Medicare supplement coverage for disabled individuals under 65 is determined primarily by state rules and Social Security Disability Insurance eligibility, not by age alone. If you are under 65 and receiving SSDI benefits, you can qualify for Medicare Parts A and B after a mandatory waiting period. The challenge is what comes next. Accessing a Medicare supplement plan, formally called Medigap, depends heavily on where you live. Some states protect your right to buy one. Others leave you navigating underwriting restrictions that can result in denial. This guide explains exactly what your options are, how enrollment timing affects your costs, and where Medicare Advantage Special Needs Plans fit into the picture.

How Medicare eligibility works for disabled individuals under 65

Medicare eligibility for disabled people under 65 is triggered by SSDI entitlement, not by a doctor’s diagnosis or a personal choice. Most SSDI beneficiaries become eligible for Medicare Parts A and B after a 24-month waiting period from the date their SSDI entitlement begins. This means two full years pass before your Medicare card arrives. That gap creates real financial exposure for people managing serious, ongoing health conditions.

Two major exceptions shorten or eliminate the wait entirely:

- ALS (Amyotrophic Lateral Sclerosis): Medicare begins immediately upon SSDI entitlement. No waiting period applies.

- ESRD (End-Stage Renal Disease): Eligibility depends on the type of treatment. Dialysis patients typically wait three months, while kidney transplant recipients may qualify sooner. ESRD also requires a manual application rather than automatic enrollment.

For everyone else, Medicare enrollment is automatic after the 24-month mark. Social Security mails your Medicare card without you filing a separate application. Part A covers hospital stays, skilled nursing facility care, and hospice. Part B covers outpatient services, doctor visits, and durable medical equipment, though it carries a monthly premium.

Once enrolled in Parts A and B, you also become eligible for Part C (Medicare Advantage) and Part D (prescription drug coverage). Understanding which combination of these parts best fits your health needs and budget is where the real planning begins. For a full breakdown of eligibility rules, Paulbinsurance has published a detailed eligibility guide specifically for under-65 disabled beneficiaries.

What are your Medicare supplement options if you’re disabled and under 65?

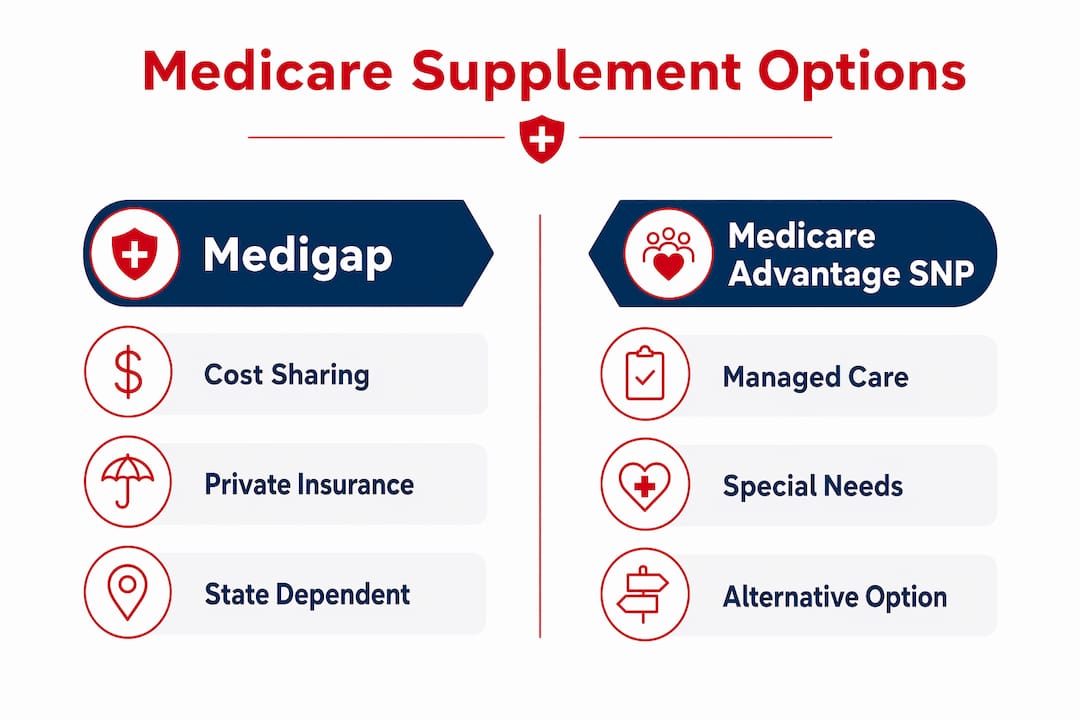

Medigap is the standard industry term for Medicare supplement insurance. These are private plans sold by insurers like Mutual of Omaha, Aetna, and UnitedHealthcare that pay costs Original Medicare leaves behind, including copayments, coinsurance, and deductibles. The problem for disabled beneficiaries under 65 is that federal law does not require insurers to sell you a Medigap policy before age 65. State rules determine whether you have guaranteed issue rights, meaning the insurer must sell you a plan regardless of your health history.

Currently, about 30 states plus the District of Columbia offer some form of Medigap access to under-65 Medicare beneficiaries. The protections vary widely. Some states require insurers to offer all standardized Medigap plans. Others limit access to one or two plan types. Several states impose waiting periods before coverage begins. If your state offers no protections, insurers can reject your application based on your medical history, which is exactly the kind of underwriting barrier that makes Medigap access difficult for people with chronic or disabling conditions.

When Medigap is unavailable or unaffordable, Medicare Advantage Special Needs Plans (SNPs) become the practical alternative. SNPs are designed specifically for people with chronic or disabling conditions. They bundle Parts A, B, and D into a single plan and often include benefits Original Medicare does not cover, such as dental, vision, hearing, and transportation.

| Feature | Medigap | Medicare Advantage SNP |

|---|---|---|

| Covers Medicare cost-sharing | Yes, broadly | Partially, with copays |

| Requires medical underwriting under 65 | Often yes, state-dependent | No |

| Includes drug coverage (Part D) | No, separate plan needed | Yes, typically included |

| Extra benefits (dental, vision) | No | Yes, many SNPs include these |

| Network restrictions | None (any Medicare provider) | Yes, plan network applies |

| Monthly premium | Higher on average | Often lower or $0 |

Pro Tip: If your state does not guarantee Medigap access under 65, apply for a Medicare Advantage SNP during your Initial Enrollment Period. Waiting can cost you this no-underwriting window.

How to enroll in Medicare supplement plans and timing considerations

Enrollment timing is the single most consequential decision a disabled under-65 Medicare beneficiary makes. Getting it wrong can mean higher premiums for life or losing access to coverage entirely.

-

Initial Enrollment Period (IEP): Your IEP begins three months before your Medicare Part B start date and extends three months after. This is your first and most protected window to enroll in Medicare Advantage, including SNPs. Missing it without a qualifying reason triggers a late enrollment penalty on Part B.

-

Medigap Open Enrollment Period: For people who turn 65, federal law provides a six-month Medigap open enrollment window with guaranteed issue rights. Under-65 disabled beneficiaries do not automatically receive this federal protection. If your state grants it, the window typically opens when you first enroll in Part B.

-

Special Enrollment Periods (SEPs): Certain life events, such as losing employer coverage or moving out of a plan’s service area, trigger special enrollment periods that allow plan changes outside standard windows. These are time-sensitive and require documentation.

-

The Birthday Rule: Several states, including California, Oregon, and Idaho, have a Medigap Birthday Rule. This rule allows you to switch to an equal or lesser Medigap plan within 30 to 60 days of your birthday each year without medical underwriting. The Birthday Rule is one of the most underused protections available to disabled beneficiaries in qualifying states.

-

Turning 65: When you turn 65, you receive a fresh six-month federal Medigap open enrollment period with guaranteed issue rights. This is often the best opportunity for disabled beneficiaries in restrictive states to finally access the Medigap plan they want.

Pro Tip: Mark your 65th birthday on your calendar now. That six-month federal open enrollment window is your guaranteed chance to buy any Medigap plan regardless of your health history. Missing it resets your options back to state rules and underwriting.

Enrollment timing details matter more for disabled beneficiaries than for any other Medicare population because the windows are narrower and the consequences of missing them are steeper.

Managing costs and maximizing coverage as a disabled under-65 beneficiary

Cost is where the reality of Medicare supplement coverage hits hardest for disabled people under 65. The average Medigap premium in 2023 was $217 per month. That figure represents a significant monthly expense for someone living on SSDI income, which averages well below typical working wages. For many disabled beneficiaries, that premium alone makes Medigap financially out of reach.

Several programs exist specifically to reduce these costs:

- Medicare Savings Programs (MSPs): These state-administered programs pay some or all of your Part B premium, deductibles, and cost-sharing. Four MSP levels exist, each with different income thresholds.

- Extra Help (Low Income Subsidy): This federal program reduces Part D drug costs for people with limited income and resources. It can eliminate or sharply reduce drug plan premiums and copays.

- Medicaid dual eligibility: Some disabled under-65 beneficiaries qualify for both Medicare and Medicaid simultaneously. Medicaid can cover costs that Medicare does not, functioning as a supplement without the premium.

| Cost factor | What it covers | How to reduce it |

|---|---|---|

| Part B premium | Outpatient services | Medicare Savings Program |

| Medigap premium | Medicare cost-sharing gaps | Shop state-approved plans; consider SNP instead |

| Part D premium | Prescription drugs | Extra Help program |

| Out-of-pocket maximums | Annual spending cap | Medicare Advantage SNP plans include a cap; Original Medicare does not |

Plan choice and enrollment timing are financially critical because delaying enrollment can lead to higher premiums and reduced access to Medigap. A Medicare Advantage SNP often provides a more affordable entry point than Medigap for disabled beneficiaries who cannot access guaranteed issue protections. SNPs coordinate care across providers, which reduces duplicate testing and unnecessary specialist visits, lowering total spending beyond just the premium.

Key takeaways

Medicare supplement access for disabled individuals under 65 depends on state law, enrollment timing, and whether Medigap or a Medicare Advantage SNP better fits your coverage needs and budget.

| Point | Details |

|---|---|

| SSDI triggers Medicare after 24 months | ALS and ESRD are exceptions with shorter or immediate eligibility windows. |

| State rules control Medigap access | About 30 states offer some guaranteed issue rights for under-65 disabled beneficiaries. |

| SNPs are a practical Medigap alternative | Medicare Advantage Special Needs Plans require no underwriting and include drug and extra benefits. |

| Enrollment timing is financially critical | Missing your Initial Enrollment Period or state-specific windows can raise premiums permanently. |

| Cost assistance programs exist | Medicare Savings Programs and Extra Help reduce Part B and Part D costs for low-income beneficiaries. |

What I’ve learned after nearly 20 years helping disabled Medicare beneficiaries

The most common mistake I see disabled under-65 clients make is waiting. They assume they will figure out supplemental coverage later, or they assume their state will protect them the way federal law protects 65-year-olds. Neither assumption holds up.

I have worked with clients in states that offer strong Medigap protections under 65 and clients in states that offer none. The difference in their options is enormous. A client in Connecticut can buy a Plan G Medigap policy the day their Medicare starts. A client in Texas with the same diagnosis and the same SSDI income may be denied by every insurer they approach. That is not a hypothetical. It happens regularly.

My honest advice: treat your Initial Enrollment Period as your most valuable window. If Medigap is unavailable or unaffordable in your state, a Medicare Advantage SNP is not a consolation prize. For many disabled beneficiaries, it is genuinely the better fit. The coordinated care model, the built-in drug coverage, and the $0 or low premium structure address the real-world financial constraints that come with living on SSDI.

I also tell every client to check their eligibility for Medicare Savings Programs before paying a single dollar out of pocket. A surprising number of people qualify and never apply. That money stays in your pocket every month if you do the paperwork.

Finally, if you are in a state with the Birthday Rule, use it. It is one of the few moments where the system actually works in your favor, and most people never hear about it until it is too late.

— Paul

Get expert help with your Medicare supplement options

Navigating Medicare supplement coverage as a disabled person under 65 is genuinely complex. The rules differ by state, the enrollment windows are narrow, and the cost of getting it wrong compounds over time. Paulbinsurance specializes in exactly this situation.

Paul Barrett and the Paulbinsurance team have been helping Medicare consumers since 2007. Whether you are weighing Medigap against a Medicare Advantage SNP, trying to understand your state’s guaranteed issue rules, or looking for the most affordable path forward, the team works as independent agents with access to multiple carriers. Start by reviewing the Medigap vs. Medicare Advantage comparison to understand which direction fits your needs, then reach out for a no-pressure conversation about your specific situation.

FAQ

Who qualifies for Medicare under 65 with a disability?

People under 65 who have received SSDI benefits for 24 months qualify for Medicare Parts A and B automatically. ALS patients qualify immediately; ESRD patients qualify based on treatment type.

Can a disabled person under 65 buy a Medigap plan?

It depends on your state. Federal law does not require insurers to sell Medigap to under-65 beneficiaries, but roughly 30 states have laws that provide some level of guaranteed issue rights for this group.

What is a Medicare Special Needs Plan and who is it for?

A Medicare Special Needs Plan (SNP) is a type of Medicare Advantage plan designed for people with chronic or disabling conditions. SNPs bundle Parts A, B, and D and often include dental, vision, and coordinated care benefits.

What happens to my Medigap options when I turn 65?

At 65, federal law grants a six-month open enrollment period during which any insurer must sell you any Medigap plan without medical underwriting. This is the strongest guaranteed issue protection available and applies regardless of your health history or prior disability status.

Are there programs to help disabled Medicare beneficiaries afford coverage?

Yes. Medicare Savings Programs cover Part B premiums and cost-sharing for qualifying low-income beneficiaries. The Extra Help program reduces Part D costs significantly and is available to people with limited income and resources.