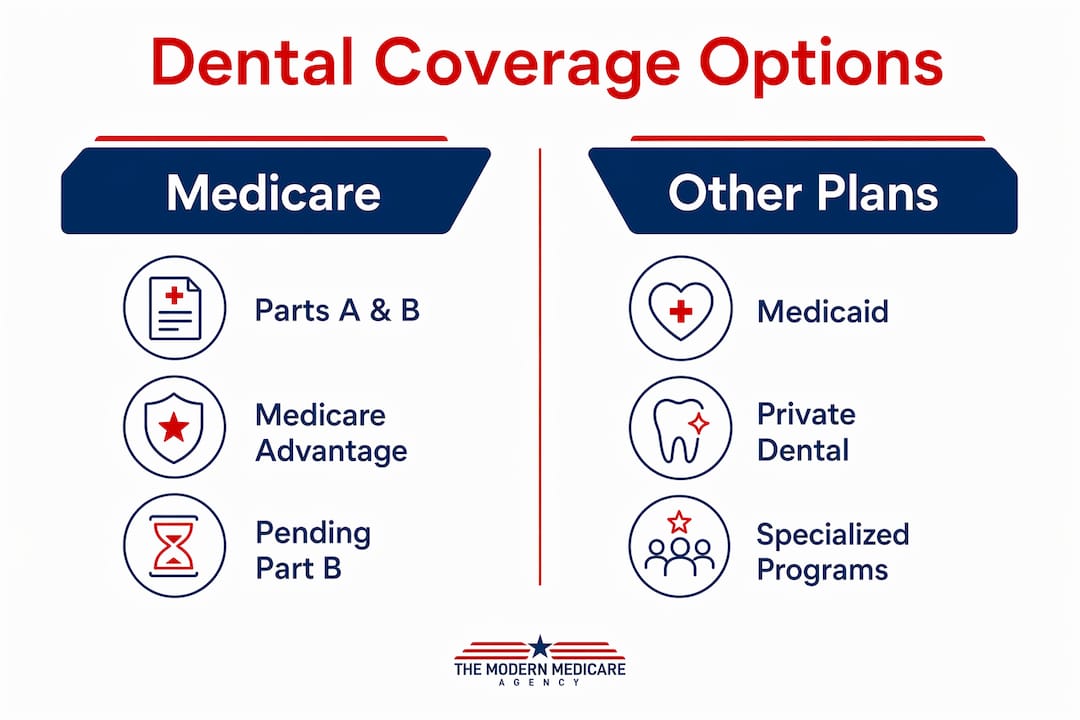

Disability dental insurance options explained simply means this: standard Medicare Parts A and B do not cover routine dental care, and people with disabilities must look elsewhere for coverage. About 24 million Medicare enrollees lack dental benefits, including 7 million people under age 65 who qualify through disability. That gap is significant. The good news is that Medicare Advantage, Medicaid, and private dental plans each offer real paths to coverage. Knowing which path fits your situation is the first step toward protecting your oral health without overpaying.

What are the main disability dental insurance options explained?

Original Medicare draws a clear line. Parts A and B cover medically necessary dental procedures only when they are directly tied to another covered Medicare service. A tooth extraction before heart surgery, for example, may qualify. Routine cleanings, fillings, dentures, and X-rays do not. That exclusion leaves millions of people with disabilities paying out of pocket for care they need regularly.

Medicare Advantage plans change that picture. Most Medicare Advantage (Part C) plans include some dental benefits as part of their bundled coverage. The catch is that coverage levels vary widely between plans, networks are limited, and cost sharing still applies. One plan may cover two cleanings per year with no copay. Another may cap annual dental benefits at $1,000 and require you to use a specific network of dentists.

Policy discussions in Washington have pushed to add dental benefits directly to Medicare Part B, which would be a major shift. That change has not passed as of 2026. Until it does, Medicare Advantage remains the most accessible route to embedded dental coverage for people already enrolled in Medicare.

Pro Tip: Evaluate Medicare Advantage plans with dental benefits before purchasing a standalone private dental plan. Bundled coverage through Medicare Advantage is often more cost-effective than layering a separate policy on top.

When comparing Medicare Advantage plans for dental coverage, focus on four things:

- Annual dental maximum: How much the plan pays per year before you cover the rest

- Covered services: Whether the plan includes basic restorative care like fillings, not just preventive cleanings

- Network size: How many dentists in your area accept the plan

- Cost sharing: What copays or coinsurance apply to each service category

How does Medicaid cover dental care for people with disabilities?

Medicaid is the other major public option, and it works very differently from Medicare. Dental coverage through Medicaid is determined at the state level, which means benefits vary dramatically depending on where you live. Some states cover only emergency dental extractions for adults. Others offer full preventive and restorative care.

The variation matters enormously for people with disabilities. Many individuals with disabilities qualify for both Medicare and Medicaid simultaneously, a status known as “dual eligibility.” Dual-eligible individuals can sometimes use Medicaid to cover costs that Medicare Advantage does not, including dental services.

Certain states go further with specialized programs. Florida’s Medicaid dental program, for example, offers comprehensive coverage for adults with severe disabilities, including hospital-based dentistry and sedation under general anesthesia or IV sedation. That level of care matters for people who cannot tolerate standard dental procedures due to physical or cognitive conditions.

| State Medicaid dental coverage type | What it typically includes |

|---|---|

| Emergency only | Extractions to relieve pain or infection |

| Limited | Preventive cleanings and basic fillings |

| Comprehensive | Restorative care, dentures, and specialist referrals |

| Special needs expanded | Sedation, hospital dentistry, and behavioral accommodations |

Prior authorization is required for advanced procedures like sedation or hospital-based dental work under most Medicaid programs. Medical necessity documentation from your physician or dentist supports that approval process. Without it, claims are routinely denied. Contact your local Medicaid office directly to confirm exactly what your state covers, because online summaries often lag behind current policy.

- Call your state Medicaid office to request a current dental benefit summary in writing

- Ask specifically whether sedation or hospital dentistry is covered for your diagnosis

- Request a list of in-network dentists who accept Medicaid and have special needs experience

- Find out whether prior authorization is required before scheduling any procedure beyond a routine cleaning

What private dental plans work best for people with disabilities?

Private dental insurance fills the gaps that Medicare and Medicaid leave open. Most private plans cover preventive care immediately but impose waiting periods of 6 to 12 months for basic restorative work and up to 12 months for major procedures like crowns or dentures. Premiums start as low as $19 to $20 per month for basic coverage, though plans with broader benefits cost more.

The trade-off between premium cost and waiting periods is the central decision. A lower-premium plan saves money monthly but delays access to fillings or extractions. A higher-premium plan with no waiting period costs more upfront but covers care right away. For people with disabilities who already have known dental needs, a plan without waiting periods is usually worth the higher monthly cost.

Pro Tip: Check whether your dental plan type is an HMO or PPO before enrolling. HMO plans generally do not cover out-of-network care at all, while PPO plans offer discounts for in-network providers but still pay a reduced amount for out-of-network visits.

Some newer private plans have expanded their coverage to address chronic illness-related dental needs. These “dental wellness” plans include specific periodontal and cavity prevention benefits for people with diabetes, heart disease, and Parkinson’s disease. Those conditions overlap heavily with disability populations, making this category worth researching if you manage a chronic condition alongside your disability.

Failing to verify network participation before enrolling is the most common and costly mistake people make with private dental plans. A dentist who accepts your insurance today may leave the network next year. Always confirm network status directly with the dentist’s office, not just through the insurer’s online directory.

What special factors matter when choosing dental coverage with a disability?

Provider experience is the factor most people overlook. Dentists with special needs expertise understand Medicaid billing, meet ADA accessibility standards, and have staff trained to accommodate patients with mobility, sensory, or cognitive differences. A dentist who has never worked with a wheelchair user or a patient with severe anxiety will struggle to deliver effective care, regardless of what your insurance covers.

Look for practices that explicitly list special needs dentistry or patients with disabilities as part of their services. Hospital-based dental programs affiliated with academic medical centers often have the broadest accommodations and accept the widest range of insurance plans.

Coordinating multiple coverage sources is another skill worth developing. If you have both Medicare Advantage and Medicaid, one plan acts as primary and the other as secondary. Used correctly, that coordination can reduce your out-of-pocket costs to near zero for covered services. A patient advocate or an independent insurance agent who specializes in Medicare can help you map out how your specific plans interact.

Common pitfalls to avoid:

- Assuming your current dentist accepts your new plan without calling to confirm

- Enrolling in a plan with a waiting period when you need restorative work immediately

- Skipping prior authorization for sedation and having the claim denied after the procedure

- Not reviewing your Medicare Advantage dental benefits annually, since plan details change each year during open enrollment

People with disabilities who are under 65 face an additional layer of complexity. Medicare supplement options for disabled individuals under 65 differ from those available at 65, and not all states require insurers to sell Medigap plans to younger Medicare beneficiaries. Understanding that distinction helps you plan realistically for what coverage you can actually access.

Key Takeaways

People with disabilities have three real paths to dental coverage: Medicare Advantage, Medicaid, and private dental plans, and combining them strategically produces the best results.

| Point | Details |

|---|---|

| Original Medicare excludes dental | Parts A and B do not cover routine cleanings, fillings, or dentures. |

| Medicare Advantage offers embedded dental | Most Part C plans include dental benefits, but coverage levels and networks vary widely. |

| Medicaid dental varies by state | Some states cover only emergencies; others provide sedation and hospital dentistry for special needs adults. |

| Private plans start at $19–$20 per month | Waiting periods of 6–12 months apply to basic and major work in most private plans. |

| Provider network verification is critical | Confirm in-network status directly with the dentist’s office before enrolling in any plan. |

What I’ve learned after years of helping people with disabilities find dental coverage

After nearly two decades of working with Medicare consumers, the pattern I see most often is this: people with disabilities wait too long to address dental coverage. They assume Medicare handles it, discover it does not, and then face an urgent dental need with no insurance in place.

The individuals who fare best start by checking their Medicare Advantage plan’s dental benefits during every annual enrollment period. Plan details change year to year, and a plan that covered fillings last year may have reduced that benefit. Reviewing your coverage in october and november, before the January 1 effective date, gives you time to switch if needed.

I also tell people not to treat Medicaid as a last resort. If you qualify, Medicaid can be a powerful complement to Medicare Advantage. The coordination between the two programs, done correctly, can cover services that neither plan would fully pay alone. The key is working with someone who understands how the two programs interact in your specific state.

The hardest conversations I have are with people who enrolled in an HMO dental plan, assumed their longtime dentist was covered, and then received a bill for the full cost of a crown. That mistake is entirely avoidable. Spend 10 minutes calling your dentist’s office before you sign up for anything. It is the single highest-return action you can take.

Finally, do not underestimate the value of a dentist who genuinely knows how to work with patients with disabilities. Good insurance means nothing if the office cannot accommodate your needs. Build that provider relationship before you have an urgent problem, not during one.

— Paul

How Paulbinsurance helps you find the right dental coverage

Sorting through Medicare Advantage plans, Medicaid rules, and private dental options takes time and expertise most people simply do not have. Paulbinsurance specializes in exactly this work, with independent agents who have helped Medicare consumers since 2007.

Whether you need a Medicare Advantage plan with dental benefits or guidance on how to layer Medicaid and private coverage, Paulbinsurance can walk you through your real options based on your location, health needs, and budget. There is no pressure and no guesswork. You get clear answers from agents who know Medicare inside and out. Reach out to Paulbinsurance today and get the coverage picture you actually need.

FAQ

Does Medicare cover dental care for people with disabilities?

Standard Medicare Parts A and B do not cover routine dental care, including cleanings, fillings, or dentures. Medicare Advantage (Part C) plans often include dental benefits, making them the primary Medicare-based option for dental coverage.

What dental benefits does Medicaid offer for disabled adults?

Medicaid dental coverage varies by state and ranges from emergency-only extractions to comprehensive care including sedation and hospital dentistry for adults with severe disabilities. Contact your state Medicaid office to confirm your specific benefits.

How much does private dental insurance cost for people with disabilities?

Private dental insurance premiums start as low as $19 to $20 per month for basic plans, though plans with no waiting periods and broader restorative coverage cost more. Most plans cover preventive care immediately but impose 6 to 12-month waiting periods for major work.

Can I have both Medicare Advantage and Medicaid dental coverage?

Yes. Dual-eligible individuals can use Medicare Advantage as primary coverage and Medicaid as secondary, which can significantly reduce out-of-pocket dental costs when both plans are coordinated correctly.

What should I look for in a dentist if I have a disability?

Seek dentists who explicitly serve patients with special needs, meet ADA accessibility standards, and have experience with Medicaid billing. Hospital-affiliated dental programs often offer the broadest accommodations and accept the widest range of insurance plans.