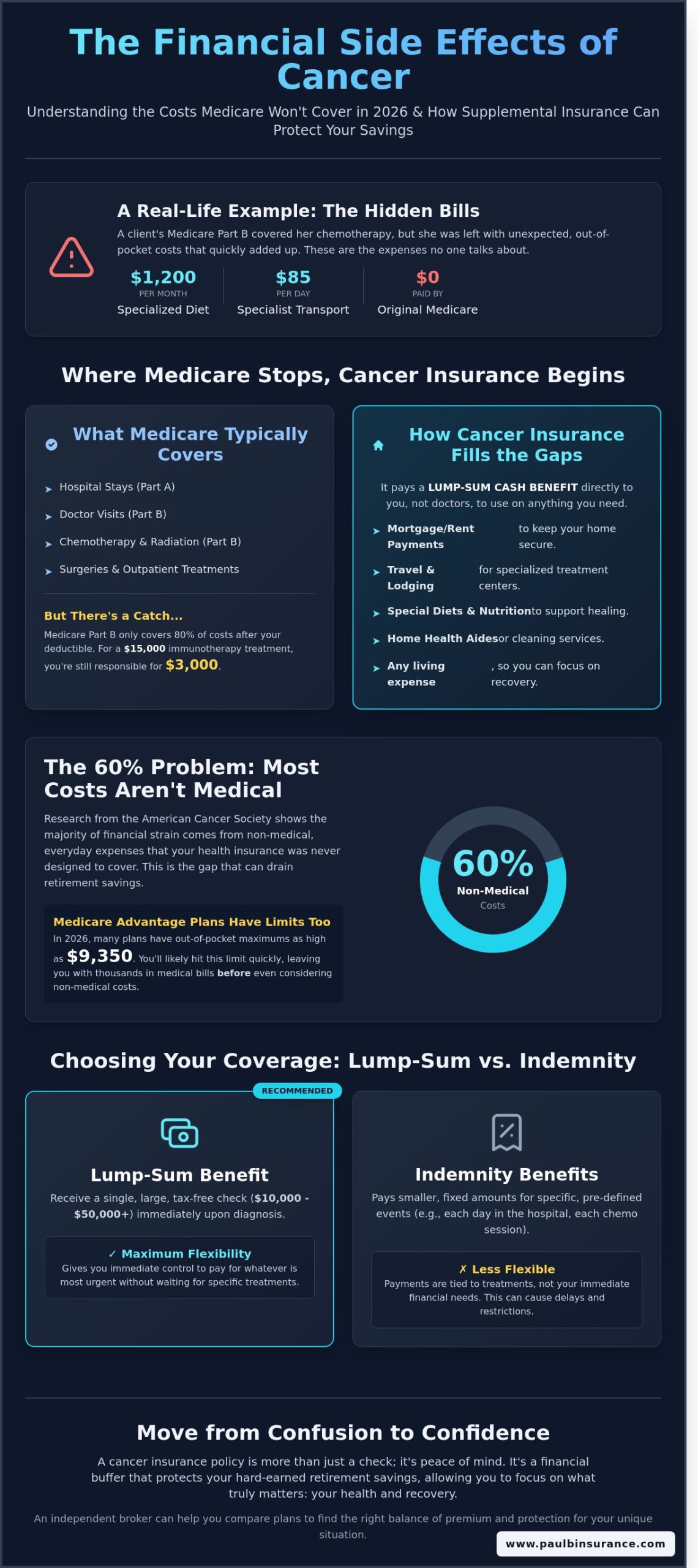

Last Tuesday, a client named Martha sat in our office, holding a stack of bills that Medicare simply wouldn’t touch. While her 2026 Medicare Part B coverage was handling her chemotherapy treatments, it didn’t pay for the $1,200 monthly specialized diet her doctor recommended or the $85 daily transportation costs to the city’s top oncology center. This is where cancer insurance steps in. It’s not about paying the doctors; it’s about protecting the life you’ve built from the expenses no one talks about.

We know you’ve spent decades saving for a peaceful retirement, and the thought of a single diagnosis draining your bank account is deeply unsettling. You deserve to focus on healing, not on whether you can afford your mortgage. In this guide, we’ll explain how these supplemental policies act as a financial buffer alongside your 2026 Medicare benefits to keep your savings intact. You’ll learn exactly what those hidden costs look like, how to evaluate if the monthly premium fits your budget, and how to avoid buying more coverage than you actually need.

Key Takeaways

- Understand why a cash-benefit plan is the essential financial shield you need to protect your hard-earned savings from unexpected costs.

- See exactly where Medicare stops and where supplemental coverage begins, so you aren’t left facing high out-of-pocket bills alone.

- Learn how to weigh 2026 premiums against your personal risk to see if cancer insurance is a smart investment for your peace of mind.

- Follow our simple 2026 checklist to evaluate your family history and genetic risks with total clarity.

- Discover how we help you move from confusion to confidence, providing unbiased guidance that is never rushed and never pressured.

What is Cancer Insurance and How Does it Work in 2026?

If you’ve spent any time looking at your Medicare options lately, you’ve likely seen the term “dread disease policy.” This is a specific type of coverage designed to handle one thing: the massive financial impact of a serious illness. What is cancer insurance? Put simply, it’s a safety net that sits alongside your regular health plan. While your medical insurance pays the surgeons and hospitals, this supplemental plan pays you directly. In 2026, we’re seeing more seniors than ever ask for these plans because they want to avoid the stress of unexpected bills during a vulnerable time.

Traditional health insurance has a very specific job. It covers doctors, hospital stays, and prescriptions. However, a gap exists that most people don’t realize until they’re in the middle of a health crisis. In 2026, the average out-of-pocket maximum for many Medicare Advantage plans has reached $8,500 or more. This is where cancer insurance steps in. It doesn’t care about your deductible or your co-pays. It provides a financial cushion, giving you a pool of money to use however you see fit. We believe this choice offers the ultimate peace of mind, especially when you’re focusing on recovery instead of debt.

Lump-Sum vs. Indemnity Benefits

You’ll usually choose between two different styles of coverage when selecting a policy. The lump-sum model is the most straightforward. You receive a single, one-time check, often ranging from $10,000 to $50,000, immediately upon a confirmed diagnosis. The indemnity model works differently; it pays out smaller amounts based on specific events like a chemotherapy session or a hospital stay. For the seniors we work with, we typically recommend the lump-sum model. It provides maximum flexibility, allowing you to pay for whatever is most urgent at that moment without waiting for a specific treatment to occur.

The “Hidden” Costs of a Cancer Diagnosis

The medical bills are only part of the story. Research from the American Cancer Society and recent 2025 data shows that 60% of the total costs associated with cancer are actually non-medical. Medicare is great, but it won’t pay for your gas to drive to a specialist three towns away. It won’t cover a home health aide to help with daily chores while you’re fatigued from treatment. These “hidden” costs add up fast. We’ve seen clients use their cash benefits for:

- Mortgage or rent payments to keep the home secure during a leave of absence.

- Travel and lodging for experimental treatments at specialized clinics.

- Nutritional supplements and organic groceries that support a healing body.

- Professional cleaning services to maintain a sterile home environment.

Having this money available means you don’t have to drain your retirement savings to cover these everyday needs. Our goal is to move you from confusion to confidence, ensuring you have the resources to fight your battle without financial fear. By choosing an independent broker, you gain access to a wide variety of these plans, ensuring you aren’t stuck with the limited options of a captive agent. We simplify the jargon so you know exactly how your protection works before you ever need it.

Medicare vs. Cancer Insurance: Do You Really Need Both?

We often hear our clients say, “I thought Medicare covered everything.” It’s a natural assumption; you’ve worked hard and paid into the system for years. However, the reality of 2026 healthcare is that Medicare has specific boundaries. While Medicare Part A handles your hospital stays and Part B covers doctor visits and outpatient treatments like chemotherapy, it doesn’t cover 100% of the costs. Part B usually leaves you responsible for 20% of the bill. When a single round of modern immunotherapy can cost $15,000, that 20% adds up to a $3,000 bill every single time.

This is where a Medicare Supplement (Medigap) plan usually steps in to pay that 20% coinsurance. It’s a fantastic tool for medical bills, but cancer creates a financial ripple effect that goes far beyond the doctor’s office. According to the American Cancer Society, many patients face significant “indirect” costs that standard insurance simply won’t touch. These are the lifestyle expenses that can lead to debt even if your medical bills are paid. Cancer insurance is designed to provide a cash benefit directly to you, helping you manage the world outside the hospital room.

Where Medicare Advantage Falls Short

In 2026, many Medicare Advantage Plans have out-of-pocket maximums reaching as high as $9,350 for in-network services. If you receive a cancer diagnosis, you’ll likely hit that maximum limit within the first few weeks of treatment. We’ve seen many seniors struggle with high deductibles in 2026 plans before their coverage even begins. A cancer policy acts as a safety net, providing the funds to “offset” these high costs so your savings remain intact. If you’re unsure how your current plan stacks up, we can help you review your benefits to find any hidden risks.

The Medigap Gap: What a Supplement Won’t Pay For

It’s vital to understand that Medigap only pays for expenses that Medicare approves first. It won’t pay for a hotel stay if you need to travel to a specialized clinic three towns over. It won’t replace your spouse’s lost wages if they need to take time off work to be your caregiver. It won’t pay for the specialized organic diet or home modifications you might need during recovery. We view cancer insurance as the missing piece of a total protection strategy, filling the gaps that even the best medical plans leave behind. It gives you the freedom to focus on getting well, rather than worrying about the mortgage or the utility bills.

We believe that clarity is the best cure for the anxiety that comes with insurance planning. By looking at these two types of coverage as partners rather than competitors, you can build a shield that protects both your health and your hard-earned retirement savings. Our goal is to move you from a state of confusion to a state of absolute confidence, knowing that every potential cost is accounted for before you ever need to use your benefits.

Evaluating the Real Cost: Is the Premium Worth the Peace of Mind?

Deciding if cancer insurance makes sense for your budget starts with looking at the actual numbers we’re seeing in 2026. For most of our clients entering the Medicare system this year, a solid lump-sum policy costs between $28 and $54 per month. This isn’t a random price. It’s a calculated rate based on three specific levers: your current age, your history with tobacco, and the total benefit amount you want delivered to your door. We’ve seen that rates typically jump by 25% or more if you’ve used nicotine products in the last 12 months, as insurers in 2026 have tightened their underwriting rules.

We suggest a simple “Self-Insurance” test to see if this coverage fits your life. Ask yourself honestly: Could I comfortably write a check for $20,000 tomorrow to cover unexpected travel, specialized home care, or my spouse’s lost wages while they care for me? If that question makes your stomach sink, the monthly premium is a small price for a guaranteed safety net. We don’t want you to buy the most expensive plan on the shelf. Instead, we focus on right-sizing your coverage. For 84% of the families we serve, a $10,000 or $20,000 lump sum provides exactly the cushion they need without overstressing their monthly retirement budget.

The hidden danger of a serious diagnosis isn’t just the medical bill. Research has shown that the financial toxicity of cancer care impacts daily living long after the initial doctor visits end. This is why we view these plans as a tool for your protection, ensuring you don’t have to choose between your health and your savings. We help you look at your fixed income and find a plan that feels like a relief, not a burden.

- Age 65 Non-Smoker: Average premiums range from $30 to $45 for a $15,000 benefit.

- Tobacco Use: Expect a significant premium increase, often 1.5 times the standard rate.

- Benefit Choice: Most 2026 contracts allow you to choose between $5,000 and $50,000 in coverage.

When to Buy: The Age and Health Factor

Waiting for a health scare to happen before you apply is a mistake that 18% of applicants make too late every year. By the time a doctor orders a diagnostic biopsy, the door to traditional coverage usually slams shut. In 2026, most insurance carriers use a strict five year look-back period for your medical history. If you’ve had a cancer diagnosis or even certain high-risk screenings since 2021, you might be ineligible. We find the sweet spot for enrollment is during your initial Medicare transition at age 65. It’s the moment when your health is documented, your options are widest, and your rates are locked in at a lower entry point.

Common Policy Exclusions to Watch For

You need to know exactly what your contract says before you sign. Most 2026 policies exclude non-melanoma skin cancers, such as basal cell or squamous cell carcinomas, because they are usually treated with simple outpatient procedures. If you’re looking for a payout for these common issues, you won’t find it here. Also, pay close attention to the 90 day waiting period standard in today’s contracts. If a diagnosis occurs within the first three months of the policy, the company won’t pay the benefit. We help you navigate this fine print so you have total confidence in how your plan works when you need it most.

A Simple 2026 Checklist: Should You Apply for Cancer Insurance?

Deciding on extra protection shouldn’t feel like a guessing game. We want to help you move from confusion to confidence by looking at your actual needs for 2026. Cancer insurance isn’t for everyone, but for many seniors, it’s the difference between focusing on recovery and worrying about the mortgage.

First, look at your family history. If a parent or sibling was diagnosed before age 65, your statistical risk is higher. In 2026, genetic screenings are more common, but they don’t pay the bills if a diagnosis occurs. Second, check your bank account. If your current Medicare plan has a high out-of-pocket maximum, do you have $6,000 to $9,000 in liquid savings ready for an emergency? Most 2026 Medicare Advantage plans have out-of-pocket limits near $8,900 for in-network care. If that number feels uncomfortable, a policy makes sense.

Don’t forget to review any “gap” coverage. Some union or former employer plans from the early 2010s still offer retiree benefits. However, we’ve seen 14% of these employer “legacy” plans reduced or eliminated in the last two years alone. If your old employer changed their benefits recently, you might have a hole in your safety net you didn’t know existed. We’ll help you spot those gaps before they become a problem.

Questions to Ask Yourself Before Calling an Agent

We believe in being prepared. Before we talk, take a moment to answer these three questions honestly. They help us understand if cancer insurance is a necessity for your household. “If I couldn’t drive myself to treatment, who would pay for my transportation?” “Does my current Prescription Drug Plan cover the newest oral chemo medications?” “Is my spouse still working, or are we relying solely on fixed income?”

Comparing Carriers: Why an Independent View Matters

A “Captive Agent” works for one company and can only show you one price. This is a major disadvantage for you. If that one company doesn’t fit your health history, you’re stuck. We compare over 40 different carriers to find the one that fits your specific profile. We’re your year-round advocate. If you have a claim later, you call us, not a 1-800 number. We simplify the jargon so your cancer insurance makes sense.

Ready to see which of our 40 carriers offers the best protection for your budget? Schedule a Call With Paul to get your personalized 2026 comparison today.

Moving From Confidence to Clarity with The Modern Medicare Agency

We know that looking at insurance can feel like trying to find your way through a thick fog. Our philosophy is simple: we are never rushed and never pressured. We act as your guides because we believe you deserve clarity before you sign anything. We take the time to strip away the confusing industry talk so you understand exactly what you are buying. Whether it’s explaining how a 2026 policy pays out or clarifying the fine print on a specific rider, we make sure you’re the expert on your own coverage. We don’t want you to just have a policy; we want you to have peace of mind.

During our personalized Medicare Protection Review, we look at your current health plan to find where you might be exposed. Medicare is a strong foundation, but it doesn’t cover every cost. By including cancer insurance in this review, we help you build a safety net that catches the expenses Medicare leaves behind. Paul Barrett always says that insurance isn’t just about paying bills; it’s about protecting the legacy you’ve worked 40 years to build. We want you to focus on your family and your health, not your bank account balance. Since 2024, the out-of-pocket costs for specialized oncology drugs have risen by 14 percent, making this review more vital than ever.

How We Help You Choose Without the Stress

We use a proven 5-step process to move you from overwhelmed to secure. First, we listen to your health history and financial goals. Second, we analyze your current 2026 Medicare plan for gaps. Third, we compare cancer insurance options from over 15 top-rated carriers. Fourth, we explain the “why” behind each recommendation in plain English. Finally, we handle the entire enrollment process for you. Because we are independent brokers, we don’t work for the big insurance companies. We work for you. This unbiased status means we prioritize your budget over a carrier’s quota. You can schedule a simple, no-obligation “Confidence Call” with our team today to start this journey.

Total Protection Beyond Cancer

A worry-free retirement requires looking at the whole picture. While cancer protection is vital, other gaps can be just as expensive for seniors in 2026. Many of our clients find that adding Dental Insurance is a smart move to cover routine care and major procedures that traditional Medicare often ignores. Taking a holistic approach ensures that a sudden tooth ache or a long-term illness won’t drain your savings. We’ve helped over 3,000 families since our founding by looking at these small details that make a big difference. Our goal is to make sure you can enjoy your retirement without looking over your shoulder. Schedule your call with Paul today and let’s get your plan in place.

Your Path to Clarity and Protection in 2026

Navigating the healthcare landscape in 2026 doesn’t have to feel like a walk through a maze. We’ve seen how Medicare often leaves gaps in coverage, specifically regarding non-medical costs that can quickly add up. By using our 2026 checklist, you’ve learned that cancer insurance acts as a vital safety net, providing cash when you need it most. We believe that your focus should stay on recovery, not on how you’ll manage a high deductible or travel expenses for specialized treatment.

At The Modern Medicare Agency, we’re here to guide you from confusion to confidence. We represent over 40+ carriers to ensure you have unbiased choices; additionally, we’re licensed in 34+ states to provide nationwide expertise. Our 5-star rated process is designed to be simple and stress-free because you deserve a partner who fights for your best interests. We’ll help you skip the enrollment mistakes and find a plan that fits your life perfectly.

Schedule a Call With Paul to Find Your Perfect Plan

You don’t have to figure this out alone. We’re ready to help you secure the peace of mind you deserve for the year ahead.

Frequently Asked Questions

Is cancer insurance a waste of money if I already have Medicare?

No, cancer insurance isn’t a waste because Medicare leaves gaps in your coverage. While Medicare handles hospital stays, it doesn’t pay for your mortgage, transportation to treatments, or specialized home care. In 2026, the average Part B deductible is $257, and many specialty drugs require a 20% coinsurance that adds up fast. We help you fill these gaps so your savings stay protected while you focus on getting better.

Does cancer insurance cover pre-existing conditions in 2026?

Most policies won’t cover a cancer diagnosis if you’ve been treated for that same condition within the last 24 months. This is called a look-back period. In 2026, standard plans also include a 30 to 90 day waiting period after you buy the policy before benefits start. We recommend applying while you’re healthy to ensure you have protection in place before a health crisis begins. It’s about protecting your future self.

Can I use the cash benefit for anything I want?

You can use your cash benefit for any expense you choose without any restrictions from the insurance company. Whether you need to pay for a $2,000 flight to a specialist clinic or just need help with your monthly utility bills, the money is yours. We see clients use these funds for experimental treatments that traditional insurance won’t cover. It’s about giving you total control and peace of mind during a difficult time.

What is the average cost of a cancer insurance policy for someone over 65?

For a senior aged 65 in 2026, a standard cancer insurance policy typically costs between $35 and $62 per month. This premium usually secures a $10,000 to $20,000 lump-sum benefit. Prices vary based on your exact age and the benefit amount you choose. We compare rates from 15 different carriers to find the most affordable option for your specific budget and needs. We make sure you never pay more than necessary.

Does cancer insurance pay out for skin cancer?

Yes, most policies pay out for skin cancer, though the amount depends on the specific diagnosis. For non-melanoma cases like basal cell or squamous cell carcinoma, many 2026 policies pay a smaller benefit of $250 to $500 per procedure. If the diagnosis is malignant melanoma, you’ll typically receive the full 100% lump-sum benefit. We’ll help you read the fine print so there are no surprises during your claim process.

What happens to my policy if I never get cancer?

If you never receive a diagnosis, the policy simply provides peace of mind throughout your life, much like car insurance. However, some plans offer a return of premium rider that refunds 100% of your paid premiums after a set period, like 20 years. We can look at these options together to see if the extra cost is worth it for your financial plan. It’s all about your personal comfort level and goals.

How is cancer insurance different from a critical illness policy?

Cancer insurance focuses solely on cancer treatments, while a critical illness policy covers a broader range of health events. A typical critical illness plan in 2026 covers 5 to 12 major conditions; these include heart attacks, strokes, and organ failure. If you’re specifically worried about a family history of cancer, a dedicated policy is often more affordable. We’ll help you weigh these two options to ensure you aren’t paying for coverage you don’t need.