What if your next birthday came with a gift that actually lowered your monthly bills? We understand the anxiety that comes with rising monthly premiums, especially as we see costs projected to climb by up to 12 percent this year. It feels unfair to stay with a company that provides poor service just because you fear a health history check. You deserve a path to better coverage that doesn’t involve stress or complex medical exams. We are here to help you understand the medigap birthday rule states so you can take control of your healthcare costs.

In this guide, we reveal which states allow you to switch plans regardless of your health status. We will explain how these rules work in places like Indiana, Delaware, and West Virginia, which have all introduced new protections for policyholders in 2026. You will learn the specific windows and carrier rules for your state so you can move toward a more secure financial future with total peace of mind. Our mission is to protect your retirement by making these complex rules simple and easy to follow.

Key Takeaways

- Learn how to bypass medical questions and lower your monthly premiums by using state-level guaranteed issue rights that protect your budget.

- See the updated 2026 list of medigap birthday rule states, including new additions like Indiana and West Virginia that offer you more freedom to switch carriers.

- Understand how to move “sideways” to a plan with equal benefits while protecting your retirement savings from high premium hikes.

- Discover the simple steps we use to compare your current rates against the 2026 market to ensure you aren’t overpaying for your coverage.

- Find out how an independent advocate can shop dozens of carriers to find the best customer service and lowest rates available in your specific zip code.

What is the Medigap Birthday Rule and How Does It Work?

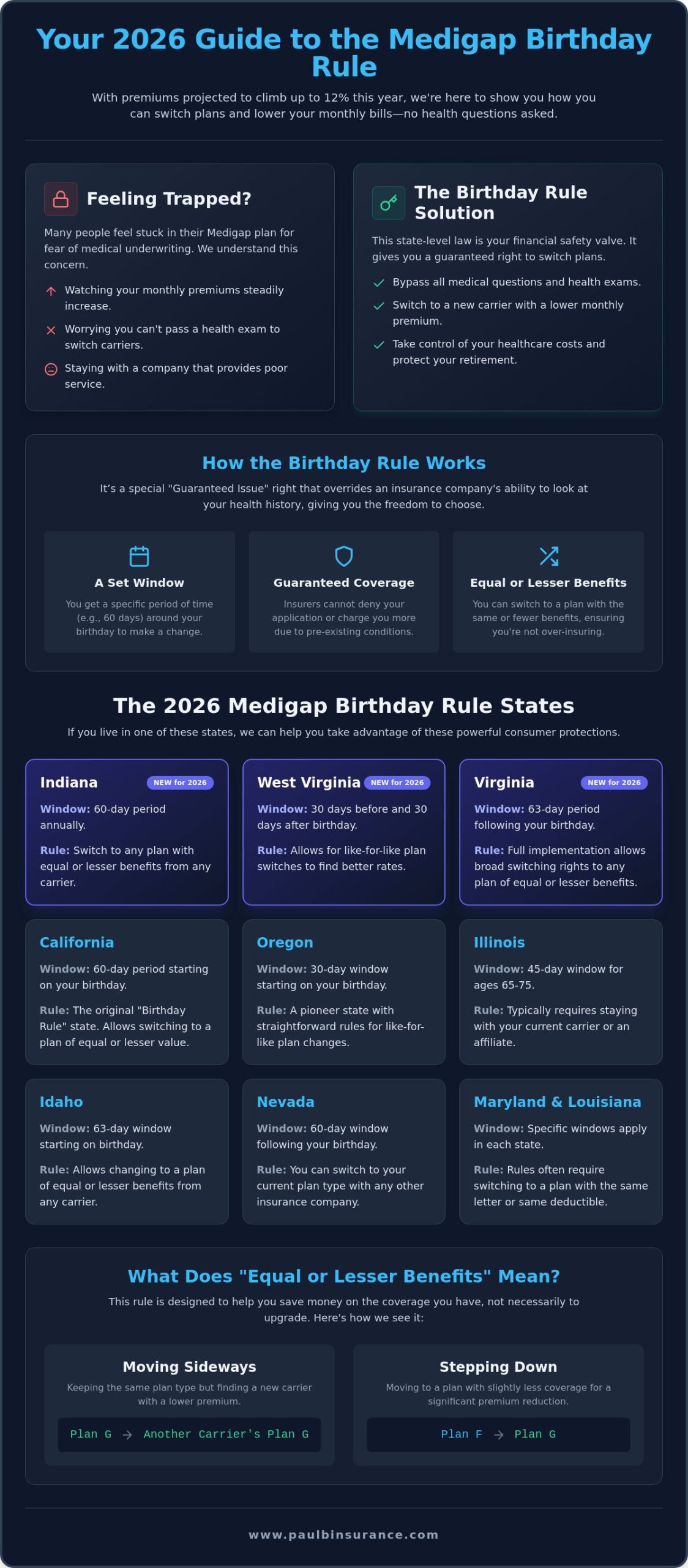

We know how it feels to watch your monthly premium climb while you feel trapped in a plan that no longer fits your budget. Most people believe they only have one chance to buy a Medigap plan without answering a long list of health questions. Under federal law, this is usually true. However, several medigap birthday rule states have created a special path for you. We call this the Birthday Rule. It is a state-level law that gives you a specific window of time around your birthday to switch your coverage without any stress or medical exams.

Why does this matter so much? Outside of these special rules, companies use a process called medical underwriting. This is when an insurer looks at your health history and pre-existing conditions to decide if they will cover you. They can charge you a much higher rate or even deny your application entirely if you’ve had a recent health setback. Because of this, many seniors think they are stuck with their plan forever. They stay with carriers that have poor customer service or high prices because they don’t think they can pass a health exam. The birthday rule removes that fear completely.

Think of this rule as a financial safety valve for your retirement. It protects your fixed income from the rising costs of healthcare. It’s also vital to remember that this is different from the Fall Open Enrollment you see on television every October. That window is specifically for Medicare Advantage and Part D plans. Medigap doesn’t have a federal annual enrollment period. Without a state-specific rule, you could be locked into your current carrier’s rate increases for the rest of your life.

The Problem with the “Standard” Medigap Rules

Under standard rules, you generally get a six-month window when you first sign up for Medicare Part B. After that, the door often slams shut. Insurance companies want to keep you on their books as you get older because they can raise your rates every year. They know you’re worried about your health history. In 2026, waiting for a federal change to these rules isn’t a safe strategy. You need to use the state-level protections that exist right now to keep your costs down.

The Birthday Rule Solution

The birthday rule overrides the insurance company’s right to ask about your health. It gives you what we call a Guaranteed Issue right. Guaranteed Issue is the legal right to buy a policy regardless of your medical history or pre-existing conditions. In most Medigap (Medicare Supplement Insurance) markets, this window lasts for 60 days. It usually begins on your birthday, though some medigap birthday rule states let you start the process up to 30 days early. We can help you time this move perfectly so your new, lower premium starts the moment your old one ends.

The 2026 List of Medigap Birthday Rule States

We’ve seen a wonderful shift recently as more states adopt these consumer protections. For years, California and Oregon were the only “pioneer states” offering this relief. Today, the list of medigap birthday rule states has grown significantly. This expansion means more people can escape high premiums without being stopped by a health exam. If you live in a state without these rules, you might feel left behind, but we are seeing a clear trend toward more states joining this movement every year. It’s a journey from feeling stuck to having total control over your healthcare budget.

Beyond the pioneers, we now see a strong presence in the “expansion states” like Illinois, Nevada, Idaho, and Maryland. Each state has its own unique rhythm for how the rule works. Some give you a month, while others give you nearly two months to shop for a better rate. You can find official Medigap policy information on the federal level, but remember that these specific birthday protections are handled by your state’s department of insurance. We are here to help you decipher those state-specific documents so you don’t have to face the confusion alone.

State-Specific Window Variations

California and Oregon offer a 60-day window that starts on your birthday. However, Oregon is slightly more restrictive with a 30-day window in many cases, so checking your specific dates is vital. Illinois provides a 45-day window, but it’s specifically for those aged 65 to 75 and usually requires staying with your current insurer or an affiliate. In Louisiana and Maryland, the rules are very specific about switching to plans with the same deductible. We don’t want you to miss these deadlines, as the clock starts ticking the moment your birthday arrives.

Virginia’s New 2026 Landscape

One of the most exciting changes for 2026 is the full implementation of Virginia’s rule, which began on July 1, 2025. Virginians now have a 60-day window following their birthday to switch to a plan with the same lettered benefits. This is a massive win for East Coast enrollees who previously felt stuck. Along with Virginia, we’ve welcomed Delaware, Indiana, and West Virginia to the list of medigap birthday rule states this year. Each of these states has slightly different rules about whether you can switch to any carrier or just your current one. Because every state has different fine print, we recommend speaking with a medicare broker to verify your specific state deadlines. If you live in New York or Connecticut, you actually have “all year” protections that are even more flexible than a birthday rule. We can help you navigate these differences by viewing current 2026 plan options together to find your best path forward.

Understanding “Equal or Lesser” Benefits

We often find that the biggest source of confusion is what you are allowed to buy when using your birthday window. The golden rule in most medigap birthday rule states is simple: you can move “sideways” or “down,” but you cannot move “up.” This means you can switch to a plan with the same benefits or fewer benefits than your current policy. You cannot use this rule to jump from a plan with less coverage to one that offers more without answering medical questions. We want to ensure you don’t lose your chance to switch by applying for the wrong level of coverage.

For example, the most common move we see in 2026 is switching from Plan G to another Plan G. Since the benefits for Plan G are identical regardless of which company provides it, this is a perfect way to lower your premium. You get the exact same coverage but at a lower price. We also see many people moving from Plan G to Plan N to save even more on their monthly bills. Plan N is a wonderful choice if you don’t mind a small copay for office visits in exchange for a much lower monthly cost. It’s a journey from high monthly bills to a more manageable budget.

If you are one of the many people still holding a grandfathered Plan F, you have a unique opportunity. Because Plan F covers the Part B deductible, which is $283 in 2026, and Plan G does not, Plan G is considered a “lesser” benefit plan. This allows you to move from Plan F to Plan G in almost every state with a birthday rule. This move helps you avoid the high premium spikes often seen with older Plan F policies while still maintaining excellent coverage for your hospital and doctor visits.

The Hierarchy of Medigap Plans

We consider Plan G the ceiling for most people who joined Medicare after 2020. It offers the most comprehensive coverage available today. If you want to understand the basics of these different levels, our guide on What Is Medicare Supplement Insurance? can help you see the full picture. Plan N is the next step down. It’s an excellent option for healthy budgeters who want to keep their out-of-pocket costs predictable while lowering their fixed monthly expenses. The Medigap birthday rule makes it easy to step down to these plans without any stress.

Switching Between Carriers

One of the most empowering parts of the rules in medigap birthday rule states is that they apply across different companies. You aren’t tied to your current insurer. In 2026, Carrier A might charge you a higher rate for a Plan G while Carrier B offers the same thing for significantly less. Because Medigap benefits are standardized by the government, the only real difference you’ll notice is the name on the card and the price you pay each month. We love helping our clients find these hidden savings by comparing every option available in their zip code.

How to Prepare for Your Medigap Birthday Switch

Preparing for a change can feel overwhelming, but we are here to make the process smooth and certain. The first thing you should do is check what you are currently paying against the 2026 market rates. Prices change every year; you might be surprised to find that a different carrier offers the exact same Plan G for much less than your current one. Next, you must verify the specific window for your location. As we discussed, the medigap birthday rule states have different timelines, ranging from 30 to 60 days. Missing this window by even a single day can mean losing your right to switch without a health exam.

Once you know your dates, gather your current Medigap ID card and your red, white, and blue Original Medicare card. Having these ready makes the application process much faster. Finally, we recommend reaching out to an independent broker. Unlike a company representative who only sells one brand, we can shop every available 2026 plan in your zip code to find the best value for you. We are dedicated to protecting your interests and ensuring you never pay more than necessary for your coverage.

Timing Your Application

We always tell our clients: do not cancel your old plan until your new coverage is fully confirmed. We can help you set the effective date so your new policy starts the very day your old one ends. This ensures you never have a gap in protection. While the window is tied to your birthday, you don’t have to wait until that day to start looking. Researching a few weeks early gives us plenty of time to find the perfect fit. This proactive approach removes the stress of a last-minute decision.

Common Pitfalls to Avoid

One of the biggest mistakes is trying to move to a plan with more benefits, which triggers the medical questions you are trying to avoid. Stick to equal or lesser benefits to keep your guaranteed right. It is also a great time to look at your other coverage. Many people forget to update their Medicare Part D or dental insurance when they switch Medigap plans. We can review your entire portfolio to ensure you have the best protection at the lowest possible price. If you are ready to start your journey to better savings, contact us today to compare 2026 rates and see how much you can save.

Why Work With an Independent Medicare Agent?

Choosing the right plan in one of the medigap birthday rule states shouldn’t feel like a solo mission. We know the stress of looking at dozens of different prices and wondering if you are making the right choice. There is a big difference between a captive agent and an independent broker. A captive agent works for one specific insurance company. They can only offer you the plans that their company sells, even if a competitor has a much lower rate. We choose a different path. As independent brokers, we work for you, not the insurance giant. We are your advocates throughout this entire process.

Our team shops over 40 different carriers to find the lowest rate for your specific zip code. Because Medigap plans are standardized by the government, the coverage is the same, but the prices are not. We take the time to compare every available option in 2026 to ensure you aren’t overpaying for your peace of mind. We handle the paperwork and the transition details so you don’t have to worry about a thing. It’s our mission to move you from a state of confusion to a state of total certainty.

No Cost to You, Every Benefit for You

You might wonder how much a service like this costs. Our help is completely free to you as a consumer. We provide unbiased comparisons that government websites often can’t offer because we understand the local market trends and carrier reputations in 2026. While a website can give you a list of numbers, we give you context and personal advice. Our year-round support is a key differentiator that ensures you always have a professional to call when questions arise, not just during your birthday window. We stay by your side long after your new policy is in place.

Starting Your 2026 Medicare Journey

We believe that everyone deserves to feel protected and empowered when it comes to their healthcare. The journey through the various medigap birthday rule states can be complex, but it doesn’t have to be painful. We invite you to reach out for a personalized consultation where we can listen to your needs and build a plan that fits your life. Let us take the anxiety out of the process and replace it with a clear, logical path forward. You’ve worked hard for your retirement, and we are here to help you protect it. Let us help you find the best Medigap rate today so you can get back to enjoying what matters most.

Take Control of Your Retirement Savings Today

You don’t have to feel trapped by rising premiums or fear medical exams. The medigap birthday rule states offer a clear, legal path to better rates by allowing you to switch to equal or lesser benefits without a single health question. We’ve seen how this annual window can protect your fixed income from the premium hikes projected for 2026. You don’t have to navigate these complex state-specific deadlines alone.

Paul Barrett and his dedicated team are licensed in over 34 states and work with more than 40 carriers to find the best fit for your budget. We are here to handle the paperwork and ensure your transition is seamless and stress-free. You deserve the peace of mind that comes with knowing you have the right coverage at the right price. We are ready to help you start this journey toward a more certain future today.

Compare 2026 Medigap Rates with a Trusted Advisor

Frequently Asked Questions

Is there a federal Medigap birthday rule for all states?

No, there is no federal law that requires a Medigap birthday rule. These protections are managed entirely at the state level. While we hope more states adopt these rules in the future, only a specific number of medigap birthday rule states currently offer this annual right. Federal law only guarantees you a window to buy a plan without health questions when you first enroll in Medicare Part B.

Can I switch from Medicare Advantage to Medigap using the birthday rule?

No, the birthday rule is only for people who already have a Medigap policy and want to move to a different one. If you are currently in a Medicare Advantage plan, you usually have to wait for the Annual Enrollment Period to leave your plan. You would also likely need to pass a health exam to get a Medigap policy unless you have a separate legal right to join.

What happens if I miss my 60-day birthday window?

If you miss the window in your state, you lose your guaranteed right to switch without medical questions until your next birthday. You can still apply for a new plan at any time during the year, but the insurance company will review your medical history. They could charge you more or even deny your application based on your health. We suggest setting a reminder so you don’t miss out.

Do I have to answer health questions if I live in a birthday rule state?

No, you do not have to answer medical underwriting questions if you switch during the approved window in one of the medigap birthday rule states. The law requires insurance companies to accept your application regardless of your health history. This is a vital protection for your retirement because it allows you to move to a plan with a lower monthly premium even if you have developed new health conditions.

Which state has the most flexible Medigap switching rules in 2026?

California and Nevada are among the most flexible because they offer a full 60-day window and allow you to switch to any insurance carrier in the state. While New York and Connecticut allow switching all year round, they don’t follow a traditional birthday schedule. Some other states are more restrictive and only let you switch to a different plan offered by your current insurance company, which limits your savings.

If I switch Medigap plans, will I have to change my doctors?

No, switching your plan will not force you to find new doctors. Medigap plans do not use provider networks like Medicare Advantage plans do. You have the freedom to see any doctor in the country who accepts Original Medicare. The insurance company simply pays the portion of the bill that Medicare doesn’t cover. Your access to care remains exactly the same even if you change your insurance carrier.

Can I use the birthday rule to switch to a Plan G if I have Plan N?

Generally, you cannot use this rule to move from Plan N to Plan G. Most states only allow you to switch to a plan with equal or lesser benefits. Because Plan G covers the Part B excess charges and Plan N does not, Plan G is considered a higher level of coverage. You would usually have to answer health questions to make that specific move, though we can help you check.

Does the birthday rule apply to Medicare Part D drug plans?

No, the birthday rule only applies to your Medicare Supplement insurance. Your Medicare Part D prescription drug plan has its own enrollment period that runs from October 15 to December 7 every year. We can help you review your drug coverage during that fall window to ensure your medications are covered at the lowest price. The birthday rule won’t help you change your drug plan or your dental coverage.