By Paul Barrett, CMIP | The Modern Medicare Agency | Melville, NY 18+ years Medicare-exclusive experience | Licensed in 34 states | 40+ carriers Last updated: July 2026

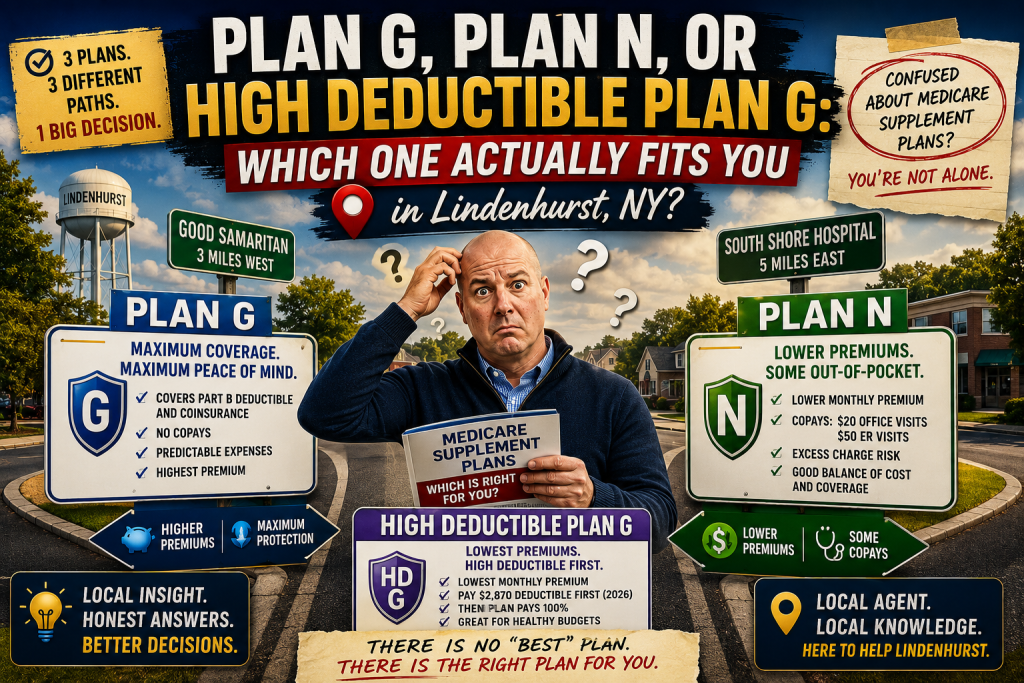

If you’ve read our companion article, Medigap Rate Increases in Lindenhurst, NY, you already know why premiums have climbed the way they have around here. This article picks up where that one leaves off. Once you understand the pricing pressure, the next question is which plan actually makes sense for your budget: Plan G, Plan N, or High Deductible Plan G.

Let’s have this conversation the way I’d have it at your kitchen table — not which plan is “best,” because there isn’t one, but which cost structure fits how you actually use healthcare and how much monthly cushion you have.

Here’s the thing that trips a lot of people up: in New York, Medigap benefits are standardized by federal law. A Plan G from UnitedHealthcare covers exactly the same things as a Plan G from Aetna. So this isn’t really a “which plan is better” conversation — it’s a “which cost structure fits your life” conversation.

The Three Plans, Side by Side

| What's Covered | Plan G | Plan N | High Deductible Plan G |

|---|---|---|---|

| Part A coinsurance & hospital costs | ✅ | ✅ | ✅ * |

| Part A deductible ($1,736 in 2026) | ✅ | ✅ | ✅ * |

| Part B coinsurance (the 20%) | ✅ | Partial** | ✅ * |

| Part B deductible ($283 in 2026) | ❌ (you pay) | ❌ (you pay) | ✅ Counts toward deductible |

| Part B excess charges | ✅ | ❌ | ✅ * |

| Skilled nursing facility coinsurance ($217/day, days 21–100) | ✅ | ✅ | ✅ * |

| Foreign travel emergency (80% up to plan limits) | ✅ | ✅ | ✅ * |

*High Deductible Plan G covers everything standard Plan G covers — but only after you’ve paid $2,950 out of pocket toward Medicare-approved costs in 2026. Until then, you’re responsible for those costs yourself. **Plan N covers Part B coinsurance except for copays up to $20 for some office visits and up to $50 for ER visits that don’t result in admission.

The New York Wrinkle Almost Nobody Explains Correctly

You’ll see a lot of national Medicare content claim that New York “bans” Part B excess charges outright, which would make Plan N’s lack of excess-charge coverage a non-issue here. That’s not quite accurate, and it’s worth getting right.

New York Public Health Law caps what a non-participating provider can bill above the Medicare-approved amount at 5% for most services — not the 15% ceiling that applies in most other states, but not zero either. One documented carve-out: certain home and office visits involving evaluation and management services are excluded from the state’s 5% cap and remain subject to the federal 15% limit. So the excess-charge risk on Plan N is real in New York, it’s just smaller than it would be in, say, Florida or Texas, for most services. Since fewer than 5% of providers nationally decline Medicare assignment in the first place, this is a modest risk either way — but “modest” isn’t “zero,” and Plan G closes that gap completely regardless of which limit applies.

What This Actually Costs: Current Long Island Rates

Coverage comparisons only tell half the story. Here’s what these plans actually cost right now, using the New York DFS Community Rated Medicare Supplement Premium Comparison Table effective July 1, 2026, for the Long Island rating region.

Plan G — Long Island:

- UnitedHealthcare (AARP): $342.50/month — lowest-priced Plan G accessible through an independent broker

- Aetna: $406.26/month — currently not accepting new individual enrollments in New York

- EmblemHealth: $432.09/month — see the caveat below before considering this one

- Globe Life: $461.00/month

- Mutual of Omaha: $511.36/month

- Humana: $709.98/month

- Bankers Conseco: $840.28/month

A word on EmblemHealth before you compare on price alone: EmblemHealth shows up repeatedly across Long Island Medigap comparisons, so it’s worth being direct about what you’re actually getting. AM Best rates EmblemHealth Plan, Inc. C+ (Marginal) — upgraded from C (Weak) on July 14, 2026, and still well below the financial strength ratings of the larger national carriers on this list. Enrollment for this product also runs through a direct paper application rather than the carrier-assigned broker support some other carriers provide. Weigh both of those against any premium difference you see on paper.

Rates above can and do change with each DFS filing cycle, so always confirm before enrolling.

What This Looks Like in a Light Year vs. a Heavy Year

Light year — a couple of annual physicals, no hospital stays:

- Plan G: You pay the $283 Part B deductible. That’s it. Premium plus $283/year.

- Plan N: You pay the $283 Part B deductible plus small office-visit copays (up to $20 each). Lower premium, slightly more in small copays.

- HD Plan G: You pay out of pocket until you hit $2,950 — in a light year, that likely means you pay close to the full $283 deductible plus routine coinsurance, well under the cap.

HD Plan G usually wins a light year on total cost.

Heavy year — a hospital stay, specialist care, a few procedures:

- Plan G: You pay $283 total for the year. Everything else Medicare-approved is covered.

- Plan N: You pay $283 plus accumulating office/ER copays — still modest relative to the premium savings.

- HD Plan G: You could pay up to the full $2,950 deductible before the plan takes over — a real number to have sitting in savings.

Plan G gives the most predictable ceiling in a heavy year.

The break-even math that actually matters: Take the annual premium difference between standard Plan G and High Deductible Plan G. If that difference is more than the $2,950 HD deductible, standard Plan G already wins outright. If it’s less, HD Plan G wins in any year where your Medicare-approved costs stay under that gap — which, for most healthy retirees, is most years. The honest answer is that HD Plan G rewards people who can comfortably absorb a $2,950 bad-year number without it disrupting their budget. If that number would keep you up at night, standard Plan G is buying you peace of mind, not just coverage.

Why High Deductible Plan G Has Been Looking Better Every Year

This is the part that genuinely confuses people, and it’s worth slowing down on: the reason HD Plan G has gotten more attractive over the last few years isn’t that the plan changed. It’s that the two numbers driving the comparison have been moving in completely different directions.

The HD Plan G deductible is set by federal formula — it only moves with the Consumer Price Index each year. It went from $2,870 in 2025 to $2,950 in 2026, an increase of about 2.8%. That’s it. It doesn’t respond to claims trends, carrier pricing pressure, or New York’s adverse selection problem. It just tracks inflation, slowly, every year, like clockwork.

Standard Plan G premiums don’t work that way. As covered in our companion article on Lindenhurst’s rate increases, UnitedHealthcare’s requested 2026 rate increases ranged from 17.7% to 18.0% across its New York Medigap plans, according to UHC’s own published rate notice, and industry-wide Plan G filings this year ranged from roughly 12% to more than 26% nationally. When the thing you’re insuring against a “worst case” barely moves, and the premium you’re paying every single month keeps jumping by double digits, the math tilts further toward the high-deductible option every year — even for people who were previously right on the fence.

Here’s what that actually looks like using the current July 2026 DFS table, for the carriers that offer both a standard and high-deductible version of Plan G on Long Island:

| Carrier | Standard Plan G | HD Plan G | Annual Premium Savings | Worst-Case Net Savings (after $2,950 deductible) |

|---|---|---|---|---|

| EmblemHealth* | $432.09/mo | $67.69/mo | $4,372.80 | $1,422.80 |

| Globe Life | $461.00/mo | $91.00/mo | $4,440.00 | $1,490.00 |

| Humana | $709.98/mo | $106.34/mo | $7,243.68 | $4,293.68 |

| Bankers Conseco | $840.28/mo | $75.69/mo | $9,175.08 | $6,225.08 |

See the EmblemHealth caveat above — financial strength rating and enrollment process apply regardless of price.

Read that last column carefully: for every carrier on Long Island that offers both versions of Plan G, the annual premium savings from choosing HD Plan G is larger than the entire $2,950 deductible — meaning even in a genuine worst-case year where you hit the full deductible, HD Plan G still comes out ahead in raw dollars for these specific carriers. That’s not a “usually” or a “probably.” At today’s premium gap, it’s true even in the worst year you could have.

One important market gap worth knowing: UnitedHealthcare and Aetna — the two carriers most Lindenhurst residents actually consider first — do not currently offer a High Deductible Plan G option on the New York DFS table. The carriers that do offer HD Plan G here (EmblemHealth, Globe Life, Humana, Bankers Conseco) are not the same carriers leading on standard Plan G price or reputation. That means choosing HD Plan G in Lindenhurst right now isn’t just a deductible decision — it also means stepping outside the carrier you might otherwise default to, which makes the financial strength and service-access conversation just as important as the premium math above.

This is also, honestly, where most of the consumer confusion sits. People hear “high deductible” and their instinct is to treat it like a warning label — something risky, something for people trying to save a few bucks and hoping nothing goes wrong. But the deductible isn’t unlimited exposure the way a health insurance deductible sometimes feels. It’s a hard, published, CPI-indexed cap that Medicare itself sets every year, and as the tables above show, the premium gap between standard and high-deductible Plan G has grown large enough that the “worst case” often isn’t actually worse in dollars — it’s just less predictable month to month, which is a very different thing than being more expensive.

Who Tends to Be Happiest With Each Plan

Plan G fits you if… you want to pay one predictable number and be done thinking about it. You see specialists regularly, you’ve had a hospital stay before, or you just don’t want deductible math in the back of your mind during a health scare. It’s also the only one of the three that fully closes the New York excess-charge gap, however modest that gap is here.

Plan N fits you if… you’re healthy, you don’t mind a small copay here and there, and you want a meaningfully lower premium than Plan G without taking on real financial risk. The trade-off is genuinely small in New York given the 5% excess-charge cap — this is often the most underrated option for people who are otherwise leaning toward Plan G just out of habit.

High Deductible Plan G fits you if… you’re comfortable with the idea that a bad year could cost you close to $2,950 out of pocket, and in exchange you want the lowest possible monthly premium in years when nothing happens. This tends to fit people with a healthy financial cushion, no major chronic conditions requiring frequent care, and a preference for keeping more cash in hand month to month.

Paul's Take: What I Actually Recommend, and Why

I bring up High Deductible Plan G with almost every healthy client I meet, even though it usually means a lower commission for me than a standard Plan G sale. It’s not the flashy answer, but for someone who rarely goes to the doctor and has $3,000 sitting in savings they’re not touching, it’s often the mathematically smart move — you’re essentially self-insuring the gap in exchange for a much lower premium for years at a time. What surprises most people once I actually walk them through the numbers above is that it’s not even close anymore. A few years ago this was a genuinely close call for a lot of clients. With standard Plan G premiums up double digits two years running and the deductible only crawling up with inflation, it isn’t close for most carriers today.

The honest catch is that UnitedHealthcare and Aetna — the two carriers most people default to — don’t offer HD Plan G in New York right now. So saying yes to the high-deductible math usually means saying yes to a different carrier too, and that’s exactly why I walk through financial strength and service access with every client before we talk premium. A cheap deductible from a carrier with no agent behind it and a weak rating isn’t automatically the win it looks like on paper.

That said, I don’t push it on everyone. If you’ve had a cancer scare, a joint replacement, or you’re managing something chronic that means regular specialist visits, the predictability of standard Plan G is worth the extra premium — not because HD Plan G is “risky,” but because you already know you’re going to use care, so the deductible math doesn’t favor you the way it does for someone healthy. And Plan N deserves more attention than it gets around here. Given how thin New York’s excess-charge exposure actually is, a lot of healthy Lindenhurst clients are paying full Plan G premiums for excess-charge protection they were never realistically going to need.

Frequently Asked Questions

Is Plan G better coverage than Plan N?

Not exactly “better” — more complete. Plan G covers the Part B coinsurance gap fully and protects against Part B excess charges. Plan N leaves you responsible for small office and ER copays and doesn’t cover excess charges, which in New York are capped at 5% rather than the 15% allowed in most states. Both plans cover the same Part A costs and skilled nursing facility coinsurance identically.

Does New York really limit Part B excess charges to 5%?

Yes, for most services. New York Public Health Law caps excess charges at 5% above the Medicare-approved amount rather than the federal 15% ceiling that applies in most other states, with one carve-out: certain home and office evaluation and management visits remain subject to the federal 15% limit rather than the state’s 5% cap. It’s a real, if partial, protection — not a full ban, so Plan N enrollees in New York do carry some residual exposure, just less than Plan N enrollees in most other states.

How does High Deductible Plan G actually save money if I might have to pay $2,950?

The savings come from the gap between what you’d pay in premium for standard Plan G versus HD Plan G, multiplied over a full year. On Long Island’s current rate table, that annual premium gap is larger than the $2,950 deductible for every carrier offering both versions — so even in a year where you use enough care to hit the full deductible, you typically still spend less overall than you would have on standard Plan G. In a lighter year, the savings are even larger since you never come close to the deductible at all.

Why doesn’t UnitedHealthcare offer High Deductible Plan G in New York?

Not every carrier chooses to file every plan type with the state. As of the current DFS rate table, UnitedHealthcare and Aetna do not offer a High Deductible Plan G option in New York, while EmblemHealth, Globe Life, Humana, and Bankers Conseco do. That means choosing HD Plan G here involves picking from a different set of carriers than the ones most people default to for standard Plan G, which is why comparing financial strength and service access matters just as much as the premium.

Is EmblemHealth a good choice just because it’s often listed with lower High Deductible Plan G pricing?

Price alone doesn’t tell the full story with EmblemHealth. AM Best rates EmblemHealth Plan, Inc. C+ (Marginal) as of a July 14, 2026 upgrade from C (Weak) — still notably weaker than the other major carriers on the New York Medigap table. Enrollment for this product is also a direct paper application rather than carrier-assigned broker support. That’s worth weighing carefully against any premium advantage.

What happens if I don’t reach the High Deductible Plan G deductible in a given year?

You simply carry forward to the next year having paid less overall than you would have on a standard plan, and the deductible resets to the new amount each January 1. There’s no penalty and nothing rolls over — it’s purely a per-calendar-year threshold.

Can I switch between Plan G, Plan N, and HD Plan G later if my health changes?

In New York, thanks to continuous open enrollment, you generally can switch between Medigap plans and carriers without medical underwriting — which is not the case in most other states. That flexibility is exactly why it’s worth revisiting this decision periodically rather than assuming your first choice has to be your last one.

I'm Here to Help — No Charge, No Pressure

Every situation is different, and the only way to know if you’re paying more than you need to is to actually run the comparison for your specific birthdate and household. I’ll walk through Plan G, Plan N, and HD Plan G side by side with you — no pressure, no scripts.

That conversation is always free.

Paul Barrett, CMIP The Modern Medicare Agency  631-358-5793 “tel:+16313585793”

631-358-5793 “tel:+16313585793” medicare@paulbinsurance.com

medicare@paulbinsurance.com  paulbinsurance.com

paulbinsurance.com  445 Broad Hollow Rd, Melville, NY 11747

445 Broad Hollow Rd, Melville, NY 11747

631-358-5793 “tel:+16313585793” medicare@paulbinsurance.com paulbinsurance.com 445 Broad Hollow Rd, Melville, NY 11747Related reading:

Primary sources:

-

-

- New York State Department of Financial Services — Comparison of Year 2026 Community Rated Standardized Medicare Supplement Monthly Premiums, effective July 1, 2026

- Medicare.gov — Compare Medigap Plan Benefits

- Centers for Medicare & Medicaid Services — 2026 Medicare Parts A & B Premiums and Deductibles

- Centers for Medicare & Medicaid Services — F, G & J High Deductible Plan Deductible Announcement

- New York Public Health Law § 19 — Reasonable Charges for Medicare Beneficiaries (5% excess charge cap, with carve-out for certain E&M office visits); New York State Assembly and NYC HIICAP consumer fact sheets

- AM Best — Credit Rating upgrade for EmblemHealth Plan, Inc. and affiliates, published July 14, 2026 (Financial Strength Rating raised to C+ from C)

- UnitedHealthcare — Official 2026 New York AARP Medicare Supplement rate notice, published July 2025

-

Disclaimer: The Modern Medicare Agency is not connected with or endorsed by the United States government or the federal Medicare program. Rates and network information reflect data available as of July 2026 and are subject to change. Always verify current rates directly with the carrier or through the NY DFS rate look-up tool before enrolling. We do not offer every plan available in your area. Contact Medicare.gov or 1-800-MEDICARE for information on all of your options.