What if the decision to save twenty dollars today ends up costing you thousands of dollars over the next decade? It seems logical to skip insurance for things you don’t use, but Medicare rules work a bit differently. You might be asking, “do I need a medicare part d plan if I take no drugs?” while your health is excellent in 2026. We understand that paying for a service you don’t need feels like a waste of your hard-earned money. It’s confusing to see jargon like “late enrollment penalties” when you just want to stay healthy and keep your costs low.

We want to move you from confusion to confidence by explaining the real math behind the 1% monthly penalty that lasts a lifetime. In this guide, we’ll show you how to secure a low-cost safety net plan that protects your wallet from future health changes and government surcharges. You will discover exactly how the 2026 Medicare updates affect your choices and how our team helps you find the cheapest way to stay compliant. Let’s look at the specific risks of going without coverage and the simple steps to avoid a permanent financial mistake.

Key Takeaways

- Understand why skipping prescription coverage today can lead to permanent, growing penalties that follow you for the rest of your life.

- If you are wondering, “do I need a medicare part d plan if I take no drugs,” we explain the “placeholder strategy” that provides a low-cost safety net.

- Discover how the landmark 2026 changes, including the new $2,000 annual out-of-pocket maximum, offer you more protection than ever before.

- Learn how we compare over 40 different carriers to find you a budget-friendly plan that protects your future without charging for extras you don’t need yet.

- Follow our simple 5-step process to move from confusion to confidence, ensuring you steer clear of expensive enrollment mistakes.

Do You Really Need Medicare Part D If You Take No Medications?

One of the most frequent questions we hear from healthy seniors is: do I need a medicare part d plan if I take no drugs? It is a fair question. If your medicine cabinet is empty and you feel great, paying for a monthly insurance plan can feel like buying a ticket to a movie you have no intention of watching. We understand that every dollar counts, especially when you are managing a fixed budget in 2026.

Technically, Medicare Part D is optional. It is private insurance designed to cover the costs of prescriptions that Original Medicare does not touch. Many healthy seniors consider skipping it to save on monthly premiums, which typically range from $15 to $30 for basic plans this year. However, we rarely recommend going without it. The core conflict is a classic risk assessment. You might save $300 a year now, but you risk spending thousands of dollars later if your health changes unexpectedly.

We see our role as your advocate. Our goal is to move you from confusion to confidence by looking at the long-term picture. While you might not need a single pill today, insurance is about protecting your future self. We want to help you avoid the stress of a sudden medical bill that could have been easily prevented.

The “Optional but Essential” Nature of Drug Coverage

Medicare calls Part D “optional” because the government does not force you to sign up. Instead, they use incentives to encourage early enrollment. Part D works alongside your Medicare Part A and Part B to create a complete safety net. Your current health is simply a snapshot in time; it is not a 20-year guarantee. In 2026, with the $2,000 cap on out-of-pocket drug costs now fully in effect, having a Medicare Part D plan provides a massive financial shield that was not as strong in years past. We help you look past today’s health to ensure you are protected for whatever tomorrow brings.

When Skipping Part D Actually Makes Sense

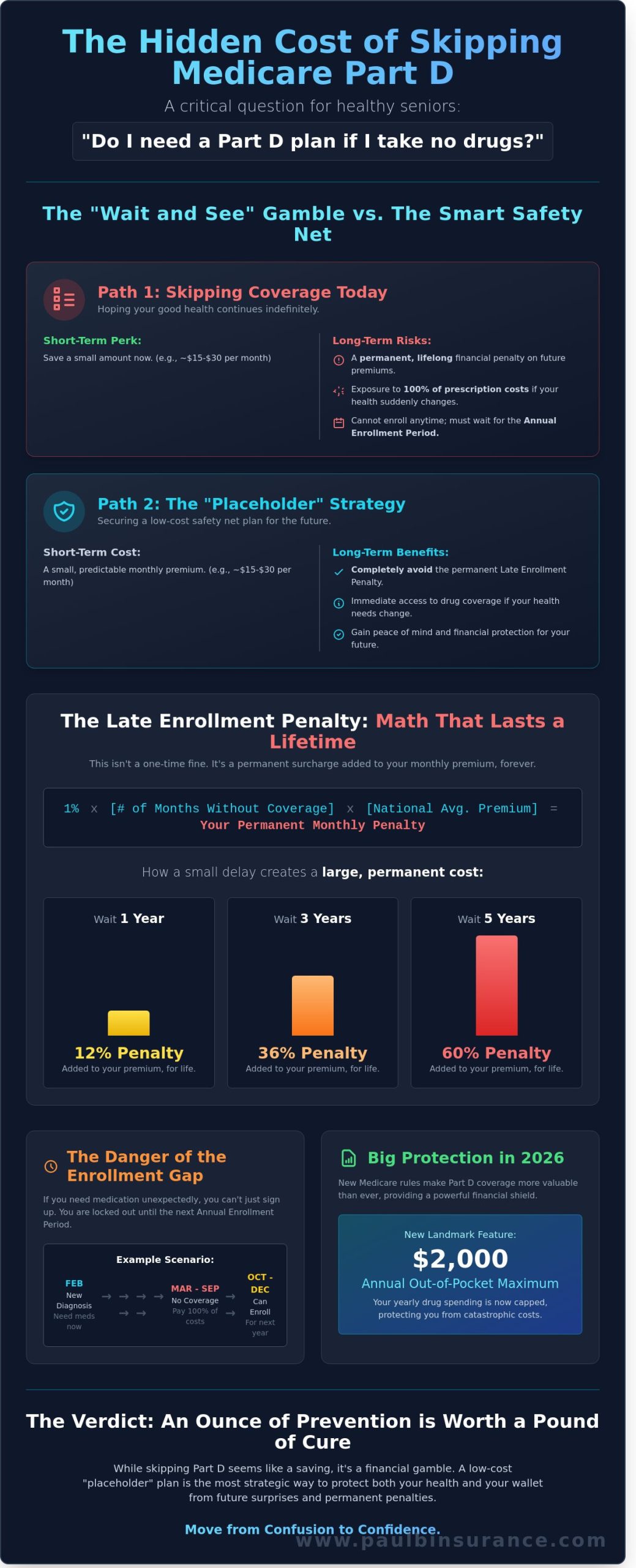

There are specific situations where skipping a standalone Part D plan is the right move. This usually happens when you already have “creditable coverage.” This is insurance, often through a former employer, a union, or the VA, that Medicare considers to be as good as or better than a standard Part D plan. When you ask, “do I need a medicare part d plan if I take no drugs,” the answer is “no” only if you can prove you have this specific type of coverage. We always tell our clients to verify this every single year. Do not assume your private plan counts. If your coverage is not officially creditable, Medicare will hit you with a lifetime late enrollment penalty of 1% per month for every month you waited to join. We want to help you steer clear of these costly, permanent mistakes.

The High Cost of ‘Waiting and Seeing’: Penalties and Risks

It feels logical to save money when you aren’t using a service. We hear it often from seniors who feel great and want to skip the monthly premium. However, Medicare Part D works much like fire insurance; you cannot buy it while your house is already on fire. If you choose to skip coverage now, you face two major hurdles: a financial penalty that lasts a lifetime and a long period where you have no protection at all.

Many people ask us, “do I need a medicare part d plan if I take no drugs?” only to realize later that waiting can be the most expensive choice they make. Medicare views prescription drug coverage as a collective pool. When healthy people stay out of the pool, the system adds a late fee to encourage everyone to join early. We want to help you understand how these rules work so you can make a choice that protects your future budget.

How the Part D Penalty Math Works in 2026

The Late Enrollment Penalty (LEP) is not a one-time fine. It is a permanent increase in your monthly premium. For every month you go without “creditable” coverage after your initial enrollment period ends, Medicare adds 1% of the national base beneficiary premium to your bill. In 2026, this base premium is the benchmark used for every calculation. If you wait five years to sign up, you will face a 60% permanent surcharge on your premium for as long as you have a drug plan. This extra cost follows you for life, even if you switch to a different insurance company later.

The Danger of the Enrollment Gap

The financial penalty is only half of the risk. The other half is the “lock-out” period. Imagine it is February 2026. You are healthy today, but a sudden diagnosis requires a medication that costs $450 every month. If you didn’t sign up for coverage when you were first eligible, you cannot simply join a plan that afternoon. You generally have to wait for the Annual Enrollment Period, which runs from October 15 to December 7.

- Delayed Coverage: Your new plan wouldn’t actually start until January 1 of the following year.

- Retail Prices: You would be responsible for paying the full retail price for your medications for several months.

- No Negotiated Rates: Without an insurance partner, you lose access to the discounted rates that plans negotiate with pharmacies.

We see how quickly these “retail” prices can drain a savings account. Choosing a basic Medicare Part D plan now acts as a safety net. It ensures that if your health changes in 2026, you won’t be stuck paying thousands of dollars out of pocket while waiting for the calendar to reset. Our goal is to move you from confusion to confidence by securing a plan that fits your current needs while shielding you from these permanent penalties.

How Medicare Part D Has Changed in 2026

The year 2026 stands as a landmark for everyone on Medicare. Because of the Inflation Reduction Act, the rules for prescription drug coverage have been completely rewritten to favor you, the consumer. We understand that these changes might feel like just another layer of complexity in an already confusing system. Our goal is to clear away that fog and show you why these updates matter, especially when you are weighing the question: do I need a medicare part d plan if I take no drugs?

This year, Part D functions less like a discount card and more like a robust catastrophic insurance policy. We help you look past the monthly premiums to see the massive safety net now in place. If your health changes unexpectedly, you are no longer at risk of unlimited financial loss. We take the stress out of this transition by comparing the new 2026 plan structures for you; this ensures you have protection without the headache of doing the math yourself.

The $2,000 Out-of-Pocket Cap Explained

The most significant change in 2026 is the introduction of a hard $2,000 annual limit on your out-of-pocket prescription costs. Before this law took effect, a single diagnosis requiring specialty medications could easily cost a senior $10,000 or more in a single year. Now, once you hit that $2,000 threshold, your plan covers 100 percent of your covered drug costs for the rest of the year. This cap provides a level of peace of mind that simply did not exist in previous years. Even if you start the year taking zero medications, this limit acts as a shield against the high costs of modern medicine. It turns a potential financial disaster into a manageable, predictable expense.

Elimination of the “Donut Hole”

We are happy to confirm that the dreaded “donut hole,” or coverage gap, is officially a thing of the past in 2026. In previous years, you had to track different phases of coverage, which caused immense confusion and sudden price hikes at the pharmacy counter. The new, simplified structure makes it much easier for us to find your perfect match. You can learn more about these streamlined options in our Medicare Part D guide.

By removing the coverage gap, the system is finally moving from a state of chaos to one of clarity. When you ask yourself, “do I need a medicare part d plan if I take no drugs,” remember that 2026 plans are designed to be simpler, more transparent, and significantly more protective than ever before. We are here to make sure you understand every detail so you can make your choice with total confidence.

Strategic Planning: Finding a Low-Cost Safety Net Plan

If you are currently healthy and medication-free, you might ask: do I need a medicare part d plan if I take no drugs? We believe the smartest answer involves what we call a “Placeholder Strategy.” You don’t need a “Cadillac” plan with a high monthly premium if your medicine cabinet is empty. Instead, we help you find the lowest-cost option available in your specific zip code for 2026. This simple move satisfies the Medicare requirement and stops the late enrollment penalty clock immediately. It gives you a vital safety net without draining your monthly budget on services you don’t currently use.

The beauty of this approach is the built-in flexibility. Medicare allows you to change your coverage every single year during the Annual Enrollment Period. If your health changes in 2027, we can upgrade you to a plan with a more robust formulary. For now, a basic plan acts as your insurance against the unknown. In 2026, the national out-of-pocket cap for prescription drugs is set at $2,000; having even a basic plan protects you from costs exceeding that limit if a surprise diagnosis occurs mid-year. It’s about buying peace of mind for the price of a few cups of coffee a month.

Comparing Low-Premium Part D Options

When we look at basic plans, we focus on the monthly premium first. In 2026, many regions offer plans with premiums ranging from $0 to $15. While these often have a standard deductible, that number is irrelevant if you aren’t buying drugs. We use our Medicare Part D search tools to filter by the absolute lowest monthly cost. This ensures you have a “just in case” plan that keeps your record clean with Medicare while keeping your fixed costs as low as possible.

Medicare Advantage as an Alternative

Many Medicare Advantage plans include drug coverage at no extra premium cost. These “all-in-one” plans are a popular choice for healthy seniors who want to simplify their monthly bills. We help you compare the Original Medicare path against these private options to ensure you aren’t overpaying. As independent brokers, we show you every path available; unlike captive agents who only represent one company, we work for you. Our goal is to move you from confusion to confidence by showing you exactly how 2026’s rules impact your wallet.

Don’t let the fear of penalties keep you up at night. Schedule a call with Paul today to find a low-cost plan that protects your future without breaking the bank.

How We Simplify Your Medicare Journey

The 2026 Medicare landscape often feels like a maze of fine print and changing rules. We know the weight of the question, do I need a medicare part d plan if I take no drugs, especially when you’re trying to avoid permanent financial penalties. We represent over 40 different insurance carriers to ensure you get a wide-angle view of every available option. This independence allows us to provide an unbiased look at the market. We don’t work for the big insurance companies; we work for you.

Our team uses a proven 5-step process to move you from confusion to confidence. First, we listen to your specific health concerns. Second, we analyze current 2026 plan data. Third, we compare the total annual costs. Fourth, we simplify the jargon so you understand the coverage. Finally, we handle the enrollment paperwork. You’ll never feel pressured or rushed during this process. We stay by your side year-round, providing support long after the enrollment window closes. Our services are always at no cost to you, as we are your advocates for life.

The Advantage of an Independent Broker

A captive agent only shows you one slice of the pie because they’re tied to a single company’s products. That’s a limited view that often leaves better options on the table. We filter through hundreds of Medicare Part D plans to find the one that fits your specific zip code and lifestyle. With our presence in 34+ states, including New York, Florida, and California, we understand the local market shifts that occurred in early 2026. We help you see the whole picture before you sign anything.

Your Next Steps to Peace of Mind

You should never feel rushed when making decisions about your health coverage. Deciding if you should get a plan when you’re currently healthy is about risk management. If you’re still asking, do I need a medicare part d plan if I take no drugs, let’s talk about the 1% monthly penalty that could haunt your future budget. You can schedule a simple, no-obligation call with Paul or our team today. We’re here to help you protect your future self so you can enjoy retirement in 2026 without the stress of unexpected medical bills.

Secure Your Peace of Mind for 2026

Navigating the current Medicare landscape shouldn’t feel like a high-stakes gamble. While you might feel healthy today, the question of do I need a medicare part d plan if I take no drugs often comes down to avoiding the permanent 1% monthly late enrollment penalty. By securing a low-cost safety net plan now, you protect yourself from unexpected health changes and take full advantage of the $2,000 out-of-pocket maximum established by 2026 regulations. We’ve helped thousands of seniors across 34+ states move from confusion to confidence using our proven 5-step process.

Our team provides unbiased guidance from 40+ insurance carriers to ensure you aren’t overpaying for coverage you don’t use yet. You don’t have to face these complex decisions alone. We’re here to simplify the jargon and give you the clarity you deserve. Schedule a Call With Paul to find your perfect low-cost safety net plan and let’s secure your health journey together. You’ve worked hard for your retirement; we’re here to help you protect it.

Frequently Asked Questions

Is there a penalty for not having Medicare Part D if I don’t take drugs?

Yes, you’ll face a permanent late enrollment penalty if you go 63 days or more without creditable drug coverage. You might ask, “do I need a medicare part d plan if I take no drugs” when your health is perfect. However, Medicare adds 1% of the national base beneficiary premium to your monthly bill for every month you delayed. This extra charge follows you for life.

Can I wait until I need prescriptions to sign up for Part D?

You can wait, but it’s a risky move that often leads to high costs. You can typically only enroll during the Annual Enrollment Period, which runs from October 15 to December 7 each year. If you’re diagnosed with a condition in February, you might pay full price for medications for 10 months. We recommend a low cost plan to keep your options open and your costs predictable.

What is considered creditable coverage for Medicare Part D?

Creditable coverage is insurance that’s expected to pay at least as much as a standard Medicare drug plan. This includes coverage from the VA, TRICARE, or an employer group plan with 20 or more employees. You should receive a notice every September from your current provider. Keep this letter in a safe place. It’s your proof to Medicare that you don’t owe a late penalty.

How much is the Medicare Part D late enrollment penalty in 2026?

The penalty is 1% of the national base beneficiary premium for every full month you were eligible but didn’t have coverage. If you missed the deadline by 24 months, you’ll pay an extra 24% on top of your plan’s premium every month. Since the base premium usually increases slightly each year, your penalty amount also grows. It’s a small fee that adds up significantly over a decade.

What happens if I skip Part D and then get a high-cost prescription later?

You’ll be responsible for the entire retail cost of the medication until your new coverage begins the following January. In 2026, Medicare plans have a $2,000 out of pocket maximum that protects you from catastrophic costs. If you don’t have a plan, that $2,000 limit doesn’t apply to you. One specialty drug could cost you $4,500 in a single month, which is why we suggest having a plan in place.

Are there Part D plans with $0 monthly premiums?

While most standalone Part D plans have a small monthly fee, many Medicare Advantage plans include drug coverage for a $0 premium. This is a popular way to answer the question, “do I need a medicare part d plan if I take no drugs” without adding a new monthly bill. These plans satisfy Medicare’s requirements and ensure you won’t face a penalty later. We can help you compare these $0 options in your zip code.

Do I need a separate Part D plan if I have a Medicare Advantage plan?

No, you shouldn’t buy a separate drug plan if your Medicare Advantage plan already includes it. Most of these plans are “all-in-one” packages. In fact, if you try to join a standalone Part D plan, Medicare might automatically kick you out of your Advantage plan. We always check your summary of benefits first to make sure your 2026 coverage is set up correctly and safely.

How do I avoid the Part D penalty if I missed my initial enrollment?

The best way to stop the penalty from growing is to sign up during the next available enrollment window. If you had other coverage that Medicare considers creditable, we can help you submit proof to clear the penalty. If you simply forgot to sign up, we’ll find the most affordable plan available for 2026. This locks in your protection and prevents the monthly fine from getting any larger.