Medicare Part B is defined as the outpatient medical insurance component of Original Medicare, covering physician visits, preventive screenings, and medically necessary services outside of a hospital stay. If you are turning 65 or retiring soon, understanding what is Medicare Part B means understanding the half of Medicare that covers most of your day-to-day medical care. Part A handles inpatient hospital stays. Part B covers outpatient services and physician care. The two work together, but they are billed separately and carry different costs. Getting clear on Part B before your enrollment window opens is the single best thing you can do to protect your budget and your coverage options.

What does Medicare Part B cover?

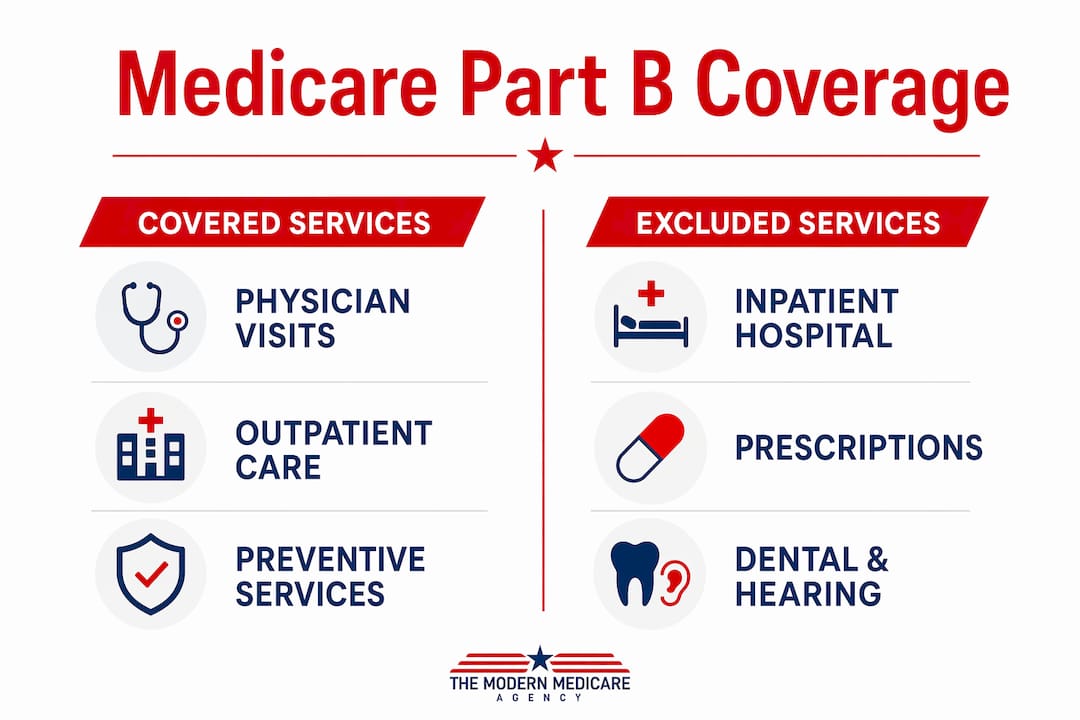

Medicare Part B coverage is broader than most people expect. Part B covers physician visits, outpatient hospital services, durable medical equipment, preventive screenings, and certain vaccines. That range makes it the workhorse of day-to-day Medicare coverage for most beneficiaries.

Medically necessary services

Medically necessary services are the core of Part B. These include:

- Doctor visits with your primary care physician or a specialist

- Outpatient hospital services such as X-rays, stitches, cast care, and lab work

- Emergency room visits when you are treated and released without being formally admitted

- Ambulance transportation when medically necessary

- Mental health services provided on an outpatient basis

- Durable medical equipment (DME) including wheelchairs, walkers, and CPAP machines

One detail that surprises many people: even during a hospital visit, some charges fall under Part B rather than Part A. If a physician bills for professional services separately from the facility, that charge goes to Part B. Billing distinctions between inpatient and outpatient care matter more than most people realize, and a single hospital encounter can generate charges under both parts.

Preventive care and vaccines

Part B covers a strong set of preventive services at no cost to you, provided your provider accepts Medicare assignment. Preventive screenings and vaccines covered include cancer screenings, cardiovascular disease screenings, annual wellness visits, flu shots, and COVID-19 vaccines. No deductible and no coinsurance apply to these services. That is a meaningful benefit. Catching a condition early through a covered screening costs you nothing out of pocket.

Pro Tip: Ask your provider before every appointment whether the visit is being billed as preventive or diagnostic. A routine wellness visit is free under Part B. If your doctor addresses a new symptom during the same visit, that portion may be billed as diagnostic and subject to cost-sharing.

What Part B does not cover

Part B does not cover inpatient hospital stays, prescription drugs you take at home, routine dental care, hearing aids, or routine vision exams. Those gaps are real and worth planning around. Preventive and diagnostic services carry different cost-sharing rules, which catches many new beneficiaries off guard.

How does Medicare Part B cost-sharing work in 2026?

Part B costs in 2026 include a monthly premium, an annual deductible, and ongoing coinsurance. Understanding all three is critical for budgeting your retirement healthcare expenses.

The 2026 premium and deductible

- Monthly premium: The standard Part B premium is $202.90 per month in 2026. Higher-income beneficiaries pay more under the Income-Related Monthly Adjustment Amount (IRMAA) surcharge.

- Annual deductible: The 2026 Part B deductible is $283. You pay all covered costs out of pocket until you meet this amount each year.

- Coinsurance: After the deductible, you pay 20% of the Medicare-approved amount for most covered services. Medicare pays the remaining 80%.

- No out-of-pocket cap: Original Medicare has no annual maximum on what you can owe in coinsurance. A serious illness with frequent outpatient care can generate thousands of dollars in 20% coinsurance charges.

- IRMAA surcharges: If your income exceeds certain thresholds, CMS adds a surcharge on top of the standard premium. These thresholds are based on your tax return from two years prior.

The absence of an out-of-pocket cap is the most underappreciated financial risk in Original Medicare. A single course of outpatient chemotherapy, for example, can result in coinsurance bills that dwarf the annual premium.

Pro Tip: A Medicare Supplement plan, also called Medigap, can cover all or most of that 20% coinsurance. Plans like Medigap Plan G pay the coinsurance after you meet the Part B deductible, giving you a predictable annual cost. Review Part B premium details before choosing a supplement plan.

Late enrollment penalties

Delaying Part B enrollment without qualifying coverage adds a permanent penalty to your monthly premium. The late enrollment penalty is 10% for every 12-month period you were eligible but did not enroll. That increase stays with you for as long as you have Medicare. A two-year delay means a 20% higher premium for life. That adds up fast over a 20-year retirement.

Rising premiums and deductibles in 2026 make this penalty even more costly for retirees who must budget carefully. Avoiding the penalty is straightforward if you enroll on time or qualify for a Special Enrollment Period.

When and how should you enroll in Medicare Part B?

Enrollment in Medicare Part B follows specific timing rules. Missing your window has permanent financial consequences.

- Initial Enrollment Period (IEP): Your IEP runs for 7 months. It starts 3 months before the month you turn 65, includes your birthday month, and ends 3 months after. Enrolling in the first 3 months of your IEP means coverage starts on the first day of your birthday month.

- Automatic enrollment: If you are already receiving Social Security benefits when you turn 65, you are automatically enrolled in Part B. You will receive your Medicare card in the mail. You must actively opt out if you do not want Part B.

- Active choice required: If you are not yet receiving Social Security, you must sign up for Part B yourself through the Social Security Administration.

- Special Enrollment Period (SEP): If you or your spouse is still working and covered by an employer group health plan, you can delay Part B without penalty. Your SEP begins when that employment or coverage ends and lasts 8 months.

- General Enrollment Period: If you miss your IEP and do not qualify for an SEP, you can enroll january through march each year. Coverage begins july 1. Late penalties apply.

Pro Tip: Check when your Part B coverage starts based on your specific enrollment month. The start date varies depending on when during your IEP you sign up.

Understand that Part B is voluntary by law, but refusing it without qualifying coverage triggers permanent penalties. Most people approaching 65 should enroll unless they have creditable employer coverage.

How does Medicare Part B differ from Part A and other Medicare parts?

| Medicare Part | What it covers | Typical cost |

|---|---|---|

| Part A | Inpatient hospital stays, skilled nursing facility care, hospice | Premium-free for most; deductible per benefit period |

| Part B | Outpatient physician services, preventive care, DME | $202.90/month premium; $283 deductible; 20% coinsurance |

| Part C (Medicare Advantage) | Combines Parts A and B with extra benefits through private insurers | Varies by plan; often includes dental, vision, drug coverage |

| Part D | Prescription drugs taken at home | Separate monthly premium; varies by plan |

Part A and Part B together form Original Medicare. Part A is premium-free for most people who worked at least 10 years and paid Medicare taxes. Part B always carries a monthly premium. The two parts are complementary but cover entirely different settings of care.

Part D covers prescription drugs you take at home. Part B does not cover those drugs. Part B does cover drugs administered in a clinical setting, such as chemotherapy infusions or injections given in a physician’s office. That distinction matters when you are comparing total drug costs.

Part B is functionally required to access Medigap supplemental insurance. Medigap plans assume you have Part B and are designed to cover its cost-sharing. Skipping Part B eliminates your ability to use most Medigap plans. Medicare Advantage plans also require enrollment in both Part A and Part B.

Pro Tip: Medicare Advantage (Part C) bundles Parts A and B through a private insurer and often adds dental, vision, and drug coverage. It can be a cost-effective alternative to Original Medicare plus a Medigap plan. Compare both paths before you commit.

Key Takeaways

Medicare Part B is the outpatient insurance half of Original Medicare, and its premiums, deductibles, and uncapped coinsurance make it the most financially complex part of Medicare to budget for.

| Point | Details |

|---|---|

| Core coverage | Part B covers physician visits, outpatient services, DME, and preventive care. |

| 2026 costs | The standard premium is $202.90/month with a $283 deductible and 20% coinsurance. |

| No out-of-pocket cap | Original Medicare has no annual coinsurance limit, creating significant financial exposure. |

| Enrollment timing | Enroll during your 7-month Initial Enrollment Period to avoid a permanent late penalty. |

| Supplement value | Medigap plans cover Part B coinsurance and require active Part B enrollment to work. |

What I have learned after nearly 20 years helping Medicare beneficiaries

Most people come to me thinking Part B is simple. They see the premium, nod, and move on. The premium is the easy part. The 20% coinsurance with no cap is where real financial risk lives.

I have worked with beneficiaries who delayed Part B because they wanted to avoid the monthly premium. A few years later, they faced a health event, needed to enroll, and discovered they owed a permanent 20% premium surcharge on top of the standard rate. That is a decision that costs money every single month for the rest of their lives. The math almost never favors delaying without qualifying employer coverage.

The other thing I see constantly is people underestimating what 20% of a large outpatient bill looks like. Twenty percent of a $50,000 outpatient procedure is $10,000. Original Medicare will not cap that. A Medigap plan will. That is why I tell every person I work with: do not just budget for the premium. Budget for the coinsurance exposure, and then decide whether a supplement plan makes sense for your situation.

Part B is also the gateway to everything else in Medicare. Without it, Medigap does not work. Medicare Advantage does not work. You are essentially locked out of the supplemental coverage market. Treating Part B as optional is a mistake most people cannot afford to make.

— Paul

Medicare Advantage and Medigap options that work with Part B

Part B coverage is the foundation, but it leaves real gaps. The right supplemental plan fills those gaps and makes your total healthcare cost predictable.

At Paulbinsurance, we work with individuals turning 65 and retirees every day to find plans that complement their Part B coverage. If the 20% coinsurance concerns you, a Medicare Supplement plan can cover most or all of that exposure. If you want bundled coverage with added benefits, Medicare Advantage plans combine Parts A and B through private insurers and often include dental, vision, and drug coverage. Paul Barrett and the Paulbinsurance team have been helping Medicare beneficiaries build the right coverage combination since 2007. Reach out to compare your options with no pressure and no cost.

FAQ

What is Medicare Part B in simple terms?

Medicare Part B is the outpatient medical insurance portion of Original Medicare. It covers doctor visits, preventive screenings, durable medical equipment, and outpatient hospital services.

Is Medicare Part B mandatory?

Part B is voluntary by law, but skipping it without qualifying coverage results in a permanent 10% premium penalty for every 12 months you delay. Most people approaching 65 should enroll.

What does Medicare Part B not cover?

Part B does not cover inpatient hospital stays, prescription drugs taken at home, routine dental care, hearing aids, or routine vision exams. Part A covers inpatient care, and Part D covers home prescription drugs.

How much does Medicare Part B cost in 2026?

The standard monthly premium is $202.90 in 2026, with a $283 annual deductible and 20% coinsurance after the deductible. Higher-income beneficiaries pay more under IRMAA.

Does Medicare Part B have an out-of-pocket maximum?

No. Original Medicare has no annual cap on coinsurance costs under Part B. A Medigap supplement plan is the primary way to limit that exposure.