A Medicare deductible is the amount you pay out of pocket before Medicare begins covering your healthcare costs. For new enrollees turning 65 or leaving employer coverage, understanding this upfront cost is the difference between a manageable budget and a financial surprise. Medicare Parts A, B, and D each carry their own deductible structure, and the 2026 amounts have shifted from prior years. This guide breaks down every deductible, what triggers it, and what you pay after it is met.

What is the Medicare deductible, and why does it matter in 2026?

A Medicare deductible is not a single annual number. It varies by plan part, resets on different schedules, and can apply more than once in a year depending on your health. Most people transitioning from employer coverage expect one annual deductible like they had at work. Medicare works differently, and that difference catches new enrollees off guard every year.

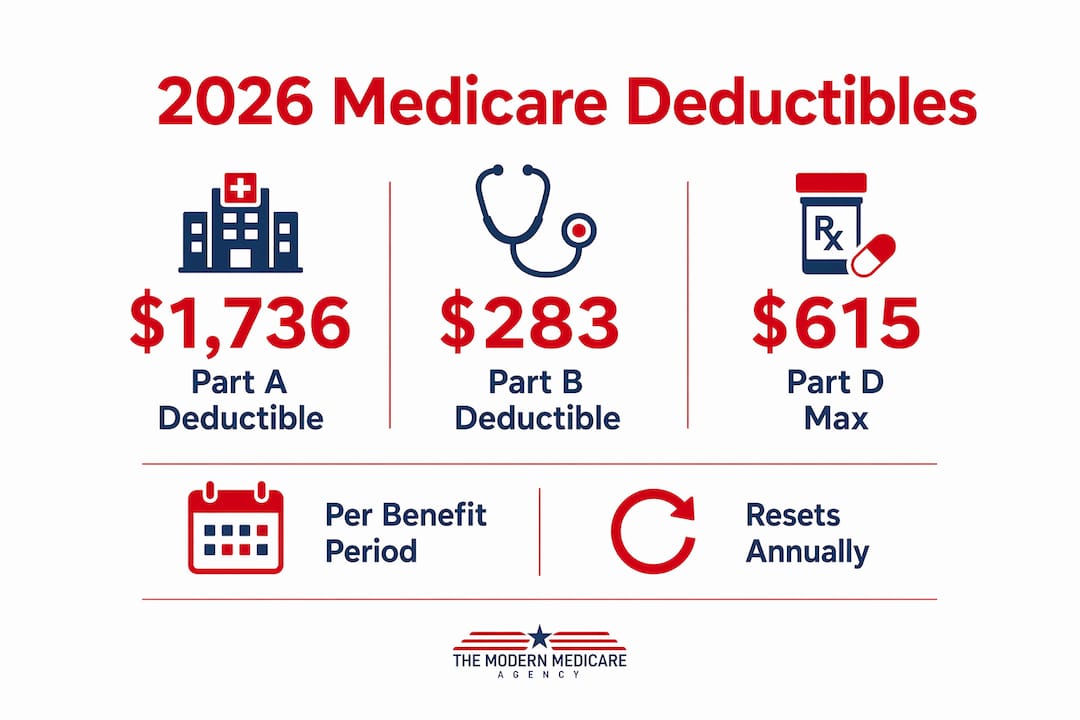

The Centers for Medicare and Medicaid Services (CMS) sets deductible amounts annually. For 2026, the three main deductibles are $1,736 for Part A, $283 for Part B, and up to $615 for Part D. Each one applies under different conditions, which is why understanding Medicare costs as a whole matters more than memorizing a single figure.

Deductibles are just one layer of what you pay. Premiums, coinsurance, copays, and income-based surcharges all stack on top. Knowing how each piece fits together lets you plan your retirement healthcare budget with accuracy instead of guesswork.

How does the Medicare Part A deductible work?

The Part A deductible is $1,736 per benefit period in 2026, not per calendar year. That distinction matters enormously. A benefit period begins the day you are admitted as a hospital inpatient and ends after you have been out of inpatient care for 60 consecutive days.

The 60-day rule is the part most new enrollees miss. Readmission within 60 days does not trigger a new deductible. But if you are discharged, recover at home for 61 days, and then return to the hospital, you owe the full $1,736 again. Two separate hospital stays in one calendar year can cost you $3,472 in Part A deductibles alone.

After you meet the deductible, coinsurance kicks in based on how long you stay:

- Days 1–60: $0 coinsurance. The deductible covers this window.

- Days 61–90: $434 per day in coinsurance.

- Days 91–150: $868 per day (lifetime reserve days).

- Beyond 150 days: Medicare pays nothing. All costs fall to you.

| Hospital Stay Length | Your Cost Per Day |

|---|---|

| Days 1–60 | $0 (after $1,736 deductible) |

| Days 61–90 | $434 |

| Days 91–150 | $868 |

| Beyond 150 days | 100% of costs |

Pro Tip: Ask your hospital whether you are admitted as an inpatient or placed under “observation status.” Observation status is outpatient care, which means your stay does not count toward a benefit period and your costs fall under Part B instead.

What is the Medicare Part B deductible, and how does it affect outpatient costs?

The Part B annual deductible is $283 in 2026, and it resets every january 1. Unlike Part A, you only pay it once per calendar year regardless of how many doctor visits or outpatient procedures you have. After you meet it, Medicare pays 80% of approved costs and you pay the remaining 20%.

That 20% coinsurance has no annual cap under Original Medicare. A $50,000 outpatient surgery leaves you with a $10,000 bill after the deductible. This is the structural gap that makes supplemental coverage worth examining for most new enrollees.

Common Part B services subject to the deductible and coinsurance include:

- Doctor office visits and specialist consultations

- Outpatient surgery and procedures

- Lab tests, X-rays, and imaging

- Durable medical equipment like wheelchairs or walkers

- Outpatient mental health services

Pro Tip: Preventive services like the annual wellness visit, flu shots, and many cancer screenings are covered at 100% under Part B with no deductible required. Schedule these early in the year to get full value from your coverage.

One detail worth knowing: if your doctor does not accept Medicare assignment, they can charge up to 15% above the Medicare-approved amount. That excess charge is not covered by Medicare and adds to your out-of-pocket total.

Understanding Medicare Part D deductibles and prescription drug costs

Part D covers prescription drugs, and its deductible structure is more flexible than Parts A or B. The maximum Part D deductible is $615 in 2026, but individual plans set their own amounts up to that ceiling. Many plans charge less, and some waive the deductible entirely for lower-tier generic drugs.

The biggest change in recent years is the out-of-pocket cap. Under the Inflation Reduction Act, Part D spending is capped at $2,100 once you reach that threshold in covered drug costs. After that point, you pay $0 for covered prescriptions for the rest of the calendar year. That cap is a significant protection for people on high-cost medications.

Part D coverage moves through phases during the year:

- Deductible phase: You pay 100% of drug costs until you meet your plan’s deductible.

- Initial coverage phase: You pay copays or coinsurance; your plan pays the rest.

- Catastrophic phase: Once out-of-pocket costs hit $2,100, you pay nothing for covered drugs.

| Part D Phase | What You Pay |

|---|---|

| Deductible phase | 100% of drug costs (up to $615 max) |

| Initial coverage phase | Copays or coinsurance per drug tier |

| Catastrophic phase | $0 for covered drugs |

Pro Tip: Compare plan formularies, not just premiums. A plan with a $0 deductible but high coinsurance on your specific drugs can cost more annually than a plan with a $400 deductible and low copays. Use the Medicare Plan Finder tool at Medicare.gov to run the numbers on your actual prescriptions.

For a deeper look at Part D coverage phases and how the old donut hole was replaced, Paulbinsurance has a dedicated guide covering the full 2026 structure.

How do Medicare Advantage and Medigap plans interact with deductibles?

Original Medicare and Medicare Advantage handle deductibles and cost sharing very differently. Medicare Advantage plans cap in-network out-of-pocket costs at $9,250 in 2026. That ceiling protects you from catastrophic costs in a way that Original Medicare does not.

Original Medicare carries no annual out-of-pocket maximum for Parts A and B combined. That means a serious illness or extended hospital stay can generate unlimited cost sharing. This structural gap is why most financial planners recommend some form of supplemental coverage for people on Original Medicare.

Two main options exist for filling that gap:

- Medicare Advantage (Part C): Replaces Original Medicare with a private plan. Includes an out-of-pocket maximum, often adds dental, vision, and hearing benefits, but restricts you to a network of providers.

- Medigap (Medicare Supplement): Works alongside Original Medicare. Medigap plans are lettered A through N with varying coverage levels. Higher-tier plans like Plan G cover the Part A deductible, Part B coinsurance, and excess charges.

The trade-off is real. Medicare Advantage plans often carry $0 premiums but require referrals, prior authorizations, and network restrictions. Medigap plans charge monthly premiums but give you access to any provider that accepts Medicare nationwide. For people who travel frequently or want to see specialists without referrals, Medigap often wins on flexibility.

For help deciding between these two paths, Paulbinsurance offers a direct comparison at Medicare Advantage vs. Supplements.

What other costs should new Medicare enrollees plan for?

Deductibles are one piece of a larger cost picture. New enrollees frequently miss all four cost categories: premiums, deductibles, coinsurance and copays, and IRMAA surcharges. Missing any one of them leads to budget shortfalls in the first year.

IRMAA (Income-Related Monthly Adjustment Amount) is the surcharge that higher-income beneficiaries pay on top of standard Part B and Part D premiums. IRMAA thresholds for 2026 are $106,000 for single filers and $212,000 for joint filers, based on your income from two years prior. If your 2024 income exceeded those levels, you will pay more for Medicare in 2026 regardless of your current income.

The standard Part B premium in 2026 is $185 per month. IRMAA surcharges can push that figure significantly higher depending on your income bracket. Part D premiums vary by plan, but IRMAA adds a separate surcharge on top of whatever your plan charges.

Key cost categories to budget for:

- Premiums: Monthly payments for Parts B and D, plus any Medigap or Advantage plan premium.

- Deductibles: Part A per benefit period, Part B annually, Part D annually.

- Coinsurance and copays: The percentage or flat fee you pay after deductibles are met.

- IRMAA surcharges: Income-based additions to Part B and Part D premiums.

Pro Tip: If your income dropped due to retirement, marriage, divorce, or another qualifying life event, you can appeal your IRMAA surcharge using Form SSA-44. CMS will recalculate based on your current income rather than the two-year-old figure.

For a full breakdown of lowering out-of-pocket Medicare costs, Paulbinsurance covers practical strategies that go beyond just picking the right plan.

Key Takeaways

Medicare deductibles vary by part, reset on different schedules, and stack with premiums, coinsurance, and IRMAA surcharges to form your true annual Medicare cost.

| Point | Details |

|---|---|

| Part A deductible resets per benefit period | You can owe $1,736 more than once per year if readmitted after 60 days. |

| Part B deductible resets annually | The $283 deductible applies once per calendar year, then 20% coinsurance continues with no cap. |

| Part D has a $2,100 out-of-pocket cap | Once you hit that threshold, covered drugs cost $0 for the rest of the year. |

| Original Medicare has no out-of-pocket maximum | Without supplemental coverage, your cost exposure is unlimited under Parts A and B. |

| IRMAA affects higher-income enrollees | Single filers earning over $106,000 in 2024 will pay surcharges on 2026 Part B and Part D premiums. |

What I’ve learned after nearly two decades helping Medicare enrollees

I have been working with Medicare beneficiaries since 2007, and the single most common mistake I see is treating Medicare like employer coverage. People assume one deductible, one reset date, one maximum. Medicare does not work that way, and the cost of that assumption can be thousands of dollars.

The benefit period concept for Part A is the biggest blind spot. I have spoken with people who had two hospitalizations in one year and were genuinely shocked to owe two full deductibles. Nobody told them that 60 days without inpatient care resets the clock.

The second thing I tell every new enrollee: review your plan every October during Open Enrollment. Plan formularies change, premiums shift, and the plan that worked perfectly this year may cost you significantly more next year. Staying enrolled in the same plan by default is one of the most expensive habits in Medicare.

Finally, do not wait until you have a health event to understand your coverage. The people who navigate Medicare well are the ones who learned the rules before they needed them. That is exactly why education comes first at Paulbinsurance.

— Paul

Managing your Medicare deductibles with the right supplement plan

Knowing your deductibles is the first step. Covering them is the second.

Medicare Supplement plans, also called Medigap, are designed to pick up the costs that Original Medicare leaves behind. Depending on the plan letter you choose, Medigap can cover your Part A deductible, your Part B coinsurance, and even excess charges from doctors who do not accept Medicare assignment. That coverage pairs with any provider who accepts Medicare, giving you nationwide access without network restrictions. At Paulbinsurance, our independent agents help you compare Medicare Supplement options side by side so you can choose the coverage that fits your health needs and budget. Paul Barrett and the team have been doing this since 2007, and the consultation costs you nothing.

FAQ

What is a Medicare deductible?

A Medicare deductible is the amount you pay for covered services before Medicare begins paying its share. Each part of Medicare, Parts A, B, and D, has its own separate deductible.

How does the Part A deductible differ from Part B?

The Part A deductible is $1,736 per benefit period and can apply more than once per year. The Part B deductible is $283 per calendar year and resets every january 1.

Can I have more than one Part A deductible in a single year?

Yes. If you are discharged from inpatient care and remain out of the hospital for 60 consecutive days, a new benefit period begins and the $1,736 deductible applies again.

Does Medicare Advantage eliminate these deductibles?

Medicare Advantage plans set their own deductible and cost-sharing structures, and they cap your in-network out-of-pocket costs at $9,250 in 2026. Original Medicare has no such cap.

What is the Part D out-of-pocket maximum in 2026?

The Part D out-of-pocket cap is $2,100 in 2026 under the Inflation Reduction Act. Once you reach that amount in covered drug spending, you pay $0 for covered prescriptions for the rest of the year.