Medicare is the primary federal health insurance program for disabled individuals under 65 who qualify through specific eligibility pathways. Three routes exist: Social Security Disability Insurance (SSDI), Amyotrophic Lateral Sclerosis (ALS), and End-Stage Renal Disease (ESRD). Each path carries different enrollment rules, waiting periods, and coverage choices. Disabled under 65 Medicare options include Original Medicare, Medicare Advantage, and Medicare Supplement plans, though younger beneficiaries face unique challenges that older enrollees do not. Understanding these distinctions before your coverage starts prevents costly gaps and missed opportunities.

What are the eligibility criteria for Medicare if disabled under 65?

Medicare eligibility for disabled individuals under 65 follows three distinct pathways, each with its own timeline and enrollment process.

The SSDI pathway is the most common route. Individuals under 65 become eligible for Medicare after receiving SSDI benefits for 24 months, with coverage starting in the 25th month. Enrollment in Part A and Part B is automatic, and Medicare sends the card to the address on file. You do not need to apply separately.

One critical detail trips up many people. The 24-month SSDI wait starts from the cash benefit entitlement date, not the application date or the date Social Security determined your disability. Misunderstanding this distinction causes people to expect coverage earlier than it actually arrives, which creates real financial risk.

The ALS pathway works differently. Medicare entitlement begins the first month an individual becomes entitled to SSDI cash benefits for ALS, with no waiting period at all. This immediate start reflects the severity and rapid progression of the disease.

The ESRD pathway requires active enrollment. Individuals with ESRD must apply for Medicare directly; coverage does not start automatically. ESRD Medicare generally begins after the third month of dialysis, though starting home dialysis training earlier can move that date forward.

| Eligibility pathway | Waiting period | Enrollment type | Coverage start |

|---|---|---|---|

| SSDI | 24 months from benefit entitlement date | Automatic | 25th month of SSDI benefits |

| ALS | None | Automatic | First month of SSDI entitlement |

| ESRD | 3 months of dialysis (standard) | Active application required | After 3rd dialysis month or earlier with training |

Pro Tip: If you receive SSDI, check your award letter for the “date of entitlement,” not the “date of approval.” Your Medicare clock starts on the entitlement date. These two dates are often months apart.

What Medicare coverage options are available for disabled individuals under 65?

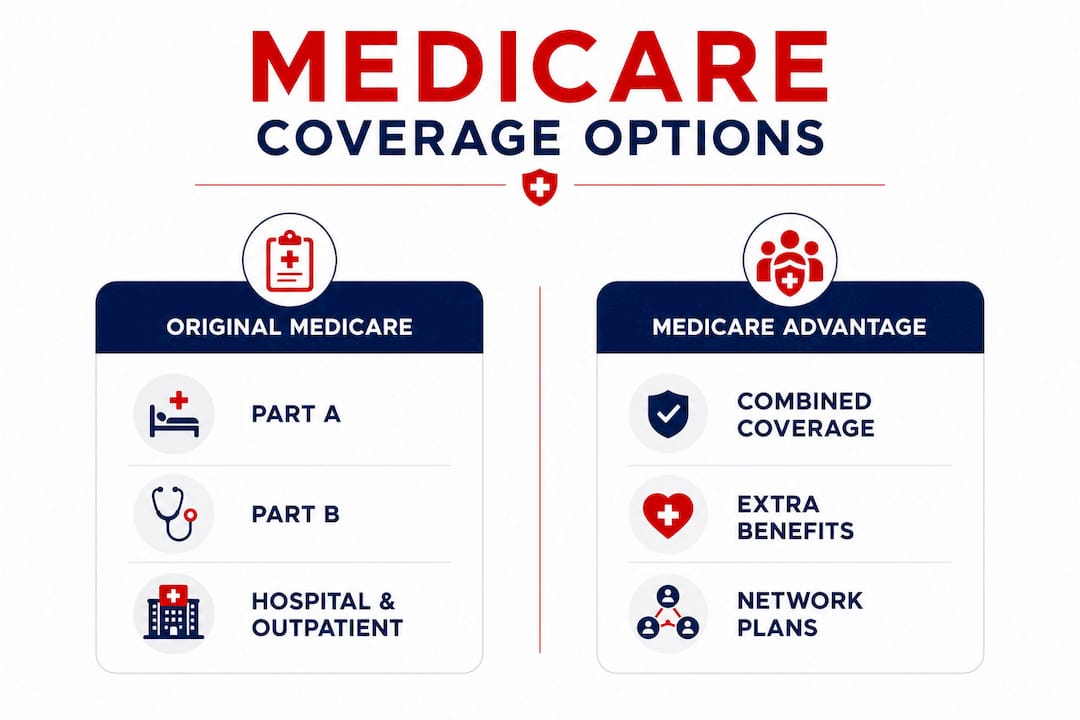

Once eligible, you have three main coverage structures to consider. Each carries real trade-offs for younger beneficiaries.

Original Medicare (Parts A and B)

Original Medicare covers hospital care under Part A and outpatient services under Part B. It gives you access to any provider who accepts Medicare, which matters when you need specialists for a complex condition. The downside is that Original Medicare has no out-of-pocket maximum, meaning costs can accumulate significantly without supplemental coverage.

Medicare Advantage plans

Medicare Advantage plans are available to under-65 disabled individuals and cover the same services as Original Medicare, often with added benefits like vision and dental. Insurers cannot deny you enrollment based on health status during your Initial Enrollment Period. This protection is significant because younger disabled people often have complex medical histories that would otherwise make private insurance difficult to obtain. You can learn more about how these plans work at Paulbinsurance’s Medicare Advantage guide.

Medicare Supplement (Medigap) plans

Medigap is where younger beneficiaries face the steepest challenge. Federal law does not guarantee Medigap plan issuance or protections to under-65 disabled beneficiaries. Some states require insurers to offer Medigap to disabled people under 65; others do not, leaving insurers free to apply medical underwriting or charge higher premiums. This is a major gap in federal coverage protections for younger enrollees. Checking your state’s rules through a resource like MySafeMap’s beneficiary access tool can clarify what protections apply where you live.

Pros and cons of each coverage option:

- Original Medicare: Wide provider access, no network restrictions. No out-of-pocket maximum, no drug coverage without adding Part D.

- Medicare Advantage: Bundled coverage including drugs in many plans, added benefits, out-of-pocket maximum protection. Network restrictions may limit specialist access.

- Medigap: Fills cost gaps in Original Medicare, predictable expenses. Federal protections do not apply under 65; availability and pricing vary by state.

Pro Tip: If your state does not guarantee Medigap access under 65, enroll in a Medigap plan immediately when you turn 65. That birthday triggers a federal Open Enrollment Period where no insurer can deny you or charge more based on health.

How do you manage Medicare enrollment and coordinate it with other insurance?

Managing enrollment timing is one of the most consequential decisions a disabled person under 65 will make. Getting it wrong costs money and creates coverage gaps.

Your Initial Enrollment Period (IEP) for Medicare begins when you first become eligible. For SSDI recipients, this window opens before your coverage actually starts, giving you time to choose a Medicare Advantage plan or decide to stick with Original Medicare. Missing this window without qualifying coverage in place triggers penalties.

Delaying Part B enrollment without proper coverage in place results in premium surcharges and coverage gaps that follow you for years. The penalty adds 10% to your Part B premium for every 12-month period you were eligible but not enrolled. That surcharge does not go away.

Coordination with employer or private insurance requires careful attention. Here are the steps to follow when Medicare eligibility starts:

- Confirm your Medicare entitlement date. Check your SSDI award letter for the exact entitlement date so you know when your 24-month clock started.

- Notify your employer’s HR department. If you have group health coverage through an employer, determine whether Medicare becomes primary or secondary. Group size matters: employers with fewer than 100 employees typically make Medicare primary.

- Evaluate your COBRA timeline. COBRA coverage can run alongside Medicare, but it does not substitute for Part B enrollment. Relying on COBRA alone while skipping Part B is a common and expensive mistake.

- Choose your plan type before coverage starts. Decide between Original Medicare and Medicare Advantage during your IEP to avoid a gap in supplemental coverage.

- Enroll in Part D if you choose Original Medicare. Skipping drug coverage when first eligible also triggers late enrollment penalties.

Pro Tip: Coordination between Medicare and private insurance is often overlooked. Work with an independent Medicare specialist before your coverage starts, not after. Fixing enrollment mistakes retroactively is far harder than planning ahead.

For a detailed look at avoiding enrollment errors, Paulbinsurance covers common Medicare enrollment mistakes that trip up younger beneficiaries.

What financial assistance exists for disabled Medicare beneficiaries under 65?

Cost is a real barrier for many disabled people under 65, particularly those living on SSDI income. Several programs exist to reduce what you pay.

Medicare Savings Programs and the Low-Income Subsidy can reduce premium and medication costs for disabled Medicare beneficiaries with limited income. Many people receiving SSDI qualify. State Medicaid agencies run these programs, so eligibility rules vary by state.

Here is a breakdown of the main assistance programs:

- Medicare Savings Programs (MSPs): Four tiers exist, ranging from help paying Part B premiums only to full coverage of premiums, deductibles, and copays. Income and asset limits apply and vary by state.

- Extra Help (Low-Income Subsidy): Reduces Part D drug plan costs including premiums, deductibles, and copays. The Social Security Administration administers this program. Applying is free.

- State Medicaid: Many disabled individuals under 65 qualify for both Medicare and Medicaid, known as “dual eligibility.” Medicaid can cover costs Medicare does not, including long-term care services.

- State Health Insurance Assistance Programs (SHIPs): Free, unbiased counseling on Medicare options available in every state. SHIP counselors can help you identify which assistance programs you qualify for.

- State Medigap protections: Some states, including Connecticut, Maine, Massachusetts, and New York, require insurers to offer Medigap to under-65 disabled beneficiaries. Others offer partial protections. Your state insurance department is the definitive source.

Younger disabled beneficiaries often leave Extra Help money on the table simply because they do not know it exists. If your income is modest, applying for Extra Help through the Social Security Administration costs nothing and can save hundreds of dollars per year on prescriptions. You can also find beneficiary-specific guidance through MySafeMap’s beneficiary resources to identify what state-level help applies to your situation.

Key Takeaways

Disabled individuals under 65 qualify for Medicare through SSDI, ALS, or ESRD pathways, each with distinct enrollment rules, coverage options, and financial assistance programs that require proactive planning.

| Point | Details |

|---|---|

| SSDI eligibility timeline | Medicare starts in the 25th month after SSDI benefit entitlement, not the application date. |

| ALS and ESRD differ | ALS triggers immediate Medicare; ESRD requires active application after three months of dialysis. |

| Medigap access varies by state | Federal law does not protect under-65 beneficiaries; check your state’s rules before relying on Medigap. |

| Part B delays cost money | Skipping Part B without qualifying coverage adds a permanent 10% premium surcharge per year missed. |

| Financial help is available | Medicare Savings Programs and Extra Help reduce costs for SSDI recipients who qualify by income. |

What I have learned helping younger Medicare beneficiaries since 2007

The biggest mistake I see younger disabled people make is treating Medicare like it works the same way it does at 65. It does not. The rules are different, the protections are thinner, and the stakes are higher because you are likely managing a serious health condition while living on a fixed income.

The Medigap situation frustrates me most. People assume federal law protects them the way it does at 65. It does not. I have spoken with people in states that offer no Medigap protections under 65 who were blindsided by medical underwriting or premiums they could not afford. Researching your state’s rules before you become eligible is not optional. It is the difference between having a plan and having a problem.

Medicare Advantage is often the right answer for younger disabled beneficiaries, but not automatically. You need to check whether your specialists and treatment centers are in-network. A plan with great extra benefits means nothing if your neurologist or dialysis center is not covered. Compare networks carefully, not just premiums.

The financial assistance programs are genuinely underused. I have seen clients qualify for Extra Help and Medicare Savings Programs who had no idea these existed. If you are on SSDI, apply for both. The worst outcome is a denial letter. The best outcome is hundreds of dollars back in your pocket every month.

Start planning at least three months before your Medicare eligibility date. That window gives you time to compare plans, confirm coordination with any existing insurance, and avoid the penalties that come from missing enrollment deadlines.

— Paul

Medicare plan options for disabled individuals under 65

Choosing the right Medicare plan when you are under 65 with a disability requires more than a quick comparison. The plan that fits your health needs, budget, and provider relationships makes a real difference in your day-to-day care.

At Paulbinsurance, our independent agents specialize in helping younger Medicare beneficiaries sort through their options without pressure or confusion. Whether you are weighing Medicare Advantage versus Supplement plans or trying to understand how your SSDI timeline affects your enrollment window, we walk you through it step by step. Paul Barrett has been working with Medicare consumers since 2007, and our team brings that same depth of experience to every conversation. Reach out to Paulbinsurance to get clear, personalized guidance on the coverage that fits your life.

FAQ

Who qualifies for Medicare before age 65?

Individuals under 65 qualify for Medicare through three pathways: receiving SSDI benefits for 24 months, being diagnosed with ALS, or having End-Stage Renal Disease. Each pathway has different enrollment rules and timelines.

How long do you wait for Medicare after SSDI approval?

Medicare coverage starts in the 25th month after your SSDI benefit entitlement date, not your application or approval date. Counting from the wrong date is a common mistake that leads to unexpected coverage gaps.

Can disabled people under 65 get a Medicare Supplement plan?

Federal law does not require insurers to sell Medigap plans to disabled individuals under 65. Some states mandate access; others allow medical underwriting or higher premiums. Check your state insurance department’s rules before assuming Medigap is available to you.

What is the best Medicare plan for a disabled person under 65?

Medicare Advantage is often the most practical choice for younger disabled beneficiaries because it includes an out-of-pocket maximum and often bundles drug coverage, and insurers cannot deny enrollment based on health status during the Initial Enrollment Period.

What financial help is available for Medicare costs under 65?

Medicare Savings Programs and the Extra Help Low-Income Subsidy can reduce premiums, deductibles, and drug costs for SSDI recipients who meet income limits. State Medicaid agencies run these programs, and applying through the Social Security Administration is free.