What if the most important healthcare decision of your life didn’t have to feel like a math test you’re destined to fail? We’ve seen so many people paralyzed by the fear of making a mistake that leads to lifelong late enrollment penalties. It’s frustrating when your mailbox is stuffed with confusing mailers and you’re just trying to find medicare explained simply for beginners without the high-pressure sales pitch.

We understand the stress of trying to distinguish between the $202.90 standard Part B premium and the various out-of-pocket caps for 2026. You deserve to feel secure and protected, not confused. In this guide, we strip away the industry jargon to give you a clear, step-by-step map of your options. We’ll show you exactly how to identify your enrollment window and explain the real differences between Advantage and Supplement plans. By the time you finish reading, you’ll have the tools to choose your coverage with total confidence and peace of mind.

Key Takeaways

- Get a clear mental map of the different Medicare parts so you can finally have medicare explained simply for beginners without the usual headache.

- Learn to navigate the two distinct paths available in 2026, choosing between Original Medicare with a Supplement plan or an all-in-one Medicare Advantage plan.

- Identify how to protect yourself from high medication costs and the financial gaps that Original Medicare alone leaves behind.

- Pinpoint your personal seven-month enrollment window to ensure you never face the lifelong Part B penalties that catch many people off guard.

- Discover why an independent advocate is your best ally in comparing dozens of plans to find the perfect fit for your specific doctors and prescriptions.

The Basics of Medicare: Understanding the Alphabet Soup

Medicare is the federal health insurance program designed primarily for people 65 and older, though it also serves younger individuals with certain disabilities. We know that the moment you approach your 65th birthday, your mailbox starts overflowing with flyers and fine print. It feels like you’re being asked to learn a new language overnight. To get medicare explained simply for beginners, we always start by focusing on the foundation: Original Medicare.

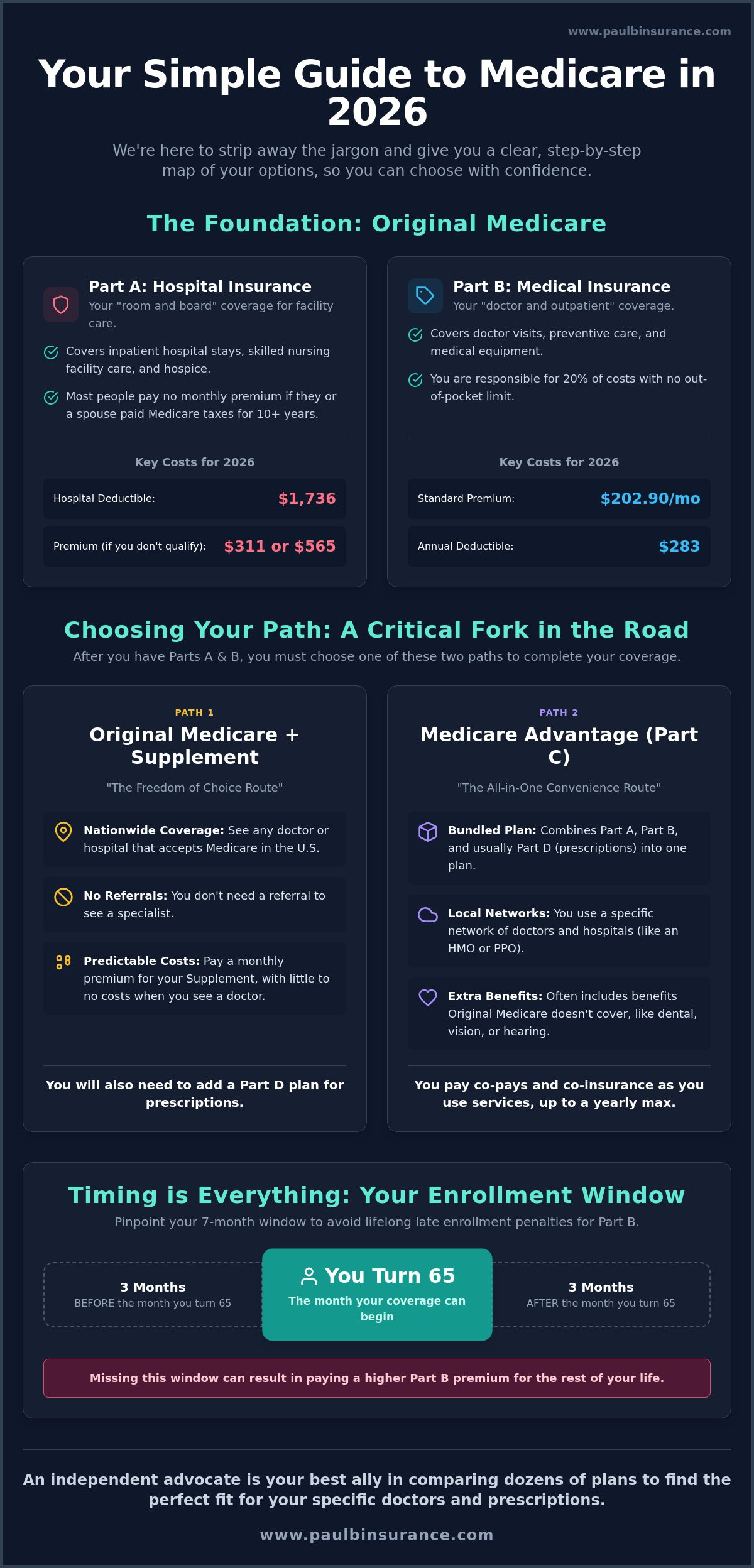

Think of Original Medicare as a two-part foundation for your healthcare house. We describe Part A as your “room and board” coverage because it handles your care when you’re admitted to a facility. In contrast, we view Part B as your “doctor and outpatient” coverage, which takes care of almost everything else. For 2026, Medicare Part A is officially defined as your hospital insurance. These two parts are the starting point for every beginner because they provide the basic security you need before you decide how to enhance your coverage.

Medicare Part A: Hospital Insurance

Part A is there for you during major health events. It covers inpatient hospital stays, care in a skilled nursing facility, and hospice care. Most people receive Part A with no monthly premium because they, or their spouse, paid Medicare taxes while working for at least 10 years. If you don’t qualify for premium-free Part A in 2026, the monthly cost is either $311 or $565, depending on your work history.

While the premium is often zero, Part A isn’t completely free when you use it. In 2026, the inpatient hospital deductible is $1,736 per benefit period. You’ll also face daily coinsurance costs if your hospital stay lasts longer than 60 days. Understanding the history and structure of Medicare helps you see that while Part A is robust, it’s designed to share costs with you rather than covering every penny.

Medicare Part B: Medical Insurance

Part B is the part of Medicare you’ll likely use most often. It covers your regular doctor visits, preventive services like annual wellness exams, and durable medical equipment like walkers or oxygen tanks. For most people in 2026, the standard monthly premium is $202.90. If you’re already receiving Social Security benefits, this amount is typically deducted from your check automatically so you don’t have to worry about missing a payment.

Before Part B starts paying, you must meet an annual deductible, which is $283 in 2026. Once that’s met, Medicare generally pays 80% of the cost for covered services. We want to be very clear about one thing: you are responsible for the remaining 20% coinsurance. This 20% has no “cap” or limit, which is why medicare explained simply for beginners must always include a discussion on how to protect yourself from these potentially high out-of-pocket costs.

Choosing Your Path: Original Medicare vs. Medicare Advantage

Once you understand the basics of Parts A and B, you face a critical fork in the road. This is where most people feel the most pressure, but we’re here to make medicare explained simply for beginners even easier. You essentially have two distinct paths to choose from, and the “right” one depends entirely on your lifestyle and how you prefer to pay for your healthcare. It’s a choice between maximum flexibility and all-in-one convenience.

Medicare Supplement plans offer predictable costs and nationwide access for a monthly premium, while Medicare Advantage plans provide lower premiums and extra benefits in exchange for using a specific network of doctors. Deciding which path to take usually comes down to whether you prefer a fixed monthly budget or if you’re comfortable with “pay-as-you-go” co-pays when you visit the doctor.

Path 1: The “Freedom of Choice” Route

If you value the ability to see any doctor who accepts Medicare anywhere in the country, Path 1 is likely your best fit. This route involves keeping Original Medicare as your primary coverage and adding Medicare Supplement insurance, also known as Medigap. Because Original Medicare only covers about 80% of your outpatient costs, a Supplement plan steps in to pay some or all of that remaining 20%.

We often recommend this path to people who travel frequently or spend part of the year in a different state. You won’t need referrals to see a specialist, and you aren’t restricted to a local network. While you’ll pay a monthly premium for the Supplement plan, your out-of-pocket costs at the doctor’s office are minimal or even zero. You can find more details in the official guide to getting started with Medicare if you want to see how the government outlines these steps. It’s the ultimate path for peace of mind and total doctor flexibility.

Path 2: The “All-in-One” Medicare Advantage Route

Path 2 is a very different journey. These Medicare Advantage plans, sometimes called Part C, are offered by private companies. They replace the way you receive your Part A and Part B benefits, often rolling them together with drug coverage into one single plan. This can make your life much simpler if you prefer having just one insurance card in your wallet.

Many people are drawn to these plans because the monthly premiums are often very low. In 2026, the average premium for these plans is actually projected to decrease to about $11.50 per month. They also include “extra” benefits that Original Medicare doesn’t cover, such as dental, vision, and hearing coverage. The trade-off is that you must stay within a specific network of doctors and hospitals. If you see someone out of network, you might pay the full cost yourself. Also, you’ll have a maximum out-of-pocket limit, which for 2026 can be as high as $9,250 for in-network care. If you’re feeling stuck between these two options, we can help you compare specific plans in your area to see which network includes your current doctors.

Filling the Gaps: Prescription Drugs and Extra Protection

While Parts A and B provide a strong foundation, they don’t cover everything. Relying on Original Medicare alone leaves you with significant financial exposure because there is no limit on that 20% coinsurance we mentioned earlier. If you face a serious illness, that 20% could quickly add up to thousands of dollars in medical bills. We want to ensure you have medicare explained simply for beginners so you can avoid these unexpected costs. To truly protect your savings, you’ll need to look at how to fill these gaps with drug coverage and supplemental insurance.

It’s also important to remember that Original Medicare doesn’t include routine dental insurance, vision exams, or hearing aids. Most people find that adding these extra layers of protection is the only way to achieve total peace of mind. You can learn more about how to enroll in Medicare and manage these additions through the Social Security Administration, which handles the administrative side of your journey.

Medicare Part D: Your Prescription Drug Plan

Even if you don’t take any medications right now, we strongly recommend enrolling in Medicare Part D as soon as you’re eligible. If you wait, you could face a lifelong late-enrollment penalty. In 2026, the Part D landscape is much friendlier for your wallet. The maximum annual deductible is $615, and the most you’ll pay out-of-pocket for covered prescriptions for the entire year is capped at $2,100. This cap is a major safeguard that didn’t exist just a few years ago.

When you’re choosing a plan, don’t just look at the monthly premium, which averages around $34.50 in 2026. You should also check if your specific pharmacy is considered “preferred” by the plan. Using a preferred pharmacy can significantly lower your co-pays. We can help you run a personalized drug list to see which plan covers your specific medications at the lowest total cost.

Medigap (Supplement) Plans Explained

If you chose “Path 1” in the previous section, you’ll be looking at Medigap plans. These are standardized plans labeled by letters, like Plan G or Plan N. They’re designed specifically to “bridge the gap” by paying that 20% coinsurance that Original Medicare leaves behind. Plan G is particularly popular because it covers almost everything except for the small Part B annual deductible. This creates a very high level of financial predictability for your monthly budget.

The most critical thing for beginners to know is the “Guaranteed Issue” window. This is a six-month period that starts the month you are both 65 and enrolled in Part B. During this time, insurance companies must sell you a Medigap policy at the best available rate, regardless of your health history. If you miss this window, you may have to answer medical questions and could be denied coverage or charged much more. We’re here to help you time this perfectly so you never lose your right to secure, affordable coverage.

Timing is Everything: When and How to Enroll

Missing a Medicare deadline is one of the most common fears we hear about, and for good reason. The rules are strict, and the consequences for being late can stay with you for the rest of your life. We believe that having medicare explained simply for beginners means focusing heavily on these dates so you can move forward without a heavy cloud of worry hanging over your head. The government gives you a specific window to join, and knowing exactly when your personal clock starts ticking is the first step toward peace of mind.

If you miss your initial window to sign up for Part B, you’ll face a lifelong late enrollment penalty. This isn’t a one-time fine. It’s a 10% increase in your monthly premium for every 12-month period you were eligible but didn’t enroll. In 2026, with the standard Part B premium at $202.90, those extra costs can add up quickly over a decade or two of retirement. We don’t want you to pay a penny more than necessary for your care.

The 7-Month Initial Enrollment Window

Your journey typically begins with the Initial Enrollment Period. This is a seven-month window that centers exactly on your 65th birthday. It includes the three months before your birth month, the month you turn 65, and the three months immediately following. If you’re already receiving Social Security benefits, the government will usually enroll you in Parts A and B automatically. You’ll simply receive your red, white, and blue card in the mail about three months before you turn 65.

If you aren’t yet taking Social Security, you must take action yourself. You can apply easily through the Social Security Administration website. We recommend starting this process during those first three months before your birthday. This ensures your coverage begins on the first day of your birth month, leaving no gaps in your protection. If you’re feeling unsure about your specific dates, you can contact us to confirm your enrollment timeline and avoid any costly mistakes.

Working Past 65: Should You Delay Part B?

Many people today continue working well past 65, which adds a layer of complexity to the process. You might be able to delay Part B without penalty if you have “creditable” coverage through a current employer. However, we see many people fall into a “Late Enrollment Trap” because they assume any work insurance is enough. If your company has fewer than 20 employees, Medicare is actually the primary payer. In this case, you must enroll in Part B at 65 or you’ll be left with massive unpaid medical bills and a permanent penalty.

If you do have qualifying large-employer coverage, you’ll eventually use a Special Enrollment Period (SEP) to join when you retire. You have an eight-month window to sign up for Part B after your employment or health coverage ends. We always suggest comparing your employer plan’s premiums and deductibles against the 2026 Medicare rates. Often, we find that switching to Medicare provides better coverage for less money than a corporate plan. Getting medicare explained simply for beginners is about making sure you never lose your right to choose the best path for your health and your wallet.

Simplifying Your Choice: Why an Independent Broker is Your Best Ally

By now, you have a solid foundation of how the system works. However, knowing the rules is only half the battle. The real challenge is looking at hundreds of available plans in 2026 and deciding which one actually fits your life. This is where we step in as your guide. Finding medicare explained simply for beginners is a great start, but applying those facts to your specific health needs requires a personal touch. We believe you shouldn’t have to face these complex decisions alone.

There is a major difference between a “captive agent” and an independent Medicare broker. A captive agent works for one specific insurance company. Their job is to sell you that company’s products, whether they are the best fit for you or not. As independent brokers, we work for you. We represent over 40 different carriers, which gives us the freedom to compare every option in your area without any bias. Our goal is to protect your interests, not a corporate bottom line.

One of the best parts of this partnership is the “Zero Cost” advantage. Our services do not cost you a penny. We are compensated by the insurance companies, and your premiums remain exactly the same whether you use our expert guidance or try to sign up on your own. You get a dedicated advocate and year-round support at no extra charge. We don’t just help you sign up and disappear; we stay by your side every year to ensure your plan still meets your needs as costs and coverage change.

Unbiased Guidance vs. High-Pressure Sales

We prioritize your peace of mind over a sales quota. Instead of pushing a specific plan, we start by listening. We analyze your current medications and your list of preferred doctors to see which plans actually cover them at the lowest cost. This removes the guesswork and the anxiety of wondering if you made a mistake. Having a professional advocate means you have someone to call if a claim is denied or if you receive a confusing bill. We are here to remove the stress from the system so you can focus on enjoying your retirement.

Your Next Steps to Certainty

Moving from confusion to certainty is a simple process. First, we recommend gathering a list of your current prescriptions and the names of the doctors you want to keep. Once you have that, you can schedule a simple, no-obligation review with us. We will walk through your options side-by-side, answering every question until you feel completely confident. We even handle the paperwork for you. Our mission is to ensure that medicare explained simply for beginners results in a plan that gives you total security for the years ahead. Let us take the weight off your shoulders today.

Your Path to Medicare Peace of Mind

You’ve already done the hard work of learning how the system functions in 2026. By understanding the foundation of Parts A and B and recognizing the importance of your initial enrollment window, you’re ahead of the curve. We hope this guide has provided medicare explained simply for beginners so you can move from a state of distress to one of absolute certainty. You now have the mental map needed to choose between the flexibility of a Supplement plan or the convenience of an Advantage plan.

We’re here to help you cross the finish line with total confidence. Our team provides independent, unbiased advice tailored specifically to your health needs and your budget. We have access to over 40 top-rated insurance carriers and are licensed in more than 34 states to serve you better. Let us help you find the right Medicare plan; schedule your free consultation today.

You deserve to feel secure and empowered as you enter this new chapter. We’re ready to act as your dedicated advocate every step of the way. Your future is bright, and we’re honored to help you protect it.

Frequently Asked Questions

Is Medicare free when I turn 65?

Medicare is not entirely free for most people. While you likely won’t pay a premium for Part A if you’ve worked for 10 years, the standard Part B premium is $202.90 per month in 2026. You are also responsible for deductibles, like the $1,736 hospital deductible, and the 20% coinsurance for doctor visits. We help you look at the total cost of each plan so there are no surprises.

Do I have to sign up for Medicare if I am still working?

Your need to sign up depends on the size of your company. If your employer has 20 or more employees, you can usually delay Part B without facing a penalty later. However, if your company has fewer than 20 employees, you must enroll at 65 to avoid coverage gaps. We always suggest comparing your work plan’s costs against Medicare to see which option saves you more money.

What is the difference between Medicare and Medicaid?

Medicare is an insurance program primarily for seniors aged 65 and older, regardless of their income level. Medicaid is a joint federal and state program designed to help people with very limited income and resources pay for medical costs. Some people qualify for both programs. If you are “dual eligible,” we can help you find specific plans that coordinate these two types of coverage for maximum protection.

Can I change my Medicare plan later if I don’t like it?

Yes, you have specific opportunities each year to adjust your coverage. The most common window is the Open Enrollment Period, which runs from October 15 to December 7. During this time, you can switch between Advantage plans or move back to Original Medicare for the following year. If you have an Advantage plan, you also get an extra window from January 1 to March 31 to make one change.

Does Medicare cover dental, vision, or hearing?

Original Medicare generally does not cover routine dental exams, glasses, or hearing aids. This is a common point of confusion for many. To get this coverage, you can choose a Medicare Advantage plan that includes these extra benefits as part of the package. Alternatively, we can help you set up a separate dental insurance plan to ensure your teeth and eyes are protected alongside your medical health.

What happens if I miss my Medicare enrollment deadline?

Missing your deadline usually results in lifelong late enrollment penalties. For every year you wait to sign up for Part B, your monthly premium increases by 10%. You might also be restricted to signing up during the General Enrollment Period, which could leave you without any health coverage for several months. We work with you to track these dates so you can avoid these permanent and costly mistakes.

Is there a Medicare plan that covers everything?

No single plan covers every single penny, but you can get very close to full coverage. Many people choose to pair Original Medicare with a Medigap Plan G. This combination covers all your hospital and medical costs except for the $283 Part B annual deductible. This is the most comprehensive way to get medicare explained simply for beginners who want to avoid unexpected medical bills throughout the year.

How much does a Medicare broker cost?

Our services as an independent broker are completely free to you. We are compensated by the insurance companies, so you never pay us a fee for our expert guidance or advocacy. Your premiums will be exactly the same whether you use our help or try to enroll on your own. We provide medicare explained simply for beginners to ensure you find the best fit without any added financial stress.