On January 5, 2026, Margaret opened her mailbox to find her updated Medicare premium notice, only to realize her monthly costs had climbed by 5.9 percent compared to last year. Like many seniors we speak with, she felt a familiar knot in her stomach while wondering if her nest egg could truly withstand another decade of rising medical inflation. We know that the maze of Medicare Parts A, B, C, and D feels more overwhelming than ever this year, especially as the 2026 cost of living adjustments continue to shift the ground beneath your feet.

Effective financial planning for healthcare in retirement shouldn’t feel like a source of constant anxiety or a gamble with your future. We are here to help you navigate these complex medical costs so you can protect your hard earned savings and retire with absolute peace of mind. In this guide, we provide a clear breakdown of projected 2026 expenses and a simple strategy to ensure you don’t make a costly enrollment mistake that results in permanent late penalties. It’s time to move from confusion to confidence with a plan that puts your needs first.

Key Takeaways

- Learn why 2026 projections suggest a healthy couple may need over $370,000 for medical care and how to shield your savings from rising inflation.

- We simplify the Medicare maze by breaking down the specific roles of Parts A, B, C, and D so you can build a predictable monthly budget.

- Identify the hidden “holes” in Original Medicare that lead to financial risk and discover how Medigap plans can buy back your peace of mind.

- Master financial planning for healthcare in retirement by using tax-efficient HSAs and understanding how your 2024 income levels affect your 2026 premiums.

- Move from feeling overwhelmed to empowered by following our proven five-step process designed to keep you protected, never rushed, and never pressured.

The Rising Cost of Staying Healthy: Why Healthcare is Your Biggest Retirement Variable in 2026

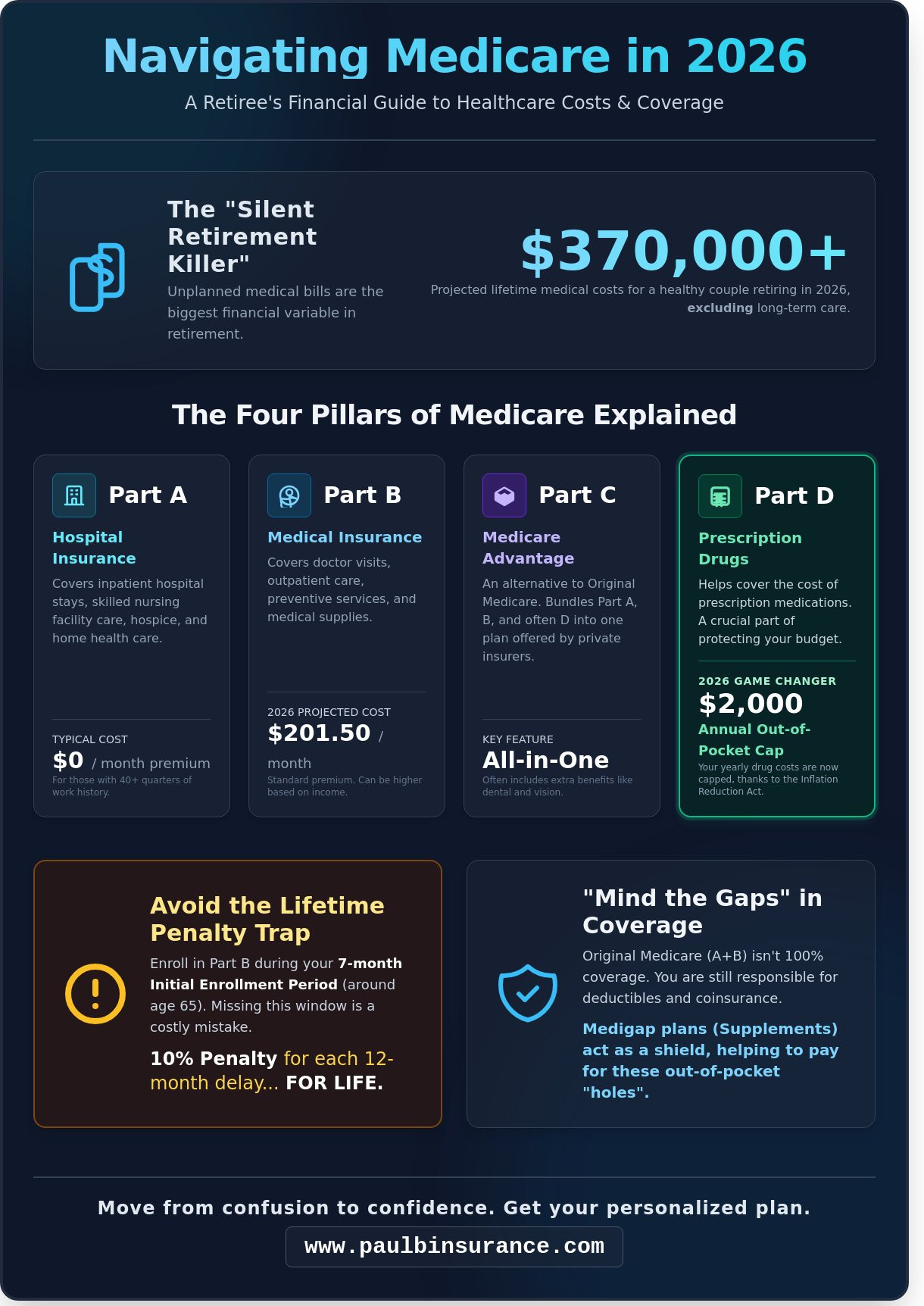

We often see retirees spend decades building a nest egg, only to watch it shrink because of a single hospital stay or a chronic diagnosis. Financial planning for healthcare in retirement is the deliberate strategy we use to protect your hard-earned assets from medical inflation. In 2026, the stakes are higher than ever. Recent industry data suggests a healthy 65-year-old couple retiring this year may need more than $370,000 to cover medical expenses throughout their lifetime. This staggering figure does not even include the potential costs of long-term care.

Think of these costs as the “Silent Retirement Killer.” Unexpected medical bills can derail even the most disciplined investment plans if you are not prepared. We help you move from confusion to confidence by teaching you to view your insurance as a financial asset. It is not just another bill to pay; it is a tool that preserves your wealth. Understanding the U.S. health insurance system is the first step in building this defense for your future.

The 2026 Healthcare Landscape

As we move through 2026, the landscape has shifted due to major regulatory changes. The full implementation of the Inflation Reduction Act now caps out-of-pocket prescription costs at $2,000 for those on Medicare. While this is a win for many, it has also caused insurance carriers to adjust their premiums and plan structures. Hoping for the best is a dangerous financial strategy for seniors. With life expectancy for a 65-year-old now frequently reaching the age of 87 or beyond, your medical budget must account for over two decades of rising costs. We often suggest reviewing your Medicare Part D options annually to ensure these shifts do not catch you off guard.

The Emotional Toll of Unplanned Expenses

Medical billing jargon often feels like a foreign language designed to confuse you. This lack of transparency creates a heavy emotional burden of stress and overwhelm. We believe clarity is the first step toward true financial security. We simplify the complex terms so you know exactly how your coverage works. You deserve to feel protected, not pressured by a system that feels like a maze. Healthcare retirement planning is the essential shield that protects your family legacy from being drained by medical debt.

Building Your Foundation: Understanding the Pillars of Medicare in 2026

Medicare often feels like a confusing maze of letters and rules. We believe that financial planning for healthcare in retirement should bring you peace of mind, not a headache. By 2026, the system has evolved to offer better protection for your wallet, but you still need a solid map to find your way through. We simplify the jargon so you know exactly how it works and how to protect your hard-earned savings.

The Core Four: A, B, C, and D

Part A and Part B form the original government foundation. Part A covers your hospital stays. Most people don’t pay a monthly premium for it because they worked at least 40 quarters. Part B covers your doctor visits and outpatient care. For 2026, the standard Part B premium is projected at $201.50 per month. This is a fixed cost we must factor into your monthly retirement budget to avoid surprises.

Part C, also known as Medicare Advantage, is an alternative way to get your coverage through private companies. We created our Medicare Advantage Guide to help you compare these bundled plans easily. Finally, Part D covers your prescriptions. The biggest win for your budget in 2026 is the $2,000 out-of-pocket cap on drug costs. No matter how expensive your medications are, you won’t pay more than $2,000 for the year. We help you look at the 2026 Part D landscape to ensure you choose a plan that includes your specific pharmacy and avoids late enrollment penalties.

Enrollment Timing and Costly Mistakes

Timing is everything when it comes to your health coverage. Your Initial Enrollment Period is a 7-month window that starts three months before you turn 65. If you miss this window, you could face a 10% lifetime penalty on your Part B premiums for every year you waited. These “late traps” drain your bank account over time, but they are completely avoidable with a bit of foresight. We recommend starting your planning at least 6 months before your 65th birthday to ensure a smooth transition.

We take pride in being independent brokers. Unlike a captive agent who only shows you products from one specific company, we shop the entire market for you. This unbiased approach is how we move you from confusion to confidence. We look at every option available in 2026 to find the one that fits your health needs and your budget. If you want to see how these pieces fit your specific situation, you can schedule a call with Paul to get clear, honest answers. Effective financial planning for healthcare in retirement starts with having a partner who is never rushed and never pressured.

Mind the Gaps: Planning for the Expenses Medicare Doesn’t Fully Cover

Many people believe that once they reach age 65, their medical bills will simply vanish. In 2026, the reality is that Original Medicare only covers about 80% of your outpatient costs. Leaving that 20% unprotected creates a massive hole in your budget. Without a limit on out-of-pocket spending, a single health crisis could wipe out years of savings. We help you identify these gaps early so your financial planning for healthcare in retirement stays on track and your assets remain protected.

Medigap vs. Medicare Advantage

Choosing between these two paths is the most important decision you’ll make. A Medigap plan offers a predictable monthly premium. You pay your bill, and the insurance company handles the rest. This acts as a powerful hedge for high-net-worth retirees because it eliminates the surprise of a $7,500 hospital co-pay. If you prefer a pay-as-you-go model, a Medicare Advantage plan might have lower premiums but comes with network restrictions. In 2026, 45% of retirees find themselves frustrated by “Doctor Choice” limitations when they realize their specialist isn’t in their plan’s network. We act as your independent advocate to ensure you aren’t trapped by a captive agent’s limited options.

The ‘Hidden’ Three: Dental, Vision, and Hearing

Medicare still treats your teeth, eyes, and ears as “extras,” but we know they are essential to your quality of life. In 2026, a high-quality pair of hearing aids can cost $5,200. Routine dental work or a single crown can easily exceed $1,500. We suggest a dedicated dental insurance plan to protect your overall health and prevent these costs from draining your retirement fund. Bundling these services often saves you 15% on premiums compared to buying separate policies. This is a cornerstone of financial planning for healthcare in retirement because it provides total certainty for your daily needs.

Long-term care remains the biggest wildcard in 2026. Medicare will not pay for long-term custodial care, such as help with bathing or dressing. With the average nursing home stay now costing over $9,800 per month, we must plan for these non-medical needs separately. We simplify the jargon so you know exactly what is covered and what isn’t. Our goal is to move you from confusion to confidence, ensuring you are never rushed or pressured into a decision that doesn’t serve your best interests.

Strategic Wealth Management for Medical Bills: HSAs, IRMAA, and Tax Efficiency

Effective financial planning for healthcare in retirement requires more than just picking a plan. It involves managing your assets so the government takes less and you keep more. We see many seniors feel blindsided by unexpected costs, but with a clear 2026 strategy, we can move you from confusion to confidence. By aligning your tax strategy with your medical needs, we protect your legacy from being eroded by rising premiums and surcharges.

The Power of the Health Savings Account (HSA)

The HSA is a powerhouse for anyone still working or recently retired. It offers a triple-tax advantage: your contributions are tax-deductible, the growth is tax-deferred, and withdrawals for medical expenses are completely tax-free. In 2026, the individual contribution limit has reached $4,300, with an additional $1,000 catch-up for those over age 55. It’s the most efficient way to pay for out-of-pocket costs.

You must be careful with the timing. If you plan to enroll in Medicare this year, we recommend stopping all HSA contributions at least six months prior. This avoids a 6% tax penalty that the IRS triggers when you have active Medicare coverage. Once you’re enrolled, you can still use your existing HSA balance to pay for Part B premiums or even certain long-term care insurance costs. We help you time these transitions so you don’t lose a penny to avoidable fees.

Navigating IRMAA Surcharges

IRMAA, or the Income Related Monthly Adjustment Amount, is a “success tax” on higher earners. For 2026, Social Security looks back at your 2024 tax return to determine your costs. If your 2024 Modified Adjusted Gross Income (MAGI) exceeded $107,000 as an individual or $214,000 for a couple, you’ll likely pay a surcharge on your Part B and Medicare Part D premiums. This surcharge can add hundreds of dollars to your monthly expenses.

If your income dropped in 2025 because you retired, we can help you file a “Life Changing Event” appeal using form SSA-44. This can lower your 2026 premiums immediately. We also look at tools like Qualified Charitable Distributions (QCDs) and strategic Roth conversions. These moves reduce your MAGI, helping you stay below the “High Income” brackets. Our goal is to ensure your Medigap and Part B costs remain as low as possible through smart planning.

Don’t let hidden surcharges drain your retirement savings. Schedule a consultation with Paul to review your 2026 tax efficiency strategy today.

From Confusion to Confidence: How an Independent Advisor Simplifies Your Future

We know that financial planning for healthcare in retirement often feels like trying to solve a puzzle with missing pieces. You’re likely facing a mailbox full of “urgent” flyers and a phone that won’t stop ringing. Our philosophy is different: we are never rushed and never pressured. We take the time to listen to your story because your health history and budget are unique. By comparing over 40 different insurance carriers, we ensure you don’t leave a single dollar on the table. We don’t just find a plan; we find your plan.

We use a proven 5-step process to move you from overwhelmed to empowered:

- Discovery: We listen to your specific medical needs, doctor preferences, and financial goals for 2026.

- Comparison: We filter through dozens of options to find the top three contenders for your situation.

- Education: We explain exactly how each choice impacts your wallet in plain English.

- Enrollment: We handle the paperwork to ensure you avoid costly late-enrollment penalties.

- Advocacy: We stay by your side year-round to answer the phone when you have a claim issue.

Why Independence Matters

There’s a big difference between a “Captive Agent” and an independent broker. Captive agents work for one specific company and can only sell you what that company offers. We work for you. We translate the complex jargon of the 2026 Medicare landscape into simple terms so you’re never left guessing. Best of all, our services are provided at no cost to you. The insurance carriers pay us a commission, which means you get expert guidance without adding another expense to your retirement budget.

Your Next Steps for 2026

The 2026 enrollment season is a critical time to review your coverage. We’ll help you create a personal “Healthcare Retirement Roadmap” that accounts for your specific prescriptions and travel plans. Whether you need a Medigap policy or a Medicare Advantage plan, we’ve got you covered. Effective financial planning for healthcare in retirement starts with one simple, stress-free conversation.

Schedule your “Confusion to Confidence” consultation today to secure your future. We promise to protect your retirement and your peace of mind as if they were our own.

Take Control of Your Health and Wealth Today

Navigating the 2026 Medicare landscape doesn’t have to feel like a walk through a maze. We’ve seen how this year’s premium adjustments and shifting IRMAA brackets can impact your monthly budget. By focusing on financial planning for healthcare in retirement, you can turn that uncertainty into a solid strategy. We’ve covered why maximizing your HSA and choosing the right supplemental coverage are vital steps to protecting your savings from unexpected medical bills.

You don’t have to make these big decisions alone. With over 15 years of experience and access to more than 40 insurance carriers, we’re here to provide the unbiased guidance you deserve. We currently support seniors across 34 states with year round assistance that never feels rushed. We’ll help you avoid late penalties and find a plan that actually fits your life. It’s time to move from a place of stress to a position of total clarity.

Schedule a Call With Paul – From Confusion to Confidence

We’re ready to help you secure the peace of mind you’ve worked so hard to earn.

Frequently Asked Questions

How much should a couple expect to spend on healthcare in retirement in 2026?

A healthy 65-year-old couple retiring in 2026 should plan to spend approximately $380,000 on medical expenses throughout their retirement years. This figure, based on updated 2026 cost projections, covers premiums, deductibles, and co-pays but does not include the cost of a long-term care facility. We help you break down these numbers so your financial planning for healthcare in retirement feels manageable rather than scary.

Can I use my HSA to pay for Medicare premiums once I retire?

You can absolutely use your HSA funds to pay for Medicare Part B and Part D premiums tax-free once you turn 65. This is a powerful tool because it allows you to use pre-tax dollars for your monthly costs, though the IRS does not allow you to use these funds for Medigap policy premiums. We’ll show you how to coordinate these accounts to keep more money in your pocket during your golden years.

What is IRMAA and how does it affect my financial planning for healthcare?

IRMAA is an extra charge added to your Medicare Part B and Part D premiums if your income from two years ago exceeds $103,000 for individuals or $206,000 for couples. In 2026, Social Security uses your 2024 tax return to determine if you’ll pay these higher rates. We work with you to spot these potential surcharges early so they don’t catch your budget by surprise or derail your financial planning for healthcare in retirement.

Does Original Medicare cover long-term care or nursing home stays?

Original Medicare does not pay for long-term custodial care or extended nursing home stays that last more than 100 days. It only provides limited coverage for skilled nursing care following a 3-day inpatient hospital stay, and even then, your 2026 co-pays start on day 21. Because 70% of seniors will need some form of long-term support, we prioritize finding solutions that protect your life savings from these high costs.

What is the $2,000 Part D out-of-pocket cap and how does it help me in 2026?

The $2,000 Part D out-of-pocket cap is a new rule for 2026 that limits your total yearly spending on covered prescription drugs to exactly $2,000. This is a major win for your budget because it eliminates the old “donut hole” and protects you from massive bills if you need expensive specialty medications. We’ll help you review your specific prescriptions to ensure you’re getting the full benefit of this new protection.

Should I choose a Medicare Advantage plan or a Medigap plan for better financial protection?

Choosing between Medicare Advantage and Medigap depends on whether you prefer a $0 monthly premium with co-pays or a higher monthly premium with $0 out-of-pocket costs at the doctor. Medigap offers the best financial protection for those who want total predictability, while Advantage plans often include extra perks like dental or vision. We’ll compare 15 different carriers side-by-side so you can move from confusion to confidence.

Is there a penalty if I don’t sign up for Medicare as soon as I retire?

You’ll face a permanent 10% late enrollment penalty for every 12-month period you were eligible for Medicare Part B but didn’t sign up. This penalty stays with you for life and can increase your monthly costs by hundreds of dollars over time. Our team ensures you hit your 2026 deadlines perfectly so you never have to pay a penny more than necessary for your coverage.