What if the most meaningful legacy you leave behind is the simple gift of a worry-free goodbye for your children? We know you’ve likely felt a sense of anxiety when thinking about the future. It’s a heavy burden to worry that your family might struggle with rising costs or get lost in a sea of jargon while searching for life insurance to cover final expenses. You want to protect them, but it’s hard to know where to start when you’re on a fixed income or concerned that past health issues might stand in your way.

We believe you deserve a path that leads from uncertainty to absolute clarity. This guide will help you understand exactly what to expect in 2026, from the median costs of services to the way modern, faster underwriting can get you covered without a medical exam. We’ll walk you through how to secure a policy that pays out quickly and fits your monthly budget; this ensures you can get back to enjoying the present with total peace of mind.

Key Takeaways

- Understand why whole life policies are a gift of certainty that ensures your family isn’t left with unexpected bills during a difficult time.

- Discover how these plans build cash value over time and stay active for your entire life as long as premiums are paid.

- Learn why choosing life insurance to cover final expenses is often a better fit for seniors than traditional term policies that might expire when you need them most.

- Follow our simple two-step process to calculate exactly how much coverage you need based on 2026 funeral and cremation costs.

- See the value of working with an independent advocate who compares the entire market to find the most affordable monthly premiums for your specific budget.

The Reality of End-of-Life Costs: Why Final Expense Coverage Matters in 2026

Planning for the future often feels overwhelming, but it doesn’t have to be. We define final expense insurance as a permanent whole life policy specifically intended to handle your end-of-life costs. Think of it as a gift of certainty for your children or spouse. It’s a way to ensure that the people you care about most aren’t stuck paying for a funeral out of their own pockets. While traditional life insurance often focuses on replacing an income, life insurance to cover final expenses is built to provide immediate relief for specific bills.

Beyond the service itself, many families are surprised by hidden costs that pop up at the end of life. These might include remaining medical bills from a hospital stay or legal fees required to settle an estate. By securing a policy now, you’re creating a buffer that protects your family’s savings. We want to help you move from a state of worry to a place of complete confidence. Our goal is to make this process so simple that you never have to wonder if your loved ones are protected.

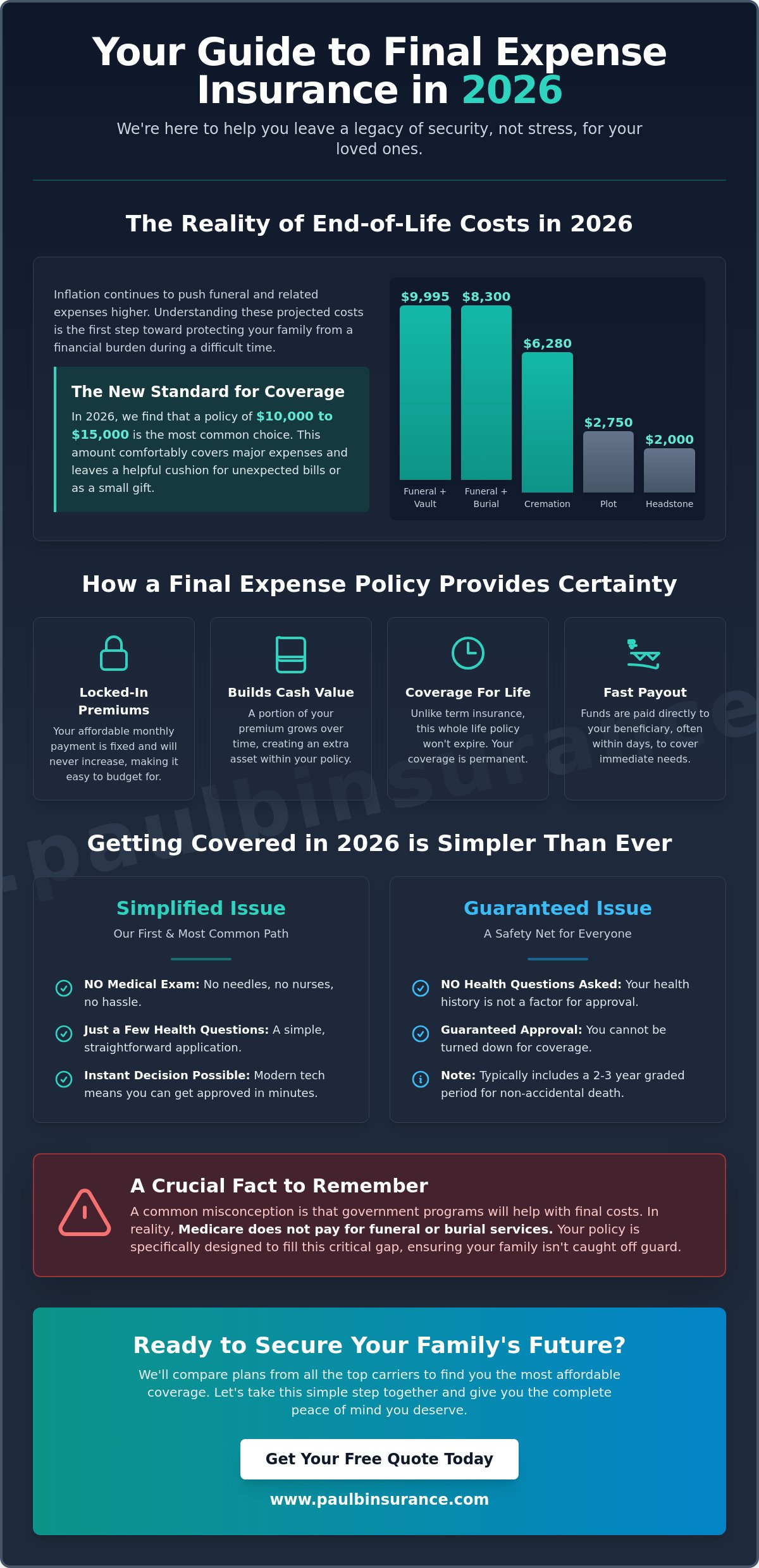

Projected Funeral Costs in 2026

In 2026, we’re seeing that funeral industry inflation continues to rise faster than the general cost of living. Today, the median cost for a funeral with a burial is $8,300; if you require a vault, that number climbs to $9,995. Even cremation, which more than 60% of families now choose, has a median cost of $6,280 when it includes a viewing. Because of these rising prices, many people find that Burial insurance in the range of $10,000 to $15,000 is the new standard recommendation. This amount covers the basics while leaving a little extra for a headstone, which currently averages $2,000, or a cemetery plot that typically costs around $2,750.

The Emotional Burden of Unfunded Expenses

The stress of losing a loved one is hard enough without the added pressure of a financial crisis. We’ve seen too many families forced to turn to online crowdfunding or high-interest credit cards just to pay for a service. This creates a state of distress during a time that should be reserved for honoring your memory. A dedicated policy provides immediate liquidity, often paying out within days of a claim. This speed gives your family the space they need to grieve without checking their bank balances. We’re committed to helping you find an affordable way to prevent these difficult moments, ensuring your legacy is one of protection and peace.

How Final Expense Insurance Works: A Simple Explanation

We want to make the technical parts of insurance feel like a conversation with a friend. At its heart, life insurance to cover final expenses is a type of whole life insurance. Unlike term policies that might end just when you need them most, these plans never expire. As long as you pay your premiums, the coverage stays exactly where it belongs. This creates a sense of security that doesn’t waver. Over time, these policies also build a small amount of cash value. This is a component of your premium that grows within the plan, adding an extra layer of reliability to your policy.

It’s also helpful to understand the different roles involved in your plan. You are typically the policy owner, which means you control the coverage and manage the payments. The death benefit is the specific amount of money your chosen beneficiary receives after you pass away. In 2026, many of the best burial insurance companies offer flexible options that allow you to name a trusted family member to receive these funds directly. This ensures the money is available right when it’s needed most.

Simplified Issue vs. Guaranteed Issue

Finding life insurance to cover final expenses doesn’t have to be a stressful journey through medical records. We use a streamlined approach to help you get covered quickly. A simplified issue policy is usually our first recommendation. It requires answering a few basic health questions but involves no blood work or invasive exams. Thanks to the AI-driven underwriting common in 2026, we can often get you a decision almost instantly. If you have more serious health challenges, we look at guaranteed issue options. These have no health questions at all. While they are slightly more expensive and usually include a two or three-year waiting period for non-accidental deaths, they ensure that no one is ever turned away regardless of their medical history.

Covering the Gaps Medicare Leaves Behind

A common point of confusion we hear is the belief that government programs will handle these final costs. In reality, Medicare does not pay for funeral or burial services. This is where your policy steps in to bridge the gap. It can even help your family cover final Part B medical co-pays or remaining costs from a hospital stay that your other insurance might not fully catch. If you’re already looking at ways to manage your healthcare, our Medicare Advantage Guide explains how those plans work alongside your other protections. We believe in building a complete safety net so you can stop worrying about the “what ifs.” If you’re ready to see how these pieces fit together for your specific situation, we invite you to explore our coverage options today.

Comparing Final Expense vs. Traditional Life Insurance

When we talk about traditional life insurance, we’re usually discussing policies meant to replace a salary or pay off a large mortgage. These plans often come with high coverage amounts that you simply might not need anymore. Life insurance to cover final expenses is different. It’s designed specifically for the 65+ demographic with smaller face amounts, usually ranging from $2,000 to $40,000. This smaller scale makes it much easier to qualify for; the insurance companies don’t require the same intense medical scrutiny as a million-dollar policy.

We see these plans as a specialized tool for dignity. While a traditional policy might require blood work and a physical, final expense plans focus on simplicity. They are built to cover final expenses such as funeral costs and medical bills, providing exactly what’s necessary to protect your family from debt. This targeted approach means you aren’t paying for extra coverage that doesn’t serve your current stage of life.

Why Term Life May Not Be the Answer

Term life insurance can be a risky choice for seniors because it has a definitive end date. If you outlive your term, your protection simply vanishes. We’ve seen many people reach their 80s only to find their policy has expired. At that age, trying to renew a term policy or buy a new one is incredibly expensive. In 2026, data shows that the sharpest increase in premiums happens between the ages of 75 and 80. Rates for men and women can jump by roughly 45% in that short window. A permanent whole life policy removes this risk entirely. It stays with you for as long as you live, so you never have to worry about losing your safety net.

The Benefit of Fixed Premiums

Budgeting on a fixed income requires total predictability. One of the best features of the policies we recommend is that your monthly premium will never increase. It doesn’t matter if you get older or if your health changes; the price you lock in today is the price you’ll pay for the life of the policy. This fits perfectly with a Social Security budget. You might see offers in the mail for policies where the price starts very low but increases every few years. We advise caution with those plans. They often become unaffordable right when you need them most. Our goal is to provide a reliable, steady cost that gives you peace of mind year after year.

Buying Guide: How Much Final Expense Coverage Do You Need?

Deciding on a coverage amount often feels like a guessing game, but we want to help you find the exact number that brings you peace of mind. You don’t want to overpay for a policy that exceeds your needs. At the same time, you want to ensure your family isn’t left with a balance to pay during their time of grief. We recommend a simple, four-step process to reach a state of certainty about your coverage.

First, decide on your desired arrangements. As we discussed earlier, the choice between burial and cremation significantly changes your baseline cost. Second, look at your current debts. Do you have a credit card balance or a small personal loan that would fall to your spouse or children? Third, factor in an emergency cushion. This extra amount handles final medical bills or hospice co-pays that often arrive weeks after a service. Finally, we suggest consulting with an independent broker. We look at your specific health and budget to see which carrier offers the best value for your needs.

Common Final Expense Tiers

To make things easier, we often group life insurance to cover final expenses into three main tiers based on your goals:

- The $5,000 Tier: This is an excellent choice for those who prefer direct cremation. Since the median cost for direct cremation in 2026 is $2,202, this tier covers the service and leaves a helpful amount for administrative or legal fees.

- The $10,000 to $15,000 Tier: We consider this the “Standard” for a traditional funeral. It comfortably covers the median burial cost of $8,300 and includes enough for a headstone or a small memorial gathering.

- The $25,000+ Tier: This is for those who want to do more than just cover costs. It provides enough to pay off larger debts or leave a small legacy for grandchildren.

Evaluating Insurance Carriers in 2026

When you’re choosing a provider, we look for A-rated companies with a proven history of fast claims processing. In 2026, many of the top carriers have digitized their systems to pay out within 24 to 48 hours of receiving proof of loss. This speed is vital for families who need to pay funeral homes upfront. We also look for policies that include “Living Benefits.” This modern feature allows you to access a portion of your death benefit while you’re still alive if you’re diagnosed with a terminal illness. We handle all this research for you by vetting over 40 different carriers. Our goal is to be your advocate, ensuring you get a policy that is reliable and ethical. If you’re ready to see how these tiers fit your budget, you can view our life insurance options to find the right path forward.

Finding the Right Policy with The Modern Medicare Agency

We believe that protecting your family shouldn’t be a high-pressure experience. Many people feel cornered when they talk to an agent who only represents one company. That agent has to fit your needs into their specific box, even if it’s not the best deal for you. We do things differently. As an independent broker, we work for you, not the insurance company. This “Independent Broker Advantage” means we have the freedom to search the entire market to find life insurance to cover final expenses that actually fits your health and your budget. We act as your personal advocate, removing the stress from a process that often feels cold or clinical.

We often see that final expense planning works best when it’s part of a larger picture. For example, if you already have a Medicare Supplement plan, you already understand the value of predictable, fixed costs. We help you integrate your final expense policy so that your total monthly protection remains manageable. Our goal is to move you from a state of worry about the future to a place of absolute clarity. We provide a clear path to getting a personalized quote without the need for a medical exam or invasive health checks.

Why One Size Does Not Fit All

Different insurance carriers look at health conditions through different lenses. One company might offer a lower premium for someone with well-controlled diabetes, while another might be more lenient with a history of heart issues. Because we vet over 40 carriers, we “shop” your specific profile to find the lowest possible rate available in 2026. This unbiased guidance ensures you aren’t overpaying simply because you were talking to a restricted representative with limited options. We prioritize your peace of mind and long-term security above everything else.

Your Journey to Peace of Mind Starts Here

Getting started is as simple as a warm, conversational phone call. You won’t have to worry about high-pressure tactics or confusing industry jargon. We provide a methodical, step-by-step path that leads you from uncertainty to a state of total protection. Our team offers support across 34 states, providing year-round help whenever your needs or budget might change. We are committed educators who want to help you make an ethical, informed choice for your legacy. Contact us today for a simple, no-obligation final expense quote and let us help you secure the gift of certainty for your loved ones.

Secure Your Legacy with Confidence

We’ve explored how the landscape of end-of-life costs has shifted in 2026 and why a permanent whole life policy is the most reliable way to protect your loved ones. You now understand that a small, targeted policy can remove the massive stress of funeral bills and medical debts. By choosing life insurance to cover final expenses, you ensure that your legacy is one of peace rather than a financial burden. It’s about more than just numbers; it’s about the comfort your family feels knowing everything is handled.

We’ve spent years specializing in senior insurance needs, and we’re licensed in over 34 states to provide that local, expert touch. Because we compare over 40 different carriers, we don’t have to settle for a restricted plan that doesn’t serve you. We find the one that fits your budget and your health profile perfectly. Our mission is to guide you through this journey with empathy and clarity. Get your personalized final expense quote from our independent experts today. You’ve done the hard work of learning your options, and we’re here to help you take that final step toward total certainty.

Frequently Asked Questions

Does life insurance to cover final expenses require a medical exam?

No, most policies available in 2026 do not require a physical exam or blood work. We focus on simplified issue policies that only ask a few basic health questions. Thanks to modern digital underwriting, we can often get you an approval decision in minutes. This process removes the stress of waiting for lab results and makes getting covered much easier than traditional life insurance.

How long does it take for a final expense policy to pay out to my family?

Payouts often happen within just a few days of the insurance company receiving proof of loss. While state laws vary, for example, California has a 30 day deadline and Texas allows up to 60 days, most top carriers in 2026 prioritize speed. We choose to work with companies known for their fast claims processing to ensure your family has the funds they need right away.

Can I get final expense insurance if I have a pre-existing condition like diabetes?

Yes, you can absolutely get coverage even with chronic health conditions. We specialize in finding carriers that are lenient with common issues like diabetes or high blood pressure. If your health challenges are more significant, we can look at guaranteed acceptance options. These plans have no health questions at all, ensuring that every senior has a path to protection.

Will my premiums go up as I get older?

No, your monthly premiums are locked in for the life of the policy as soon as you are approved. These are whole life plans, which means the price you pay today is the same price you’ll pay ten or twenty years from now. This predictability is a cornerstone of the peace of mind we provide, especially for those managing a fixed Social Security budget.

Is the payout from a final expense policy taxable for my children?

Generally, the death benefit payout from life insurance to cover final expenses is not considered taxable income for your beneficiaries. This is one of the primary benefits of using insurance for end-of-life planning. It ensures that the full amount you intended for your funeral or debts goes directly to those costs without being reduced by the IRS.

What is the average cost of a final expense policy for someone over 65 in 2026?

The cost of your policy depends on several individual factors, including your age, gender, and whether you use tobacco. We’ve seen that the sharpest increase in premiums happens between ages 75 and 80, where rates can rise by roughly 45%. Because costs vary so much between companies, we shop over 40 different carriers to find the most affordable monthly payment for your specific profile.

Can I use the money from a final expense policy for things other than a funeral?

Yes, your beneficiaries have the flexibility to use the funds for any immediate needs that arise. While many families use the payout for burial or cremation, it can also cover remaining medical co-pays, utility bills, or even travel expenses for family members coming to a service. We believe this flexibility is vital for protecting your family from a state of financial distress.

What happens if I move to a different state after I buy a policy?

Your coverage stays exactly as it is, no matter where you move within the United States. Life insurance is regulated at the state level, and your policy is governed by the laws of the state where it was originally issued. You don’t need to worry about losing your protection or having to start over with a new plan just because you change your address.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com