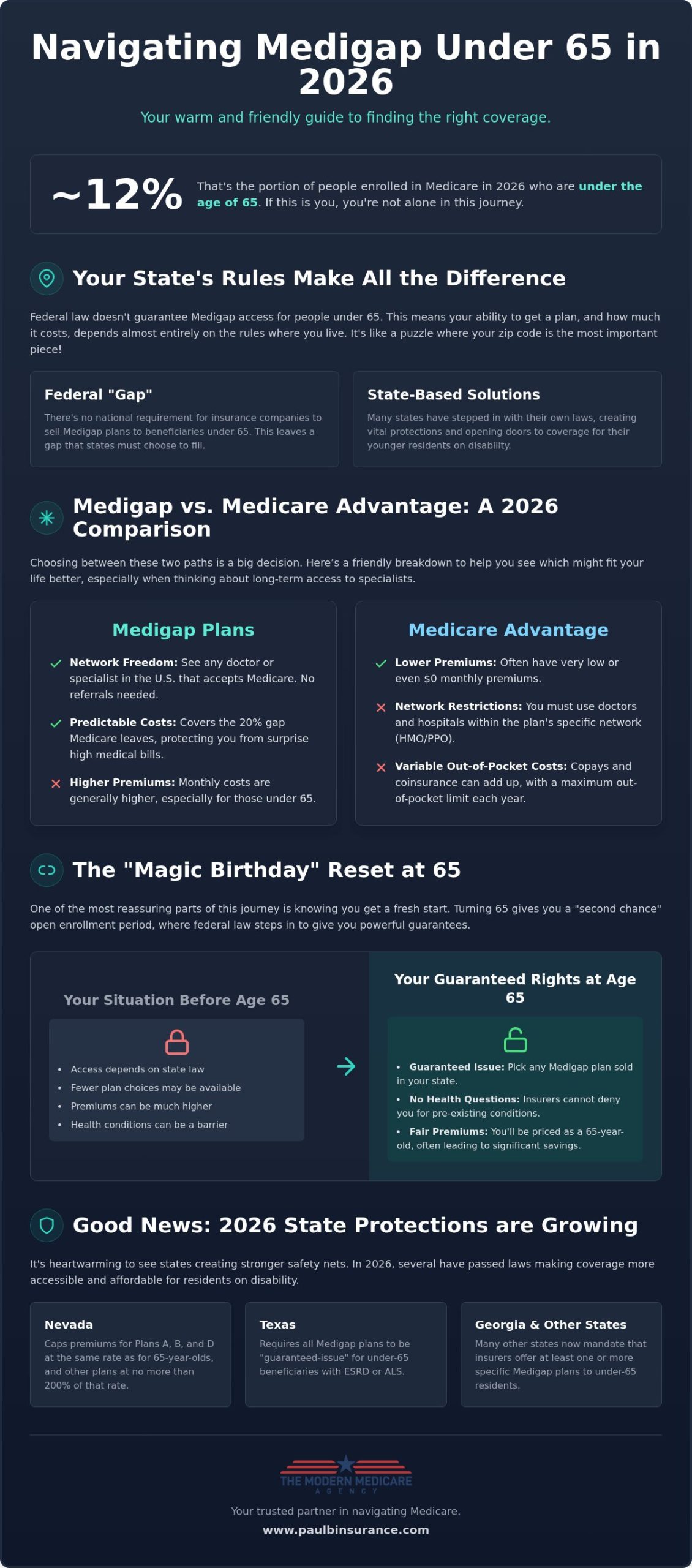

Did you know that nearly 12% of people enrolled in Medicare in 2026 are actually under the age of 65? If you’re one of them, you’ve likely discovered that finding medigap plans for people under 65 feels like trying to solve a puzzle where the pieces change depending on where you live. It’s completely normal to feel stressed by higher premiums or the fear that a pre-existing condition might keep you from getting the protection you need.

I understand how confusing this process is when federal laws don’t offer the same guarantees for everyone. You deserve a clear path to the coverage that fits your life and provides real peace of mind. This guide will walk you through your state’s specific rules and compare Medigap with Medicare Advantage so you can make a choice with confidence. We’ll also look at the “second chance” window you’ll get at age 65, ensuring you have a reliable plan for both today and your future.

Key Takeaways

- Understand why your state’s specific laws determine your access to medigap plans for people under 65, as federal rules don’t provide a universal guarantee.

- Compare the long term value of Medigap’s network freedom against the lower monthly costs of Medicare Advantage to protect your access to specialists.

- Learn about the “magic birthday” reset that gives you a guaranteed right to any plan at age 65, regardless of your current health or pre-existing conditions.

- Discover how new 2026 state protections are capping premiums and expanding enrollment windows to make coverage more accessible for those on disability.

- See how an independent broker can map out options from over 40 carriers to find the specific companies that welcome under-65 applicants in your zip code.

Can You Get a Medigap Plan If You Are Under 65?

The short answer is yes, but the path to getting there isn’t always a straight line. While federal law provides a clear safety net for those turning 65, it doesn’t offer that same universal guarantee to younger beneficiaries. This creates a “federal gap” that leaves many people feeling overlooked by the system. If you’ve qualified for Medicare early due to a disability, your ability to buy a plan depends almost entirely on the laws of your specific state. You aren’t alone in this frustration. In 2026, nearly 12% of all Medicare enrollees are under the age of 65. Many of them are asking these exact same questions while trying to find security in a complex market.

It’s okay to feel overwhelmed by the conflicting information you find online. Finding medigap plans for people under 65 is a journey that requires both patience and the right map. My goal is to act as your guide, removing the anxiety from this process and helping you see the options available in your backyard. We’ll look at how your eligibility works and why your location changes everything.

The Difference Between Federal and State Medigap Rights

Your zip code is the most important factor in your search for coverage. Because there’s no national requirement, each state writes its own rules for Medigap policies for people under 65. Some states require insurance companies to offer every plan they sell to everyone, while others only require one or two specific options. When you hear the term “Guaranteed Issue,” it means a company cannot turn you down or charge you more because of your health history. Think of Medigap as a financial bridge that covers the 20% gap left by Original Medicare, protecting you from high medical bills that could otherwise be devastating. You can explore how these Medicare Supplement (Medigap) plans work to see which bridge is right for you.

Qualifying for Medicare Before Age 65

Most people enter this system through Social Security Disability Insurance (SSDI). It’s often a long road. Usually, you must receive SSDI benefits for a full 24 months before your Medicare coverage actually begins. However, 2026 rules continue to provide faster access for specific conditions. If you have Amyotrophic Lateral Sclerosis (ALS), your Medicare starts the very same month your disability benefits begin. For those with End-Stage Renal Disease (ESRD), eligibility usually starts on the first day of the fourth month of dialysis treatments. Checking your 2026 status is as simple as reviewing your Social Security statement or speaking with an expert who understands the timeline. Understanding when your coverage starts is the first step toward finding medigap plans for people under 65 that provide the peace of mind you deserve.

State Rules for Under-65 Medigap: Where Do You Stand?

Since Federal law doesn’t require insurance companies to offer medigap plans for people under 65, your home state becomes the architect of your health coverage. This creates a patchwork of rules that change the moment you cross state lines. It can feel deeply frustrating to find out that a plan available to your neighbor in another state is off-limits to you. However, many states have stepped up to fill this gap, creating protections that ensure you aren’t left without options. Your journey to finding coverage starts with understanding the “map” of your specific state.

In 2026, the way companies set your price is just as important as the plan itself. You’ll often hear about “Community-rated” states where everyone pays the same premium regardless of age. Other states use “Issue-age” rating, where your cost is based on how old you are when you first sign up. Some states only require insurers to offer Plan A to younger residents. While Plan A is the most basic option, it still provides a vital layer of security against the high costs of hospital stays and outpatient care. It’s about finding the best available safety net for your situation.

States with Strong Consumer Protections

There is good news for residents in states like Nevada and Georgia. As of 2026, Nevada has implemented caps on premiums for Plans A, B, and D, ensuring they stay at the same rate as those for 65-year-olds. Other plans are capped at no more than 200% of that rate. Texas has also enacted legislation requiring all plans to be guaranteed-issue for those with ESRD or ALS. If you live in one of these protective states, you can often find comprehensive Medicare Supplement Insurance without the fear of being priced out. I can help you compare these state-specific plans to see which carriers are offering the best value this year.

What to Do If Your State Has Limited Options

If you live in a state with fewer mandates, don’t lose hope. Some states maintain high-risk pools or “shadow” markets where coverage is available but rarely advertised on big websites. You might also find that specific carriers choose to offer medigap plans for people under 65 even when the law doesn’t force them to. Legislative changes move quickly. For instance, states like Michigan and Ohio have seen bills introduced recently that aim to expand these rights. Staying informed about these 2026 updates is key. If you’re feeling stuck, reaching out to an independent expert can help you uncover these hidden paths to coverage.

Medigap vs. Medicare Advantage for People Under 65

The choice between Medigap and Medicare Advantage is often the most important financial decision you’ll make this year. It’s a balance between how much you want to pay every month and how much freedom you need when choosing your doctors. While medigap plans for people under 65 can come with higher monthly premiums, they offer a level of certainty that many find worth the cost. On the other hand, Medicare Advantage Plans often start with lower monthly costs, but they usually require you to stay within a specific network of providers. This “pay now” versus “pay later” trade-off is the heart of the decision.

Don’t forget about your prescriptions during this comparison. Medigap plans do not include drug coverage, so you’ll need to enroll in a separate Medicare Part D plan to ensure your medications are covered. Advantage plans typically bundle this coverage together. If you prefer knowing exactly what your medical bills will look like each month, the Medigap route is usually the winner. If you’re looking for a budget-friendly alternative and don’t mind staying within a network, Advantage might be your best fit.

Why Network Access Matters for Chronic Conditions

If you’re managing a complex health condition, seeing the right specialist isn’t just a preference; it’s a necessity. With Medigap, you can see any doctor in the country who accepts Medicare. This is a huge relief compared to HMO or PPO plans that might limit you to a local group or require a referral for every visit. Because state rules for under-65 Medigap vary so much, checking if your specific specialists are in-network is vital for your 2026 planning. Medigap Plan G is the gold standard for predictability because it covers almost every gap in Original Medicare once your deductible is met.

The 2026 Financial Picture: Deductibles and Caps

Money is always a major part of the conversation. In 2026, the Part B deductible is projected to be approximately $283. If you choose Medigap, that’s often the only major out-of-pocket cost you’ll face for covered services all year. Medicare Advantage works differently. While you might pay $0 in premiums, you’ll pay copays as you go. These plans have a maximum out-of-pocket limit to protect you from financial disaster, but you still have to budget for those individual doctor visits. Choosing medigap plans for people under 65 means you’re essentially pre-paying your medical expenses to avoid surprises later.

The “Turning 65” Reset: Your Second Chance at Medigap

If you’ve been managing your health with medigap plans for people under 65, you know that the costs can sometimes feel like a heavy weight. But there is a bright light on the horizon. Turning 65 is what we call a “magic birthday” in the Medicare world. It doesn’t matter if you’ve been on Medicare for years due to a disability; the moment you hit 65, the clock resets. You get a brand-new, six-month Medigap Open Enrollment Period. This is your second chance to secure the coverage you’ve always wanted without the stress of medical underwriting. It’s a moment where the system finally works in your favor, giving you the same rights as someone who is just joining Medicare for the first time.

During this window, your health history is essentially wiped clean in the eyes of insurance companies. They can’t look at your pre-existing conditions, your medications, or your past hospital visits to deny you coverage or charge you more. It’s a powerful moment of empowerment that lets you move from a state of uncertainty to one of total protection. For many of my clients, this feels like a fresh start. You can finally choose the plan that offers the best security for your 2026 healthcare needs without worrying about your medical records holding you back.

Lowering Your Premiums at Age 65

One of the biggest reliefs is the change in your monthly budget. In many states, medigap plans for people under 65 are priced much higher than plans for those over 65. When you reach this milestone, you move into the senior-rated pool, which often leads to significantly lower premiums. You can switch to a more comprehensive plan, like Plan G, without a medical exam. I recommend starting your application process about three to six months before your 65th birthday. This proactive approach ensures a seamless transition and gives you plenty of time to compare the 2026 rates from different carriers.

A Checklist for Your 65th Birthday Transition

This transition is the perfect time to evaluate if your current coverage still meets your needs. If you’ve been using a Medicare Advantage plan because Medigap was too expensive, this is your golden opportunity to switch back to a Supplement plan.

- Review your current specialist list to ensure they accept Original Medicare.

- Compare the latest 2026 rates for Plan G and Plan N.

- Check your Part D prescription coverage to see if a new plan offers better savings.

- Confirm your enrollment dates to avoid any gaps in your protection.

You can view our full Medigap plan comparison to see which options will be available to you when you hit that 65-year milestone. If you’re approaching this big day, schedule a time to review your 2026 options so we can make the most of your second chance.

How an Independent Broker Simplifies Your 2026 Search

Searching for medigap plans for people under 65 can feel like you’re trying to find a path through a dense fog. You’ve already seen how state rules change and how premiums can vary wildly. This is where the value of an independent broker becomes clear. Unlike a “captive agent” who only works for one specific insurance company, an independent broker like Paul Barrett works directly for you. We aren’t restricted to a single list of products. Instead, we have the freedom to look at the entire market to find the coverage that actually fits your life.

In 2026, our agency compares options from over 40 different insurance carriers. This is vital for younger beneficiaries because not every company is eager to accept applicants under age 65. We know which carriers are “under-65 friendly” in your specific state and which ones offer the most stable rates over time. Our goal is to move you from a state of distress to a state of absolute certainty. We provide this expert support year-round, not just during your initial enrollment. If you have questions about a bill or a change in your 2026 benefits, we are just a phone call away.

You might wonder how much this personalized service costs. The answer is simple: our services are completely free to you. We are compensated by the insurance companies, but our loyalty remains with you, the client. This model allows us to act as your unbiased guide, focusing solely on your health needs and budget rather than a sales quota. It’s a partnership built on trust and reliability.

Removing the Stress from the Application Process

The paperwork involved in a Medigap application can be daunting, especially when you’re already managing a health condition. We handle the heavy lifting for you. From gathering the necessary documents to communicating directly with the insurance carriers, we ensure every detail is correct. We know which companies in 2026 have the most efficient approval processes for younger applicants. We are your advocate, not the insurance company’s. This means we fight to get you the best possible outcome while you focus on your health and your family.

Taking the First Step Toward Certainty

Taking that first step doesn’t have to be scary. When you reach out to a Medicare Broker, you can expect a calm, pressure-free conversation. We start by listening to your story and understanding your specific medical needs. From there, we provide a personalized quote that shows you exactly what medigap plans for people under 65 are available in your zip code. There are no high-pressure tactics or rush to sign. We simply provide the clarity you need to make an informed choice. We help you find the right path, one step at a time, ensuring you feel protected and empowered as you move forward into 2026.

Secure the Protection You Deserve Today

Finding the right coverage shouldn’t feel like a solo mission through a confusing system. You’ve seen how state laws, network choices, and the “turning 65” reset all play a role in your healthcare journey. Whether you’re currently facing high premiums or worry about how your health history impacts your options, there is a clear path forward. My mission is to help you move from a state of worry to one of absolute certainty by providing the simple clarity you’ve been looking for.

Finding medigap plans for people under 65 is a unique challenge, but you don’t have to solve it alone. As an independent broker licensed in 34+ states, I can compare 40+ carriers instantly to find the best fit for your specific zip code and medical needs. This expert, unbiased guidance is always provided at no cost to you. You deserve a dedicated advocate who prioritizes your health and peace of mind over an insurance company’s bottom line.

Let Paul Barrett find the right under-65 plan for you—Get your free comparison today.

You’ve already taken the most important step by educating yourself on your 2026 options. Now, let’s work together to find the reliable protection and comfort you and your family deserve.

Frequently Asked Questions

Is Medigap available for people under 65 in all states?

No, medigap plans for people under 65 are not available in every state. While the majority of states have created rules to help, three states currently have no provisions for younger beneficiaries. Your ability to buy a plan depends entirely on where you live. This is why it’s so important to check your specific state’s 2026 regulations before you start your search.

Why are Medigap premiums so much higher for people under 65?

Premiums are often higher because insurers view younger beneficiaries on disability as having higher medical risks. Without federal laws to cap these costs, many states allow companies to charge more for medigap plans for people under 65 compared to those over 65. This can be a shock, but remember that these rates often drop significantly once you reach your 65th birthday and enter the senior-rated pool.

Can an insurance company deny me Medigap if I have a disability?

Yes, they can deny you in states that don’t have “Guaranteed Issue” protections for younger residents. In these areas, companies use medical underwriting to look at your health history before deciding to cover you. However, many states now require insurers to offer at least one plan regardless of your condition. It’s a patchwork of rules that an independent broker can help you navigate easily.

What happens to my Medigap plan when I turn 65?

When you turn 65, you get a fresh start with your coverage. You’ll enter a new six-month window where you can buy any Medigap policy at a lower senior rate. Your health history is ignored during this time, allowing you to switch plans without a medical exam. This “reset” is a golden opportunity to lower your monthly costs while keeping the high-quality protection you need.

Do I need a separate Part D plan if I have Medigap under 65?

Yes, you will need a standalone Part D plan to cover your medications. Medigap plans only cover the “gaps” in medical and hospital costs, such as copays and coinsurance. Adding a Part D plan ensures you won’t face late enrollment penalties later on. It also protects you from high out-of-pocket drug costs that Original Medicare and Medigap don’t cover on their own.

Is Medicare Advantage a better option than Medigap for disabled individuals?

It depends on your priorities and medical needs. Medicare Advantage often has lower monthly costs, but Medigap offers total network freedom. For many people managing a disability, being able to see any specialist who accepts Medicare is worth the higher Medigap premium. If you prefer fixed monthly costs and no network restrictions, Medigap is usually the more reliable choice for long term care.

What is the best Medigap plan for someone under 65 in 2026?

Plan G is widely seen as the most comprehensive choice for 2026. It covers nearly every out-of-pocket cost except for the Part B deductible. However, since some states only require insurers to offer Plan A to younger residents, the “best” plan is often the one that provides the most protection within your state’s specific limits. We can help you compare what’s actually available in your area.

How much is the Medicare Part B deductible in 2026?

The Medicare Part B deductible is projected to be approximately $283 in 2026. You’ll need to pay this amount once per year for outpatient services before your Medigap plan or Original Medicare starts to pay. Knowing this specific number helps you budget for your healthcare. It’s one of the few out-of-pocket costs you’ll have if you choose a comprehensive supplement plan like Plan G or Plan N.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com