Adding dental insurance to your Medicare coverage means selecting a Medicare Advantage plan that includes dental benefits or purchasing a standalone supplemental dental plan alongside Original Medicare. Most Medicare recipients are surprised to learn their current coverage leaves routine dental care entirely unprotected. The gap is real, it is expensive, and it is fixable. This guide walks you through every option available in 2026, from Medicare Advantage dental benefits to standalone plans, community resources, and the exact steps to enroll or switch.

Why does Medicare lack dental coverage in the first place?

Original Medicare excludes routine dental care as a matter of original design. When Medicare was created in 1965, dental care was considered a separate category from medical care, and that distinction was written into law. The result is that Medicare Parts A and B do not pay for cleanings, fillings, extractions, dentures, or periodontal treatment under any standard circumstance.

The narrow exception covers dental services that are medically necessary as part of a covered inpatient hospital procedure. Examples include dental clearance required before cardiac surgery, treatment of jaw fractures caused by an accident, or oral exams directly connected to a covered hospital stay. Even in these cases, providers must be Medicare-enrolled and document medical necessity with precision, coordinating with the treating physician to get the claim approved.

This coverage gap hits Medicare recipients hard. A single crown can cost $1,000 to $1,500 out of pocket. A full set of dentures can run $3,000 or more. For people on fixed incomes, these costs are not minor inconveniences. They are reasons people delay care until a dental problem becomes a medical emergency.

The practical takeaway: if you rely solely on Original Medicare, you have no dental coverage for routine or restorative care. You need to add it through one of the options below.

What dental benefits do Medicare Advantage plans actually include?

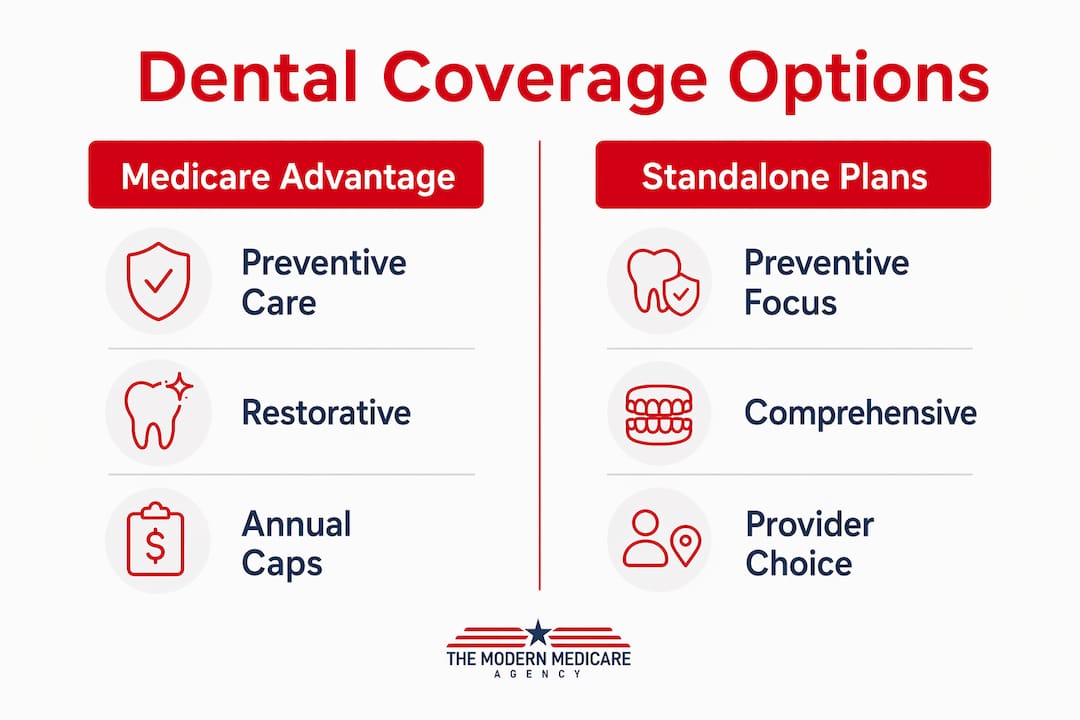

About 94% of Medicare Advantage plans included some form of dental benefit in 2026. That statistic sounds reassuring until you read the fine print. “Some form” can mean anything from two free cleanings per year to a $2,000 annual maximum that covers exams, X-rays, fillings, and basic extractions.

What is typically covered

Most Medicare Advantage dental benefits cover preventive services at 100%: routine cleanings, oral exams, and X-rays. Some plans extend coverage to basic restorative work like fillings and simple extractions, often at 50% to 80% after a copay. Major restorative procedures such as crowns, bridges, root canals, and dentures are covered by fewer plans, and when they are, annual dollar caps apply.

| Service Type | Typical Coverage Level | Common Annual Cap |

|---|---|---|

| Preventive (cleanings, exams, X-rays) | 80% to 100% | No separate cap |

| Basic restorative (fillings, extractions) | 50% to 80% | Shared with major |

| Major restorative (crowns, dentures) | 0% to 50% | $1,000 to $2,000 |

| Orthodontics | Rarely covered | Plan-specific |

The variability is the problem. Many seniors discover that their Medicare Advantage dental coverage only handles preventive care after assuming it covered major work. That assumption leads to thousands of dollars in unexpected bills.

Pro Tip: Never rely on a plan’s marketing materials to understand dental coverage. Pull the actual Evidence of Coverage document and search for the dental benefits section. The EOC lists every covered procedure, the cost-sharing percentage, and the annual maximum. A plan that says “dental included” on its summary page may cap major services at $500 per year.

Medicare Advantage plans also manage dental coverage through separate dental networks, meaning your dentist must be in the plan’s dental network, not just its medical network. Confirm your dentist’s in-network status before enrolling. Switching plans only to find your dentist is out of network eliminates most of the benefit.

How do standalone supplemental dental plans work for Medicare recipients?

Standalone supplemental dental insurance is the primary solution for Original Medicare beneficiaries and for those whose Medicare Advantage dental benefits fall short. These plans operate independently of Medicare and pay for covered dental services directly. You can learn more about your options through the supplemental dental insurance guide at Paulbinsurance.

Preventive-focused standalone plans average about $360 per year in premiums. Comprehensive plans that cover major restorative work cost more and typically include waiting periods of 6 to 12 months before major services are covered. That waiting period is the most common frustration among new enrollees who need a crown or dentures right away.

PPO vs. HMO standalone plans

The two main structures for standalone dental plans are PPO and HMO. Here is how they compare for Medicare recipients:

| Feature | Dental PPO | Dental HMO |

|---|---|---|

| Provider flexibility | Any licensed dentist, in or out of network | Must use plan’s network dentist |

| Monthly premium | Higher | Lower |

| Annual maximum | $1,000 to $2,500 typically | Fixed copays, no annual max |

| Out-of-network coverage | Yes, at reduced rate | No |

| Best for | Those with an established dentist | Those prioritizing lower cost |

PPO plans offer more flexibility and are generally the better fit for Medicare recipients who already have a dentist they trust. HMO plans cost less monthly but require you to choose from a limited network, which can be restrictive in rural areas.

Pro Tip: If you have a Medicare Advantage plan with some dental coverage, a standalone plan can layer on top of it. Standalone plans coordinate benefits by billing your Medicare Advantage plan first, then covering remaining costs per the supplemental plan’s terms. This coordination can significantly reduce your out-of-pocket exposure on major procedures.

Alternatives to traditional insurance include dental savings cards, sometimes called discount dental plans. These are not insurance. They are membership programs that negotiate reduced fees with participating dentists, typically 10% to 60% off standard rates. They have no waiting periods, no annual maximums, and no claim forms. For someone who needs immediate restorative work and cannot wait out an insurance waiting period, a dental savings card can be a practical short-term bridge.

Steps to add or upgrade your dental coverage

Adding dental insurance to your Medicare coverage is a structured process. Follow these steps to avoid common mistakes and get the right coverage in place.

-

Review your current Evidence of Coverage. If you have a Medicare Advantage plan, locate the dental benefits section in your EOC document. Note the annual maximum, covered procedures, and cost-sharing percentages. This tells you exactly what you have and what you are missing.

-

Identify your dental care needs. Are you primarily looking for preventive coverage, or do you anticipate needing major restorative work? Your answer determines whether a preventive-only plan or a comprehensive plan makes sense. Comprehensive plans cost more but protect against large unexpected expenses.

-

Compare Medicare Advantage plans during Annual Enrollment. The Annual Enrollment Period runs October 15 through December 7. This is your primary window to switch to a Medicare Advantage plan with stronger dental benefits. Use Medicare’s Plan Finder tool at Medicare.gov to filter plans by dental coverage in your zip code. You can also explore Medicare Advantage plans explained at Paulbinsurance for a clear breakdown of what to look for.

-

Check provider networks before enrolling. Confirm your current dentist participates in any plan you are considering. If your dentist is not in the network, factor in the cost and inconvenience of switching providers.

-

Purchase a standalone dental plan if needed. Standalone dental plans are available year-round. You do not need a special enrollment period to buy one. Compare plans through licensed agents or directly through insurers, focusing on the annual maximum, waiting periods, and covered procedures.

-

Ask about mid-year supplemental dental options. Some Medicare Advantage plans allow you to add supplemental dental benefits mid-year through optional supplemental benefits selection, usually for an additional monthly premium. Contact your plan directly to ask if this option exists.

Pro Tip: Do not wait until you need dental work to review your coverage. Enroll in or upgrade your dental plan during Annual Enrollment each fall, before any dental issues arise. Waiting until you need a crown to buy a comprehensive plan means you will likely face a 12-month waiting period before that crown is covered.

Alternatives when insurance is not the right fit

Insurance is not the only path to affordable dental care for Medicare recipients. Low-income seniors should explore Medicaid dental benefits, Federally Qualified Health Centers, and dental schools as cost-effective alternatives. These resources are underused and genuinely effective.

Here is a breakdown of the main alternatives:

- Medicaid dental benefits: If you qualify for both Medicare and Medicaid (called dual eligibility), your state Medicaid program may cover dental services that Medicare does not. Medicaid dental benefits vary by state, with some states covering comprehensive care and others covering only emergency extractions.

- Federally Qualified Health Centers (FQHCs): FQHCs are federally funded clinics that offer dental care on a sliding-scale fee basis tied to your income. You pay only what you can afford. Use the HRSA Health Center Finder at findahealthcenter.hrsa.gov to locate one near you.

- Dental schools: Accredited dental schools such as those affiliated with major universities offer cleanings, fillings, crowns, and dentures at 50% to 70% below private practice rates. Work is performed by supervised dental students, and quality is closely monitored.

- Dental savings cards: As noted above, these membership programs provide immediate discounts without waiting periods. They work well alongside insurance or as a standalone option for those who cannot afford premiums.

Safety-net resources like FQHCs and dental schools often deliver more cost-effective solutions than private dental insurance for seniors on limited budgets. For someone paying $150 per month for a comprehensive dental plan, the math may not work out in their favor compared to paying sliding-scale fees at an FQHC.

For medically necessary dental care that may qualify under Medicare, work with your dentist and physician together. Proper documentation of medical necessity and provider enrollment in Medicare are both required for any claim to be approved.

Key takeaways

Adding dental insurance to Medicare requires choosing between Medicare Advantage dental benefits and standalone supplemental plans, with the right choice depending on your specific dental needs, budget, and provider preferences.

| Point | Details |

|---|---|

| Original Medicare covers almost no dental | Routine cleanings, fillings, and dentures are excluded; only medically necessary inpatient dental is covered. |

| Most Medicare Advantage plans include dental | About 94% include some dental benefit, but coverage scope and annual caps vary widely across plans. |

| Standalone plans fill the gap | Preventive plans average $360 per year; comprehensive plans cost more and often have waiting periods for major work. |

| Annual Enrollment is your key window | October 15 to December 7 is when you can switch Medicare Advantage plans to get better dental coverage. |

| Alternatives exist for low-income seniors | FQHCs, dental schools, and Medicaid dental benefits provide affordable care outside traditional insurance. |

What I have learned after years of helping Medicare recipients with dental coverage

After working with Medicare consumers since 2007, I have seen the same pattern repeat itself hundreds of times. A person enrolls in a Medicare Advantage plan, checks the box that says “dental included,” and assumes they are covered. Two years later, they need a crown or a partial denture and discover their plan’s annual dental maximum is $500. The crown alone costs $1,200. They are blindsided.

The uncomfortable truth is that checking “yes” for dental coverage on a plan search tool tells you almost nothing about what you actually have. The Evidence of Coverage document is the only source of truth. I tell every client to read that section before they sign anything.

My honest recommendation for most Medicare recipients: if your Medicare Advantage plan’s dental maximum is under $1,500 and does not cover major restorative work, add a standalone dental plan. The premium cost is manageable, and the protection against a $3,000 denture bill is real. For those on tight budgets, an FQHC or dental school combined with a basic discount card often beats paying for a comprehensive insurance plan that has a 12-month waiting period anyway.

The one mistake I see most often is waiting. People wait until they have a dental problem to think about coverage. By then, their options are limited and expensive. Review your dental coverage every fall during Annual Enrollment, even if you think you are fine. Dental needs change, and so do the plans available in your area.

— Paul

How Paulbinsurance can help you find the right dental coverage

Sorting through Medicare Advantage plans, standalone dental options, and enrollment windows takes time you may not have. Paulbinsurance specializes in exactly this kind of comparison work for Medicare recipients across the country.

The team at Paulbinsurance can review your current Medicare plan’s dental benefits, identify Medicare Advantage plans in your area with stronger dental coverage, and help you evaluate standalone dental insurance options that fit your budget and care needs. Whether you are on Original Medicare with no dental coverage at all or frustrated with a Medicare Advantage plan that barely covers cleanings, there is a better option available. Start by exploring Medicare Advantage plans explained to understand what dental benefits are possible, then connect with a Paulbinsurance agent for a personalized plan comparison. You can also review the dental coverage for seniors guide for a full breakdown of enrollment steps and costs.

FAQ

Does Medicare cover routine dental cleanings?

Original Medicare does not cover routine dental cleanings or any standard preventive dental care. Coverage is limited to dental services that are medically necessary as part of a covered inpatient hospital procedure.

What is the best way to add dental coverage to Medicare?

The two main options are switching to a Medicare Advantage plan that includes dental benefits or purchasing a standalone supplemental dental plan. The right choice depends on your current plan, your dentist’s network participation, and whether you need preventive-only or comprehensive coverage.

When can I switch Medicare Advantage plans to get better dental benefits?

The Annual Enrollment Period runs October 15 through December 7 each year. This is the primary window to switch Medicare Advantage plans and is the best time to upgrade to a plan with stronger dental benefits.

How much does standalone dental insurance cost for Medicare recipients?

Preventive-focused standalone dental plans average about $360 per year in premiums. Comprehensive plans that cover major restorative work cost more and typically include waiting periods of 6 to 12 months before major services are payable.

What dental options exist for low-income Medicare recipients?

Low-income seniors may qualify for Medicaid dental benefits, access sliding-scale care at Federally Qualified Health Centers, or receive discounted treatment at accredited dental schools. These community-based dental resources are often more cost-effective than private insurance for those on limited budgets.