What if missing a single deadline in 2026 meant paying a higher price for your healthcare every month for the rest of your life? It’s a heavy thought, and we know how much stress these complex windows can cause. You shouldn’t have to feel like you’re walking a tightrope just to get the medical coverage you deserve. We understand the confusion surrounding medicare initial enrollment vs general enrollment, and we’re here to act as your calm, patient guide through the process.

We’ve created this guide to help you protect your future and your wallet. You’ll learn exactly when your first chance to join begins and what happens if you need to use your yearly second chance. We’ll also break down 2026 costs, like the $202.90 standard Part B premium, so you can plan with total confidence. By the end of this article, you’ll have a clear timeline and the peace of mind that comes from making an informed, secure choice for your health.

Key Takeaways

- Discover the specific seven-month window surrounding your 65th birthday and why the first three months are the most critical for seamless care.

- Understand the fixed dates for the 2026 General Enrollment Period and how it serves as a vital yearly safety net for your health coverage.

- We clarify the differences between medicare initial enrollment vs general enrollment to help you secure the best possible start date for your benefits.

- Learn how to avoid lifelong financial penalties by choosing the right window and protecting your savings from unnecessary premium increases.

- Explore how we advocate for you by comparing options like Medicare Supplement and Part D plans to find the perfect fit for your unique needs.

Understanding Medicare Enrollment: The Difference Between Your First and Second Chance

We know that staring at a calendar full of deadlines can feel overwhelming. It’s perfectly normal to feel a bit of anxiety when you’re trying to get these dates right. Our mission is to take that weight off your shoulders. Think of us as your patient guides on this journey. We’ll help you move from a place of uncertainty to a state of total peace of mind. To start, we need to look at the two most important windows you’ll encounter: your first chance to join and your backup plan. Understanding the nuances of medicare initial enrollment vs general enrollment is the first step toward protecting your health and your hard-earned savings.

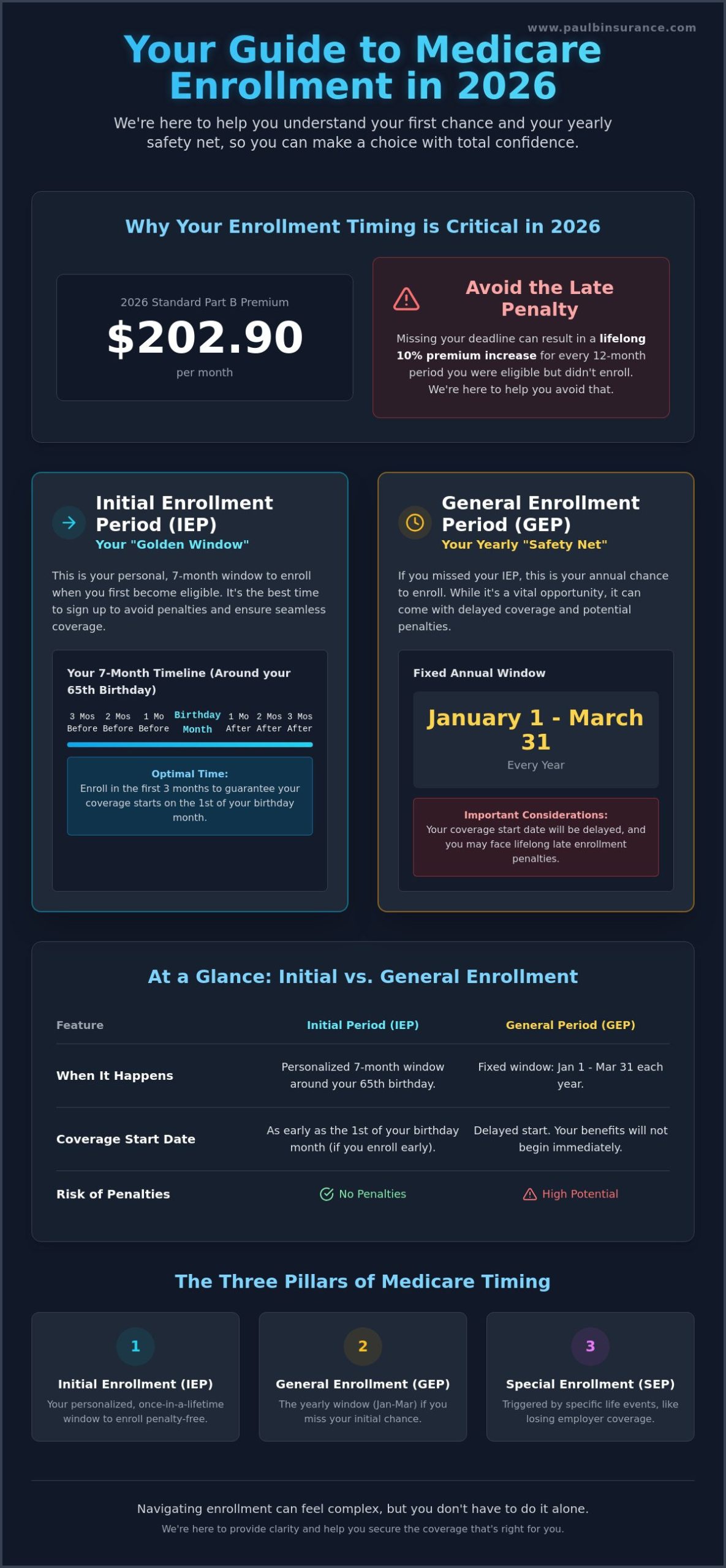

We often call the Initial Enrollment Period (IEP) your “Golden Window.” This is a seven-month period centered around your 65th birthday. It’s your primary opportunity to sign up for Medicare without any hurdles or health questions. On the other hand, the General Enrollment Period (GEP) is your annual “safety net.” It’s there for those who missed their first chance for one reason or another. While the GEP is a vital second chance, it often comes with higher costs and fewer choices. We’re here to make sure you understand the difference so you can choose the path that offers the most security.

Why Timing Matters for Your 2026 Coverage

Many people believe that Medicare begins automatically the moment they turn 65. Unfortunately, that isn’t always the case. If you aren’t already receiving Social Security benefits, you’ll likely need to take action yourself. Missing your window isn’t just a paperwork headache; it has real financial consequences. For instance, the Part B late enrollment penalty is a permanent 10% increase in your premium for every full 12-month period you were eligible but didn’t sign up. In 2026, with the standard Part B premium at $202.90, those extra costs can add up quickly. We want to help you avoid these lifelong penalties entirely.

The Three Pillars of Medicare Timing

To understand the full picture of Medicare (United States), it helps to view enrollment as having three main “doors.” This guide focuses specifically on the “vs” between the first two for Part A and Part B coverage:

- Initial Enrollment Period (IEP): Your personalized seven-month window for first-time eligibility.

- General Enrollment Period (GEP): The yearly window from January 1 to March 31 for those who missed their IEP.

- Special Enrollment Periods (SEP): Specific windows triggered by life events, like losing employer coverage.

By focusing on these dates now, you’re ensuring that your transition into Medicare is smooth and stress-free. If you’re worried about which window applies to you, don’t worry. We’re here to help you calculate your dates and explore options like Medicare Supplement (Medigap) Plans to ensure you have the most robust coverage possible.

The Initial Enrollment Period (IEP): Your First Opportunity

Your Initial Enrollment Period (IEP) is the most significant milestone in your Medicare journey. It’s a personalized seven-month window that revolves entirely around your 65th birthday. This window includes the three months before you turn 65, your birthday month, and the three months that follow. We always recommend signing up during the first three months of this window. Doing so ensures your coverage begins on the very first day of your birthday month, leaving no room for medical bills to slip through the cracks. When comparing medicare initial enrollment vs general enrollment, the IEP is clearly the superior choice because it offers the most flexibility without the threat of late enrollment penalties.

There is a unique exception we often help clients manage called the “First Day Rule.” If your birthday happens to fall on the first of any month, Medicare treats you as if you turned 65 the month before. For example, a June 1st birthday means your coverage can actually start on May 1st. This shifts your entire seven-month window earlier, so you’ll need to act sooner than you might expect. You can find more official Medicare enrollment information to verify your specific dates and ensure you don’t miss this critical start line.

What You Can Enroll in During Your IEP

During these seven months, you can sign up for Part A (Hospital Insurance) and Part B (Medical Insurance). This is also your chance to choose a Medicare Part D prescription drug plan to cover your medications. If you prefer an all-in-one option, you might look into Medicare Advantage plans, which often include drug coverage and extra benefits like dental. Your six-month Medigap Open Enrollment window also begins the month you are 65 and enrolled in Part B. This is the only time you are guaranteed the right to buy any Medicare Supplement (Medigap) plan regardless of your health history.

Common IEP Mistakes to Avoid

We see many people assume their retiree health plan works exactly like Medicare. Often, it doesn’t. If your employer coverage isn’t considered “creditable” by the government, you could face those lifelong penalties we mentioned earlier. Another common pitfall is waiting until the very last month of your IEP. This can lead to a stressful gap where you have no active insurance while you wait for the paperwork to process. Finally, don’t let the mountain of “junk mail” stop you from acting. We can help you sort through the noise to find the documents that actually matter for your 2026 enrollment.

The General Enrollment Period (GEP): Your Yearly Second Chance

If you missed your first window, please don’t panic. We understand how frightening it can be to realize you’ve missed a deadline, but you aren’t alone. We’re here to help you find your way back to security. The General Enrollment Period (GEP) is your annual safety net. In 2026, this window runs from January 1st through March 31st. It’s designed specifically for those who didn’t sign up when they first became eligible and don’t qualify for a Special Enrollment Period. One piece of good news is that coverage now starts the first of the month after you apply. In the past, people had to wait many months for their benefits to begin. This modern rule provides a much faster path to peace of mind. When we look at medicare initial enrollment vs general enrollment, the GEP is the “second chance” door for those who missed the first one.

You can find the Social Security Administration’s guide to Medicare enrollment for the specific steps on how to submit your application during this time. Remember, the GEP is a fixed calendar window. Unlike your personal initial window, it doesn’t care about your birthday. If you miss the March 31st deadline, you must wait until the following year to try again. We want to help you act quickly so you can stop worrying about medical bills and start focusing on your health.

The Cost of Missing the Boat

While the GEP is a helpful backup, it does come with financial consequences. The Part B late enrollment penalty is a 10% increase in your premium for every full 12-month period you could’ve had coverage but didn’t. This isn’t a one-time fee; it lasts for the rest of your life. With the 2026 standard Part B premium at $202.90, a 20% or 30% penalty can significantly impact your monthly budget. There is also a “Double Penalty” risk. If you have to pay for Part A, you’ll face a 10% penalty there too. We’ll help you calculate these costs so there are no surprises when your bill arrives.

Special Considerations for GEP Enrollees

Enrolling during the GEP also impacts your plan choices. For instance, getting Medicare Supplement (Medigap) Plans is much harder once you’re outside of your initial window. Most companies will require medical underwriting, which means they can look at your health history and potentially deny coverage. You also have a limited time to add drug coverage or look at Medicare Advantage plans after you sign up for Part B. We act as your advocate during this process. We’ll look at every available option to find the best remaining path for your 2026 coverage, ensuring you still get the protection you need.

Medicare Initial vs. General Enrollment: A Direct Comparison

When we look at medicare initial enrollment vs general enrollment, the biggest difference is how much control you have over your future. One period is a celebration of your 65th birthday; the other is a rescue mission for missed deadlines. Your Initial Enrollment Period (IEP) is a personal seven-month window that moves with you. The General Enrollment Period (GEP) is a rigid calendar window from January 1st to March 31st that applies to everyone at once. Choosing the right door doesn’t just change your start date. It dictates whether you pay the standard 2026 Part B premium of $202.90 or a much higher amount due to lifelong penalties.

The level of choice you have also changes depending on your window. During your IEP, every door is open to you. You can choose any plan without answering questions about your health. If you wait for the GEP, some of those doors might be locked. We want to help you understand these differences clearly so you can feel secure in your decision. Here is a quick look at how they compare:

- The Why: IEP is for those newly eligible for Medicare. GEP is for those who missed their first chance.

- The When: IEP is a 7-month personal window. GEP is a 3-month fixed calendar window.

- The Cost: IEP enrollees pay standard rates. GEP enrollees often face permanent 10% penalties for every year they delayed.

- The Choice: IEP offers full access to all plans. GEP may limit your ability to get certain types of supplemental coverage.

Which Period Are You In? A Simple Checklist

We know these dates can be confusing. To find your path, ask yourself if you are within three months of your 65th birthday. If the answer is yes, you are likely in your IEP. Are you still working and covered by a large employer plan? You might qualify for a Special Enrollment Period (SEP) instead of the GEP, which could save you from penalties entirely. We recommend checking our Medicare Eligibility guide to see exactly where you stand in the 2026 landscape.

The Impact on Supplemental Coverage

One detail often missed by other guides is how your enrollment window affects Medicare Supplement (Medigap) Plans. During your IEP, you have “Guaranteed Issue” rights. This means insurance companies must sell you a policy at the best price, regardless of your health. If you enroll during the GEP, you will likely face “Medical Underwriting.” This process allows companies to look at your medical history and potentially charge you more or deny you coverage altogether. We act as your advocate to help you compare your options and find a path that offers the most protection for your health and your wallet.

How We Help You Navigate the Enrollment Maze

We know that choosing between medicare initial enrollment vs general enrollment feels like a high-stakes game where the rules are constantly changing. It’s completely natural to feel a bit of “analysis paralysis” when your long-term health and finances are on the line. Our mission is to step into that confusion and offer you a clear, structured path to certainty. We aren’t restricted representatives who can only show you a handful of options. As independent brokers, we work for you, not the insurance companies. This independence allows us to be your unambiguous champion, protecting your interests above all else.

One of the biggest worries we hear from clients in 2026 is the fear of lifelong penalties. If you’ve missed your initial window, we’ll sit down with you and calculate exactly what those costs look like based on the current $202.90 standard Part B premium. We don’t just give you a number; we look for every possible way to minimize that impact. Whether it’s finding a Medicare Advantage Plan with a lower monthly cost or checking if you qualify for a Special Enrollment Period you didn’t know existed, we are here to serve and protect your savings.

Our Step-by-Step Enrollment Process

We believe that clarity comes from a methodical approach. Our journey together starts with a simple conversation to pin down your specific enrollment window. Once we know your dates, we compare options from over 40 different carriers. We look at everything from Medicare Supplement (Medigap) Plans to Medicare Part D Plans to ensure your doctors are in-network and your medications are covered at the lowest price. Finally, we handle the heavy lifting of the paperwork. You’ve worked hard for your retirement; you should be able to enjoy it without worrying about government forms.

Ready for Peace of Mind?

You shouldn’t wait until the January 1st General Enrollment deadline is staring you in the face to start planning. The most successful transitions happen when we have time to review your unique situation without the pressure of a closing window. We stay with you long after the initial sign-up, providing year-round support as your needs change. If you’re also looking for Dental Insurance Plans or life insurance to round out your protection, we can help with those too. You don’t have to do this alone. Reach out to us today for a personalized review and let us help you move from a state of distress to one of total certainty.

Take Control of Your 2026 Medicare Journey

We’ve explored how your choice between medicare initial enrollment vs general enrollment defines your future healthcare costs and coverage quality. You now know that acting during your initial seven-month window is the most secure way to avoid lifelong penalties and ensure your coverage starts exactly when you need it. You also understand that the General Enrollment Period serves as a vital yearly safety net, even if it comes with different rules and potential costs. While these systems are complex, you don’t have to face them alone. We are here to help you move from a state of uncertainty to one of complete confidence.

Paul Barrett and his expert team are dedicated to acting as your patient guides through this transition. We serve clients in over 34 states with unbiased advice that puts your needs first. Because we represent over 40 top-rated carriers, we have the freedom to find the specific plan that fits your life and your budget. Let us take the stress out of Medicare—contact The Modern Medicare Agency for a free consultation today.

We are here to protect your health and your peace of mind. You’ve worked hard to reach this milestone. Let’s work together to ensure your future is as secure and comfortable as possible.

Frequently Asked Questions

What happens if I miss my Medicare Initial Enrollment Period?

If you miss your seven-month initial window, you generally have to wait for the General Enrollment Period to sign up. This period runs from January 1st to March 31st each year. Missing your first chance often leads to lifelong late enrollment penalties that increase your monthly premiums. We recommend looking for a Special Enrollment Period first, as this might allow you to join without any extra costs or wait times.

Can I sign up for Medicare any time of the year?

No, you can only enroll during specific windows like your Initial Enrollment Period or the General Enrollment Period. This is why understanding the timeline of medicare initial enrollment vs general enrollment is so critical for your peace of mind. If you miss these windows and don’t qualify for a special exception, you might have to wait months for the next chance, leaving you with a risky gap in your health coverage.

Does the Medicare General Enrollment Period have a late penalty?

The period itself isn’t a penalty, but using it usually means you’ll pay more for your coverage. Most people who enroll during this time have already missed their initial window, which triggers a permanent 10% increase in the Part B premium for every full 12-month period they delayed. In 2026, with the standard Part B premium at $202.90, these penalties can add a significant burden to your monthly retirement budget.

How long does the Part B late enrollment penalty last?

The Part B late enrollment penalty is a permanent cost that lasts for the rest of your life. It doesn’t expire after a few years; it stays attached to your premium as long as you’re enrolled in Medicare. This is why we focus so heavily on getting your timing right the first time. We want to protect you from these lifelong extra charges so you can keep more of your hard-earned savings.

When does coverage start if I sign up during the General Enrollment Period in 2026?

Under the modern rules for 2026, your coverage starts on the first of the month after you sign up. For example, if you complete your application in February, your benefits will begin on March 1st. This is much faster than the old rules that made people wait until July. However, you should still plan carefully to avoid being without insurance for those few weeks while your application processes.

Can I switch from a Medicare Advantage plan during the GEP?

Yes, because the Medicare Advantage Open Enrollment Period happens at the same time, from January 1st to March 31st. During this window, you can switch to a different Medicare Advantage plan or move back to Original Medicare. We can help you compare over 40 carriers to see if a different plan offers better benefits or lower costs for your specific doctors and medications in the coming year.

Is there a difference between the General Enrollment Period and Open Enrollment?

Yes, they serve two different purposes. The General Enrollment Period is for people who missed their first chance to sign up for Part B and need to get into the system. The Annual Open Enrollment Period in the fall is for people who already have Medicare and want to change their plans. We know it’s confusing, so we’re here to help you identify exactly which window you should be using.

Do I need to sign up for Medicare if I am still working at 65?

It depends on the size of your employer. If your company has 20 or more employees, your work coverage is usually considered “primary,” and you might be able to delay Medicare without a penalty. However, if your company is smaller, you likely need to sign up for Medicare to avoid huge gaps in your coverage. We can review your employer’s plan with you to make sure you’re making the safe choice.