Original Medicare is a federal health insurance program that lets you see any doctor, specialist, or hospital in the United States that accepts Medicare, with no network restrictions and no referral requirements. For people approaching Medicare eligibility, understanding why original Medicare may be better than private alternatives is the most important decision you will make before your 65th birthday. The program covers hospital care under Part A and medical services under Part B. When paired with a Medigap supplement policy, it delivers both access freedom and cost predictability that bundled plans often cannot match.

Why original Medicare may be better for provider access

Provider access is where Original Medicare separates itself most clearly. Approximately 99% of doctors who treat adults accept Medicare as of 2026. That figure means you can walk into virtually any physician’s office, specialist clinic, or hospital in the country and receive covered care without asking whether they are “in network.”

Medicare Advantage plans work differently. They contract with a specific group of providers in a defined service area. If your cardiologist leaves that network, you either pay out-of-network rates or find a new doctor. Original Medicare removes that risk entirely.

The benefits of Original Medicare for provider access include:

- No network restrictions. You choose any Medicare-accepting provider, anywhere in the country.

- No primary care referrals. You can schedule a specialist appointment directly without a gatekeeper.

- No service area limits. Coverage follows you across all 50 states, not just your home county.

- Continuity with existing doctors. If your current physician accepts Medicare, you keep them.

- Emergency coverage nationwide. Hospital care is covered wherever you travel, not just near home.

Pro Tip: If you split time between two states, such as spending winters in Florida and summers in New York, Original Medicare covers you fully in both locations. Medicare Advantage plans tied to a local network often leave travelers underinsured outside their home service area.

How does cost exposure compare between Original Medicare and Medicare Advantage?

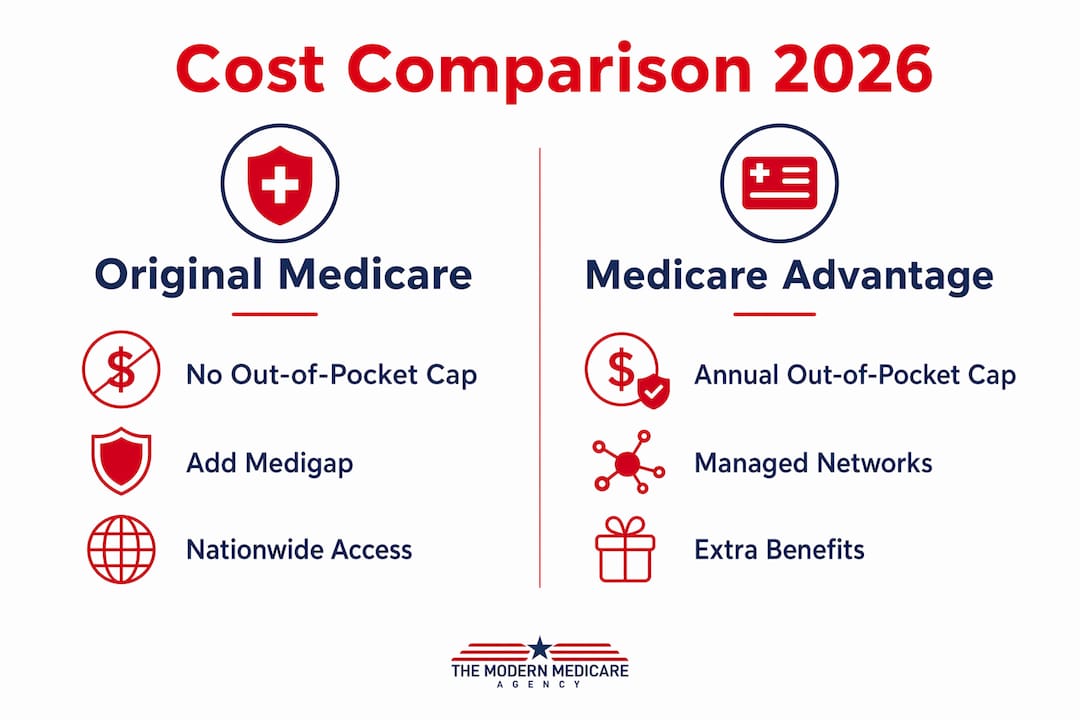

Cost is the most misunderstood part of this comparison. Original Medicare Parts A and B carry no annual out-of-pocket spending cap. Medicare Advantage plans, by contrast, are required by the Centers for Medicare and Medicaid Services to cap in-network spending at $9,250 in 2026. That cap sounds protective, but it only applies to in-network care.

The absence of a cap in Original Medicare is a real financial risk if you go without supplemental coverage. The solution is a Medigap policy, also called a Medicare Supplement plan. Medigap covers most or all of the coinsurance, copays, and deductibles that Original Medicare leaves unpaid. The result is a predictable monthly premium with very little surprise billing.

| Cost element | Original Medicare with Medigap | Medicare Advantage |

|---|---|---|

| Annual out-of-pocket cap | Varies by Medigap plan; Plan G covers most costs | $9,250 in-network maximum (2026) |

| Network restrictions | None | In-network required for lowest costs |

| Prior authorization | Rarely required | Frequently required |

| Monthly premium | Part B premium plus Medigap premium | Often lower or $0 premium |

| Specialist access | Direct, no referral | Often requires referral |

Pro Tip: The Initial Enrollment Period is the only time you are guaranteed the right to buy any Medigap policy regardless of your health history. Miss that window and insurers can deny you coverage or charge higher premiums based on pre-existing conditions. Enroll in Medigap the moment you go on Medicare Part B.

Original Medicare beneficiaries also report fewer cost-related barriers to care than those in Medicare Advantage plans, with 15% versus 19% reporting such barriers in recent studies. That gap reflects the real-world friction that network rules and prior authorizations create. Understanding Medigap costs before you enroll puts you in a much stronger position.

What administrative differences affect your care timelines?

Original Medicare rarely requires prior authorizations for covered services. You schedule care, receive it, and Medicare pays its share. That simplicity is not a minor convenience. It is the difference between getting a procedure in two weeks and waiting two months while an insurer reviews paperwork.

Medicare Advantage plans frequently require prior authorizations, and denial rates cause real delays in care. A surgeon may be ready to operate, but the plan needs to approve the procedure first. That approval process can take days or weeks, and denials require appeals that add more time.

The administrative advantages of Original Medicare include:

- No prior authorization for most services. Covered care is approved by definition, not by a private insurer’s review team.

- Stable coverage rules year to year. As a federal program, Original Medicare does not change its networks or benefits annually the way private plans do.

- No forced plan switching. Medicare Advantage plans can alter provider networks, drug formularies, and cost-sharing each january, sometimes forcing you to change doctors or pay more.

- Consistent specialist access. Your relationship with a specialist does not depend on whether that specialist renews a contract with a private insurer.

Coverage stability is a documented benefit of Original Medicare for continuity of care. Private Medicare Advantage plans are managed by insurance companies whose business priorities can shift. Original Medicare’s rules are set by federal law and change only through an act of Congress.

Who benefits most from choosing Original Medicare?

The original Medicare advantages are not universal. They matter most to specific groups of people, and recognizing whether you fall into one of those groups makes the decision much clearer.

-

Frequent travelers and snowbirds. If you spend significant time in more than one state, nationwide coverage without service area limits is a major practical benefit. Medicare Advantage plans often deny or charge more for out-of-network care outside their designated areas.

-

People with established specialist relationships. If you already see a cardiologist, oncologist, or rheumatologist you trust, Original Medicare lets you keep that relationship without worrying about network changes.

-

Those who value predictable rules. If you want to know exactly what your coverage looks like next year without reviewing a new plan document every october, Original Medicare delivers that stability.

-

People managing serious or complex health conditions. When you need frequent specialist visits, imaging, or procedures, avoiding prior authorization delays can directly affect your health outcomes.

-

Those willing to add Medigap coverage. The original Medicare coverage options work best when paired with a Medigap policy. Beneficiaries who enroll in Medigap during their Initial Enrollment Period get guaranteed coverage regardless of health history.

Medicare Advantage plans do offer extra benefits like dental, vision, and hearing that Original Medicare does not cover. That trade-off is real. But for people who prioritize access, stability, and freedom from administrative delays, Original Medicare paired with Medigap and a standalone Part D drug plan is the stronger combination.

Key Takeaways

Original Medicare paired with a Medigap policy delivers nationwide provider access, stable coverage rules, and fewer administrative delays than Medicare Advantage plans for most beneficiaries.

| Point | Details |

|---|---|

| Nationwide provider access | 99% of adult-treating doctors accept Medicare, with no network or referral restrictions. |

| Medigap fills the cost gap | Enrolling in Medigap during Initial Enrollment Period guarantees coverage and controls out-of-pocket costs. |

| Fewer administrative delays | Original Medicare rarely requires prior authorizations, reducing care delays compared to Medicare Advantage. |

| Stable coverage year to year | Federal rules govern Original Medicare, so networks and benefits do not change each january. |

| Best fit for travelers and complex cases | Snowbirds, frequent travelers, and those with specialist relationships benefit most from Original Medicare. |

What I tell every client who asks me this question

After nearly two decades helping Medicare beneficiaries, I have seen the same pattern repeat itself. People choose Medicare Advantage because the $0 premium sounds like a great deal. Then, a year or two later, they call me frustrated because their surgeon needs prior authorization, their specialist left the network, or the plan changed its cost-sharing in january and nobody told them clearly.

The clients who are happiest long-term are almost always the ones who chose Original Medicare with a solid Medigap plan. They pay more upfront in monthly premiums, but they never fight for approvals, they never lose their doctors to a network change, and they never get a surprise bill after a hospital stay.

The one mistake I see most often is waiting too long to enroll in Medigap. Once you miss your Initial Enrollment Period, insurers in most states can underwrite you based on health history. That means a pre-existing condition can lead to a denial or a premium so high it defeats the purpose. If you are approaching 65, Medigap enrollment timing is the single most important detail to get right.

My honest advice: match your Medicare choice to your life, not to a premium number. If you travel, see specialists, or simply want coverage that works the same way every year, Original Medicare is worth the premium difference.

— Paul

How Paulbinsurance can help you choose the right Medicare path

Choosing between Original Medicare and Medicare Advantage is not a one-size-fits-all decision. At Paulbinsurance, our team of independent Medicare specialists has been guiding beneficiaries through exactly this choice since 2007. We do not push one plan over another. We help you understand your options so you can decide with confidence.

Whether you want to understand Medicare Advantage plans in detail or explore how a Medicare Supplement plan can protect you under Original Medicare, Paulbinsurance has the expertise to walk you through both. You can also review how to choose between Medicare Advantage and Supplement plans side by side. Reach out to Paulbinsurance for a no-pressure conversation about which path fits your doctors, your budget, and your life.

FAQ

What is Original Medicare, exactly?

Original Medicare is the federal health insurance program consisting of Part A (hospital coverage) and Part B (medical services). It allows you to see any Medicare-accepting provider in the United States without network restrictions.

Does Original Medicare have an out-of-pocket spending cap?

Original Medicare Parts A and B do not include an annual out-of-pocket maximum. Most beneficiaries pair it with a Medigap policy to cap their costs and avoid large unexpected bills.

Why choose Original Medicare over Medicare Advantage?

Original Medicare offers nationwide provider access, no prior authorization requirements for most services, and stable coverage rules that do not change annually. It is the better fit for travelers, those with complex health needs, and people who value provider freedom.

Can I add drug coverage to Original Medicare?

Yes. Original Medicare does not include prescription drug coverage, but you can add a standalone Medicare Part D plan to cover your medications alongside Parts A and B.

Is it too late to switch from Medicare Advantage to Original Medicare?

You can switch to Original Medicare during the Medicare Advantage Open Enrollment Period from january 1 through march 31 each year. However, Medigap guaranteed-issue rights may not apply after your Initial Enrollment Period, so underwriting could affect your options.