What if your total prescription drug costs for the year were capped at exactly $2,000, yet you still ended up overpaying by $450 because of a hidden pharmacy network rule? We know that staring at drug tiers and shifting premiums feels like trying to solve a puzzle with missing pieces. It is completely normal to feel a bit of anxiety when your 2026 Annual Notice of Change arrives in your mailbox this September. Learning how to compare medicare part d plans shouldn’t feel like a second career or a source of constant stress.

We are here to lead you from confusion to confidence. We will show you exactly how to navigate the 2026 prescription drug landscape so you can find the best coverage for your medications without the headache. This guide breaks down the latest out-of-pocket limits, explains how to verify your preferred pharmacy status, and provides a clear path to calculating your total annual costs. You deserve to walk up to the pharmacy counter knowing exactly what you’ll pay, every single time.

Key Takeaways

- Understand how the $2,000 out-of-pocket cap for 2026 changes your coverage strategy, and let us show you how it protects your savings.

- Learn how to compare medicare part d plans using our simple three-pillar approach to avoid hidden costs and pharmacy sticker shock.

- We’ll explain how the Medicare Prescription Payment Plan can smooth out your drug expenses into predictable, stress-free monthly payments.

- Follow our clear, step-by-step guide to organizing your medications so you can move from confusion to total confidence.

- See why we research over 40 different carriers to find your best fit rather than limiting your choices like a captive agent.

Why Comparing Medicare Part D Plans in 2026 is Different (and Essential)

Medicare Part D is the specific piece of the Medicare puzzle that handles your prescription drugs. For many years, this was the most frustrating and unpredictable part of healthcare for seniors. We understand the stress you feel when you open a pharmacy bill and see a price that doesn’t make sense. Our mission is to move you from confusion to confidence by showing you exactly how to compare medicare part d plans so you never pay a penny more than necessary.

The 2026 landscape is a landmark year for your wallet. Major legislative changes have finally reached full implementation, shifting the financial burden away from you and back onto the insurance companies. While this is great news, it also means the insurance companies are changing their tactics. We help you look past the glossy marketing brochures to find the actual math that fits your life. We are here to protect you from overpaying.

The End of the Coverage Gap (Donut Hole)

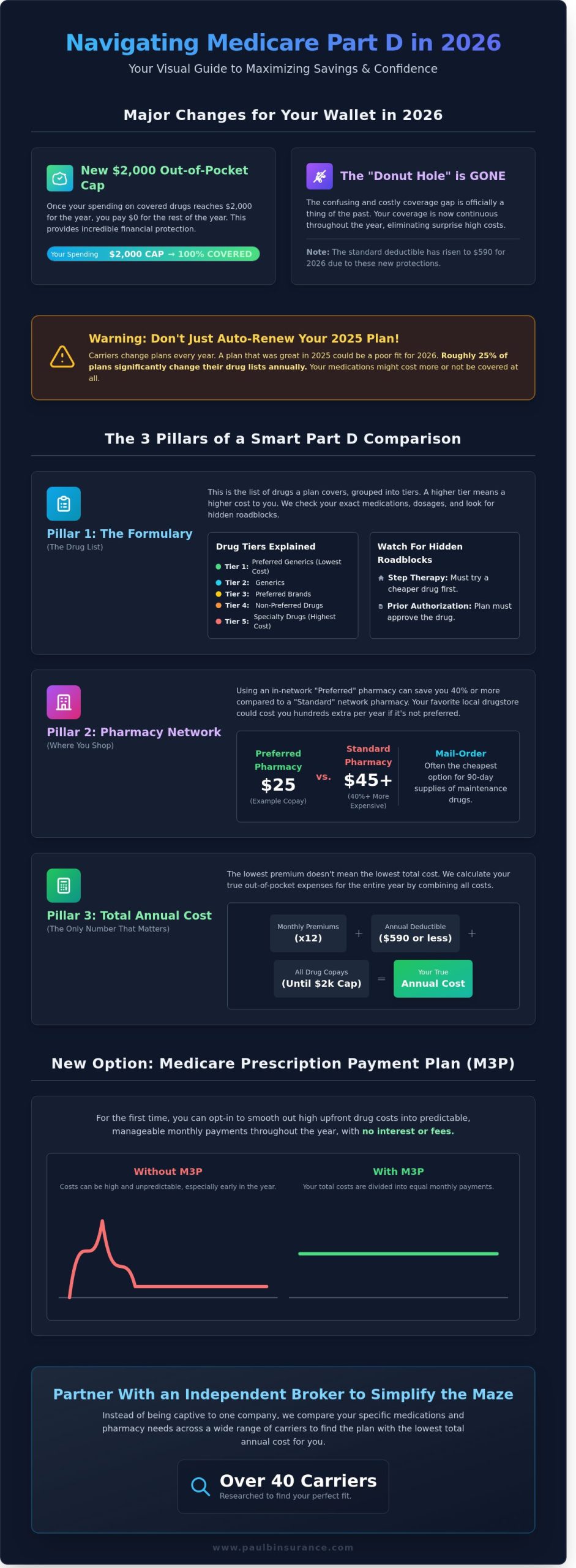

The infamous “donut hole” is officially a thing of the past in 2026. This year, every Part D plan includes a mandatory $2,000 out-of-pocket maximum. Once you spend $2,000 on your covered medications, your plan pays 100 percent of your drug costs for the rest of the year. This change provides incredible peace of mind for the 1 in 10 seniors who previously faced thousands of dollars in costs. You should be aware that because of this new protection, the standard deductible for 2026 has risen to $590. We simplify these numbers so you know exactly what to expect at the pharmacy counter.

Why Your 2025 Plan Might Not Be Your Best 2026 Plan

It is tempting to let your current plan auto-renew, but that is a dangerous financial move. Carriers frequently update their “formularies,” which is just the list of drugs they agree to cover. A medication that was affordable in 2025 might be moved to a higher cost tier or dropped entirely in 2026. Data shows that roughly 25 percent of plans change their drug lists significantly each year. If you want to know how to compare medicare part d plans effectively, you must check these three factors:

- The specific tier level of your most expensive medications.

- The monthly premium, which may have increased to offset the new $2,000 cap.

- Which local pharmacies are considered “preferred” to keep your copays low.

We are dedicated advocates who believe you deserve an unbiased look at your options. A plan that worked perfectly last year might be a poor fit today. If you need a refresher on the basics, you can view our detailed guide on Medicare Part D to see how these pieces fit together. We are never rushed and never pressured, we simply want you to have the right coverage.

The Three Pillars of a Smart Part D Plan Comparison

Learning how to compare medicare part d plans doesn’t have to be a headache. We see too many folks pick a plan based solely on the lowest monthly premium, only to face “sticker shock” when they stand at the pharmacy counter in January. This happens because the cheapest premium doesn’t always mean the lowest cost for your specific medications. We use a three-pillar approach to build a personalized comparison that protects your wallet and your health.

Checking these pillars every year during the Annual Enrollment Period is vital. Plan details change every single January 1st, and a plan that served you well in 2025 might have dropped your most important medication for 2026. We simplify the jargon so you know exactly how your coverage works before you ever sign up.

Pillar 1: The Formulary (The Drug List)

A formulary is the list of drugs a plan agrees to cover. These drugs are grouped into tiers, usually ranging from Tier 1 generics to Tier 5 specialty drugs. We always check your exact dosage and frequency against these tiers because a higher tier means a higher copay. You should also watch out for hidden roadblocks like “Step Therapy,” where a plan requires you to try a cheaper drug before they cover the one your doctor prescribed. We also look for “Prior Authorization” rules that could cause delays at the pharmacy.

Pillar 2: The Pharmacy Network

Where you shop matters as much as what you buy. In 2026, the price difference between “Preferred” and “Standard” pharmacies is often 40% or more. Your favorite local drugstore might be convenient, but if it isn’t in your plan’s preferred network, you will pay significantly more for the same bottle of pills. We often find that using mail-order services for 90-day supplies provides the best combination of savings and convenience, especially for maintenance medications you take every day.

Pillar 3: Total Annual Cost (The Only Number That Matters)

Total Annual Cost is the sum of all out-of-pocket drug expenses for the calendar year. This is the most reliable way to understand how to compare medicare part d plans without getting distracted by flashy $0 premium offers. We calculate this by adding your monthly premiums for 12 months, your annual deductible, and your estimated copays based on your specific drug list.

With the $2,000 out-of-pocket cap now fully in effect for 2026, we can help you see exactly when you might reach that limit. If you feel confused by the math, we can help you review your Medicare Part D options to ensure you aren’t overpaying. Our goal is to move you from confusion to confidence by showing you the real bottom-line cost of every plan available to you.

Navigating the New “Medicare Prescription Payment Plan” (M3P)

Since January 1, 2025, the Medicare Prescription Payment Plan (M3P) has changed the way we handle drug costs. In 2026, this option is even more vital because of the universal $2,000 out-of-pocket limit. Think of it as a “smooth out” feature for your wallet. Instead of facing a massive bill at the pharmacy counter in January, your plan allows you to spread those costs across the entire year. We help you look at your specific medications to see if this monthly installment approach makes sense for your budget.

We often see clients who feel overwhelmed by these new choices. If your annual drug costs are low, perhaps under $500, this program might just add unnecessary paperwork to your life. However, for those on fixed incomes, it provides a predictable monthly expense. We simplify the jargon so you know exactly how it works before you sign up. Our goal is to move you from confusion to confidence by showing you exactly how these payments look on paper.

How the $2,000 Cap and M3P Work Together

The $2,000 cap is a safety net, but M3P is the tool that helps you reach it without financial stress. If you take a high-cost specialty drug that normally costs $1,800 in your first month, the M3P option breaks that down. You’d pay roughly $166 per month instead of one giant lump sum. This is a game-changer for the 1 in 10 seniors who previously skipped doses due to high upfront costs. It isn’t a discount; you still pay the full $2,000 eventually. It’s simply a restructuring of the timeline to protect your monthly cash flow.

Common Misconceptions About the 2026 Cap

Many people we talk to think the $2,000 cap covers every expense. It doesn’t. This limit only applies to your out-of-pocket costs for covered drugs at the pharmacy. Your monthly premiums and any drugs not on the plan formulary don’t count toward this total. Once you hit that $2,000 mark, you enter the “Catastrophic” phase where you pay $0 for covered drugs for the rest of 2026. This is why learning how to compare medicare part d plans remains a critical step. Plans still have different premiums and different lists of covered drugs. Choosing the wrong plan could mean paying for a drug that doesn’t count toward your cap at all.

We are here to help you evaluate these details. We compare the total cost of each plan, including the premium and the specific tier of your medications. You can find more details on our Medicare Part D page to see how we help you avoid costly enrollment mistakes. Understanding how to compare medicare part d plans in 2026 is about more than just the $2,000 limit; it’s about finding the specific carrier that treats your unique list of prescriptions most fairly.

A Step-by-Step Guide: How to Compare Medicare Part D Plans

We know that looking at a long list of insurance options feels like staring at a bowl of alphabet soup. It’s confusing, but we can clear that up together. Learning how to compare medicare part d plans starts at your kitchen table, not a computer screen. By following a simple process, you can move from a state of confusion to complete confidence about your 2026 coverage.

Step 1: The “Medicine Cabinet” Audit

Start by gathering your current pill bottles. You need the exact spelling and the specific dosage, such as 20mg or 50mg. In 2026, even a small typo can change your estimated annual cost by $500 or more because drug formularies are so specific. We recommend making a list of everything you take, including vitamins or supplements. While Medicare Part D generally doesn’t cover over-the-counter vitamins, knowing your full routine helps us ensure nothing interferes with your new plan. This audit ensures your quote is based on reality, not a guess.

Step 2: Comparing “Advantage” vs. “Standalone” PDP

You have two main paths for drug coverage in 2026. You can choose a Medicare Advantage Plan, which bundles your medical and drug coverage into one “all-in-one” card. This is often convenient for those who want a single point of contact. Alternatively, you might keep Original Medicare and add a Medigap plan along with a standalone Part D plan. This second option offers more flexibility if you see many specialists. With the 2026 out-of-pocket cap now set at $2,000 for all plans, the choice often comes down to which pharmacy you prefer and which doctors you want to keep.

Step 3: The Final Decision Checklist

Before you sign anything, we use a three-point checklist to guarantee peace of mind. First, check the CMS Star Ratings. A 4 or 5-star rating tells us the plan has a history of reliable customer service and few billing errors. Second, look for “Value Added” features. Many 2026 plans now include perks like dental insurance or vision discounts that aren’t part of basic Medicare. Finally, use the “Sleep Test.” Which plan makes you feel most secure? We want you to choose the option that lets you sleep soundly knowing your health is protected.

- Identify your preferred local pharmacy and one mail-order backup.

- Check the “Effective Date” to ensure your new coverage starts exactly when the old one ends.

- Verify that your specific pharmacy is “preferred” to keep copays at their lowest.

Understanding how to compare medicare part d plans doesn’t have to be a solo struggle. We’re here to run the numbers and find the hidden savings for you. Schedule a call with Paul today and let’s simplify your 2026 coverage together.

Why Partnering With an Independent Broker Simplifies the Maze

The Medicare system often feels like a confusing maze of fine print and deadlines. We’re here to clear the path for you. One of the biggest mistakes we see is people confusing a captive agent with an independent broker. A captive agent works for one specific insurance company. They are limited to offering only that company’s products. If a better or cheaper plan exists elsewhere, they can’t offer it to you. We operate differently as independent brokers. We represent over 40 different carriers. This allows us to search the entire 2026 market to find your specific best fit based on your unique medications and budget.

Our service costs you exactly $0. We are paid directly by the insurance companies, not by you. This means you receive our expert guidance, year-round advocacy, and detailed plan analysis without any added fees. Your premium remains the same whether you use our help or try to figure it out on your own. We stay by your side long after your initial enrollment. If you have a billing issue or a pharmacy dispute in the middle of the year, we are the ones who pick up the phone to fight for you. We show you exactly how to compare medicare part d plans without the stress of doing it yourself.

From Confusion to Confidence

We take the math homework off your plate so you can focus on your life. Government websites are often cold and difficult to navigate, especially with the 2026 changes to the $2,000 out-of-pocket maximum. We provide a human voice and a patient ear. During our consultations, we are never rushed and never pressured. We simplify the jargon so you know exactly how your coverage works before you sign anything. Our goal is to move you from a state of worry to a state of total confidence.

Ready to Compare? Let’s Get Started

Learning how to compare medicare part d plans is much easier when you have an advocate in your corner. If you’re ready for a 2026 plan review, we’re ready to help. To make our first conversation as productive as possible, please have a few items ready:

- Your current Medicare card.

- A complete list of your current medications and dosages.

- The name of your preferred pharmacy.

You don’t have to face these complex decisions alone. We’ve helped thousands of seniors find peace of mind by making the complex simple. If you want to explore your options for the coming year, visit our Medicare Part D page or reach out to schedule a call with our team. We look forward to helping you save money and secure the coverage you deserve for 2026.

Move From Confusion to Confidence in 2026

The 2026 landscape for prescription drugs has changed significantly with the $2,000 out-of-pocket maximum and the new Medicare Prescription Payment Plan. You don’t have to feel overwhelmed by these updates or worry about picking the wrong coverage. We’ve shown you the essential steps for how to compare medicare part d plans, from checking your specific medications against current formularies to weighing the benefits of monthly payment smoothing. Our goal is to ensure you never pay a penny more than necessary for the medications you need.

Navigating these choices alone is difficult; we’re here to protect your peace of mind. We provide unbiased guidance tailored to your unique health needs with access to over 40 insurance carriers. Our team is licensed in over 34 states and offers year-round support so you’re never left searching for answers. You can skip the stress of the “crazy maze” and secure a clear path forward today. We’ll help you steer clear of costly enrollment mistakes and late penalties with a plan that fits your life.

Schedule a Call With Paul to Compare Your 2026 Part D Options

You deserve the security of knowing your healthcare is in expert hands. We’re ready to help you find the clarity you’ve been looking for.

Frequently Asked Questions

Is there a penalty for not signing up for Medicare Part D?

Yes, you’ll face a permanent late enrollment penalty if you go 63 days or more without creditable drug coverage. This penalty adds 1% of the national base beneficiary premium to your monthly bill for every full month you were eligible but didn’t have a plan. We help you avoid these lifelong extra costs by ensuring you choose a plan as soon as you’re eligible, keeping your long term costs as low as possible.

Can I change my Medicare Part D plan at any time?

No, you can generally only change your coverage during the Annual Enrollment Period that runs from October 15 to December 7 each year. Outside of this window, you typically need a Special Enrollment Period, which is triggered by specific life events like moving to a new address or losing employer coverage. When you learn how to compare medicare part d plans during these set windows, you ensure your 2026 coverage stays aligned with your health needs.

What is the $2,000 out-of-pocket cap for Medicare Part D in 2026?

The $2,000 cap is a new federal limit that ensures you don’t pay more than $2,000 for covered prescriptions during the 2026 calendar year. Once your personal spending reaches this $2,000 threshold, your insurance plan pays 100% of your covered drug costs for the rest of the year. This change provides vital financial protection for the 1.4 million seniors who previously faced much higher costs when they hit the coverage gap or “donut hole.”

Does Medicare Part D cover insulin in 2026?

Yes, all Medicare Part D plans cover your insulin with a monthly copay that’s capped at $35 for a 30 day supply. This price protection applies even if you haven’t met your 2026 deductible yet, which helps keep your monthly expenses predictable. We make sure your specific insulin brand is on your plan’s list so you never have to worry about paying more than this fixed amount at the pharmacy counter.

What happens if my drug is not on a plan’s formulary?

If your medication isn’t on the plan’s list, you may have to pay the full retail price, which can easily cost $500 or more per refill. You can ask your doctor to request a formulary exception from the insurance company, but there’s no guarantee they’ll approve it. We recommend checking every one of your medications against the 2026 drug lists before you enroll so you aren’t hit with these expensive and stressful surprises.

How do I find out if my pharmacy is in-network for a Part D plan?

You can find out if your pharmacy is in-network by checking the plan’s 2026 Pharmacy Directory or using the official search tool on Medicare.gov. Many plans use “preferred” pharmacies where your copays might be $0 or $5 instead of the standard $20 rate. We help you look at these details closely because using an out-of-network pharmacy could cost you an extra $200 or more over the course of a single year.

What is the “Medicare Prescription Payment Plan” (M3P)?

The Medicare Prescription Payment Plan is a new 2026 program that lets you pay your out-of-pocket drug costs in monthly installments instead of all at once. If you have a $600 pharmacy bill in January, this option allows you to spread that balance across the remaining months of the year. It’s a voluntary, interest-free program designed to help you manage your monthly cash flow and avoid large, unexpected bills at the pharmacy.

Do I need a Part D plan if I have a Medicare Advantage plan?

You usually don’t need a separate Part D plan because about 89% of Medicare Advantage plans already include prescription drug coverage. In fact, if you’re in an Advantage plan and try to buy a standalone Part D plan, you might be automatically disenrolled from your health coverage. Understanding how to compare medicare part d plans helps you determine if your current Advantage plan’s drug list is still the most cost-effective choice for your 2026 medications.