A Medicare agent is a licensed professional who specializes in helping people with disabilities navigate Medicare eligibility, enrollment, and coverage options to secure the right healthcare plan. The role of Medicare agent disability planning goes far beyond paperwork. Agents educate beneficiaries on how Social Security Disability Insurance (SSDI), the Centers for Medicare & Medicaid Services (CMS) rules, and Medicare Advantage plans interact. For individuals under 65 with disabilities, and for the families supporting them, this guidance can mean the difference between full coverage and costly gaps. Paulbinsurance has built its practice around exactly this kind of education-first approach since 2007.

What does a Medicare agent do in disability planning?

A Medicare agent serves as a guide, educator, and advocate for people with disabilities who must navigate one of the most complex benefit systems in the country. Their core function is not simply enrolling you in a plan. It is making sure the plan fits your medical needs, your budget, and your broader financial picture.

Agents who specialize in disability planning understand the specific rules that apply to people under 65. They know which enrollment windows apply, which plan types are available, and how a wrong choice can affect other benefits like Supplemental Security Income (SSI) or Medicaid. That knowledge is not standard across all agents, which is why choosing a specialist matters.

Paulbinsurance agents, for example, work across Medicare Advantage plans, Medicare Supplements, Medicare Part D, and related products like hospital indemnity and critical illness coverage. That breadth means they can see your full picture, not just one piece of it.

How do Medicare agents assist with eligibility and enrollment?

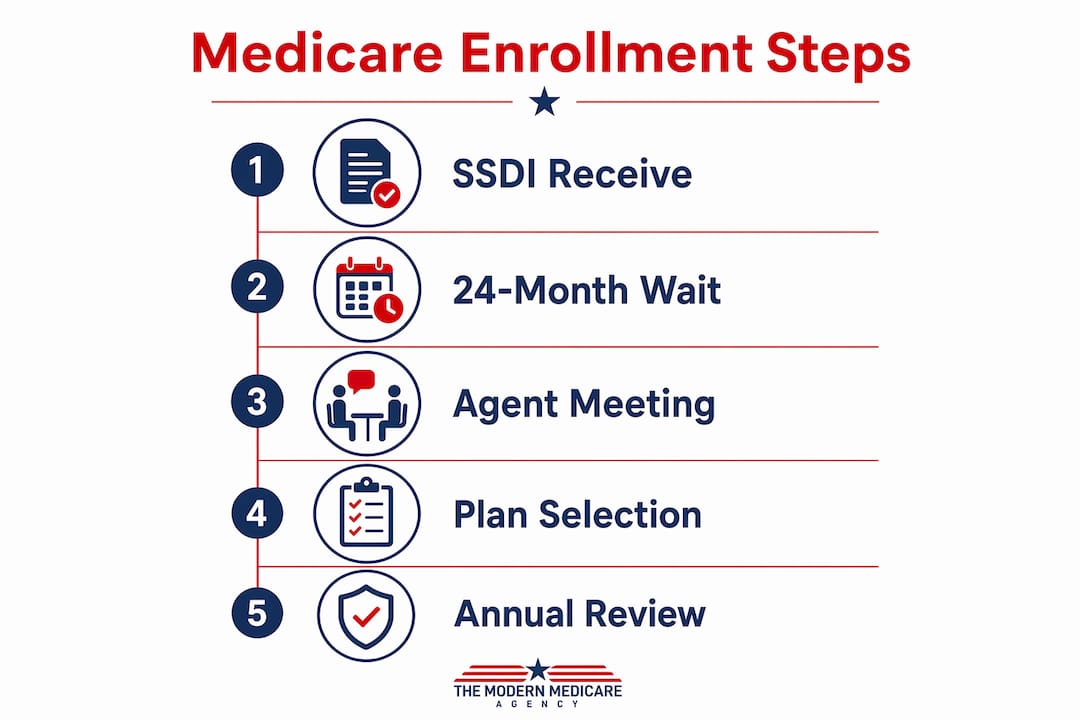

Eligibility for Medicare through disability follows a specific path, and the timing is strict. SSDI recipients receive automatic enrollment in Medicare Parts A and B after a 24-month waiting period, with notification arriving by mail approximately 3 months before coverage begins. Missing that window or misunderstanding it leads to coverage gaps that are hard to fix.

Not every disability category follows the automatic path. People with End-Stage Renal Disease (ESRD) must actively enroll to avoid gaps in coverage. An agent tracks these distinctions and helps you prepare the right documentation at the right time.

There is also a lesser-known provision worth understanding. The SSA’s Ticket to Work program allows disability beneficiaries who return to work to retain Medicare coverage for up to 93 months, though the exact duration depends on employer size and other factors. An agent can explain how that extended coverage period affects your planning.

- Parts A and B basics: Part A covers hospital stays; Part B covers outpatient care and doctor visits. Both activate together for most SSDI recipients.

- Enrollment timing: Your Initial Enrollment Period begins 3 months before your 24th month of SSDI benefits.

- ESRD enrollment: Active enrollment is required. An agent helps you file the correct forms before your coverage start date.

- Late enrollment penalties: Missing your window can trigger permanent premium increases on Part B and Part D.

Pro Tip: Set a calendar reminder 6 months before your 24th month of SSDI benefits. That gives you time to meet with a Medicare agent, review your options, and enroll without rushing.

What plan options exist for people under 65 with disabilities?

Plan selection for people under 65 with disabilities is more limited than most people realize, and that limitation shapes the agent’s entire approach. Most states do not require insurers to offer Medigap plans to individuals under 65 with disabilities. That means the standard Medicare Supplement route available to seniors is often closed to younger beneficiaries.

Medicare Advantage fills that gap. In 2026, Medicare Advantage plans for under-65 beneficiaries commonly include dental, vision, and prescription drug coverage with $0 monthly premiums beyond the standard Part B cost. That bundled structure makes Advantage plans the primary option for most people with disabilities under 65.

An agent’s job during plan selection involves three specific steps. First, they review your current doctors and confirm network participation. Second, they check your prescriptions against each plan’s formulary to avoid surprise drug costs. Third, they factor in your personal preferences, such as whether you want a Health Maintenance Organization (HMO) structure or a Preferred Provider Organization (PPO) with more flexibility.

The Annual Election Period runs from october 15 through december 7 each year. During that window, you can switch Medicare Advantage plans without penalty. An agent reviews your current plan against new offerings each fall so you are never stuck in a plan that no longer fits.

- Medigap availability: Limited in most states for under-65 disabled beneficiaries. Check your state’s rules with an agent.

- Medicare Advantage: Bundled coverage with $0 premium options is the standard path for most under-65 disability beneficiaries.

- Drug coverage: Confirm your prescriptions are covered before you enroll. Formularies change annually.

- Annual review: Plan benefits shift every year. A yearly check-in with your agent protects you from unexpected cost increases.

Pro Tip: Even if your current plan feels fine, review it every october during the Annual Election Period. A better plan with lower drug costs or added dental benefits may be available at no extra cost.

How does Medicare planning coordinate with broader disability financial planning?

Medicare coverage does not exist in isolation. For many people with disabilities, it sits alongside SSI, Medicaid, Special Needs Trusts (SNTs), and ABLE accounts. A Medicare agent who understands this ecosystem helps you make choices that protect all of your benefits, not just your health coverage.

Including Medicare agents as part of a coordinated disability planning team helps safeguard against benefits loss and maximizes both financial and healthcare security. The risk is real. Choosing the wrong Medicare plan or holding assets incorrectly can reduce or eliminate SSI payments, which in turn affects Medicaid eligibility.

Special Needs Trusts and ABLE accounts serve distinct but complementary roles in disability planning. An SNT holds assets for a person with a disability without counting against SSI resource limits. An ABLE account allows tax-advantaged savings for disability-related expenses. A Medicare agent does not replace an attorney or financial planner in setting up these tools, but they do ensure your Medicare choices align with the rules governing them.

- SSI coordination: Certain Medicare Advantage plan benefits, like grocery allowances, can interact with SSI income calculations. An agent flags these issues before enrollment.

- Medicaid interaction: Dual-eligible beneficiaries must understand how Medicare and Medicaid work together. An agent maps that relationship clearly.

- ABLE accounts: Funds in an ABLE account can cover Medicare premiums and out-of-pocket costs without affecting SSI eligibility.

- SNT alignment: Trustees and families benefit from agent input to confirm that Medicare plan choices do not create unintended benefit reductions.

For families navigating both Medicare and legal disability claims, understanding how long-term disability appeals interact with Medicare timing is also worth exploring with a qualified attorney alongside your agent.

What misconceptions do people have about Medicare agents and disability?

The most common misconception is that Medicare and Medicaid are the same program. They are not. Medicare is a federal health insurance program based on age or disability status. Medicaid is a joint federal-state program based on income. Many people with disabilities qualify for both, and that dual eligibility opens access to plans with significant added benefits.

Dual-eligible beneficiaries can access Dual Special Needs Plans (D-SNPs) that include benefits not available under standard Medicare, such as transportation assistance and grocery allowances. Identifying whether you qualify for a D-SNP is one of the most valuable things a Medicare agent does. Most beneficiaries do not know these plans exist until an agent points them out.

A second misconception is that agents only help at enrollment. Medicare agents provide ongoing support throughout the plan lifecycle, including help with appeals, plan changes, and benefit questions that arise mid-year. That ongoing relationship is what separates a good agent from a one-time transaction.

“A Medicare agent who specializes in disability planning does not just find you a plan. They watch your coverage year after year, flag changes that affect you, and make sure your benefits stay intact as your health and life circumstances shift. That ongoing advocacy is the real value.”

When choosing a Medicare agent, look for someone who works independently across multiple carriers, not one tied to a single insurance company. An independent agent compares options across the market and gives you unbiased advice. Paulbinsurance operates as an independent agency, which means the recommendation you receive is based on your needs, not a sales quota.

Key Takeaways

A Medicare agent’s greatest value in disability planning is not enrollment. It is ongoing, coordinated guidance that protects your coverage and your other benefits simultaneously.

| Point | Details |

|---|---|

| Enrollment timing is strict | SSDI recipients must act during their Initial Enrollment Period to avoid permanent premium penalties. |

| Medicare Advantage is the primary option | Most states do not require Medigap access for under-65 disabled beneficiaries, making Advantage plans the standard path. |

| Coordination protects all benefits | Medicare choices must align with SSI, Medicaid, SNTs, and ABLE accounts to avoid unintended benefit reductions. |

| D-SNPs offer hidden value | Dual-eligible beneficiaries often qualify for plans with transportation and grocery benefits most people never discover without an agent. |

| Ongoing support matters | A good Medicare agent assists with appeals, annual plan reviews, and mid-year changes, not just initial enrollment. |

What I’ve learned after nearly two decades of disability Medicare planning

I have worked with Medicare consumers since 2007, and the cases that stay with me are not the complicated ones. They are the straightforward ones that went wrong because nobody explained the basics in plain language.

People with disabilities face a Medicare system that was not originally designed for them. The 24-month SSDI waiting period, the Medigap restrictions, the D-SNP eligibility rules. None of it is intuitive. And the cost of a wrong decision is not just financial. It can mean losing Medicaid, losing SSI, or ending up in a plan that does not cover your doctors or your medications.

What I have seen work, consistently, is the education-first approach. When a beneficiary or a family member understands why a plan is being recommended, they make better decisions and they stick with them. They also ask better questions the following year during the Annual Election Period.

The Medicare landscape for 2026 has shifted in ways that benefit disability enrollees. More $0-premium Advantage plans with bundled benefits are available than ever before. But more options also means more chances to pick the wrong one without guidance. My advice is simple. Do not go through this alone. Work with an independent agent who specializes in disability cases, reviews your full benefit picture, and stays with you after enrollment.

— Paul

Paulbinsurance Medicare agents are here for disability planning

Paulbinsurance specializes in Medicare coverage for people with disabilities, including those under 65 navigating Medicare Advantage for the first time. Our independent agents review your doctors, prescriptions, and benefit situation before recommending any plan.

Whether you are newly eligible through SSDI, exploring D-SNP options as a dual-eligible beneficiary, or helping a family member sort through coverage choices, Paulbinsurance provides personalized guidance at no cost to you. Start with our detailed breakdown of Medicare Advantage plans to understand your options, or connect with a Paulbinsurance agent directly for a one-on-one review of your disability coverage needs.

FAQ

What is the role of a Medicare agent in disability planning?

A Medicare agent guides individuals with disabilities through eligibility, enrollment, and plan selection while ensuring Medicare choices do not jeopardize other benefits like SSI or Medicaid.

When does Medicare start for SSDI recipients?

Medicare Parts A and B begin automatically after a 24-month waiting period for SSDI recipients, with enrollment notification arriving approximately 3 months before coverage starts.

Can people under 65 with disabilities get a Medigap plan?

Most states do not require insurers to offer Medigap to under-65 disabled beneficiaries, making Medicare Advantage for under 65 the primary coverage option in most cases.

What is a Dual Special Needs Plan (D-SNP)?

A D-SNP is a Medicare Advantage plan designed for people who qualify for both Medicare and Medicaid, often including added benefits like transportation and grocery allowances not available in standard Medicare.

How do I choose the right Medicare agent for disability needs?

Choose an independent agent who works across multiple carriers, specializes in disability cases, and provides ongoing support beyond initial enrollment, not just a one-time plan comparison.