Medicare Supplement insurance, formally known as Medigap, is defined as private health coverage that fills the cost gaps left by Original Medicare Parts A and B. When you compare Medicare supplement plans, the core question is always the same: how much of your out-of-pocket exposure do you want to eliminate, and at what monthly premium? Nationally, plans are lettered A through N and standardized by the federal government. Massachusetts operates under its own rules entirely, offering two unique plan types with pricing protections that most states do not provide. Understanding those differences is the first step toward making a confident coverage decision.

What are the different Medicare Supplement plan types?

The federal system organizes Medigap into lettered plans ranging from Plan A through Plan N. Each letter represents a specific combination of benefits, and those benefits are identical across every carrier that sells that letter. Plan G, for example, covers Part A coinsurance, Part B coinsurance, the Part A deductible, skilled nursing facility coinsurance, and foreign travel emergency care. Plan A covers only the most basic benefits. The letter tells you exactly what you get, regardless of which insurance company you buy it from.

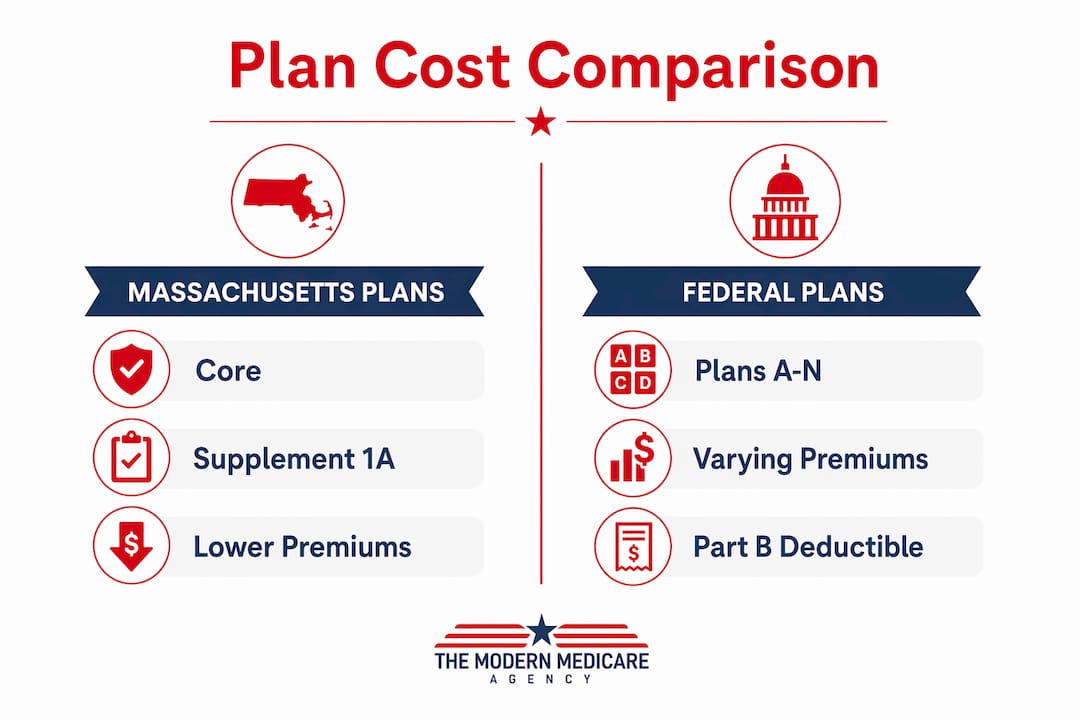

Massachusetts does not follow the federal lettering system. Massachusetts offers two unique plans: Core and Supplement 1A. The Core plan covers basic Medicare gaps in a way similar to federal Plan A, making it the lower-cost entry point. Supplement 1A is more comprehensive, covering Part A and Part B coinsurance, the Part A deductible, and skilled nursing facility costs, but it does not cover the annual Part B deductible. That distinction matters when you are budgeting for the year.

The table below shows how the two Massachusetts plans compare on key benefit categories.

| Benefit | Core plan | Supplement 1A |

|---|---|---|

| Part A hospital coinsurance | Covered | Covered |

| Part B coinsurance | Covered | Covered |

| Part A deductible | Not covered | Covered |

| Skilled nursing facility coinsurance | Not covered | Covered |

| Part B deductible | Not covered | Not covered |

| Foreign travel emergency | Not covered | Covered (80%) |

One detail that surprises many people: Medigap plans do not cover prescription drugs. You need a separate Medicare Part D plan for drug coverage. This applies to both Massachusetts plans and all federal lettered plans. Knowing this upfront prevents a costly assumption.

Pro Tip: If you are new to Medicare in Massachusetts, do not search for Plan G or Plan F. Those federal letters do not exist here. Ask specifically about Core and Supplement 1A to get accurate quotes.

How do costs vary among Medicare Supplement plans?

Premium pricing is where Massachusetts beneficiaries hold a significant advantage over most of the country. Massachusetts mandates community rating, meaning every insurer must charge the same premium for a given plan regardless of your age or health history. A 65-year-old and a 78-year-old pay the same rate for the same plan from the same carrier. That is not the case in most other states, where attained-age rating causes premiums to climb steadily as you get older.

Supplement 1A premiums average around $240 per month, with a typical range of $212 to $270 depending on the carrier. That spread exists because while the benefits are identical across all carriers, insurers compete on price, financial strength, and customer service. The Core plan carries a lower monthly premium, reflecting its narrower benefit set.

Several factors influence which carrier offers you the best long-term value:

- Premium stability: Some carriers raise rates more aggressively than others over time, even under community rating rules.

- Financial strength ratings: A carrier rated A or higher by AM Best is less likely to exit the market or face claims-paying problems.

- Customer service reputation: Claim processing speed and member support quality vary widely between insurers.

- Household discounts: Some carriers offer a discount when two people in the same household both hold policies.

Pro Tip: Get quotes from at least three carriers for the same plan type. The benefits are identical, so the only rational reason to pay more is a demonstrably better service record or stronger financial rating.

One often-overlooked cost factor is the Part B deductible, which neither Massachusetts plan covers. In 2026, that deductible is a fixed annual amount you pay before Part B benefits kick in. Factor it into your total annual cost estimate when comparing Core versus Supplement 1A.

When and how can you enroll in or switch Medicare Supplement plans?

Nationally, the Medigap Open Enrollment Period begins the month you turn 65 and are enrolled in Medicare Part B. This six-month window is the only time federal law guarantees you the right to buy any Medigap plan without medical underwriting. Miss it, and insurers in most states can deny coverage or charge higher premiums based on your health history. That denial risk is real and common.

Massachusetts removes that risk entirely. The state allows continuous open enrollment, meaning you can enroll in or switch between Core and Supplement 1A any month of the year. Coverage takes effect the following month. No medical underwriting applies. This is one of the most beneficiary-friendly policies in the country, and it gives Massachusetts residents a flexibility that most Americans simply do not have.

Here is how to use that flexibility without making costly mistakes:

- Compare your current plan annually. Premiums can change each year. What was the best price last year may not be this year.

- Switch before a major procedure if possible. If you are on Core and anticipate a hospital stay, switching to Supplement 1A before the procedure eliminates the Part A deductible.

- Confirm the effective date. Switching mid-month means your new plan starts the first of the following month. Time your switch to avoid a gap in coverage.

- Keep your Part D plan separate. Switching your Medigap plan does not affect your drug coverage. Manage them independently.

For beneficiaries outside Massachusetts, the stakes around enrollment timing are much higher. Waiting to enroll past the initial open enrollment window can result in permanent premium surcharges or outright denial. If you live outside a protected state, treat the six-month window as a hard deadline.

What tools and resources help you compare Medicare Supplement plans?

Accurate plan comparison starts with local data. Plan availability varies by ZIP code, and a carrier active in one county may not participate in another. Relying on generalized advice or national averages leads to inaccurate cost estimates.

The most reliable resources for a Medicare supplement plans comparison include:

- Medicare.gov: The official plan finder tool lets you search by ZIP code and see which carriers offer plans in your area, along with current premium data.

- State Health Insurance Assistance Programs (SHIPs): Every state has a SHIP office staffed by trained counselors who provide free, unbiased guidance. In Massachusetts, the program is called SHINE (Serving Health Insurance Needs of Everyone).

- Independent licensed agents: An agent who works with multiple carriers can pull quotes across the market and explain differences in carrier financial ratings and service records.

- AM Best and NAIC: These organizations publish financial strength ratings and complaint ratios for insurers, giving you an objective measure of carrier quality beyond the premium.

“Beneficiaries should always verify plan availability and carrier participation locally rather than rely on generalized advice.” — U.S. News Health

When you compare Medicare supplement insurance quotes, line them up on the same plan type. Comparing a Core plan from one carrier against a Supplement 1A from another tells you nothing useful. Same plan, different carriers, same benefit year. That is the only apples-to-apples comparison that holds up.

For beneficiaries weighing Medigap against Medicare Advantage, the tradeoffs between plan types are significant and worth reviewing before committing to either path.

Key takeaways

Choosing the right Medicare Supplement plan requires matching your coverage needs, budget, and state-specific rules before you sign anything.

| Point | Details |

|---|---|

| Massachusetts uses unique plans | Core and Supplement 1A replace the federal A-N lettered plans for Massachusetts residents. |

| Community rating protects your premium | Massachusetts law prevents insurers from charging more based on your age or health. |

| Supplement 1A costs more but covers more | Average premiums run $212–$270 monthly, covering the Part A deductible that Core excludes. |

| Continuous enrollment is a major advantage | Massachusetts residents can switch plans any month without medical underwriting. |

| Drug coverage is always separate | No Medigap plan covers prescriptions; a standalone Part D plan is required. |

What I have learned after years of helping Massachusetts Medicare beneficiaries

Most people walk into a Medicare Supplement conversation thinking the hardest part is picking a plan letter. In Massachusetts, there are no plan letters. That confusion alone causes people to delay enrollment, ask the wrong questions, and sometimes end up in plans that do not fit their actual needs.

The continuous open enrollment rule in Massachusetts is genuinely powerful, but I have seen people misuse it. They assume they can always switch later, so they start with Core to save money and never revisit the decision. Then a hospitalization hits, and they absorb a deductible they could have avoided. The right move is to review your plan every fall, the same way you review your Part D coverage.

The other mistake I see constantly is choosing a carrier based on premium alone. Two carriers can offer Supplement 1A at $215 and $255 per month. The $40 difference feels significant. But if the cheaper carrier has a poor claims processing record or a history of aggressive rate increases, you pay for that in frustration and eventual premium shock. Financial strength ratings from AM Best exist for a reason. Use them.

My honest advice: treat this decision like hiring a contractor. Price matters, but reputation and reliability matter more over a multi-year relationship. And if you are outside Massachusetts, do not wait on enrollment. The protections that make shopping easy here do not exist in most other states.

— Paul

How Paulbinsurance helps you find the right Medicare Supplement plan

Sorting through plan options, carrier ratings, and state-specific rules takes time that most people do not have. Paulbinsurance has been helping Medicare beneficiaries make these decisions since 2007, and the team works as independent agents, meaning no loyalty to any single carrier.

Whether you are enrolling for the first time or reconsidering your current coverage, the licensed agents at Paulbinsurance can pull quotes across multiple carriers, explain the difference between Core and Supplement 1A in plain language, and help you maximize your healthcare savings without overpaying for benefits you do not need. If you are also sorting out drug coverage, the Medicare Part D guide on the site walks through that decision separately. Reach out to the Paulbinsurance team directly to get a personalized plan comparison built around your specific situation.

FAQ

What is a Medicare Supplement plan?

A Medicare Supplement plan, also called Medigap, is private insurance that pays costs Original Medicare does not cover, such as deductibles, coinsurance, and copayments. It does not replace Medicare; it works alongside it.

Does Massachusetts use the same Medigap plans as other states?

No. Massachusetts offers two unique plans called Core and Supplement 1A instead of the federal A-N lettered plans. Both use community-rated pricing, so premiums do not increase based on age or health.

Can I switch Medicare Supplement plans at any time in Massachusetts?

Yes. Massachusetts allows continuous open enrollment, so you can switch plans any month without medical underwriting, with coverage starting the following month.

Do Medicare Supplement plans cover prescription drugs?

No. Medigap plans do not cover prescription drugs. You need a separate Medicare Part D plan for drug coverage, regardless of which Medigap plan you hold.

How do I find the best price on a Medicare Supplement plan?

Get quotes from multiple carriers for the same plan type in your ZIP code, then compare premiums alongside AM Best financial strength ratings and NAIC complaint ratios. An independent agent can pull this data across the market at no cost to you.