In February 2026, a retiree named Robert discovered that his HR department’s advice to stay on COBRA after turning 65 was a mistake that would cost him an extra 10% on his Part B premiums every month for the rest of his life. We know how overwhelming it feels when you’re caught between conflicting instructions from your former employer and Social Security. It’s stressful to worry about whether you can keep your favorite doctors or if you’re overpaying for coverage you don’t actually need. If you’re wondering about medicare and COBRA what are the rules, you deserve clear answers that don’t put your savings at risk.

We’re here to help you move from confusion to confidence by explaining exactly how these two systems interact. You’ll learn how to manage the 8 month special enrollment window and which insurance is required to pay your medical bills first. We’ll provide a clear timeline for your 2026 enrollment so you can secure affordable coverage without the fear of lifelong penalties. This guide breaks down the coordination of benefits and shows you how to protect your healthcare freedom with total peace of mind.

Key Takeaways

- Understand medicare and COBRA what are the rules for coordination in 2026 so you know exactly which plan pays your medical bills first.

- Avoid the “Part B enrollment trap” by learning why COBRA isn’t considered active coverage and how to protect yourself from permanent late-enrollment penalties.

- We compare the high cost of 2026 COBRA premiums against Medicare Advantage and Medigap to help you find more affordable coverage that still includes your trusted doctors.

- Follow our simple, stress-free timeline to transition from your employer plan to Medicare with the clarity and peace of mind you deserve.

- Discover how we provide unbiased guidance to help you navigate the maze of 2026 rules and choose the plan that best fits your unique needs.

Medicare and COBRA Coordination: Who Pays First in 2026?

Leaving a career is a major life transition, and we know how overwhelming it feels to manage your health benefits during that shift. If you lose your job-based insurance, you might be offered the chance to keep your current plan through the Consolidated Omnibus Budget Reconciliation Act (COBRA). While COBRA provides a temporary safety net, it doesn’t work the same way as active employee coverage. We want to help you understand medicare and COBRA what are the rules to ensure you don’t end up with unexpected medical debt.

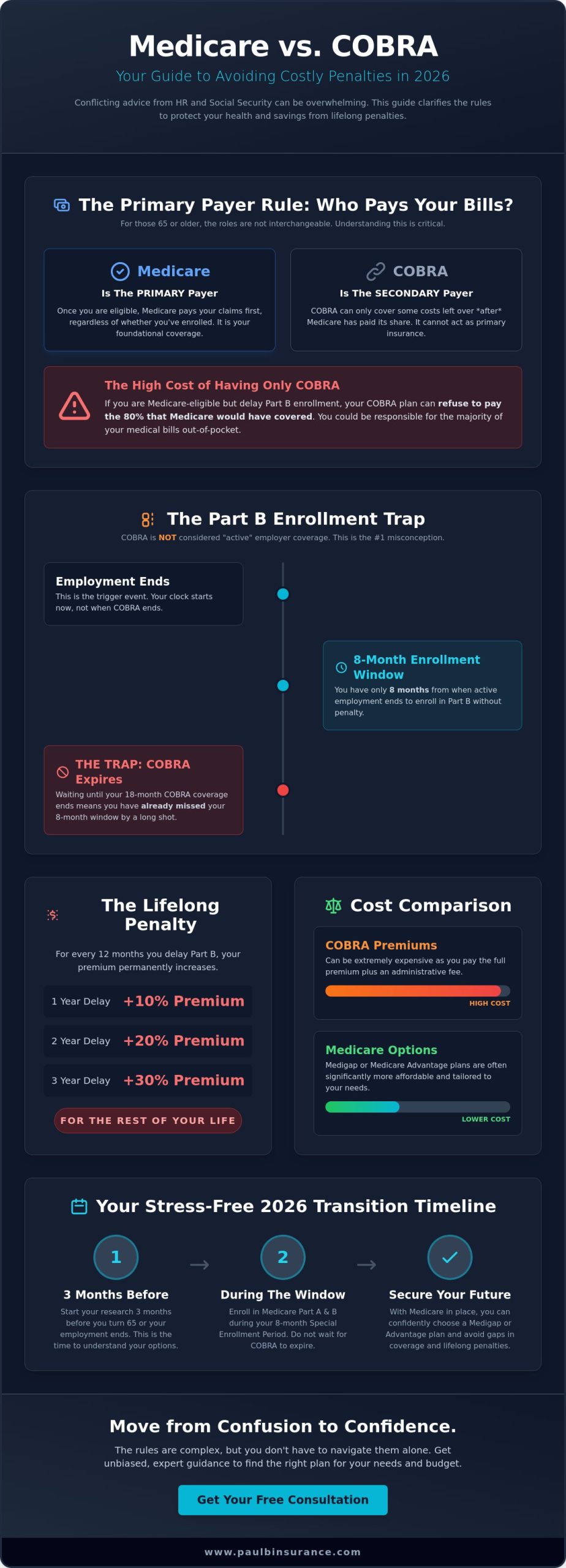

The most critical concept is the Primary Payer Rule. In 2026, for almost everyone aged 65 or older, Medicare is the primary payer. This means Medicare is responsible for paying your claims first. COBRA then acts as a secondary payer, covering only what Medicare leaves behind. This rule applies even if you haven’t signed up for Medicare yet. If you are eligible for Part B but choose to stay only on COBRA, the insurance company can refuse to pay for services that Medicare would have covered. This could leave you paying 80 percent of a hospital bill out of your own pocket.

- Large Employers (20+ employees): Medicare is primary, and COBRA is secondary.

- Small Employers (Under 20 employees): Medicare is always primary, and rules are even more rigid.

- The Financial Risk: Without Medicare Part B, you are essentially uninsured for the majority of your medical costs because COBRA will not pay the primary portion.

If You Have Medicare Before Getting COBRA

If you already have Medicare Part A and B when you qualify for COBRA, you usually cannot keep the full COBRA plan. Your employer is allowed to terminate your COBRA coverage because you already have Medicare. Most of our clients find it much more cost-effective to drop the expensive COBRA premiums and move to a supplement or an Advantage plan. We also suggest looking closely at Medicare Part D to handle your prescriptions, as COBRA drug coverage can be significantly more expensive than a standalone Part D plan in 2026.

If You Have COBRA Before Getting Medicare

When you turn 65 while already enrolled in COBRA, your coverage will almost certainly end. The month you become eligible for Medicare is a trigger event that allows the COBRA provider to stop your benefits. We see many seniors wait until their COBRA runs out to look for Medicare, only to find they have missed their enrollment window. To stay protected, we recommend starting your search 3 months before your 65th birthday. Knowing medicare and COBRA what are the rules ahead of time helps us move you from confusion to confidence without any gaps in your care.

The Part B Enrollment Trap: Why COBRA Isn’t ‘Active’ Coverage

We often see people breathe a sigh of relief when they receive their COBRA paperwork. It feels like a safety net that buys you 18 months of time to figure things out. However, when it comes to Medicare, this safety net is often a disguised trap. The biggest misconception we encounter is the belief that having COBRA coverage grants you a Special Enrollment Period (SEP) to join Medicare later. This is simply not true in 2026. Understanding medicare and COBRA what are the rules is about more than just knowing your monthly costs; it’s about protecting your future budget from permanent penalties.

The Social Security Administration is very strict about the eight-month window for enrolling in Part B. This window begins the month after your “active employment” ends. It does not matter if your COBRA coverage lasts for another year or more. If you wait until your COBRA expires to sign up for Medicare, you’ve likely already missed your chance to enroll without a penalty. This article from Forbes explains the Part B Enrollment Trap and how it catches even the most diligent retirees off guard.

The cost of making this mistake is high and permanent. For every 12-month period you were eligible for Part B but didn’t have “active” employer coverage, your premium increases by 10%. This isn’t a one-time fee. It’s a lifetime surcharge added to your monthly bill. In 2026, those extra costs can add up to thousands of dollars over the course of your retirement. We want to help you avoid this unnecessary drain on your savings.

Defining ‘Active Employment’ for Social Security

The definition used by the Social Security Administration (SSA) is the only one that matters here. Active Employment is work performed for an employer by a current employee. If you’re receiving a severance package or you’re on COBRA, you’re no longer considered an active employee in their eyes. Even if your former company provides “extended” retiree benefits that look exactly like your old plan, it doesn’t count as active work. To verify your status, we recommend looking at your tax records or asking your HR department specifically if you’re classified as a “current active employee” for Medicare purposes. If the answer is no, your eight-month clock is already ticking.

The Danger of the General Enrollment Period

If you miss that eight-month window because you stayed on COBRA too long, you’re forced into the General Enrollment Period. This period only runs from January 1st through March 31st each year. The real danger here is the gap in coverage. If you sign up in February, your Medicare coverage won’t actually start until the following month, but historically, many people faced a July 1st effective date. While rules have shifted to make coverage start the month after you sign up, missing your window still leaves you vulnerable and uninsured for months if your COBRA ends unexpectedly. We help our clients move from confusion to confidence by mapping out these dates long before the deadline hits, ensuring you never have a single day without protection.

Evaluating Costs: COBRA Premiums vs. Medicare Advantage and Medigap

When you’re looking at your options, the price tag is often the first thing that catches your eye. COBRA is famous for being expensive because you’re paying the full premium plus a 2% administrative fee. That’s 102% of the total cost your employer used to help cover. In 2026, the standard Medicare Part B premium is projected to be $192.50 per month. Even when you add a Medigap plan to cover the 20% that Medicare doesn’t pay, your monthly total often stays well below a COBRA premium. We want to help you understand medicare and COBRA what are the rules so you don’t overpay for coverage you could get elsewhere for less.

Drug costs are another huge factor this year. Thanks to the Inflation Reduction Act, Medicare Part D now has a $2,000 annual out-of-pocket cap in 2026. If your COBRA plan has a high deductible for prescriptions, switching to Medicare could save you thousands. You should also look at your doctors. Many people stay on COBRA just to keep their current physicians, but we often find those same doctors are already in Medicare networks. This U.S. Department of Labor guide on COBRA explains how these benefits overlap, which is a great starting point for your research. We simplify these details so you can see which path protects your wallet and your health.

When Does Keeping COBRA Actually Make Sense?

Sometimes, staying put is the right move. If you’ve already hit your out-of-pocket maximum or high deductible for 2026, COBRA might be cheaper for the rest of the year. We also see this work well for families. If you have a younger spouse or kids on your plan, they can’t move to Medicare with you. In those cases, you might keep COBRA for the family or just keep dental insurance through your former employer while you move your medical care to Medicare. It’s about finding the balance that keeps everyone covered without unnecessary stress.

The Savings Potential of Switching

Switching can lead to massive monthly savings. Many Medicare Advantage plans offer $0 premiums because they’re funded differently than private employer plans. While COBRA premiums stay high, Medicare gives you choices. We help you compare these costs side-by-side. Locking in a Medigap rate early also protects you from future price hikes. It’s about moving from confusion to confidence by seeing the real numbers. We’ll show you exactly how medicare and COBRA what are the rules apply to your specific bank account and your unique needs.

Your 2026 Timeline for Switching from COBRA to Medicare

We know the clock feels like it’s ticking when you’re on a temporary plan. Moving from a former employer’s coverage to Medicare involves specific windows that you cannot afford to miss. By following a structured six month plan, we can replace your anxiety with a clear sense of direction. It’s about moving from confusion to confidence.

- Months 1-3: Start by looking at your current COBRA summary of benefits. Most people pay 102% of the plan’s full cost, which is often a shock to the budget. We’ll help you compare this high monthly premium against the 2026 Medicare Part B rates to see exactly how much you’ll save.

- Month 4: This is the most critical month. You must contact Social Security to start your Part B enrollment. Many folks think they can stay on COBRA for the full 18 months before joining Medicare, but that’s a dangerous mistake. Understanding medicare and COBRA what are the rules is vital here because COBRA is not considered “active” employment coverage. If you wait too long, you’ll face a lifetime late enrollment penalty.

- Month 5: Now we look at your lifestyle. Do you want the “Freedom of Choice” found in a Medigap plan, or do you prefer the “All-in-One” structure of Advantage? We check your specific doctors against the 2026 provider networks to ensure your transition is seamless.

- Month 6: We finalize your Part D prescription plan. This ensures you have no gap in coverage. A gap of even one month can lead to a permanent penalty added to your monthly costs, so we get this right the first time.

Gathering Your Documentation

We need to prove to the government that you didn’t just skip out on insurance after turning 65. You’ll need Form CMS-L564. Your former employer or HR department fills this out to verify you had “active” group coverage. This form is your golden ticket to waiving the Part B late penalty. In 2026, you can upload this directly to the Social Security portal or mail it to your local office. We’ll walk you through the form to make sure every box is checked correctly.

Choosing Your New Path

Deciding between Medigap and Advantage is a personal choice. Medigap lets you see any doctor in the country who accepts Medicare, which is about 98% of providers. Alternatively, our Medicare Advantage guide explains how those plans bundle dental, vision, and hearing into one package. We always aim for your new coverage to start on the first day of the month. This coordination prevents double billing and ensures you’re never without protection.

Don’t let the “COBRA trap” catch you off guard. Schedule a Call With Paul to build your personalized 2026 transition plan today.

Finding Confidence: How an Independent Broker Simplifies the Rules

Deciding between staying on COBRA or moving to Medicare is one of the most stressful financial choices you will make this year. Many people naturally turn to their HR department for guidance. While HR managers are experts at handling company benefits, they are rarely Medicare specialists. In 2026, the coordination rules are more technical than ever. We often see HR representatives give well-meaning but incorrect advice, such as telling employees that COBRA counts as “creditable coverage” for Part B. This mistake leads to permanent late enrollment penalties that stay with you for life.

We provide an unbiased advantage because we aren’t tied to a single insurance company. We represent over 40 different carriers. This independence allows us to focus entirely on your needs rather than a corporate sales quota. When you ask about medicare and COBRA what are the rules, we don’t just give you a pamphlet; we give you a roadmap. Our goal is to move you from a state of confusion to a state of total confidence through our proven 5-step process:

- Listen: We learn about your health priorities and budget.

- Analyze: We compare your current COBRA costs against 2026 Medicare premiums.

- Search: We check 40+ carriers to ensure your specific doctors are in-network.

- Simplify: We translate the jargon into plain English so you understand your coverage.

- Enroll: We handle the paperwork and provide year-round support as rules change.

The Difference Between a Broker and a Captive Agent

A captive agent works for one specific insurance company. They can only show you what that one company offers, even if a better or more affordable plan exists elsewhere. As independent brokers, we shop the entire market for you. This variety is essential in 2026 because plan networks and drug formularies change frequently. Having more options typically leads to lower monthly costs and better access to the specialists you trust. We review your plan every year to ensure it still serves you well. Medicare rules are not static, and your coverage shouldn’t be either.

Next Steps: Schedule a Call With Paul

You don’t have to solve this puzzle alone. We invite you to book a complimentary 15-minute consultation to discuss your specific situation. During this call, we will look at your current COBRA costs and compare them to the updated 2026 Medicare benchmarks. There is never a fee for our services because the insurance carriers compensate us directly. You get expert, personalized guidance at no cost to you. Schedule a Call With Paul to review your COBRA vs. Medicare options today and gain the peace of mind you deserve.

Take Control of Your 2026 Healthcare Journey

Navigating the transition from employer coverage to Medicare in 2026 doesn’t have to be a source of stress. We’ve seen how easy it’s to fall into the Part B enrollment trap because many people assume COBRA counts as active employment coverage. It doesn’t. Missing your window can lead to lifetime penalties and gaps in your care that no one should have to face. Understanding medicare and COBRA what are the rules for 2026 is the first step toward protecting your savings and your health.

We take the weight off your shoulders by comparing options across 40+ carriers to find the right fit for your specific needs. Our team has provided personalized guidance to seniors in over 34 states, acting as expert educators featured in Medicare planning resources. You don’t have to guess which plan is best or worry about the fine print alone. We’re here to simplify the jargon and give you a clear path forward.

You’ve worked hard for your retirement; let’s make sure your healthcare works just as hard for you.

Frequently Asked Questions

Is COBRA considered creditable coverage for Medicare Part B?

No, COBRA isn’t considered creditable coverage for Medicare Part B. While it feels like a continuation of your work insurance, the Social Security Administration doesn’t view it as active employment coverage. If you wait until your COBRA ends to sign up for Part B, you’ll likely face a lifetime late enrollment penalty and a gap in your health care. We’ve seen many people get caught in this trap, but we’re here to help you avoid it.

Can I have Medicare and COBRA at the same time?

Yes, you can have both, but they must follow specific coordination of benefits rules. In this scenario, Medicare acts as your primary payer, while COBRA serves as secondary insurance to help cover remaining costs like deductibles. We help you look at the math to see if paying two premiums makes sense for your budget in 2026. Most of our clients find that Medicare alone offers better value and simpler claims.

What happens to my spouse’s COBRA if I switch to Medicare?

Your spouse usually keeps their coverage for up to 36 months if you transition to Medicare. This is a federal protection under the Consolidated Omnibus Budget Reconciliation Act. It ensures your partner stays protected even when your own insurance status changes, giving you both peace of mind during the transition. We’ll help you review the 2026 costs to ensure this is the most cost effective path for your family’s unique needs.

How much is the Medicare Part B late enrollment penalty in 2026?

The Medicare Part B late enrollment penalty is an extra 10% added to your monthly premium for every full 12 month period you were eligible but didn’t sign up. This penalty stays with you for as long as you have Part B. For example, if you waited 24 months, you’ll pay a 20% surcharge on top of the standard 2026 premium every single month. It’s a permanent cost we want to help you avoid.

Do I need Medicare Part D if I have COBRA prescription drug coverage?

You only need Medicare Part D if your COBRA drug coverage isn’t considered creditable, meaning it doesn’t meet Medicare’s minimum standards. Your plan administrator must send you a notice by October 15 each year confirming its status. If it’s not creditable, you have 63 days to join a Part D plan to avoid a lifetime penalty. We’ll help you check your current plan’s status so you stay protected and avoid future fees.

What is the 8-month Special Enrollment Period for Medicare?

The 8 month Special Enrollment Period lets you sign up for Part B without a penalty after your group health coverage ends. This window begins the month your employment ends or the month your group insurance stops, whichever happens first. It’s vital to remember that COBRA doesn’t extend this window; the clock starts ticking the moment you stop being an active employee. We make sure you hit these deadlines with total confidence.

Can COBRA cancel my coverage once I become eligible for Medicare?

Yes, a COBRA provider can legally cancel your coverage if you enroll in Medicare after you’ve already started COBRA. However, if you already had Medicare before you elected COBRA, you can usually keep both. Understanding medicare and COBRA what are the rules helps you avoid a sudden loss of benefits when you need them most. We’ll guide you through the timing to ensure your coverage remains seamless, secure, and uninterrupted.

Is it better to have Medicare or COBRA?

Medicare is almost always the more affordable and comprehensive choice for seniors in 2026. COBRA premiums are often 102% of the full plan cost because you’re paying both the employee and employer portions. We find that switching to Medicare typically lowers monthly costs by hundreds of dollars while providing more stable, long term protection. We’ll help you compare the numbers so you can make a choice that brings you true peace of mind.