Last Tuesday, a client named Margaret sat at her kitchen table surrounded by fifteen different insurance flyers, all claiming to have the best plan for 2026. She felt paralyzed by the fear that choosing the wrong one would mean losing the specialist she has seen for ten years. If your mailbox looks like Margaret’s, you aren’t alone. Having medicare open enrollment explained in plain English is the only way to escape that feeling of being buried under a mountain of jargon. We know it’s frustrating when every letter you open mentions a different 2026 premium change or benefit update.

At The Modern Medicare Agency, we believe you deserve to feel steady and secure during this important window, which runs from October 15 to December 7, 2025. Our goal is to move you from a state of confusion to total confidence by simplifying the complex rules. We promise to show you exactly how to protect your current doctor relationships and lower your out-of-pocket costs without any sales pressure. This guide provides a clear timeline of the 2026 deadlines, a breakdown of what you can change right now, and a simple checklist to ensure you don’t miss a single beat.

Key Takeaways

- Mark your calendar for the 2026 window between October 15 and December 7 to ensure you have plenty of time to review your options without feeling rushed.

- We have medicare open enrollment explained in simple steps, showing you how to easily move between Original Medicare and Advantage plans for the upcoming year.

- Learn to spot common pitfalls like the “set it and forget it” trap and discover how to tune out high-pressure advertisements that cause unnecessary stress.

- See how we compare over 40 different carriers to find your perfect 2026 match, giving you the unbiased guidance you need to feel completely secure in your choice.

What is Medicare Open Enrollment? The Basics for 2026

Medicare can feel like a maze of confusing dates and complex choices. We see people every day who feel overwhelmed by the stacks of mail and constant phone calls from insurance companies. Our goal is to help you move from confusion to confidence. To get started, medicare open enrollment explained simply is this: it’s your annual window to review and change your health and drug coverage to ensure it matches your needs for the coming year.

This period, also known as the Annual Election Period (AEP), is the one time each year when most people already enrolled in Medicare can switch plans. Whether you want to move from Original Medicare to a private plan or just find a better way to cover your prescriptions, this is your chance. Understanding What is an Open Enrollment Period? is the first step toward taking control of your healthcare costs for 2026. It’s not about being sold a policy; it’s about making sure you aren’t overpaying for benefits you don’t use.

The Purpose of the Annual Enrollment Window

Why does the government allow this yearly reset? It’s because the insurance market doesn’t stand still. Every year, insurance companies adjust their premiums, change their doctor networks, and update their lists of covered medications. A plan that was perfect for you in 2025 might have much higher out-of-pocket costs in 2026. This window exists so you don’t get stuck in a plan that no longer serves your health or your budget.

For 2026, a review is more essential than ever. We’ve seen significant shifts in how drug costs are structured, including the ongoing impact of the $2,000 out-of-pocket cap on prescriptions. Even if you’re happy with your current coverage, you should check your “Annual Notice of Change” (ANOC) letter. We can help you compare these updates against other available Medicare Part D options to see if a different plan would save you money. We simplify the jargon so you know exactly how your benefits will look on January 1st.

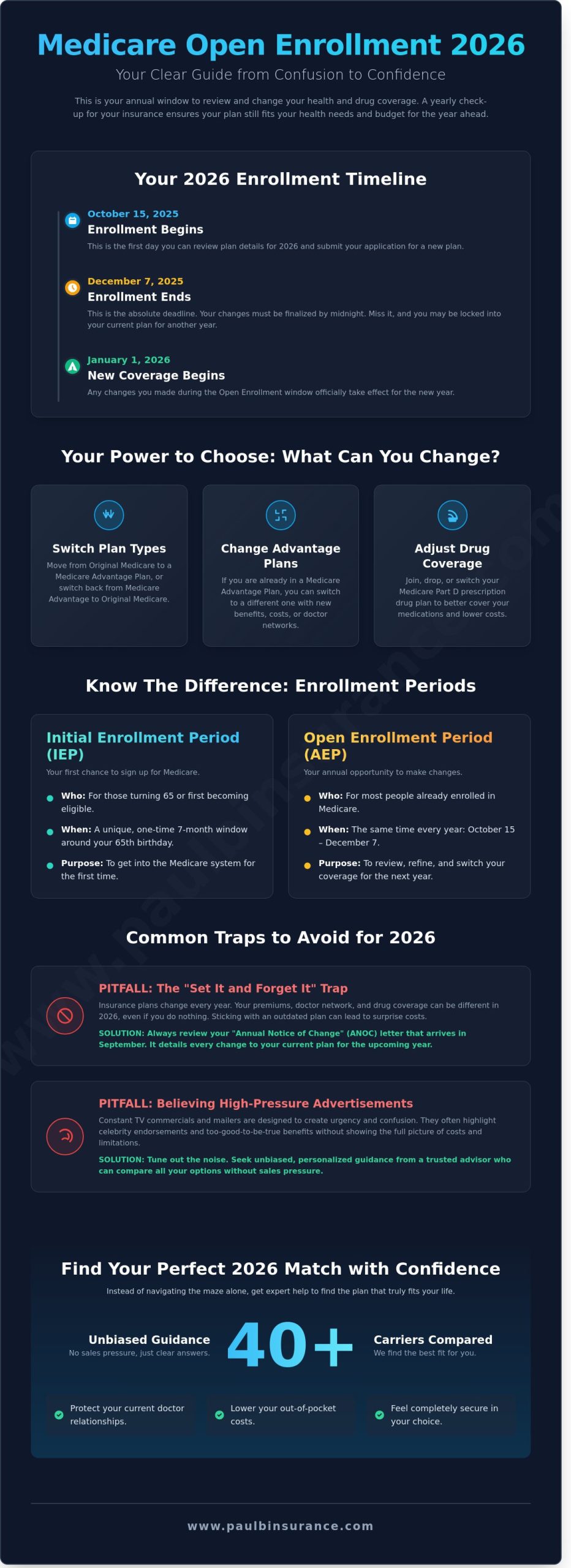

OEP vs. Initial Enrollment: Knowing the Difference

It’s easy to get these terms mixed up, but they serve very different purposes. Your Initial Enrollment Period is a one-time window unique to you. It usually happens around your 65th birthday, starting three months before you turn 65 and ending three months after. That’s when you first sign up for Medicare. If you’re looking for a clear guide for those just starting out, we have resources specifically for first-timers.

The Medicare Open Enrollment Period is different because it happens at the same time for everyone, regardless of when they turned 65. It runs from October 15 through December 7. While Initial Enrollment is about getting into the system, OEP is about refining your choices. Think of it as an annual check-up for your insurance. We act as your advocate during this time, offering unbiased guidance to ensure you stay protected without the stress of doing it alone.

Key Dates: Your 2026 Medicare Open Enrollment Timeline

We know the calendar can feel like an enemy when you’re trying to make sense of your health coverage. The dates seem to rush at you, and the pressure to choose the right plan can feel heavy. Having the medicare open enrollment explained in a simple, step-by-step way is the best way to move from confusion to confidence. We’ve mapped out the essential dates for your 2026 coverage so you don’t have to worry about missing a thing.

- October 15, 2025: This is the official start date. It’s the first day you can submit your 2026 plan changes. We recommend having your choices ready before this date so you can click “submit” with peace of mind.

- December 7, 2025: This is the hard deadline. Once the clock strikes midnight, the window for the Annual Enrollment Period closes. You must have your enrollment finalized by this date.

- January 1, 2026: This is the day your new coverage and benefits officially begin. Any changes you made during the fall will take effect as soon as the ball drops on New Year’s Day.

If you miss the December 7 deadline, you’re likely stuck with your current coverage for the rest of 2026. This can be a scary thought if your favorite doctor left the network or your prescription costs jumped up. Unless you qualify for a Special Enrollment Period due to moving or losing other coverage, you won’t be able to make changes until the following year. Following the Official Medicare Enrollment Rules ensures you stay protected and avoid these costly gaps in care.

The Pre-Enrollment Period: September and October

Your preparation actually starts before the official window opens. In late September, keep a close eye on your mailbox for the Annual Notice of Change (ANOC). We recommend starting your plan comparison in early October so you aren’t rushed. The Annual Notice of Change (ANOC) is your cheat sheet for 2026 plan updates.

The Medicare Advantage Open Enrollment Window

There’s a separate window that runs from January 1 to March 31 every year. This specific period is only for those who are already enrolled in a Medicare Advantage plan. We often call this a “safety valve” because it allows you to make one more change if you realize your new 2026 plan isn’t the right fit. If you’re feeling unsure about your current choice, you can look through our Medicare Advantage guide to see if a different path might serve you better. We’re here to make sure you never feel trapped in a plan that doesn’t work for you.

What Changes Can You Make During Open Enrollment?

We know that looking at a stack of insurance papers feels like staring at a puzzle with missing pieces. This period is your chance to put those pieces together so you can breathe easier. Having medicare open enrollment explained in simple terms helps you take control of your health care for the coming year. During this window, you have the freedom to make several specific moves to protect your health and your savings. We are here to guide you through each one of them.

You can use this time to perform the following actions:

- Switch from Original Medicare (Part A and Part B) to a Medicare Advantage plan.

- Move from one Medicare Advantage plan to another to take advantage of better 2026 benefits.

- Join, drop, or switch a Medicare Part D prescription drug plan to lower your pharmacy costs.

- Return to Original Medicare from a Medicare Advantage plan if you prefer more flexibility.

The official Medicare Open Enrollment information confirms these choices are available to most beneficiaries. Our goal is to make sure you feel confident in whatever choice you make.

Updating Your Medicare Advantage Coverage

In 2026, many plans have updated their provider networks and added new extra benefits. Your current plan might have been perfect last year, but it may no longer be the best option if your primary doctor or specialist left the network. We suggest checking our Medicare Advantage guide to see how these plans have evolved. Don’t feel stuck in a plan that doesn’t serve you anymore. We can help you compare the latest 2026 benefit packages to find a fit that feels right.

Managing Your Part D Prescription Drug Plan

Drug costs are a major concern for almost everyone we talk to. Formularies change every January. This means a drug that was covered at a low cost in 2025 might move to a more expensive tier in 2026. A massive change for 2026 is the full implementation of the $2,000 out of pocket cap on prescription drugs. This effectively replaces the old “donut hole” structure with a simpler, more protective limit. You can read our guide to Medicare Part D to understand these new 2026 rules. We want to ensure you don’t pay a penny more than necessary at the pharmacy counter.

The Role of Medicare Supplement (Medigap) Plans

It’s a common mistake to think you can jump into a Medigap plan without any questions asked during this time. Medicare Supplement plans have different rules than Advantage plans. In most states, switching to Medigap insurance usually requires medical underwriting. This means a company can look at your health history before accepting your application. If you drop your Medigap plan during the medicare open enrollment explained period without a solid backup, you might find it hard to get that coverage back. We are here to help you avoid these risky moves and keep your coverage secure.

Common Pitfalls and How to Prepare for 2026

Many seniors fall into the “Set It and Forget It” trap every autumn. Even if you loved your coverage in 2025, your plan is almost certainly different for the new year. Insurance companies adjust their terms every January 1st; they don’t stay static. You might find that while your monthly premium stayed the same, your deductible for a specific tier of medication jumped by $50 or more. When you have medicare open enrollment explained by a dedicated advocate, you can spot these hidden traps early and protect your retirement savings.

Don’t let the high-pressure TV commercials or generic mailers dictate your health care. Those loud advertisements often promise “free” benefits that might not even be available in your specific county or with your trusted doctors. We focus on your unique situation, not a generic script from a corporate call center. We want to ensure your specific medications are still covered in the 2026 formulary and that your preferred hospitals remain in-network. If they aren’t, we’ll find a plan that keeps them there.

Reading Your 2026 Annual Notice of Change (ANOC)

This document usually arrives in your mailbox by late September. “The ANOC is the most important piece of mail you will receive this year, yet most people throw it away.” We help our clients decode this document for free so they aren’t hit with a surprise bill in January. There are three critical things we look for in your ANOC:

- Premium changes: Even a small monthly increase adds up over twelve months.

- Copay updates: Check if your cost for a specialist visit or physical therapy has gone up.

- Drug list shifts: Insurance companies move medications between “tiers” frequently, which can drastically change your out-of-pocket costs.

If your regular prescription moved from a Tier 2 to a Tier 4, your costs could triple overnight. You can check your current coverage against new options on our Medicare Part D page.

Evaluating Your Health Needs for the Coming Year

Has your health changed in the last 12 months? Maybe you’ve received a new diagnosis or your doctor mentioned a possible surgery for later in 2026. We look at your total out-of-pocket maximum rather than just focusing on the lowest premium. A plan with a $0 premium might actually be the most expensive choice if you have frequent specialist visits or upcoming procedures. We simplify the jargon so you know exactly how it works. You can learn more about how we compare these options in our Medicare Advantage guide.

Navigating the 2026 Maze with a Trusted Broker

We know how heavy the weight of these choices feels. By 2026, the Medicare system has grown even more complex, and you shouldn’t have to carry that burden alone. When you work with an independent broker, you get an advocate who sits on your side of the table. A captive agent works for a single insurance company. That means their loyalty is to their employer, not to you. We’re different. We compare plans from over 40 different carriers to find the one that fits your life, not the other way around. We want to make sure you have the right fit for your specific health needs without any bias toward a single brand.

This service doesn’t cost you a single penny. We get paid by the insurance companies, so our professional guidance is provided at no cost to you. Our goal is simple. We want to take you from a state of confusion to a place of total confidence. Having medicare open enrollment explained by a pro ensures you don’t miss out on better benefits or lower premiums available this year. You deserve to have someone in your corner who isn’t rushed or pressured by sales quotas. We focus on your peace of mind above all else, ensuring you understand every detail of your coverage.

Why a Local Advisor Makes a Difference

Whether you live in New York, Florida, or California, we understand the local networks that matter to you. Medicare isn’t just a national program; it’s a local one. A doctor available in Los Angeles might not be in a network in Miami. We stay with you every month of the year, not just during the busy enrollment season. If you get a confusing bill in July or a coverage notice in October, we’re here to help you solve it. You can find more details in our Medicare guide to help you understand how these local options impact your wallet.

Ready for a Stress-Free 2026? Let Us Help

We’ve developed a simple 5-step process to audit your current coverage and ensure it still serves you well. This audit is essential because plan details change every single year. Our process includes:

- Current Plan Review: We look at what you have now and what it will cost in 2026.

- Doctor Verification: We confirm your specialists are still in-network for the coming year.

- Prescription Check: We run your 2026 drug list through every available plan to find the lowest total cost.

- Benefit Comparison: We look for extra perks like dental insurance or vision coverage.

- Seamless Enrollment: We handle the paperwork so you don’t have to worry about mistakes.

To get started, please gather your current list of medications and the names of your primary doctors. We want to make sure your 2026 coverage is seamless and stress-free. Having medicare open enrollment explained clearly is the first step toward a worry-free year. If you’re ready to secure your health future, you can reach out to us today to start your personalized coverage audit.

Take Control of Your 2026 Healthcare Future

Navigating the 2026 season doesn’t have to be a source of stress. Now that you’ve had medicare open enrollment explained, you know that the window between October 15 and December 7 is your best chance to secure the right coverage. We’ve seen many people fall into common traps by sticking with plans that no longer serve them, but we’re here to protect you from those mistakes. Our team provides unbiased guidance from 40+ carriers to ensure you get the best fit for your specific needs.

We’re currently licensed in 34+ states and use a proven 5-step process to move you from confusion to confidence. You won’t find any high-pressure sales tactics here; we’re dedicated advocates who want to see you empowered. It’s about more than just insurance; it’s about your peace of mind and financial security. Let us handle the complex details so you can focus on what matters most in 2026. We simplify the jargon so you know exactly how your plan works before you ever sign.

Schedule a Call With Paul for a Free 2026 Coverage Audit and let’s make this your simplest enrollment yet. We’re ready to walk beside you every step of the way.

Frequently Asked Questions

Is Medicare Open Enrollment the same as the Marketplace Open Enrollment?

No, these are two completely separate events with different dates and rules. Medicare Open Enrollment runs from October 15 to December 7, 2026, and is specifically for people already enrolled in Medicare. The Health Insurance Marketplace is for individuals under age 65 who don’t have government coverage. We’ve seen many seniors get confused by the overlapping dates, but keeping them separate ensures you don’t miss your chance to update your 2026 benefits.

Can I change my Medicare Supplement (Medigap) plan during Open Enrollment?

You can apply for a new Medigap plan at any time, but doing so during the fall enrollment period doesn’t guarantee acceptance. Unlike Medicare Advantage, most states allow Medigap insurers to ask health questions and deny coverage based on pre-existing conditions. Having medicare open enrollment explained by a professional helps you understand if you’ll need to pass a health screening before making a switch for the 2026 calendar year.

What happens if I am happy with my current plan and do nothing?

Your current coverage will typically renew automatically for January 1, 2027, if you take no action. However, we strongly advise against this approach because plans change their costs and benefits every year. In 2026, 90 percent of plans have adjusted their drug lists or co-pays. Reviewing your Annual Notice of Change ensures you aren’t surprised by a sudden price hike or a dropped medication when the new year starts.

How many times can I change my plan during the Open Enrollment period?

You can submit a new choice as many times as you want between October 15 and December 7. Medicare only honors the very last application they receive before the midnight deadline on the final day. We help you compare options thoroughly so you don’t feel rushed. This flexibility allows us to make sure you have the exact coverage you need for 2026 without any lingering doubts or stress.

Will I be penalized if I switch from Medicare Advantage back to Original Medicare?

There’s no federal financial penalty for returning to Original Medicare, but you might face challenges getting a Supplement plan. If you’ve been on an Advantage plan for more than 12 months, insurers in 46 states can charge more or deny you a Medigap policy. We guide you through these rules to protect you from losing the comprehensive coverage you expect. Having medicare open enrollment explained clearly means you won’t make a move that leaves you vulnerable.

Does Open Enrollment apply to me if I just started Medicare last month?

Yes, this period applies to you even if your coverage began as recently as September or October 2026. You can use this time to change your Medicare Advantage or Part D prescription plan for the upcoming year. It’s an excellent opportunity to fix any initial choices that don’t feel right. We’ll look at your current doctors and prescriptions to see if a different 2026 plan offers better value or more peace of mind.

How do I know if my medications are still covered for 2026?

You should check the 2026 formulary, which is the official list of covered drugs for your specific plan. Plans often move medications to different tiers, which changes your out-of-pocket cost. Since the $2,000 cap on prescription costs is now standard practice, many companies have updated their coverage rules. We can run a personalized search for you to confirm every single one of your medications is still on the list for next year.

Can a Medicare broker charge me for their help during Open Enrollment?

No, we never charge you a fee for our services or guidance. Our help is completely free to you because we’re compensated by the insurance companies. This allows us to act as your personal advocate without adding any financial burden to your retirement. You get expert, unbiased advice and a simplified process at no cost. We’re here to help you move from confusion to confidence throughout the entire 2026 enrollment season.