If you have a Medicare Supplement plan, there’s a good chance your premium went up this year. And if it went up more than you expected — you’re not imagining it. 2026 has brought some of the steepest Medigap rate increases in recent memory, catching many retirees off guard right when household budgets are already being stretched by inflation.

After 18+ years of working exclusively in Medicare, I’ve seen rate cycles come and go. But what’s happening in 2026 is different in scale. This isn’t the typical low-single-digit annual adjustment that most policyholders had come to expect. We’re talking about double-digit increases across major carriers, in states all across the country — and in some cases, increases that would have been unthinkable just a few years ago.

This post is going to give you the straight story: what’s actually driving these increases, which companies have raised rates the most, which states have been hit hardest, and — most importantly — what your options are right now.

Key Takeaways

- According to Telos Actuarial, Plan G rate increases among six major carriers ranged from 12% to 26% in the first quarter of 2026 alone.

- Some states have seen increases as high as 45% (Chubb) and 55.6% (Asuris Northwest Health in Alaska) from certain carriers — levels that are genuinely unprecedented.

- The increases are being driven by a combination of medical inflation, higher healthcare utilization, aging risk pools, and years of aggressive “teaser rate” pricing that insurers are now correcting.

- Not all companies raised rates equally. Some carriers have managed increases more conservatively than others.

- If your rate spiked this year, you may have options — including switching carriers, moving to High-Deductible Plan G, or exploring other strategies.

Table of Contents

- How Bad Are the 2026 Medigap Rate Increases, Really?

- Which Companies Raised Rates the Most in 2026?

- Which States Got Hit the Hardest?

- What’s Actually Driving These Increases?

- Companies with More Stable Rate Histories

- What Can You Do If Your Rate Spiked?

- The Bottom Line: What This Means for Your Coverage

- Frequently Asked Questions

How Bad Are the 2026 Medigap Rate Increases, Really?

Let me put this in context with some numbers.

Historically, annual Medigap rate increases ran in the low-to-mid single digits for most carriers in most markets. In many states, a 3% to 5% increase was typical. A 7% to 8% increase was considered elevated. Anything above 10% was unusual enough to raise eyebrows.

That’s no longer the world we’re living in.

According to Telos Actuarial — an independent Nebraska-based actuarial firm that tracks Medigap rate filings nationwide — Plan G rate increases among six major carriers ranged from 12% to 26% in early 2026 state filings. In 2022, that same group of insurers was averaging increases as low as 5%. The acceleration has been steep and fast.

More than 12 million Americans are enrolled in a Medicare Supplement policy — approximately 43% of all people on traditional Medicare. These increases are not affecting a small group. They are hitting millions of retirees on fixed incomes, in some cases during the same year they’re also absorbing higher Part B premiums ($202.90 in 2026) and higher Part D costs.

Half of all Medicare Supplement companies implemented double-digit rate increases for Plan G during the 2023–2024 period. 2026 is continuing — and in many cases accelerating — that trend.

As one industry observer noted, five years ago it was “exceedingly uncommon” to see a carrier with an increase above 10%. Today, 10% is closer to the floor for many major carriers.

Which Companies Raised Rates the Most in 2026?

Based on state rate filings and industry data, here is an honest look at where the biggest increases have been concentrated.

UnitedHealthcare (AARP)

UHC is the largest Medigap carrier in the country by enrollment, and their rate activity in 2026 has drawn significant attention. State-by-state filings show UHC raising Plan G rates meaningfully across multiple markets:

- New York: +17.8%

- Texas: +15.1% (effective July 2025, carrying into 2026)

- Illinois, North Dakota, Ohio: +12.6%

UHC is a financially stable company — that’s not in dispute. But their sheer size means that when they file double-digit increases, millions of people feel it simultaneously. And because many UHC policyholders enrolled years ago based on brand recognition rather than rate history, they’re now experiencing increases on top of already-elevated premiums.

Aetna

Aetna has been particularly aggressive with rate corrections in several states:

- Kentucky: +14.3%

- Maryland and Pennsylvania: +15.8%

- South Dakota: +19%

Telos Actuarial’s data shows that Aetna, along with Mutual of Omaha and UHC, took significant steps to address rising claims trends in 2024 — meaning their 2025 and 2026 rate actions reflect ongoing correction after years of elevated claims experience.

Blue Cross Blue Shield / Anthem

BCBS affiliates have shown mixed results across states, but some markets have seen notable increases:

- Arizona (BlueCross): +14.5%

- North Carolina (Blue Cross NC): +4.7% — one of the more modest increases among major carriers

- Alaska (Premera Blue Cross): +12% on Plan G

In certain regions, Anthem-affiliated carriers have implemented significant premium jumps, particularly in older, closed blocks where the risk pool has aged considerably. The wide range — from 4.7% in North Carolina to 12%+ in Alaska — illustrates how much carrier performance varies by state even within the same affiliated family.

Regional Carriers in Alaska — An Extreme Case

Alaska has been one of the hardest-hit states in 2026. Premera Blue Cross raised Plan G premiums by nearly 12%, with another carrier in the state filing close to 13%. But the most extreme filing came from Asuris Northwest Health, which filed an increase of 55.6% — one of the largest single-carrier rate actions documented anywhere in the country this year. While Asuris is not a national carrier, this filing illustrates just how severe the closed-block and claims-pressure problem can become in concentrated markets.

Chubb

While not one of the household names, Chubb reportedly filed increases as high as 45% in certain markets in early 2026. This is an example of the closed-block problem in extreme form — a smaller insurer with an aging, concentrated risk pool facing actuarial reality all at once.

A Note on Cigna

Cigna’s rate picture is more nuanced. Their legacy blocks of business — particularly older individual policies from prior acquisitions — have seen steeper increases as those risk pools age. However, Telos Actuarial’s 2025 data showed Cigna’s increases were more aligned with historical norms compared to the larger swings at Aetna, UHC, and others. That said, policyholders in older Cigna blocks should still review their current rates carefully.

Which States Got Hit the Hardest?

Rate increases aren’t uniform across the country — where you live matters enormously. Here’s where the data shows the most significant impacts:

Oklahoma saw the largest average Plan G increase of any state — 22% year-over-year, according to ValuePenguin, with average monthly premiums rising from $130 to $158.

Alaska has been hammered, with multiple carriers filing increases well above 10%, and at least one outlier filing above 50%.

Illinois, Ohio, and Texas have seen consistent double-digit filings from multiple major carriers simultaneously.

New York and Massachusetts, by contrast, have fared somewhat better. States with stronger regulatory oversight of insurance rate filings have seen smaller approved increases pass through — though New York’s community-rated system means premiums are already among the highest in the nation ($354/month average for Plan G in 2026).

Rhode Island, Missouri, Delaware, and Hawaii have seen the lowest average increases — approximately 7% each — providing some insulation against the broader trend.

The lesson: the same carrier can file very different increases in different states, depending on local claims experience, regulatory environment, and the specific risk pool in that market.

What's Actually Driving These Increases?

Understanding the “why” behind these increases isn’t just academic. It helps you evaluate whether your carrier is responding to real market forces or simply correcting years of irresponsible pricing.

1. Healthcare Utilization Is Up Significantly

Americans — and Medicare beneficiaries in particular — are using healthcare services at elevated rates. More doctor visits, more procedures, more ongoing care management. As the population ages, claims volume rises, and insurers must adjust premiums to cover those costs.

2. Medical Inflation Is Running Hot

Healthcare inflation is outpacing general inflation by a meaningful margin. Labor costs for healthcare workers, hospital facility fees, specialist costs, and pharmaceutical expenses are all rising. Employers are projecting a 6.5% increase in healthcare costs for 2026 — one of the largest jumps in over a decade. Medigap carriers absorb these same underlying cost pressures.

3. Medicare Advantage Refugees Coming Back to Medigap

This is a factor that doesn’t get enough attention. When Medicare Advantage plans tighten networks, add prior authorizations, or exit markets — which has been happening with increasing frequency — some sicker, higher-utilizing beneficiaries return to traditional Medicare and Medigap. This can shift the claims profile of a Medigap risk pool upward, contributing to higher loss ratios and subsequent rate corrections.

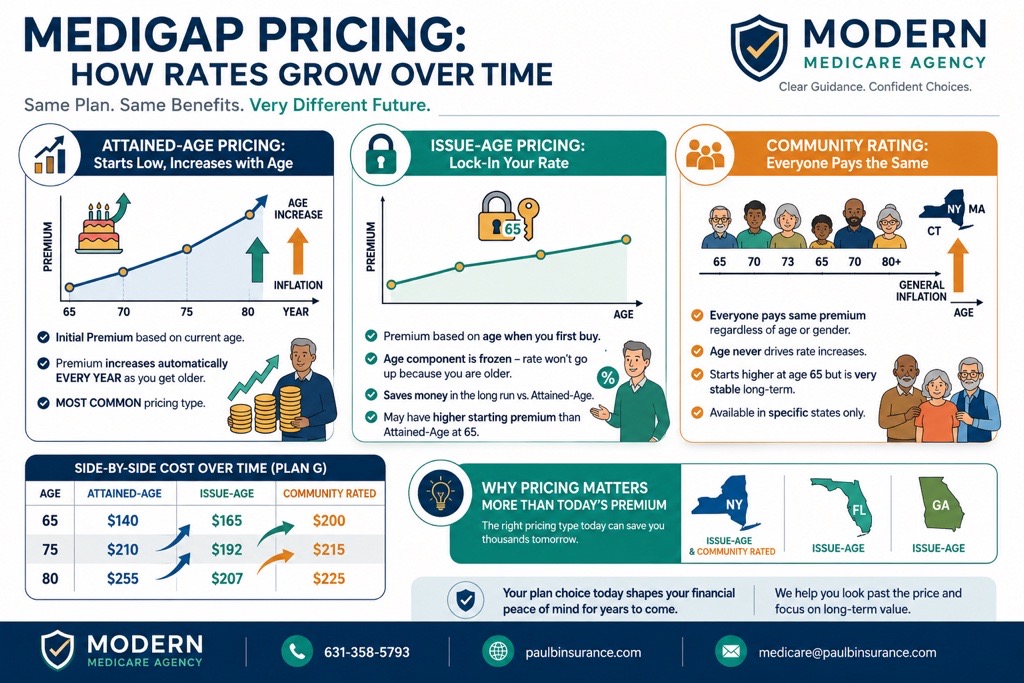

4. The Closed Block Problem

When a carrier stops selling a plan to new enrollees — as happened broadly with Plan F after January 2020 — that group of policyholders becomes a “closed block.” No new, younger, healthier members join. The existing members age together, use more healthcare services, file more claims, and premiums climb faster than they would in an active, open block. This is the single biggest structural driver of the largest rate spikes we’re seeing.

5. Years of Teaser Rate Pricing Coming Due

Some carriers spent several years pricing their plans aggressively below actuarial reality to attract market share. Those decisions are now being corrected with steeper-than-average increases. The retirees who were lured in by low introductory rates at 65 are now absorbing the bill.

Companies with More Stable Rate Histories

This picture isn’t uniformly grim. Some carriers have historically managed rate increases more conservatively — and that track record matters.

State Farm consistently ranks among the most rate-stable Medigap carriers in the country, with an A++ (Superior) A.M. Best rating — the highest possible. Their increases have historically been modest and predictable.

Mutual of Omaha benefits from one of the largest active Medigap risk pools in the country. A large, open pool of continuously enrolling, relatively healthy new members helps dilute claims costs and supports more conservative rate adjustments. Note: Telos data did show Mutual of Omaha among the carriers taking more significant steps to address claims trends in 2024 — so “more stable” doesn’t mean immune to increases, but their pool dynamics provide structural advantages.

Wellabe (formerly Medico) has generally maintained more modest, predictable rate histories over time and is worth including in any independent broker comparison.

Key distinction: Even the more stable carriers are raising rates in 2026. The difference is degree and consistency. A carrier raising rates 5% to 7% annually in a disciplined, predictable way is categorically different from one that keeps rates artificially low for years and then corrects with a 20%+ single-year spike.

What Can You Do If Your Rate Spiked?

If you opened your renewal notice this year and felt the shock, here’s what I’d actually recommend.

Option 1: Shop Competing Carriers (If You Can Pass Underwriting)

If you’re still in good health, this is the first conversation to have with an independent broker. Because Medigap plans are standardized, a Plan G from one A-rated carrier covers the exact same benefits as a Plan G from another. If your rate jumped 18% this year and a comparable carrier is offering the same plan for significantly less, the math may strongly favor switching — even accounting for a modest premium at the new carrier.

The honest caveat: switching requires medical underwriting in most states (outside of specific guaranteed issue windows). If you have significant health conditions, you may not be able to qualify. This is exactly why choosing the right carrier at age 65 — before health conditions develop — is so critical.

Option 2: Consider High-Deductible Plan G

High-Deductible Plan G (HD Plan G) offers the same ultimate coverage as standard Plan G but requires you to meet a deductible first ($2,950 in 2026) before the plan covers gaps. In exchange, the premium is dramatically lower — often around $50 to $90 per month depending on your state and carrier, versus $180+ for standard Plan G.

For someone in good health who rarely uses significant medical services, HD Plan G can represent real annual savings even after accounting for the deductible. It’s worth running the numbers.

I’ll be transparent: HD Plan G pays a lower commission than standard Plan G. I recommend it anyway when it’s the right fit — because the right answer for the client is the right answer, period.

Option 3: Leverage State-Specific Protections

New York is one of the few states with year-round guaranteed issue for Medigap — meaning you can switch carriers at any time without medical underwriting. If you’re in New York, you have more flexibility than most. A handful of other states have birthday rules or similar protections that create annual windows to switch without underwriting. Ask your broker what applies in your state.

Option 4: Have an Independent Broker Run a Full Comparison

This costs you nothing and takes about 15 minutes. An independent broker who represents 40+ carriers can run a side-by-side comparison of your current plan against competing options in your state — including rate histories, AM Best ratings, and current premiums. If switching makes sense, they’ll tell you. If it doesn’t, a good broker will tell you that too.

The Bottom Line: What This Means for Your Coverage

The 2026 Medigap rate environment is a wake-up call — not just for people experiencing increases right now, but for anyone who hasn’t yet enrolled in a Medicare Supplement plan.

The decisions you make at age 65, during your initial enrollment window, are the most important Medicare decisions you’ll ever make. Choosing a carrier based solely on the lowest introductory rate is a strategy that looks good on paper for one year and can cost you thousands of dollars over the following decade.

Can I switch Medicare Supplement companies after a rate increase? Yes, you can apply to switch at any time — but outside of specific guaranteed issue windows, you’ll need to pass medical underwriting. An insurance company can decline your application based on your health history. If you’re in good health, switching may be a strong option. If you have significant health conditions, it may be more difficult. This is why making a careful choice at age 65 is so important.

A good independent Medicare broker who works exclusively in this space — not a generalist who handles home, auto, life, and Medicare — knows this rate history. They track it. And they use it to help you make a decision that holds up not just at 65, but at 75 and 85 as well.

If your rate went up significantly this year, let’s talk. I’ll run a free, no-pressure comparison of every option available in your state and give you a straight answer about whether switching makes sense for your specific situation.

Call 631-358-5793 or visit paulbinsurance.com to schedule your free consultation.

Frequently Asked Questions

Why did my Medicare Supplement premium go up so much in 2026? You’re not alone. According to Telos Actuarial, Plan G increases among major carriers ranged from 12% to 26% in early 2026 — far above the low-single-digit increases that were typical in most markets just a few years ago. The primary drivers are higher healthcare utilization, medical inflation, aging risk pools, and years of artificially low “teaser rate” pricing that insurers are now correcting. It’s a market-wide issue, though the size of the increase varies significantly by carrier and state.

Can I switch Medicare Supplement companies after a rate increase? Yes, you can apply to switch at any time — but outside of specific guaranteed issue windows, you’ll need to pass medical underwriting. An insurance company can decline your application based on your health history. If you’re in good health, switching may be a strong option. If you have significant health conditions, it may be more difficult. This is why making a careful choice at age 65 is so important.

Which Medicare Supplement company has the lowest rate increases? Historically, State Farm has been recognized for the most conservative rate increases, along with a top A++ AM Best rating. Mutual of Omaha and Wellabe (formerly Medico) have also shown more predictable rate histories than many larger carriers. That said, “lowest rate increases” varies by state, plan type, and the specific block of business — which is why working with an independent broker who tracks this data is so valuable.

Are rate increases the same in every state? No — and the differences can be dramatic. Oklahoma saw an average 22% Plan G increase. Rhode Island, Missouri, Delaware, and Hawaii saw closer to 7%. In Alaska, Premera filed a 12% increase while Asuris Northwest Health filed an extraordinary 55.6% increase — among the highest documented anywhere in the country. Your state’s regulatory environment, the specific carriers active there, and the local claims experience all influence what rate increases look like where you live.

Is High-Deductible Plan G a good option if my rates are too high? It can be, depending on your health and financial situation. HD Plan G offers the same ultimate coverage as standard Plan G but requires you to meet a $2,950 deductible first. In exchange, premiums are dramatically lower — often $50 to $90/month. For someone in good health who doesn’t use significant medical services, the annual premium savings can more than offset the deductible risk. Run the numbers with an independent broker before deciding.

What’s the difference between an open block and a closed block? An open block is a group of policyholders that continuously adds new, younger, healthier members — which helps spread risk and moderate rate increases. A closed block is a group that stopped accepting new members at some point. As existing members age together and use more healthcare services, costs per person rise faster. Closed blocks are a major driver of the largest rate spikes. Always ask your broker whether the plan you’re considering is an open or closed block of business.

Does using an independent broker cost me anything? No. Independent Medicare brokers are compensated by the insurance company when you enroll. Your premium is identical whether you use a broker or go directly to the carrier. There’s no fee, no markup, and no financial reason not to work with one. What you gain is access to 40+ carriers, rate history data that isn’t available to the public, and an advocate who works for you — not for any single company.

Paul Barrett is the founder and Principal Agent of The Modern Medicare Agency, a Medicare-only independent brokerage based in Melville, NY. With 18+ years of Medicare-exclusive experience, licensure in 34 states, and relationships with 40+ carriers, Paul has helped 5,000+ clients navigate Medicare with clarity and confidence. He is the author of Medicare Mastery Unlocked.