Medicare dental upgrade options explained simply: Original Medicare does not cover routine dental care, which means cleanings, fillings, crowns, and implants come entirely out of your pocket unless you take action to upgrade. For seniors approaching 65 and disabled Medicare beneficiaries, this gap is one of the most expensive surprises in the entire Medicare system. The good news is that three proven paths exist to add real dental coverage: Medicare Advantage plans, standalone dental insurance, and dental savings programs. Each works differently, costs differently, and fits different situations. This article breaks down all three so you can choose with confidence.

What dental services does Original Medicare cover vs. Medicare Advantage dental benefits?

Original Medicare covers dental care only when it is medically necessary during a hospital stay or directly connected to a covered medical procedure. A tooth extraction before heart surgery may qualify. A routine cleaning never does. This distinction catches many new Medicare enrollees completely off guard.

Parts A and B exclude the dental services most people use every year: exams, X-rays, cleanings, fillings, extractions, dentures, and crowns. If you stay on Original Medicare alone, every one of those costs lands on you. For many seniors on fixed incomes, that exposure is significant.

Medicare Advantage plans, also called Part C, are the most common way to fill this gap. 94% of Medicare Advantage plans include some form of dental benefit in 2026, with an average annual coverage cap of about $1,300. That number tells you something important: most plans cover preventive care well, but major work can still leave you with a large bill.

Coverage scope varies widely across plans. Many Medicare Advantage plans cover preventive dental care at 100%, meaning exams, cleanings, and X-rays cost you nothing. Fillings and extractions typically land at 50–80% coverage after a deductible. Major restorative work like crowns, bridges, or implants often sits at the lowest reimbursement tier and eats through annual caps quickly.

Pro Tip: Never rely on a plan’s marketing brochure to understand dental benefits. Pull the Evidence of Coverage (EOC) document and search specifically for “dental” to see exact coverage percentages, annual maximums, and excluded procedures.

You can learn more about what Medicare Advantage plans cover at Paulbinsurance, including how dental benefits vary by carrier and region.

How do standalone dental plans and savings programs work as upgrade options?

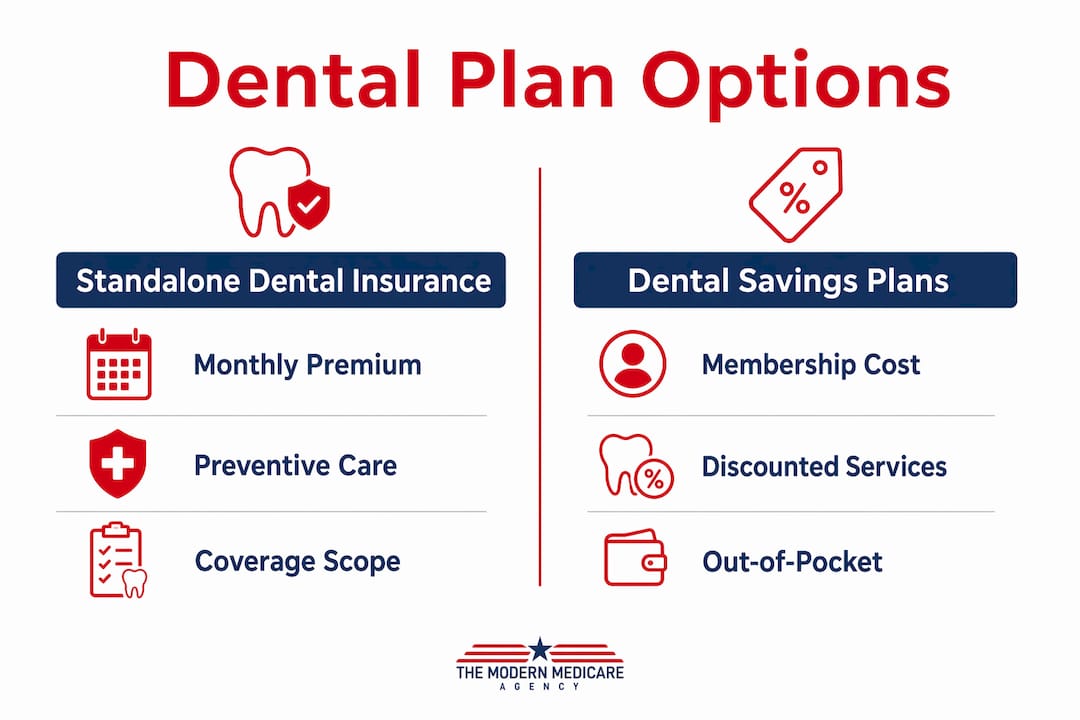

Standalone dental insurance plans operate completely independently of Medicare. You pay a monthly premium, and the plan covers a share of your dental costs according to a tiered structure. Standalone dental insurance typically costs between $20 and $60 per month, while dental savings programs charge an annual fee of $100 to $200 and offer discounts of 10% to 60% on services.

These two options are not the same thing, and the difference matters.

Standalone dental insurance: how it works

Standalone plans follow the same structure as most dental insurance you may have had through an employer. Preventive care is usually covered at 100%. Basic care like fillings runs at 70–80%. Major care like crowns or root canals often comes in at 50%. Most plans carry an annual maximum benefit in the $1,000–$2,000 range, and many impose a waiting period of 6–12 months before covering major procedures.

Standalone plans make the most sense when your Medicare Advantage plan has weak dental benefits, or when you are enrolled in Original Medicare and want structured coverage with predictable cost sharing.

Dental savings plans: a different model entirely

Dental savings plans, sometimes called dental discount plans, are membership programs rather than insurance. You pay an annual fee, receive a membership card, and visit any dentist in the network at a pre-negotiated discount. Dental savings plans have no annual maximums, no waiting periods, and no claim forms. That simplicity makes them practical for immediate needs or procedures that insurance caps out on.

The tradeoff is that you still pay the discounted rate out of pocket. There is no insurer sharing the cost. For someone who needs one crown per year, a savings plan at $150 annually plus a 40% discount may beat a standalone insurance plan with a $480 annual premium and a $1,500 cap.

| Feature | Standalone dental insurance | Dental savings plan |

|---|---|---|

| Monthly cost | $20–$60/month | $8–$17/month (annual fee) |

| Annual maximum | $1,000–$2,000 | None |

| Waiting periods | Often 6–12 months for major work | None |

| Claim forms | Yes | No |

| Best for | Ongoing, predictable dental needs | Major procedures or immediate access |

Pro Tip: If you need a crown or implant within the next 60 days, a dental savings plan gets you discounted care immediately. A standalone insurance plan with a waiting period will not help you in time.

You can also add dental insurance to your existing Medicare coverage by following a straightforward process outlined at Paulbinsurance.

What factors matter most when comparing Medicare dental coverage options?

Choosing the right dental upgrade is not about finding the lowest premium. Experts advise prioritizing total annual cost over monthly premiums when selecting Medicare Advantage dental plans, factoring in deductibles, coinsurance, and benefit maximums. A $0-premium Medicare Advantage plan with a $1,000 dental cap may cost you far more than a plan with a modest premium and a $2,500 cap if you need significant work.

Here are the five factors that should drive your decision:

-

Total annual cost. Add up premiums, deductibles, copays, and your share of covered services. Then compare that number to the plan’s annual maximum benefit. If the math does not work in your favor, the plan is not the right fit.

-

Scope of coverage. Confirm whether the plan covers only preventive care or also includes basic and major services. A plan that covers cleanings but not fillings leaves a real gap.

-

Provider network. Check that your current dentist participates in the plan’s network. Switching dentists to save money on premiums often costs more in convenience and continuity of care.

-

Waiting periods and prior authorization. Some plans require prior authorization before covering crowns or oral surgery. Waiting periods on major care can delay treatment for months.

-

Enrollment timing. During the Annual Enrollment Period, which runs from october 15 to december 7 each year, you can switch Medicare Advantage plans to improve your dental benefits. Missing this window means waiting another full year.

Many seniors mistakenly assume they have dental coverage through their Medicare Advantage plan when they actually have only limited preventive benefits or none at all. Reading the EOC document rather than relying on sales materials is the only way to know for certain what you have.

How to combine dental upgrade options for more complete coverage

No single plan covers everything perfectly. The most cost-effective approach for many seniors combines two or more options to close coverage gaps.

Here is how that works in practice:

-

Pair a Medicare Advantage plan with a dental savings plan. Use your MA plan’s benefits for preventive care and basic work. When you hit the annual cap, your savings plan membership kicks in for discounted rates on the remaining balance.

-

Use dental schools for major procedures. Accredited dental schools like those at New York University, the University of Michigan, and many state universities provide high-quality care at 50–70% below market rates. Combining dental savings programs with dental school services gives seniors affordable access to major procedures that insurance caps leave uncovered.

-

Ask about federally qualified health centers (FQHCs). FQHCs offer sliding-scale dental fees based on income. They serve Medicare and Medicaid patients and are often overlooked by seniors who assume they do not qualify.

-

Negotiate payment plans for major work. Most dental offices will spread large treatment costs over several months with no interest. For major treatments like implants, combining discount programs, dental schools, and negotiated payment plans is often more cost-effective than relying solely on insurance benefits capped annually.

-

Review your EOC every fall. Plan benefits change year to year. A plan that covered crowns at 50% in 2025 may reduce that to 30% in 2026. Reading the Evidence of Coverage document line by line is the only reliable way to catch those changes before they affect your wallet.

You can find a dentist that accepts Medicare coverage through CWD Dental Group’s provider guide, which helps you locate in-network providers by location.

Key takeaways

Upgrading your Medicare dental coverage requires comparing total annual costs, coverage scope, and provider networks across Medicare Advantage plans, standalone insurance, and dental savings programs.

| Point | Details |

|---|---|

| Original Medicare excludes routine dental | Parts A and B cover dental only in medically necessary hospital situations, not cleanings or fillings. |

| Medicare Advantage is the most common upgrade | 94% of plans include some dental, but average caps of $1,300 limit major procedure coverage. |

| Savings plans fill gaps insurance cannot | No waiting periods or annual caps make dental savings programs ideal for immediate or high-cost needs. |

| Total cost beats low premiums | Compare deductibles, coinsurance, and caps together, not just the monthly premium. |

| Combine options for best results | Pairing an MA plan with a savings plan and dental school access covers the widest range of needs. |

Paul’s take on navigating Medicare dental upgrades

I have been helping Medicare consumers since 2007, and dental coverage is the single topic that generates the most frustration. People come to me after they have already had a procedure done, assuming their Medicare Advantage plan covered it, only to find out they owe $1,800 out of pocket. That is a painful and avoidable situation.

Here is what I have learned from working with thousands of beneficiaries. Most people pick a Medicare Advantage plan based on the premium and the brand name. They never open the EOC. They assume that because the plan advertises dental benefits, those benefits are comprehensive. They are almost never comprehensive. Preventive care at 100% sounds great until you need a crown.

My honest advice: treat your dental health as a separate financial planning problem. Ask yourself what dental work you realistically expect in the next 12 months. If you have healthy teeth and just need cleanings, a Medicare Advantage plan with basic dental coverage is probably enough. If you have older crowns, missing teeth, or gum disease, you need a plan with a higher annual cap or a dental savings plan running alongside it.

Preventive dental care covered at 100% by many Medicare Advantage plans can significantly reduce the need for costly restorative procedures down the road. Use those free cleanings. Show up for those exams. The seniors who get the most value from their dental benefits are the ones who use preventive care consistently and plan ahead for major work.

Switching Medicare Advantage plans annually during the enrollment period is one of the most overlooked strategies I see. Plans change their dental benefits every year. Spending 30 minutes comparing plans each October can save you hundreds of dollars in the year ahead.

— Paul

How Paulbinsurance helps you upgrade your Medicare dental coverage

At Paulbinsurance, we specialize in helping seniors and disabled Medicare beneficiaries find the right dental coverage for their specific situation. Our team of independent agents compares Medicare Advantage plans, standalone dental insurance, and savings programs side by side so you see the real numbers before you enroll. Principal agent Paul Barrett has been guiding Medicare consumers through these decisions since 2007, and education always comes first.

If you are approaching 65 or reviewing your current coverage, start by exploring your Medicare Advantage plan options or reviewing the full dental coverage guide for seniors on our site. When you are ready to talk through your specific dental health needs and find a plan that actually covers what you need, our licensed agents are here to help at no cost to you.

FAQ

Does Original Medicare cover dental cleanings?

Original Medicare does not cover routine dental cleanings. Medicare Parts A and B only pay for dental care that is medically necessary during a hospital stay or connected to a covered medical procedure.

What is the average dental benefit cap on Medicare Advantage plans?

The average annual dental coverage cap on Medicare Advantage plans is about $1,300. That amount typically covers preventive care and some basic restorative work, but major procedures like implants or full crowns can exceed it quickly.

Can I have both a Medicare Advantage plan and a standalone dental plan?

Yes, you can enroll in a standalone dental insurance plan or a dental savings program even if you already have a Medicare Advantage plan with dental benefits. The two plans do not conflict, and the combination often provides broader coverage.

When can I switch my Medicare Advantage plan for better dental coverage?

The Annual Enrollment Period runs from october 15 to december 7 each year. During this window, you can switch to a Medicare Advantage plan with stronger dental benefits, and your new coverage begins january 1 of the following year.

Are dental savings plans worth it for seniors on Medicare?

Dental savings plans are worth considering when you need major dental work immediately or when your insurance cap has been reached. With no waiting periods and discounts of 10–60%, they provide real savings on procedures that insurance often covers poorly.