Choosing the most expensive monthly plan isn’t always the safest way to protect your savings here in Suffolk County. We’ve seen many of our neighbors struggle when weighing Medigap Plan G vs HDG in Commack, wondering if the lower monthly premium is worth the higher deductible risk. It’s completely normal to feel a bit of anxiety when you see the 2026 High Deductible Plan G amount sitting at $2,950. You want to lower your monthly expenses, but you don’t want a surprise medical bill to ruin your peace of mind.

We’re here to show you that Medicare doesn’t have to be a source of stress. We’ll help you find the right balance of savings and security for your specific needs. This guide breaks down the math between these two popular options and explains how the $283 Part B deductible fits into the puzzle. We’ll also look at why New York’s rules on excess charges provide an extra layer of protection for you. By the end, you’ll have a clear understanding of your costs and the confidence to choose the plan that fits your life.

Key Takeaways

- We explain the simple difference between predictable monthly costs and taking on a bit more initial responsibility for lower premiums.

- Discover how to calculate your personal break-even point when comparing Medigap Plan G vs HDG in Commack for the 2026 plan year.

- We clarify the 2026 deductible amounts so you can feel confident about your maximum out-of-pocket costs before any bills arrive.

- Learn whether your health habits make you a better fit for the gold standard of Plan G or the long-term savings of the high-deductible option.

- See how a local expert can help you navigate the unique Long Island market to protect your savings from rising premiums.

What Is the Difference Between Medigap Plan G and High Deductible Plan G?

We often find that our neighbors in Suffolk County are looking for two things: security and value. In 2026, the discussion around Medigap Plan G vs HDG in Commack has become the most common conversation we have with clients. Both options fall under the category of Medigap (also called Medicare supplement insurance), which is designed to fill the “gaps” left behind by Original Medicare. While they share the same name, they offer very different experiences for your wallet.

The core similarity between these two plans is the freedom they provide. Whether you choose the standard version or the high-deductible version, you can see any doctor in the United States who accepts Medicare. There are no networks to navigate and no referrals required to see a specialist. This flexibility is why these plans remain the top choices for seniors in our community who want to maintain control over their healthcare journey.

The Standard Plan G Experience

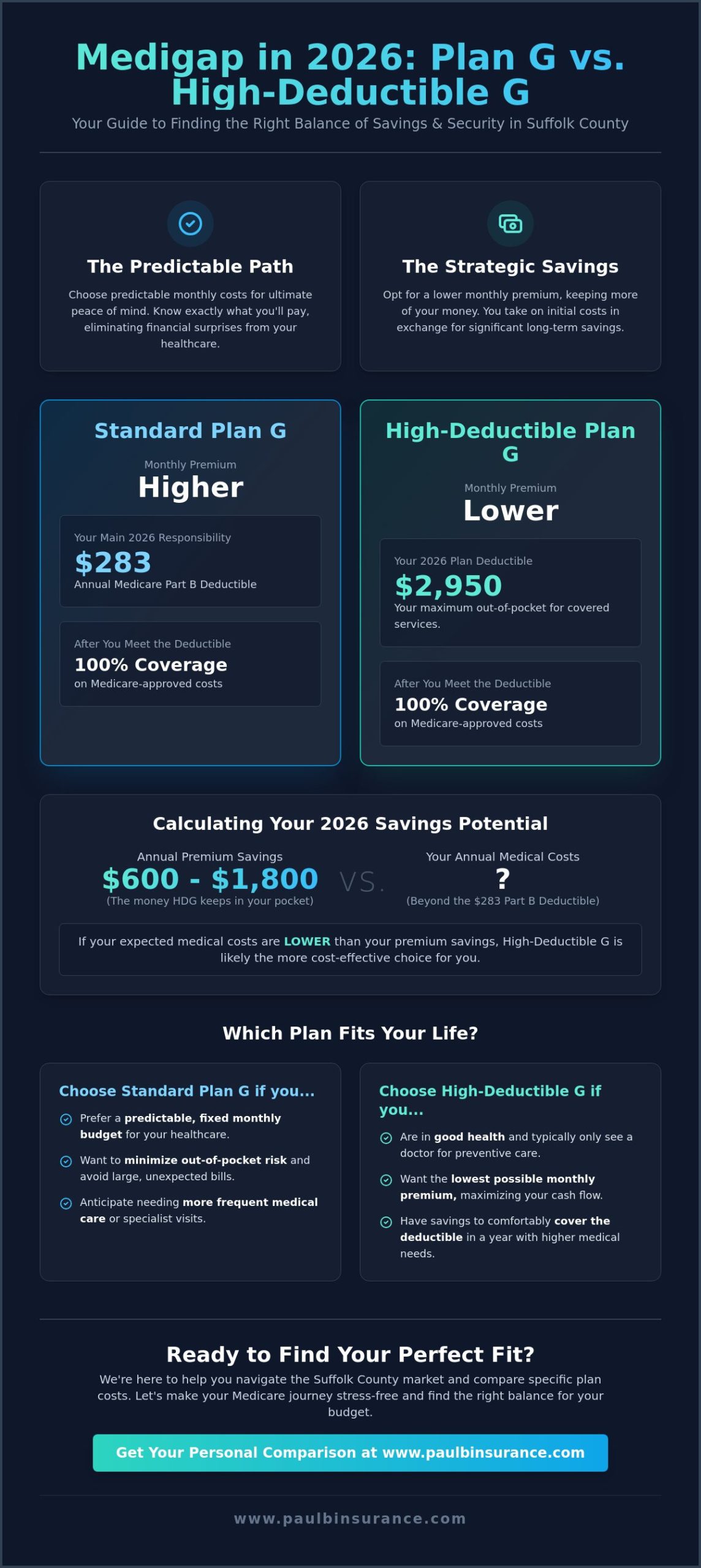

We describe Standard Plan G as the gold standard for comprehensive coverage. It’s designed for people who want to eliminate the “what ifs” from their monthly budget. With this plan, your only major out-of-pocket responsibility for Medicare-covered services is the Part B deductible, which is $283 in 2026. Once you meet that small amount, your Medicare Supplement Plan takes over. It covers 100% of your remaining coinsurance and hospital costs. This predictability is why Plan G replaced Plan F as the most popular choice in New York. It offers peace of mind for those on a fixed income who don’t want to worry about a sudden illness causing a financial crisis.

The High Deductible Plan G Alternative

High Deductible Plan G (HDG) offers the exact same coverage benefits as the standard version, but with a different financial structure. For 2026, the deductible for this plan is $2,950. This means you’re responsible for your medical costs until you’ve paid that amount out-of-pocket. In exchange for taking on this initial cost, your monthly premiums are significantly lower.

It’s a common misconception that you’ll pay full price for services before hitting that deductible. You actually benefit from Medicare’s negotiated rates from day one. You pay the lower, “approved” amount rather than the retail price a provider might charge. This plan acts as a powerful safety net. It protects you from the unlimited 20% coinsurance of Original Medicare while keeping your fixed monthly expenses as low as possible. It’s a strategic choice for those who are currently in good health and prefer to keep their money in their own savings account rather than sending it to an insurance company every month.

2026 Cost Comparison: Premiums vs. Out-of-Pocket Risks

We know that living on Long Island comes with a unique set of financial realities. When we look at the costs for Medigap Plan G vs HDG in Commack, the premium gap is often wider than what you might see in national averages. This is because our local healthcare market is one of the most expensive in the country. In 2026, many of our neighbors are finding that the monthly savings between these two plans can be substantial, sometimes reaching over $100 per month depending on the carrier. Choosing between them requires a clear look at your “fixed” costs versus your “variable” risks.

Standard Plan G represents a fixed cost. You pay a higher premium every month regardless of whether you visit a doctor once or fifty times. HDG represents a variable cost. You pay a much lower premium, but you agree to pay for your own care until you hit the $2,950 deductible. To make an informed choice, you should read What You Should Know About Medigap Plan G to understand how these financial trade-offs impact your long-term retirement budget. If you’re feeling stuck on the math, we can help you compare these specific plan costs side-by-side to see which one fits your budget.

Monthly Savings vs. Annual Deductible

In Suffolk County, the annual savings on premiums for HDG can range from $600 to $1,800 compared to the standard version. We often see healthy clients choose the high-deductible route because they would rather keep that money in their own savings account than give it to an insurance company. A typical Commack senior finds that HDG is the more affordable path unless they have enough medical visits in a single year to completely exhaust the premium savings they’ve kept in their pocket. It’s a simple calculation of how much you are willing to “self-insure” in exchange for a lower monthly bill.

The Role of the Part B Deductible in 2026

The Part B deductible for 2026 is $283. This amount is the first thing you pay under either plan. If you have standard Plan G, this is usually your only out-of-pocket cost for the year. If you have HDG, that $283 counts toward your larger $2,950 deductible. We always tell our clients to take the money they save on HDG premiums and put it into a dedicated “medical emergency” account. This way, if you do have a year with more doctor visits, the money is already there to cover the 2026 Medicare cost adjustments without causing any financial stress. Planning ahead like this turns a potential risk into a manageable strategy.

Is High Deductible Plan G Too Risky for You?

Many of our neighbors in Suffolk County ask us the same scary question: “What if I choose the high-deductible plan and end up needing a major surgery in February?” It’s a valid concern that can cause a lot of late-night worry. We understand the anxiety that comes with seeing a $2,950 deductible on paper. When we help you weigh Medigap Plan G vs HDG in Commack, we look at risk through a different lens. The real risk isn’t the deductible itself. The real risk is the unlimited 20% coinsurance you would face if you stayed with Original Medicare alone.

We believe that peace of mind comes from knowing exactly where your financial responsibility ends. For some, that means choosing Standard Plan G. It feels like “pre-paying” your healthcare so you never have to think about a bill again. For others, it means keeping their premium dollars in their own pocket and only paying the deductible if a medical need actually arises. We’re here to help you evaluate your “Health Risk IQ” so you can decide which path feels most supportive of your lifestyle.

Visualizing Your Worst-Case Scenario

Think of High Deductible Plan G as a stop-loss strategy for your retirement savings. If you have a major health event in 2026, Original Medicare has no cap on what you might owe for doctor services or outpatient care. One long hospital stay or a series of specialist visits could easily exceed $2,950 in 20% coinsurance costs. According to the official Medicare website, Medigap policies are standardized to ensure you have a clear limit on your spending. You can learn more about how Medigap protects you by looking at how these plans act as a ceiling for your medical bills. Once you hit that 2026 deductible, the insurance company takes over the rest.

When the “Risk” Isn’t Really a Risk

If you are a healthy senior who rarely visits a specialist, the high-deductible option often becomes the clear winner. We see many clients use the substantial money they save on monthly premiums to fund other areas of their health. You could use those extra savings to pay for a dental insurance plan or to cover your Part D prescription costs. This approach allows you to control your cash flow rather than giving it to an insurance carrier every month.

Confidence in your choice comes from understanding the numbers, not fearing them. If you prefer the security of knowing your only cost is the $283 Part B deductible, then Standard Plan G is your best fit. If you would rather keep your money and only pay for care when you use it, HDG is a very safe alternative. We’ll walk you through both scenarios so you can see which one lets you sleep better at night.

Who Should Choose Plan G vs. High Deductible Plan G?

Choosing between Medigap Plan G vs HDG in Commack isn’t just a math problem. It’s a choice about how you want to live your daily life. We’ve found that the right plan usually depends on your personal comfort level with uncertainty. Some people want to know their costs to the penny. Others prefer to keep their cash and only pay when they actually use medical services. Your three to five year health outlook is a great place to start your decision process. If you expect a knee replacement or regular specialist visits soon, your needs will differ from someone who only sees a doctor for an annual checkup.

We also encourage you to look at your total healthcare budget, including your prescriptions. While Medigap doesn’t cover your medications, the money you save on a high-deductible premium can be redirected toward your Part D costs. It’s about looking at the big picture of your 2026 expenses. We want you to feel empowered by your choice, not restricted by it. Whether you are a high utilizer or a value seeker, there is a strategy that fits your lifestyle.

Scenario A: You Value Predictability Above All

If you visit the doctor frequently, the standard Plan G is likely your best fit. We call this the high utilizer profile. You might have a chronic condition that requires regular specialist visits or physical therapy. With this plan, you get a “no-bill” experience. You pay your $283 Part B deductible for the year, and that’s it. It’s simple and clean. Many of our Commack neighbors love this because it removes the stress of opening the mail. If you’re also considering other low-premium options, you can compare Medigap to Medicare Advantage to see how they differ in coverage style.

Scenario B: You Want to Keep Your Money in Your Pocket

The value seeker profile is perfect for High Deductible Plan G. These are often our neighbors who are active, healthy, and rarely see a doctor. They treat the $2,950 deductible as a self-insurance fund. They know that even in a bad year, they’ve saved so much on premiums over a ten year period that they’re still ahead financially. It’s the independent thinker’s plan. You keep your money in your own pocket instead of the insurance company’s vault. This plan offers the same medical freedom as the standard version without the high monthly “entry fee.” If you’re ready to see the numbers for your specific age, we can help you request a personalized Medigap quote today to see the exact savings available in Suffolk County.

Finding the Right Medicare Path in Commack with a Local Expert

We know that the stack of mail on your kitchen counter in Commack can feel overwhelming. Navigating the choice between Medigap Plan G vs HDG in Commack shouldn’t feel like a solo mission through a maze. We’ve spent years helping our neighbors move from a state of distress to one of absolute certainty. In 2026, with shifting deductibles and new premium rates, having a steady hand to guide you is more important than ever. Our mission is to serve as your dedicated advocate, removing the stress from a process that should be about your protection and comfort.

A generic call center representative is often restricted to a few limited options. They don’t know the Long Island market, and they certainly don’t know your personal story. We take a different path. Our approach is to listen first, ensuring we understand your health needs and budget before we ever suggest a specific plan letter. We are independent experts who prioritize your needs over high-pressure tactics. We want you to feel empowered by your decision, knowing you have a local professional to call whenever a question arises.

Why a Local Suffolk County Agent Matters

Local knowledge changes everything when it comes to your healthcare. We know that if you see doctors at St. Catherine of Siena or Huntington Hospital, you want a plan that is accepted without any hurdles. The New York Medicare market has its own unique quirks, especially regarding how plans are priced and how regulations protect you from excess charges. We understand these specific pressures of the Suffolk County economy. You can learn more about why a Medicare broker is your best advocate in this complex environment. We are here to help you navigate the 2026 plan changes with clarity and ease.

Take the Next Step Toward Peace of Mind

Getting a personalized comparison shouldn’t be a high-pressure event. We promise to provide clear, honest answers without the scripts or sales tactics you might find elsewhere. We’ll look at your specific zip code and your current health status to show you the real-world impact of choosing Standard Plan G versus the high-deductible option. Our goal is to remove the anxiety from this process so you can focus on enjoying your retirement years.

If you’re ready for a conversation that truly prioritizes your needs, we invite you to reach out. We’ll help you find the path that leads to long-term security and true peace of mind. Please schedule your simple Medicare review with us today. Together, we can make sure your 2026 coverage is exactly what you need it to be.

Secure Your Medicare Future Today

We’ve explored how the choice between Medigap Plan G vs HDG in Commack ultimately comes down to your personal comfort with monthly costs versus out-of-pocket responsibility. Whether you prefer the absolute predictability of standard Plan G or the long-term savings potential of the high-deductible version, the most important thing is that you feel protected. You don’t have to make this decision based on guesswork or confusing mailers.

Paul Barrett and our dedicated team are here to provide the local Suffolk County expertise you deserve. As an independent broker working with over 40 carriers, we offer the impartial support needed to find your perfect fit. We’ll help you look at the 2026 numbers for your specific zip code and health profile. Our goal is to move you from uncertainty to a state of complete confidence.

Get your free, simple comparison of Plan G and HDG today. We’re ready to listen to your needs and help you protect your retirement savings with a plan you can trust. You’ve worked hard for your retirement, and we’re here to help you enjoy it with total peace of mind.

Frequently Asked Questions

Is High Deductible Plan G available in Commack, NY for 2026?

Yes, High Deductible Plan G is widely available in Commack for the 2026 plan year. Because Medigap plans are standardized by the government, any insurance company offering supplements in New York can choose to include this high-deductible option in their portfolio. We can help you compare the different carriers serving Suffolk County to find the one that fits your specific budget and needs.

Can I switch from High Deductible Plan G to standard Plan G later if my health changes?

You can absolutely switch between these plans in New York without worrying about your health history. Our state has unique rules that allow you to change your Medigap coverage at any time of the year. This means if you start with HDG and find your health needs increasing, we can help you move to the standard Plan G without any medical questions or health screenings.

Does Plan G or HDG cover my prescription drugs in Suffolk County?

Neither Plan G nor HDG includes coverage for your prescription drugs. Medigap is strictly designed to cover the “gaps” in Medicare Part A and Part B, such as hospital stays and doctor visits. To protect yourself from high pharmacy costs in Suffolk County, you will need to enroll in a separate Medicare Part D plan. We can help you find a drug plan that covers your specific medications.

What is the actual deductible for High Deductible Plan G in 2026?

The verified deductible for High Deductible Plan G in 2026 is $2,950. This is the total amount you must pay out-of-pocket for Medicare-covered services before the plan begins to pay 100 percent of your costs. It is important to remember that the $283 Part B deductible counts toward this $2,950 limit, so you are not paying two separate deductibles on top of each other.

Will my Commack-based doctors accept both Plan G and High Deductible Plan G?

Your Commack-based doctors will accept both plans equally because they do not use separate provider networks. As long as your physician or specialist accepts Original Medicare, they will accept any Medigap plan, regardless of whether it is the standard or high-deductible version. This includes local specialists and major facilities like St. Catherine of Siena and Huntington Hospital that serve our community.

How much can I expect to save on monthly premiums with HDG in New York?

You can typically expect to save between $600 and $1,800 per year by choosing the high-deductible route. When weighing Medigap Plan G vs HDG in Commack, these monthly savings are often enough to cover a significant portion of the deductible itself. Many of our neighbors find that if they have a healthy year, that extra money stays right in their own savings account.

Does either plan cover dental or vision care for Long Island seniors?

No, these plans do not cover routine dental, vision, or hearing care for Long Island seniors. Medigap is focused on medical expenses like surgery and hospitalizations. However, we do offer separate dental insurance plans that can be added to your coverage. This ensures you have protection for your teeth and eyes while your Medigap plan handles your major medical needs.

What happens if I cannot meet the high deductible in a year with many medical bills?

If you have a year with many medical bills, you are responsible for all Medicare-approved costs until you reach the $2,950 limit. After you hit that amount, the plan pays for everything else. This is why we suggest setting aside your monthly premium savings into a dedicated account. If the thought of a $2,950 bill causes you stress, the standard Plan G is the better choice.