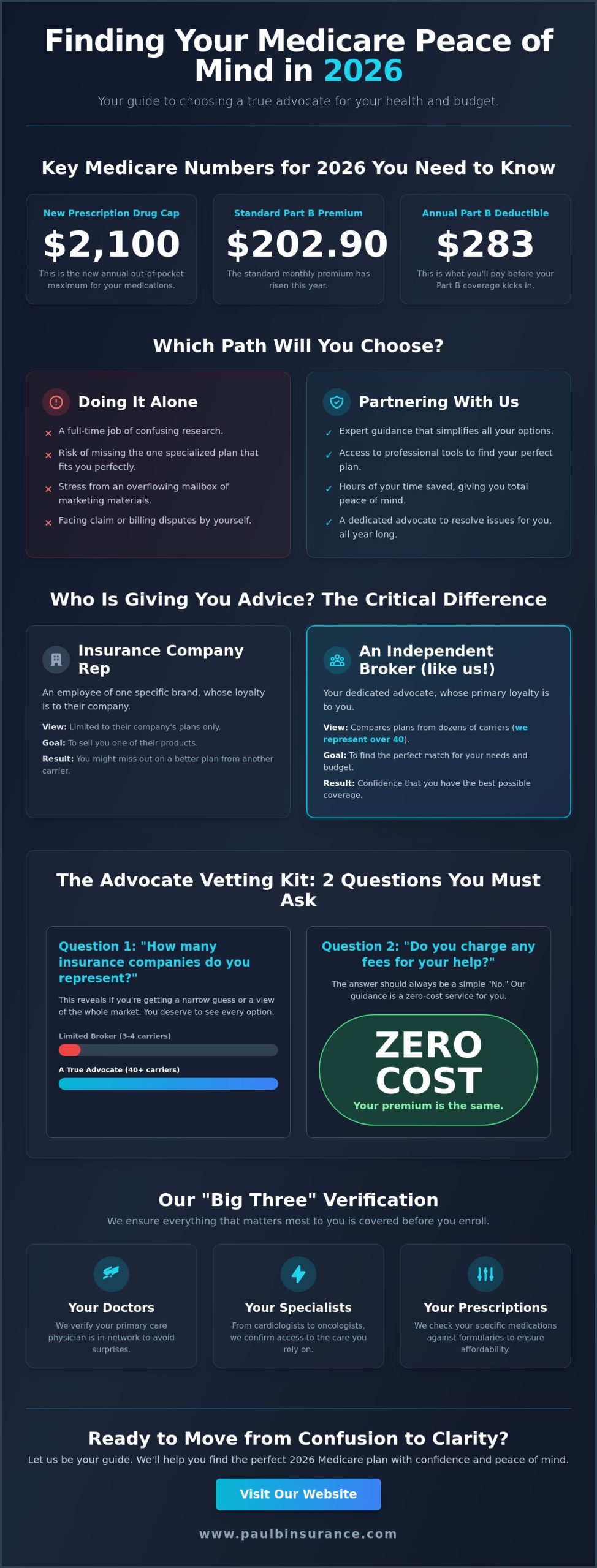

What if I live in a state with only attained-age plans? Focus on two things: the carrier’s rate increase history in your state over the past five to ten years, and the size of their active risk pool. These two factors — more than the starting premium — will determine what your plan costs a decade from now. An independent broker who works with 40+ carriers will have this data.

Why do some states require community rating and others don’t? It’s a state-level regulatory decision. States that require community rating are prioritizing consumer protection and premium stability for older enrollees. States that allow attained-age rating are allowing the free market to price insurance based on actuarial risk. Both approaches have tradeoffs — community rating starts higher for younger enrollees but protects older ones; attained-age starts lower but escalates significantly with age.

How do I find out which pricing type is available in my state? The easiest way is to call an independent Medicare broker who is licensed in your state and works with multiple carriers. In about 15 minutes, they can tell you exactly which pricing types are available to you, run comparison quotes across carriers, and walk you through rate histories so you can make a fully informed decision. And it costs you nothing.

The Bottom Line

The premium you see today is just the starting point. What matters is where that premium goes over the next 15 to 20 years — because that’s how long most people keep their Medigap plan.

Attained-age pricing starts low and climbs with your age, every single year. Issue-age pricing starts a little higher but freezes the age component, so only inflation drives future increases. Community rating puts everyone in the same pool regardless of age, which starts higher at 65 but becomes increasingly favorable as the years go by.

None of these is automatically right or wrong. The right answer depends on where you live, what options are available to you, and which carrier has the most disciplined rate history in your state.

This is exactly the kind of analysis I do with every client I work with — walking through not just what a plan costs today, but what it’s likely to cost five, ten, and fifteen years from now. Because Medicare is a long game, and the decisions you make at 65 ripple forward for decades.

If you’d like a free, no-pressure conversation about which pricing type makes sense for your situation and which carriers have the strongest long-term rate track records in your area, I’m happy to help.

Call 631-358-5793 or visit paulbinsurance.com to schedule your free consultation.

Paul Barrett is the founder and Principal Agent of The Modern Medicare Agency, a Medicare-only independent brokerage based in Melville, NY. With 18+ years of Medicare-exclusive experience, licensure in 34 states, and relationships with 40+ carriers, Paul has helped 5,000+ clients navigate Medicare with clarity and confidence. He is the author of Medicare Mastery Unlocked.