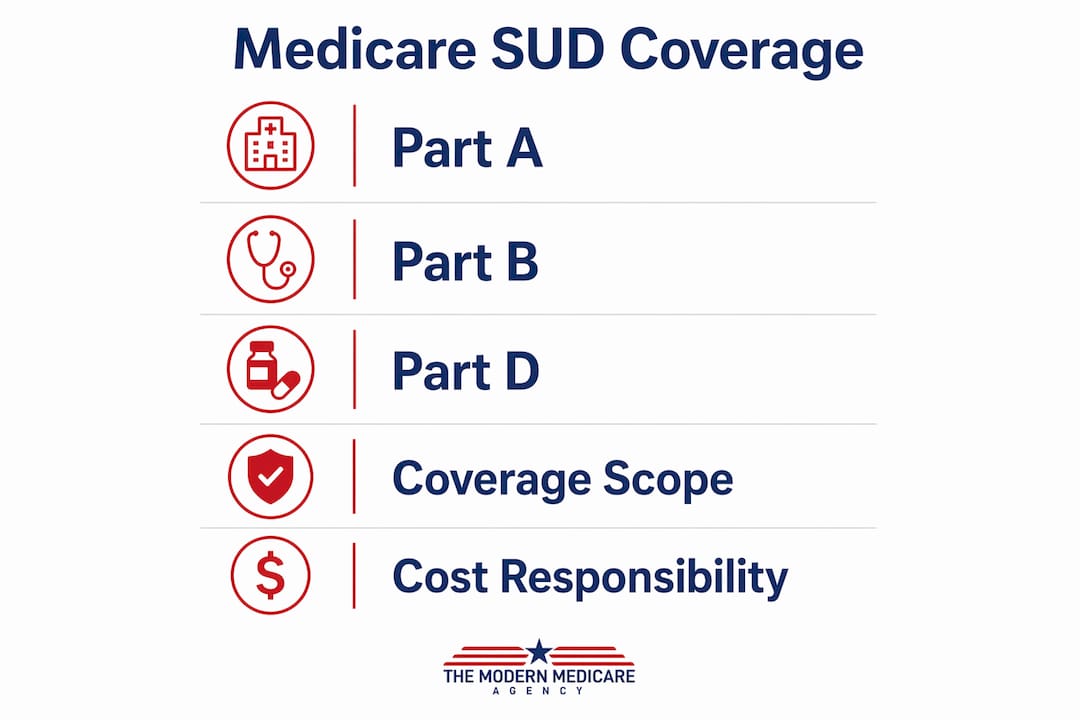

Medicare substance use disorder coverage is defined as the set of federal benefits that pay for addiction treatment services, including inpatient detox, outpatient therapy, and medication-assisted treatment, for eligible beneficiaries 65 and older or those qualifying through disability. Coverage is divided across Medicare Parts A, B, and D, with each part handling a distinct level of care. The Mental Health Parity and Addiction Equity Act (MHPAEA) requires Medicare to provide addiction treatment benefits comparable to medical and surgical care, meaning no more restrictive cost-sharing or coverage limits for substance use disorder (SUD) than for physical health conditions. Understanding how each part works is the first step toward getting the care you need without unexpected bills.

What types of substance use disorder treatments does Medicare cover?

Medicare SUD coverage is split across three parts, each covering a different stage of treatment. Knowing which part applies to your situation prevents costly surprises.

Part A: Inpatient hospital and detox stays

Part A covers inpatient hospital stays for medically supervised detox and stabilization. This includes stays in general hospital psychiatric units. Coverage applies when a doctor certifies that inpatient care is medically necessary. Freestanding psychiatric hospitals carry a lifetime limit of 190 days under Original Medicare, but psychiatric units inside general hospitals do not carry that same cap.

Part B: Outpatient programs and counseling

Part B covers the widest range of SUD services. In 2024, Medicare expanded coverage to include Intensive Outpatient Programs (IOPs), which provide 9–19 hours of structured therapy per week. Partial Hospitalization Programs (PHPs) require 30 or more hours of care per week and have been covered longer. Standard outpatient counseling typically runs 1–9 hours per week. Part B also covers individual and group therapy sessions, psychiatric evaluations, and physician office visits related to addiction care.

Part D: Medication-assisted treatment drugs

Part D covers FDA-approved medications used in medication-assisted treatment (MAT). Buprenorphine and naltrexone are covered through standard Part D drug plans. Methadone for opioid use disorder works differently. Medicare pays licensed Opioid Treatment Programs a monthly bundled rate that includes the medication, counseling, and toxicology testing together. That bundled model is rare among insurance programs and means you cannot fill a methadone prescription at a retail pharmacy for addiction treatment. You must receive it through a certified clinic. For a full breakdown of how Part D works, the Part D drug coverage guide at Paulbinsurance walks through plan comparison in plain language.

Medicare Advantage (Part C) and SUD benefits

Medicare Advantage plans must cover everything Original Medicare covers, but many go further. Some plans cover residential treatment programs, transportation to treatment, and additional counseling sessions. The trade-off is that most Advantage plans require prior authorization before you begin treatment, which can delay access to urgent care.

How much does Medicare coverage for substance use disorder treatment cost you?

Cost-sharing under Medicare SUD benefits depends on which part covers your treatment and whether you carry supplemental coverage.

Part A costs apply when you need inpatient hospital care:

- The 2024 Part A deductible is $1,632 per benefit period for inpatient stays.

- Days 1–60 in the hospital carry no daily copay after the deductible.

- Days 61–90 require a daily copay of $408.

- Beyond 90 days, lifetime reserve days apply at $816 per day.

Part B costs apply to outpatient SUD services:

- The 2024 annual Part B deductible is $240.

- After the deductible, you pay 20% coinsurance on all covered outpatient services.

- That 20% applies to IOP sessions, PHP days, counseling visits, and physician services.

Medicare Advantage cost structures vary by plan. Many Advantage plans replace the 20% coinsurance with fixed copays per visit, which can be lower or higher depending on the plan. Some plans offer $0 copays for certain behavioral health visits.

Medigap (Medicare Supplement) plans cover the gaps Original Medicare leaves open. A Medigap Plan G, for example, covers the Part A deductible and the 20% Part B coinsurance entirely, leaving you with only the Part B annual deductible to pay out of pocket. That protection matters significantly when you are looking at weeks of outpatient therapy or a multi-day inpatient stay. Paulbinsurance’s guide on reducing out-of-pocket costs explains how supplement plans work alongside Medicare SUD benefits.

Pro Tip: If you are enrolled in Original Medicare without a Medigap plan, ask your treatment provider about sliding-scale fees or financial assistance options before your first appointment. Many facilities offer payment plans or scholarship programs that reduce your share of costs.

What are the coverage limitations and common challenges with Medicare SUD benefits?

Medicare addiction treatment benefits have real gaps. Knowing them before you need care prevents delays and denials.

-

Residential rehab is largely excluded. Original Medicare does not cover stays at standalone residential treatment facilities unless the facility is a licensed hospital or certified psychiatric unit. This surprises many people who assume that any inpatient rehab setting qualifies. It does not.

-

The 190-day psychiatric hospital limit applies. Freestanding psychiatric hospitals carry a lifetime cap of 190 inpatient days under Original Medicare. General hospital psychiatric units do not have this limit, which makes the type of facility a critical factor in long-term treatment planning.

-

Medical necessity is required for higher-level care. Medicare will not approve inpatient or PHP-level treatment without clinical documentation proving the care is medically necessary. A licensed physician or addiction specialist must provide that documentation. Medical necessity is the pivotal factor in authorization decisions, and missing or incomplete documentation is the most common reason claims are denied.

-

Prior authorization delays care in Medicare Advantage. Advantage plans can introduce authorization delays that slow access to urgent SUD treatment. If you are in a crisis situation, a delay of even a few days carries serious consequences.

-

Telehealth has new in-person requirements. As of january 31, 2026, Medicare requires at least one in-person behavioral health visit every 12 months for ongoing telehealth SUD services. An initial in-person visit within 6 months before the first telehealth appointment is also required. For beneficiaries in rural areas, this rule creates a real access barrier.

Pro Tip: Before enrolling in a Medicare Advantage plan, ask the plan directly whether your preferred treatment facility is in-network and whether prior authorization is required for IOP or PHP services. Get the answer in writing.

How can you appeal if Medicare denies your SUD treatment claim?

A denial is not the final word. Many denials are overturned on appeal when supported by proper clinical documentation. The Medicare appeals process has five levels, and most successful appeals happen at the first or second level.

-

Request a Redetermination. File within 120 days of receiving the denial notice. Submit a written request to the Medicare contractor who processed the claim, along with a letter from your treating physician explaining medical necessity.

-

Request a Reconsideration. If the redetermination is denied, request a Qualified Independent Contractor (QIC) review within 180 days. Attach updated clinical notes and any new supporting documentation.

-

Request an ALJ Hearing. If the QIC upholds the denial and the disputed amount meets the threshold, request a hearing before an Administrative Law Judge (ALJ) within 60 days of the QIC decision.

-

Escalate to the Medicare Appeals Council. If the ALJ rules against you, appeal to the Medicare Appeals Council within 60 days.

-

File in Federal District Court. This final level applies when the disputed amount meets the federal court threshold.

For a detailed walkthrough of each step, Paulbinsurance has a plain-language guide on appealing denied Medicare claims that covers what to submit and when. The Medicare mental health coverage page also explains how parity rules under MHPAEA support your appeal rights for SUD treatment specifically.

Pro Tip: Ask your treatment provider to write a detailed letter of medical necessity before you begin treatment, not after a denial. Proactive documentation prevents most first-level denials entirely.

Key Takeaways

Medicare substance use disorder coverage spans Parts A, B, and D, and understanding each part’s scope, costs, and limits is the single most effective way to avoid denied claims and unexpected bills.

| Point | Details |

|---|---|

| Coverage spans three Medicare parts | Part A covers inpatient detox, Part B covers outpatient programs, and Part D covers MAT medications. |

| Residential rehab has a major gap | Original Medicare does not cover standalone residential rehab unless the facility is a licensed hospital or psychiatric unit. |

| Out-of-pocket costs are significant | The 2024 Part A deductible is $1,632 per benefit period; Part B requires 20% coinsurance after a $240 deductible. |

| Medical necessity documentation is critical | Clinical documentation from a licensed provider is required for inpatient and higher-level outpatient approvals. |

| Denials can be overturned | Most successful appeals are won at the first or second level when supported by strong clinical documentation. |

What I have learned after years of helping Medicare beneficiaries navigate SUD coverage

The biggest mistake I see is people waiting until they are in a crisis to figure out what Medicare actually covers. By then, they are making decisions under pressure, and that is when costly misunderstandings happen. I have worked with Medicare consumers since 2007, and the pattern repeats: someone assumes their inpatient rehab stay is covered, then receives a bill that should never have surprised them.

The residential rehab exclusion catches people off guard more than any other gap in Medicare SUD benefits. Families assume that any facility calling itself a “rehab center” qualifies. It does not. The facility must be a licensed hospital or certified psychiatric unit for Original Medicare to pay. That distinction changes everything about which facility you choose.

My honest advice is to verify your benefits before you need them. Call Medicare directly, or work with an independent agent who knows the details. If you are on a Medicare Advantage plan, read the prior authorization rules for behavioral health before a crisis forces your hand. The coverage is there. The gaps are real. Knowing both puts you in control.

— Paul

How Paulbinsurance helps you get more from your Medicare SUD benefits

Navigating Medicare’s cost-sharing rules for addiction treatment is genuinely complex. A Medigap supplement plan can eliminate the 20% Part B coinsurance and the Part A deductible entirely, which makes a real difference when treatment runs for weeks or months.

Paulbinsurance specializes in helping Medicare beneficiaries find the right supplement or Advantage plan for their specific health needs. Whether you want to choose between Medicare Advantage and supplements or need help comparing Medigap options that reduce SUD treatment costs, the team at Paulbinsurance is ready to walk you through your options. Contact Paulbinsurance today for a no-pressure conversation about the coverage that fits your situation.

FAQ

What does Medicare cover for substance use disorder treatment?

Medicare covers inpatient hospital detox through Part A, outpatient programs including IOPs and PHPs through Part B, and FDA-approved MAT medications through Part D. Methadone for opioid use disorder is covered through licensed Opioid Treatment Programs under a bundled monthly payment.

Does Medicare cover residential rehab for addiction?

Original Medicare does not cover stays at standalone residential rehab facilities. Coverage applies only when the facility is a licensed hospital or certified psychiatric unit. Some Medicare Advantage plans offer residential treatment as an added benefit.

How much does Medicare SUD treatment cost out of pocket?

Part A carries a $1,632 deductible per benefit period, and Part B requires 20% coinsurance after a $240 annual deductible. A Medigap supplement plan can cover most or all of those costs.

Can Medicare deny my substance use disorder treatment claim?

Yes, Medicare can deny claims that lack medical necessity documentation. Many denials are overturned on appeal when a licensed provider submits detailed clinical records supporting the need for treatment.

Does Medicare Advantage cover more SUD services than Original Medicare?

Medicare Advantage plans often cover additional services such as residential treatment and transportation, but they typically require prior authorization, which can delay access to urgent care.