Medicare Part D is a prescription drug coverage program available to people 65 and older and to those under 65 who qualify for Medicare through a permanent disability. It works through private insurance plans approved by Medicare, and it follows federal rules that cap your out-of-pocket drug costs. In 2026, the out-of-pocket maximum sits at $2,100 for covered drugs. Part D drugs disability coverage comes in two forms: a standalone Prescription Drug Plan (PDP) or a Medicare Advantage plan that bundles drug coverage (called an MA-PD). The Extra Help program, also known as the Low-Income Subsidy (LIS), can reduce premiums, deductibles, and copays for people who qualify.

How does Part D drug coverage work for disability recipients?

Medicare Part D is available to people under 65 who qualify for Medicare due to a disability, and it works exactly the same as it does for those 65 and older. The plan types, cost protections, and enrollment rules all apply equally. That is a fact many people with disabilities do not realize until they are already past their enrollment window.

The key trigger is the 24-month waiting period. After 24 months of disability benefits through Social Security Disability Insurance (SSDI), you become eligible for Medicare, including Part D. There are two exceptions to this rule: people diagnosed with ALS (Lou Gehrig’s disease) qualify for Medicare immediately, and people with End-Stage Renal Disease (ESRD) have a separate eligibility path.

Once you have Medicare Part A and Part B, you can enroll in Part D. Your options are:

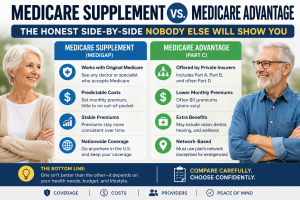

- Standalone PDP: A separate drug plan paired with Original Medicare or a Medicare Supplement plan.

- MA-PD: A Medicare Advantage plan that includes drug coverage, often bundling medical and prescription benefits into one monthly premium.

- Automatic enrollment: If you receive Extra Help and have not chosen a plan, Medicare may auto-enroll you in a low-premium PDP.

Delaying Part D enrollment during the disability-to-Medicare transition can result in a late enrollment penalty. That penalty adds a permanent percentage to your monthly premium for every month you went without creditable drug coverage. Enrolling on time is one of the most important financial decisions you will make when you first become Medicare-eligible.

Pro Tip: Review your Part D options at least 60 days before your Medicare start date. Use the Medicare Plan Finder tool at Medicare.gov to compare plans based on your specific medications.

What does Part D cost in 2026?

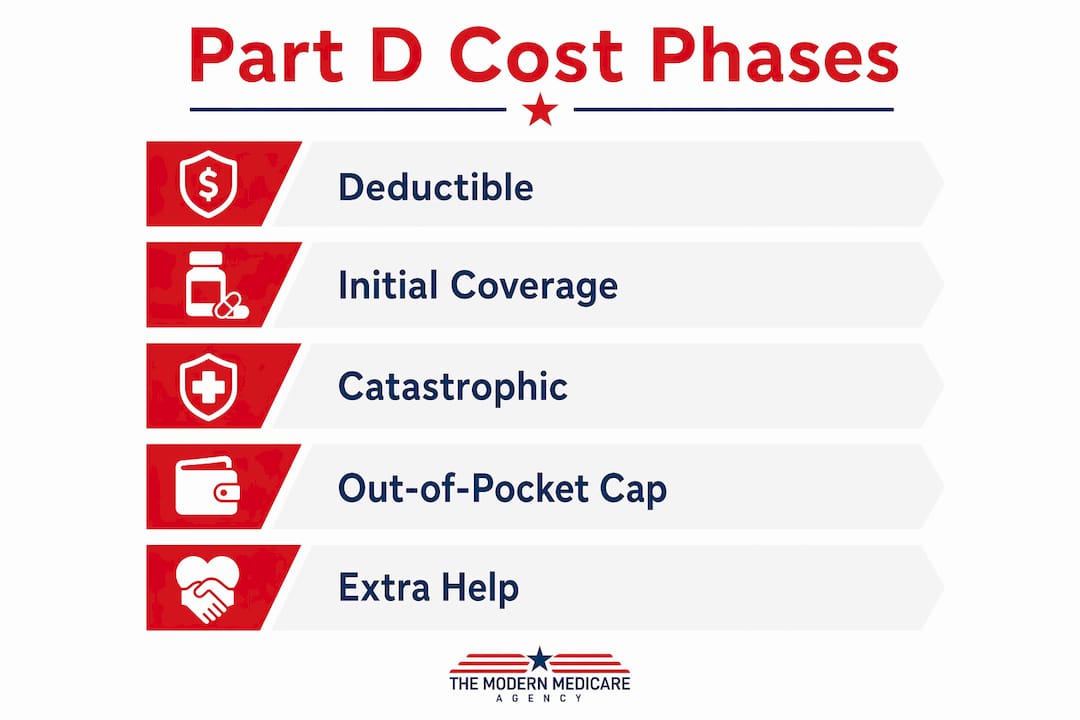

The Part D cost structure has three phases. Each phase determines how much you pay for covered drugs at the pharmacy.

| Phase | What triggers it | Your cost |

|---|---|---|

| Deductible phase | Start of plan year | You pay 100% up to $615 maximum |

| Initial coverage | After deductible is met | Standard 25% coinsurance |

| Catastrophic coverage | After $2,100 out-of-pocket | $0 copay or coinsurance |

The 2026 Part D deductible is capped at $615, though some plans set a lower deductible or none at all. Not every plan charges the maximum, so comparing plans by their deductible is worth your time.

After the deductible, you enter the initial coverage phase. Here, you typically pay 25% coinsurance on covered drugs. Your plan pays the rest. Costs in this phase count toward your $2,100 out-of-pocket limit.

Once you hit $2,100 in true out-of-pocket spending, you enter catastrophic coverage. At that point, no copay or coinsurance applies for covered drugs for the rest of the calendar year. This is a major protection for people who take expensive specialty medications or multiple brand-name drugs. For someone managing a chronic condition like multiple sclerosis or rheumatoid arthritis, reaching the catastrophic threshold mid-year can mean thousands of dollars in savings.

Beneficiaries should prioritize how quickly they expect to reach the catastrophic threshold over monthly premiums when selecting a plan. A plan with a slightly higher premium but a better formulary for your specific drugs may get you to $2,100 faster, saving more money overall.

How does Extra Help reduce Part D drug costs?

Extra Help is not simply a discount program. Extra Help is a critical tool to avoid long-term costs and penalties tied to Medicare Part D. The program covers premiums, deductibles, and copays, and it waives the late enrollment penalty entirely.

The average annual value of Extra Help is approximately $5,700. That figure reflects how much the program saves a qualifying beneficiary compared to paying full Part D costs without assistance.

Who qualifies? Eligibility is based on income and assets. Social Security automatically enrolls certain groups, including people who receive Medicaid or Supplemental Security Income (SSI). Others must apply through Social Security or their State Medicaid office.

Key benefits of Extra Help in 2026 include:

- Copay caps: No more than $12.65 for brand-name drugs and $5.10 for generics per fill.

- No late enrollment penalty: Extra Help waives this fee permanently while you remain enrolled.

- Reduced or eliminated deductible: Many Extra Help recipients pay no deductible at all.

- Special Enrollment Periods (SEPs): Extra Help grants SEPs during the first three quarters of the year, letting you switch plans outside of the standard Open Enrollment window.

The assumption that Extra Help guarantees zero cost in every plan is incorrect. Plan formularies vary, and some drugs may still carry higher cost-sharing under certain plan structures. Reviewing your plan annually protects you from unexpected cost increases.

Pro Tip: Even if you receive Extra Help, compare plans every fall during Open Enrollment (october 15 through december 7). Your current plan’s formulary or premium may change, and a better option may be available.

How do you choose the best Part D plan for disability recipients?

Choosing between standalone PDPs and Medicare Advantage plans with drug coverage can significantly affect your premiums and out-of-pocket costs. The right choice depends on your medications, your doctors, and your budget.

Medicare Advantage plans have grown as the primary source of drug coverage over standalone PDPs. Many MA-PD plans offer $0 premiums and bundle medical, hospital, and drug coverage into one plan. That simplicity appeals to many people, but it comes with network restrictions.

Here is how to evaluate your options:

- Check the formulary first. Every plan has a drug list called a formulary. Confirm your medications are covered before enrolling.

- Compare total costs, not just premiums. A $0 premium plan with high copays may cost more than a plan with a modest monthly premium.

- Verify pharmacy networks. Some plans offer lower costs at preferred pharmacies. Using an out-of-network pharmacy can significantly raise your costs.

- Use Medicare Plan Finder. This free tool at Medicare.gov lets you enter your medications and compare plans by total estimated annual cost.

Enrolling during your Initial Enrollment Period avoids the late enrollment penalty. For people with disabilities, this period begins when you first become eligible for Medicare after the 24-month SSDI waiting period. Missing it means paying a penalty for every month you were without coverage.

| Plan type | Best for | Key consideration |

|---|---|---|

| Standalone PDP | People with Original Medicare | Pairs with Medicare Supplement plans |

| MA-PD | People wanting bundled coverage | Network restrictions apply |

| Extra Help auto-enrollment | Low-income beneficiaries | Review annually to confirm best fit |

For a deeper look at comparing Part D drug plans, Paulbinsurance has a step-by-step guide that walks through formulary checks and cost comparisons. People with disabilities under 65 can also find specific guidance on Medicare options for disabled individuals at Paulbinsurance.

Key Takeaways

Medicare Part D provides prescription drug coverage to both seniors 65 and older and disabled individuals under 65, with the 2026 out-of-pocket cap at $2,100 and Extra Help reducing costs further for those who qualify.

| Point | Details |

|---|---|

| Disability eligibility | Medicare Part D becomes available after 24 months of SSDI benefits, with exceptions for ALS and ESRD. |

| 2026 out-of-pocket cap | Once you spend $2,100 on covered drugs, you pay $0 for the rest of the year. |

| Extra Help value | The program saves qualifying beneficiaries an average of $5,700 annually in Part D costs. |

| Enrollment timing | Enrolling during your Initial Enrollment Period avoids a permanent late enrollment penalty. |

| Annual plan review | Formularies and premiums change yearly, so reviewing your plan every fall protects your savings. |

What I have learned after nearly 20 years helping Medicare beneficiaries

The biggest mistake I see people with disabilities make is waiting. They assume they have time to figure out Part D after they get their Medicare card. By then, the enrollment window has often passed, and they are looking at a penalty that follows them for years.

The second mistake is ignoring Extra Help. People assume they will not qualify because they own a home or a car. The asset rules are more flexible than most people think. I have helped clients who were certain they would not qualify walk away with $0 premiums and $5 generic copays. Applying costs nothing and takes about 30 minutes.

The third thing I want you to understand is that the $2,100 out-of-pocket cap changes the math on plan selection. For years, people chased the lowest monthly premium. That made sense when there was no cap. Now, if you take expensive medications, a plan with a slightly higher premium but a better formulary may get you to zero cost-sharing faster. Run the numbers on total annual cost, not just the monthly bill.

I have seen people save over $3,000 a year simply by switching to a plan that covered their specific drugs at a lower tier. The Medicare Plan Finder tool makes this comparison straightforward. You enter your medications, your pharmacy, and your zip code. It shows you total estimated annual cost for every available plan. Use it every fall without exception.

— Paul

How Paulbinsurance can help you find the right Part D plan

Sorting through dozens of Part D plans while managing a disability or chronic condition is a real challenge. Paulbinsurance specializes in exactly this situation.

Paul Barrett has been helping Medicare beneficiaries since 2007, including people under 65 who qualify through disability. The team at Paulbinsurance compares standalone PDPs, Medicare Advantage plans with drug coverage, and Extra Help eligibility on your behalf. There is no cost to work with an independent agent, and you get a plan matched to your actual medications and budget. Whether you are newly eligible for Medicare or reviewing your current coverage, Paulbinsurance offers the guidance you need to make a confident decision.

FAQ

Who qualifies for Part D if they are under 65?

People under 65 qualify for Medicare Part D after receiving Social Security Disability Insurance (SSDI) benefits for 24 months. Individuals with ALS qualify immediately, and those with ESRD follow a separate eligibility path.

What is the Part D out-of-pocket maximum in 2026?

The 2026 Part D out-of-pocket cap is $2,100. Once you reach that amount in covered drug spending, you pay no copay or coinsurance for the rest of the calendar year.

How do I apply for Extra Help with Part D costs?

You apply for Extra Help through Social Security online at SSA.gov, by phone at 1-800-772-1213, or through your State Medicaid office. Some beneficiaries, including those on Medicaid or SSI, are automatically enrolled.

What is the late enrollment penalty for Part D?

The late enrollment penalty adds 1% of the national base beneficiary premium to your monthly Part D cost for every full month you went without creditable drug coverage. It is permanent and stays with you as long as you have Part D.

Can I change my Part D plan if I have Extra Help?

Yes. Extra Help gives you Special Enrollment Periods during the first three quarters of the year, allowing you to switch plans outside of the standard Open Enrollment window that runs from october 15 through december 7.