Understanding AARP Medicare Supplement Plans: Who is Behind the Name?

When you see the name AARP, you likely think of a trusted advocate for seniors. It’s a name that brings a sense of security, which is why so many people are drawn to their Medicare plans. But navigating the world of aarp medicare supplement plans can feel confusing. Let’s clear up the confusion and give you the confidence to understand exactly what you are buying.

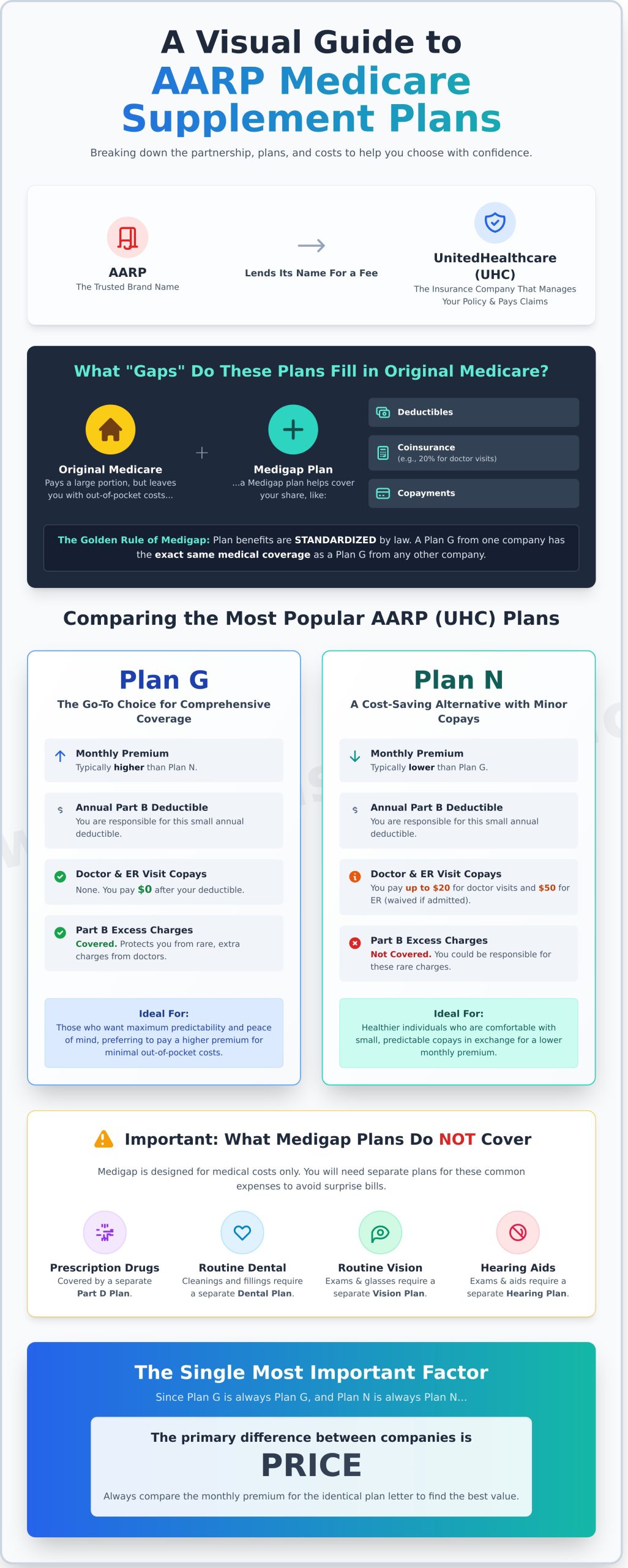

The first and most important thing to know is that these plans are designed to “fill the gaps” left by Original Medicare (Part A and Part B). Before you can even purchase one, you must be enrolled in both Part A and Part B. Once you are, a Medigap plan can help cover your share of the costs, giving you predictable expenses and peace of mind.

So, what are these “gaps”? They are the out-of-pocket costs that Original Medicare requires you to pay, such as:

- Deductibles: The amount you must pay before Medicare starts paying its share.

- Coinsurance: The percentage of costs you pay for services, like the 20% for most doctor visits.

- Copayments: Fixed amounts you pay for specific services.

The AARP and UnitedHealthcare Partnership Explained

Here’s the secret behind the name: AARP is not an insurance company. The organization, AARP, lends its powerful and trusted brand to an insurance carrier in exchange for a royalty fee. For Medicare Supplement plans, that carrier is UnitedHealthcare (UHC), one of the largest health insurers in the country. This means that while the plan has AARP’s name on it, UnitedHealthcare is the company that underwrites your policy, processes your claims, and provides all customer service.

How Medigap Plans Are Standardized by Law

The good news for consumers is that the federal government standardized Medigap plans. This makes comparing them much simpler. Plans are identified by letters (e.g., Plan G, Plan N), and every plan with the same letter must offer the exact same basic medical benefits, regardless of the company selling it. A Plan G from AARP/UnitedHealthcare covers the same medical costs as a Plan G from any other insurer. This standardization means the primary differences between companies come down to price, rate stability, and customer service-not the core coverage.

A Deep Dive into the Most Popular AARP (UHC) Medigap Plans

Navigating the different “letter plans” can feel overwhelming, but it doesn’t have to be. Most people find their perfect fit among just a few popular options. While AARP offers several Medigap policies through UnitedHealthcare, the benefits for each plan letter are standardized by the government. This means a Plan G from one company must offer the same core benefits as a Plan G from another, a fact you can confirm on the official Medicare website. Let’s simplify the most common aarp medicare supplement plans to give you clarity and confidence.

(Note: You may also hear about Plan F. It was once the most popular plan, but due to a federal law change, it is only available to those eligible for Medicare before January 1, 2020.)

AARP Medicare Supplement Plan G: The Go-To Choice

For new Medicare beneficiaries, Plan G is overwhelmingly the most popular choice, and for good reason. It offers incredibly comprehensive coverage, picking up nearly all the costs that Original Medicare leaves behind. This includes your Part A hospital deductible and the 20% coinsurance for Part B services. Your only major out-of-pocket medical expense is the annual Part B deductible. Once you meet that, the plan pays 100% of Medicare-approved costs for the rest of the year. It’s ideal for those who want predictable costs and true peace of mind.

AARP Medicare Supplement Plan N: A Cost-Saving Alternative

If you’re looking for a lower monthly premium and don’t mind some small, predictable cost-sharing, Plan N is an excellent alternative. In exchange for paying less each month, you’ll have a copay of up to $20 for some doctor’s office visits and a $50 copay for an ER visit (if you aren’t admitted). It’s important to note that Plan N does not cover Part B excess charges, which are rare but can occur if your doctor doesn’t accept Medicare’s assigned rates. This plan is often a great fit for healthier individuals comfortable with a “pay-as-you-go” approach for minor costs.

Comparing AARP Plan G vs. Plan N

Seeing the key differences side-by-side can make the choice much clearer. The decision often comes down to your personal financial philosophy.

| Feature | Plan G | Plan N |

|---|---|---|

| Monthly Premium | Higher | Lower |

| Part B Deductible | You pay | You pay |

| Doctor Visit Copays | $0 | Up to $20 |

| ER Visit Copays | $0 | $50 (waived if admitted) |

| Part B Excess Charges | Covered | Not Covered |

Do you prefer to pay a higher, fixed premium each month for maximum predictability (Plan G)? Or would you rather save on premiums and pay small, occasional copays when you see a doctor (Plan N)? There is no single right answer, only the one that best fits your health needs and budget. Not sure which is right? An independent Medigap expert from The Modern Medicare Agency can help you decide.

The Pros and Cons of Choosing an AARP-Branded Plan

When you see the AARP name, it often brings a feeling of trust and familiarity. It’s a powerful brand that has served seniors for decades. But when it comes to your healthcare coverage, it’s crucial to look past the name and analyze the real value. Are you getting the best deal for your money, or are you simply paying for a well-known logo? Let’s break it down with a clear, unbiased look.

The most important thing to understand is that Medicare Supplement (Medigap) plans are standardized by the federal government. This means a Plan G from one company offers the exact same core medical benefits as a Plan G from another. The only differences are the monthly premium, the company’s customer service, and its history of rate increases.

Potential Advantages of AARP/UHC Plans

- A Name You Know: For many, there’s immense peace of mind in choosing a brand they’ve trusted for years. This sense of security is a significant, though intangible, benefit.

- Financial Strength: The plans are underwritten by UnitedHealthcare, one of the largest and most financially stable insurers in the country. You can be confident they have the resources to pay claims.

- Member Perks: Policyholders often get access to extra benefits, such as the Renew Active® fitness program, which provides gym memberships at no additional cost.

Potential Disadvantages to Consider

- Often Higher Premiums: When you compare quotes, you’ll frequently find that AARP Medicare Supplement plans are not the lowest-cost option in many states for the same standardized coverage.

- The “Brand Tax”: You might be paying a higher monthly premium for the brand name and perks like a gym membership that you could potentially purchase separately for less.

- Rate Increases: While all Medigap rates increase over time, starting with a higher premium means future percentage-based increases will result in a larger dollar amount, further widening the cost gap between it and more competitive plans.

Ultimately, the decision comes down to personal value. AARP and UnitedHealthcare offer a stable, reliable product with some nice perks. However, an independent broker can show you quotes from other A-rated companies that provide the exact same coverage, often for a significantly lower monthly premium. Our goal is to give you the clarity to decide if the comfort of a familiar name is worth the extra cost over the lifetime of your policy.

How to Find Your Best-Value Medigap Plan

While it’s wise to research popular options like AARP Medicare Supplement plans, the secret to finding the best value isn’t loyalty to one brand-it’s adopting a smart shopping strategy. Medigap plans are standardized by the federal government. This means a Plan G from one company offers the exact same medical benefits as a Plan G from any other company. The only difference is the price you pay.

Insurance carriers set your monthly premium based on a few key factors:

- Your age and gender

- Your location (ZIP code)

- Your use of tobacco

Because each company weighs these factors differently, the price for identical coverage can vary dramatically. This is where comparing your options becomes essential to protecting your retirement savings.

Why You Must Compare Carriers

The monthly premium for the same Medigap Plan G can differ by $30, $50, or even more depending on the carrier. That can easily add up to over $600 in savings per year and thousands of dollars over your lifetime. Some companies also have a history of more stable rates than others. An independent broker can provide all of these quotes and rate histories in one simple, clear comparison, saving you time and giving you peace of mind.

What an Independent Broker Does For You

Navigating this process alone can be overwhelming. As your dedicated advocate, we simplify the entire process. We are independent brokers, which means we work for you, not for any single insurance company. Our goal is to find the right plan for your needs at the most competitive price.

- We shop the market for you: We compare rates from over 40 top-rated carriers, including AARP/UnitedHealthcare, to find your best value.

- Our service is always free: You get expert, unbiased guidance at no cost, and there is never any pressure or obligation to enroll.

- You get unbiased advice: We provide straightforward recommendations based on your unique situation, ensuring you make a decision with confidence.

Stop wondering if you’re overpaying. Let us help you find the best coverage at the best price. Get your free, unbiased Medigap quote comparison today.

What AARP Medigap Plans Don’t Cover (And How to Fill Those Gaps)

One of the biggest sources of confusion-and unexpected bills-comes from assuming your Medicare Supplement plan covers everything. While aarp medicare supplement plans offer fantastic protection against major medical costs, they are designed to fill the “gaps” in Original Medicare, not to cover services that Medicare itself excludes. Understanding these limitations is the key to building a truly comprehensive healthcare strategy and achieving complete peace of mind.

Let’s clear up two of the most common coverage gaps so you can plan with confidence.

Prescription Drug Coverage

This is the most critical point to understand: Medigap plans sold after 2006, including all current AARP plans, do not include prescription drug coverage. To get help with the cost of your medications, you must enroll in a separate, standalone Medicare Part D plan. Delaying your Part D enrollment can lead to a permanent late enrollment penalty, a monthly fee that gets added to your premium for as long as you have coverage. Securing a Part D plan when you first become eligible is the simplest way to avoid this lifelong extra cost.

Routine Dental, Vision, and Hearing

Original Medicare does not cover routine care for your teeth, eyes, or ears. This means cleanings, fillings, eye exams, glasses, and hearing aids are all out-of-pocket expenses. Since Medigap only supplements Medicare-approved services, these are not covered by aarp medicare supplement plans either. This is a significant difference when compared to some all-in-one Medicare Advantage plans, which often bundle these benefits. The solution for Medigap enrollees is to purchase affordable, standalone dental insurance plans, which can also include vision and hearing benefits.

Building your complete health coverage doesn’t have to be a stressful puzzle. As your independent broker, our mission is to provide the trusted, unbiased guidance you need to find the right pieces for your unique situation. We ensure there are no surprises, just simple, effective protection. If you have questions about rounding out your coverage, we’re here to help.

Your Next Step to Medicare Confidence

Choosing a Medigap plan is a major decision for your health and financial future. We’ve seen that while the AARP Medicare Supplement plans from UnitedHealthcare are a popular and reliable choice, they aren’t the only option. The most important takeaway is this: the best plan for you might not be the one with the most familiar name. True peace of mind comes from knowing you’ve compared the market to find the best possible value.

Navigating this alone can feel overwhelming, but you don’t have to. As an independent agency, our loyalty is to you, not an insurance company. We provide the unbiased advice you need to compare over 40 top-rated carriers at once, ensuring you see the full picture. Our guidance is always free, and our only mission is to help you find the right coverage with clarity and confidence.

Take the first step toward securing your healthcare future. Schedule a free, no-pressure call to compare all your Medigap options. We’re here to make it simple.

Frequently Asked Questions About AARP Medicare Supplement Plans

Do I have to be an AARP member to get their Medicare Supplement plan?

Yes, you must have an active AARP membership to enroll in a Medicare Supplement plan offered through UnitedHealthcare. Fortunately, becoming a member is a simple and inexpensive step. You can join before or during your application process. Membership is available to anyone age 50 or older, so you do not need to be retired to qualify for the insurance products and other benefits that AARP offers its members.

How much do AARP Medicare Supplement plans cost?

The cost of AARP Medicare Supplement plans varies significantly based on several key factors. Your monthly premium is determined by your location (zip code), age, gender, and the specific plan you select (such as Plan G or Plan N). Because rates are not one-size-fits-all, the only way to know your exact cost is to get a personalized quote. This allows you to accurately compare the options available in your state and choose a plan that fits your budget.

Are AARP/UHC Medigap rates stable or do they increase every year?

You should expect your AARP/UHC Medigap premium to increase over time. Most of these plans use an “attained-age” pricing model, which is common in the industry. This simply means your rate is based on your current age and will rise as you get older. These annual age-based adjustments are typical for this type of plan, in addition to potential increases due to inflation. Understanding this helps you budget for your healthcare costs with confidence and no surprises.

Can UnitedHealthcare drop me from my AARP Medigap plan?

No, you cannot be dropped from your plan as long as you continue to pay your premiums. All Medigap policies, including those from AARP/UnitedHealthcare, are “guaranteed renewable.” This is a critical protection that provides lasting peace of mind. It means that regardless of any health conditions you may develop, your coverage is secure. The insurance company cannot cancel your policy for any health-related reason, ensuring you have reliable protection when it matters most.

What is the difference between an AARP Medigap plan and an AARP Medicare Advantage plan?

Navigating the difference is a common source of confusion, but it’s quite simple. An AARP Medigap plan works *with* Original Medicare to pay for costs that Medicare doesn’t cover, like copayments and deductibles. It gives you the freedom to see any doctor nationwide who accepts Medicare. In contrast, an AARP Medicare Advantage plan is an *alternative* to Original Medicare. It bundles your benefits into one plan, typically with a local provider network you must use for care.

When is the best time to enroll in an AARP Medigap plan?

The absolute best time to enroll is during your Medigap Open Enrollment Period. This is a one-time, six-month window that begins on the first day of the month you are both 65 or older and enrolled in Medicare Part B. During this protected period, you have “guaranteed issue rights.” This means an insurance company cannot deny you coverage or charge you more based on your health history. Enrolling at this time is the key to avoiding costly mistakes.